Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

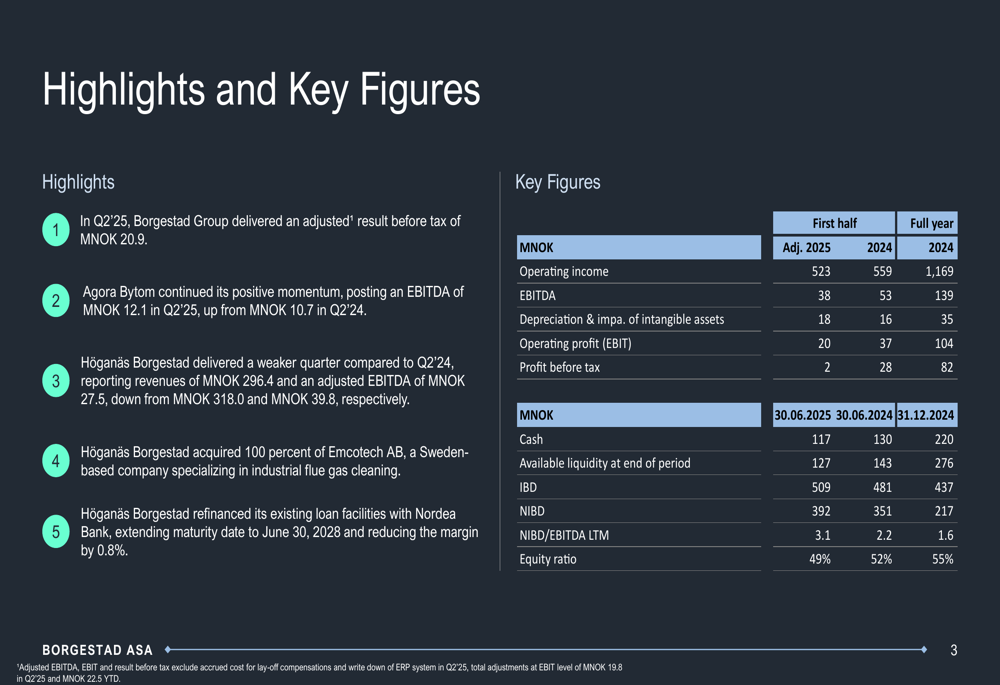

Borgestad ASA (OB:BOR) presented its Q2 2025 results on August 21, 2025, revealing a mixed performance across its business segments. The industrial investment company, which focuses on real estate and refractory industries, reported an adjusted result before tax of MNOK 20.9 for the quarter, down from MNOK 32.7 in Q2 2024. The company’s stock has recently experienced volatility, closing at NOK 20 on August 20, 2025, representing a 0.99% decline.

The presentation comes after a challenging first quarter, when Borgestad reported an 8.8% revenue decline and negative adjusted EBIT, as mentioned in previous earnings reports. While Q2 showed some sequential improvement, year-over-year comparisons remained challenging, particularly in the company’s refractory business.

Quarterly Performance Highlights

Borgestad’s Q2 2025 results showed divergent performance between its two main business segments. The company reported operating income of MNOK 523 for Q2 2025, down from MNOK 559 in Q2 2024, while EBITDA declined to MNOK 38 from MNOK 53 in the same period last year.

