Apple announces iPhone 17 with 48MP cameras and 6.3-inch display

Introduction & Market Context