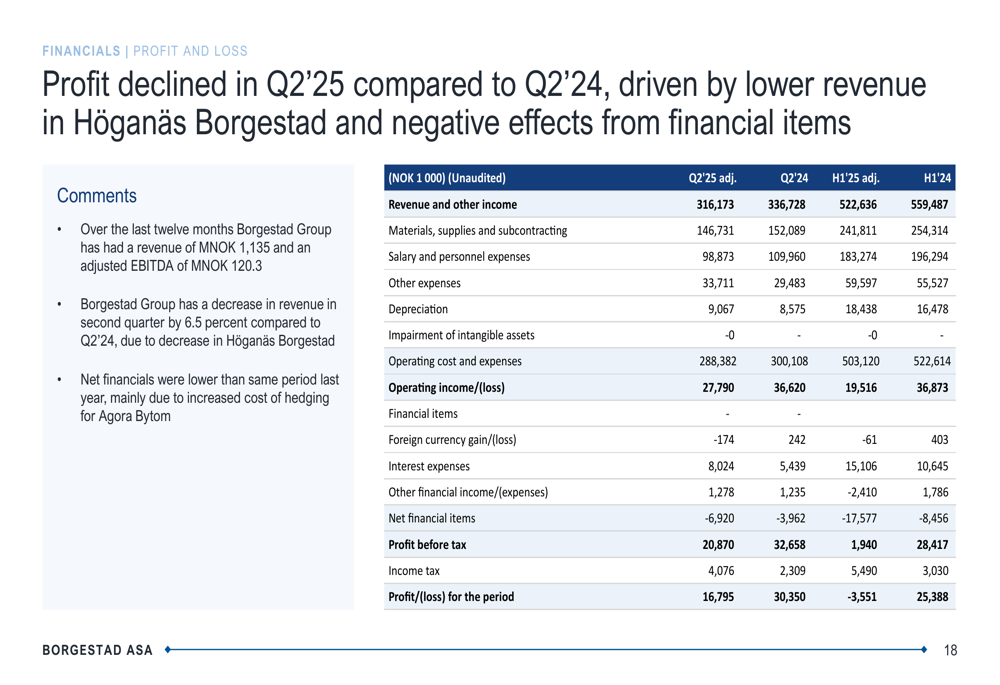

As shown in the following financial highlights slide, profit before tax declined significantly to MNOK 2 from MNOK 28 in Q2 2024, while the company’s net interest-bearing debt to EBITDA ratio increased to 3.1x from 2.2x a year earlier:

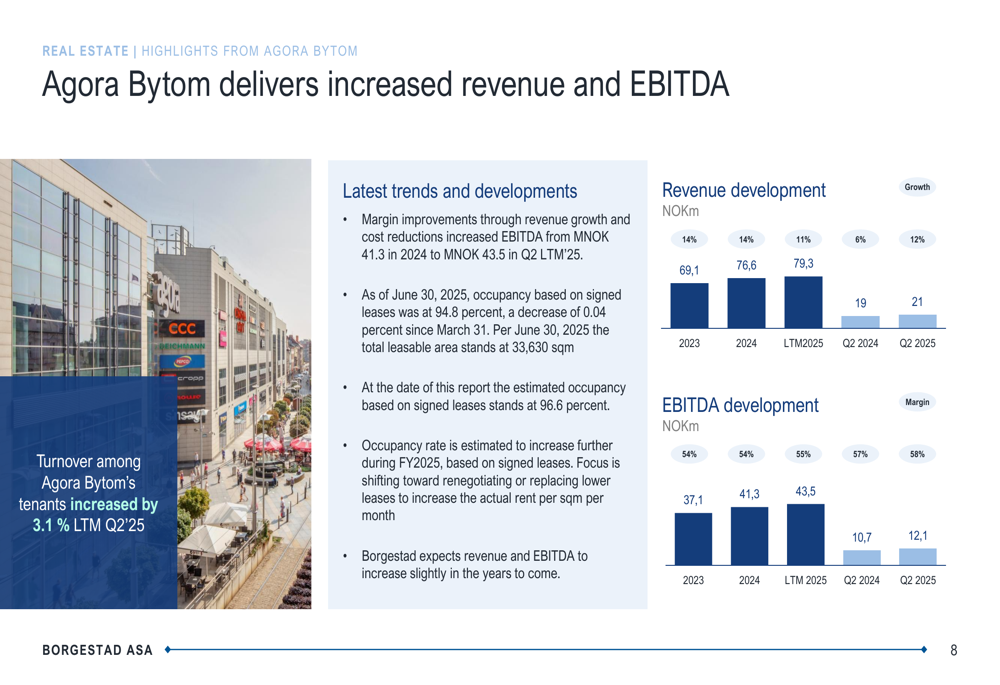

The real estate segment, represented by the Agora Bytom shopping center in Poland, continued its positive momentum with EBITDA of MNOK 12.1 in Q2 2025, up from MNOK 10.7 in Q2 2024. The improved performance was driven by both revenue growth and cost reductions.

As illustrated in the following chart, Agora Bytom’s revenue and EBITDA have shown consistent growth:

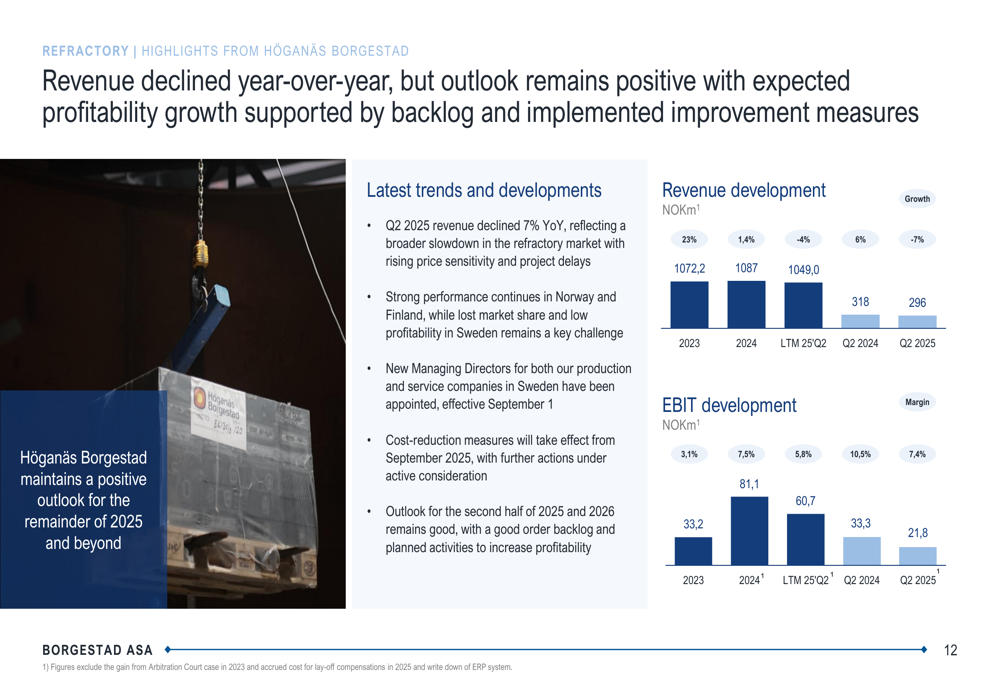

In contrast, the refractory business under Höganäs Borgestad delivered weaker results, with revenues of MNOK 296.4 and adjusted EBITDA of MNOK 27.5 in Q2 2025, down from MNOK 318.0 and MNOK 39.8, respectively, in Q2 2024. This represents a 7% year-over-year revenue decline, reflecting broader challenges in the refractory market.

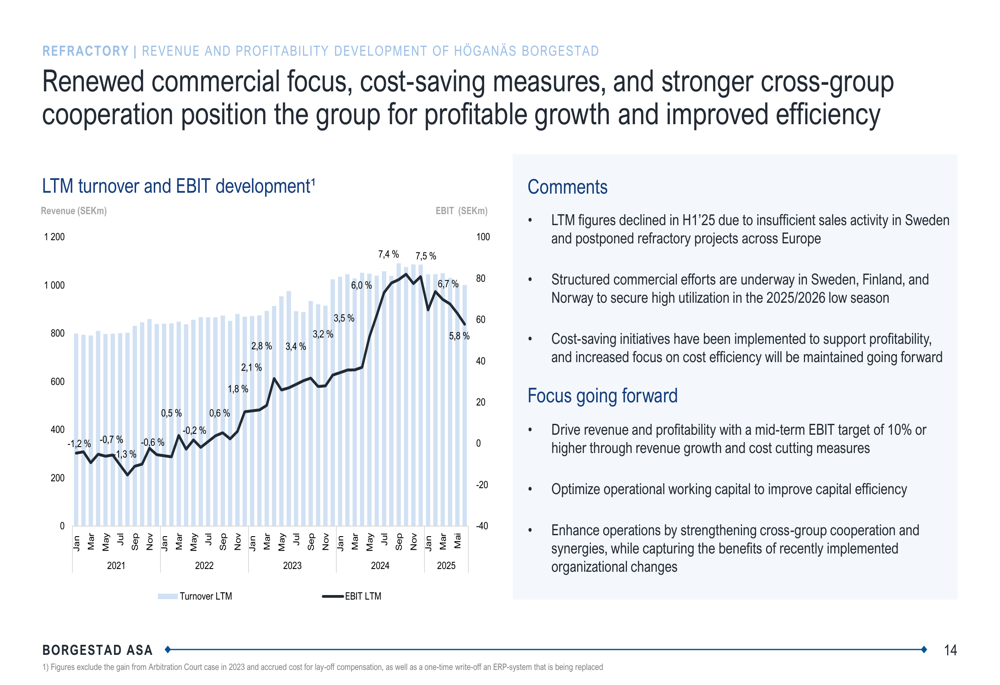

The following slide illustrates the revenue and EBIT development for Höganäs Borgestad:

Strategic Initiatives

Despite challenging market conditions, Borgestad has undertaken several strategic initiatives to strengthen its business. On June 17, 2025, Höganäs Borgestad announced the acquisition of 100% of Emcotech AB, a Swedish company specializing in industrial flue gas cleaning. Emcotech generated MSEK 45.4 in revenue and MSEK 6.4 in EBITDA in 2024.

The acquisition, which strengthens the group’s industrial filter offering, was financed through Nordea loan commitments, including a MSEK 9 mortgage facility and a MSEK 10 overdraft facility. The purchase price included MSEK 10.5 at closing, plus a performance-based earn-out of up to MSEK 10.

Additionally, Höganäs Borgestad successfully refinanced its existing loan facilities with Nordea Bank, extending the maturity date to June 30, 2028, and reducing the margin by 0.8%. This refinancing was previously mentioned as a planned action in earlier earnings reports and represents an important step in improving the company’s financial flexibility.

The company also outlined its strategy and key tools for future growth, as shown in the following slide:

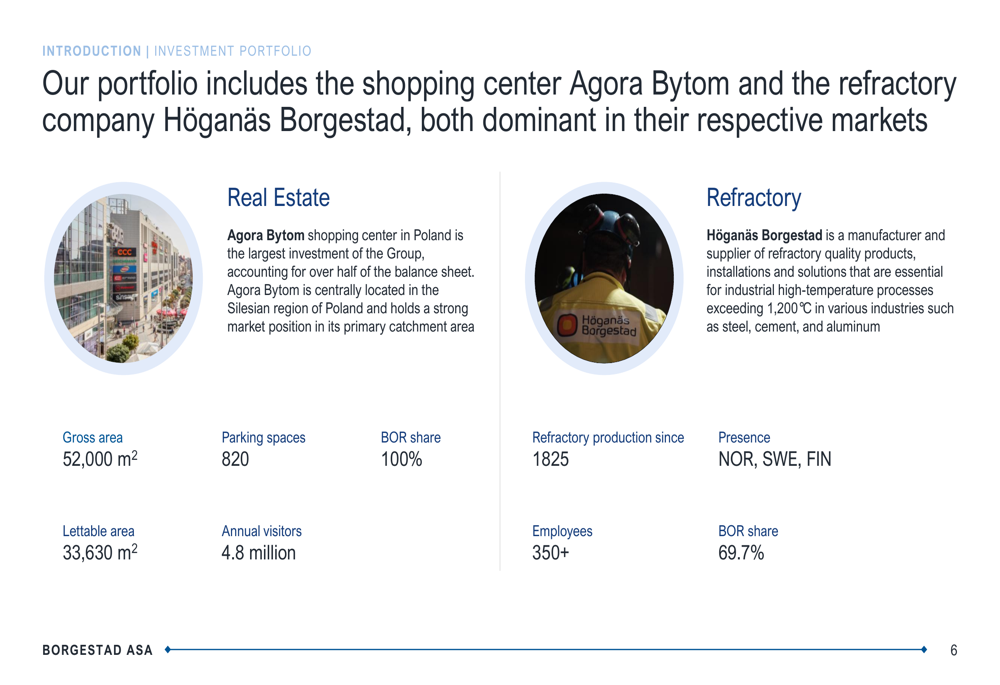

Borgestad’s investment portfolio continues to be focused on two main segments: real estate (Agora Bytom) and refractory (Höganäs Borgestad), as illustrated in the following overview:

Detailed Financial Analysis

A closer examination of Borgestad’s financial statements reveals several important trends. The profit and loss statement shows that while revenue declined, the company also managed to reduce salary and personnel expenses to MNOK 98.9 in Q2 2025 from MNOK 110.0 in Q2 2024.

The following profit and loss statement provides a comprehensive view of the company’s financial performance:

The company’s cash flow and liquidity position has weakened, with cash and cash equivalents decreasing to MNOK 117.0 as of June 30, 2025, from MNOK 130.3 a year earlier and MNOK 220.5 at the end of 2024. This decline was driven by negative cash flow from operations, investments, and financing activities.

Working capital increased ahead of the high season, particularly in the refractory business, which typically experiences peak demand in Q3. This seasonal pattern is a characteristic feature of the Nordic refractory market, as illustrated in the company’s presentation.

The company’s revenue and profitability development over time shows the challenges faced by Höganäs Borgestad, with declining LTM figures in H1 2025 due to insufficient sales activity in Sweden and postponed refractory projects across Europe:

Forward-Looking Statements

Looking ahead, Borgestad remains cautiously optimistic about its prospects for the remainder of 2025 and beyond. For Agora Bytom, the company expects revenue and EBITDA to increase slightly in the coming years, with a focus on renegotiating or replacing lower leases to increase the actual rent per square meter per month.

The occupancy rate at Agora Bytom based on signed leases was 94.8% as of June 30, 2025, with an estimated increase to 96.6% at the time of the report. The company expects this rate to increase further during FY2025.

For Höganäs Borgestad, the company is implementing cost-reduction measures that will take effect from September 2025, with further actions under active consideration. New Managing Directors for both production and service companies in Sweden have been appointed, effective September 1, to address the challenges in the Swedish market.

The outlook for the second half of 2025 and 2026 remains positive for the refractory business, with a good order backlog and planned activities to increase profitability. The company has set a mid-term EBIT target of 10% or higher through revenue growth and cost-cutting measures.

As outlined in the following slide, Borgestad’s priorities include operational improvements, capital efficiency, and cash flow gains for Höganäs Borgestad, while also exploring strategic M&A opportunities:

In conclusion, while Borgestad faces challenges in its refractory business, particularly in Sweden, the company’s real estate segment continues to perform well. Strategic initiatives such as the Emcotech acquisition and debt refinancing, combined with cost-cutting measures and management changes, position the company to address current challenges and potentially improve performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.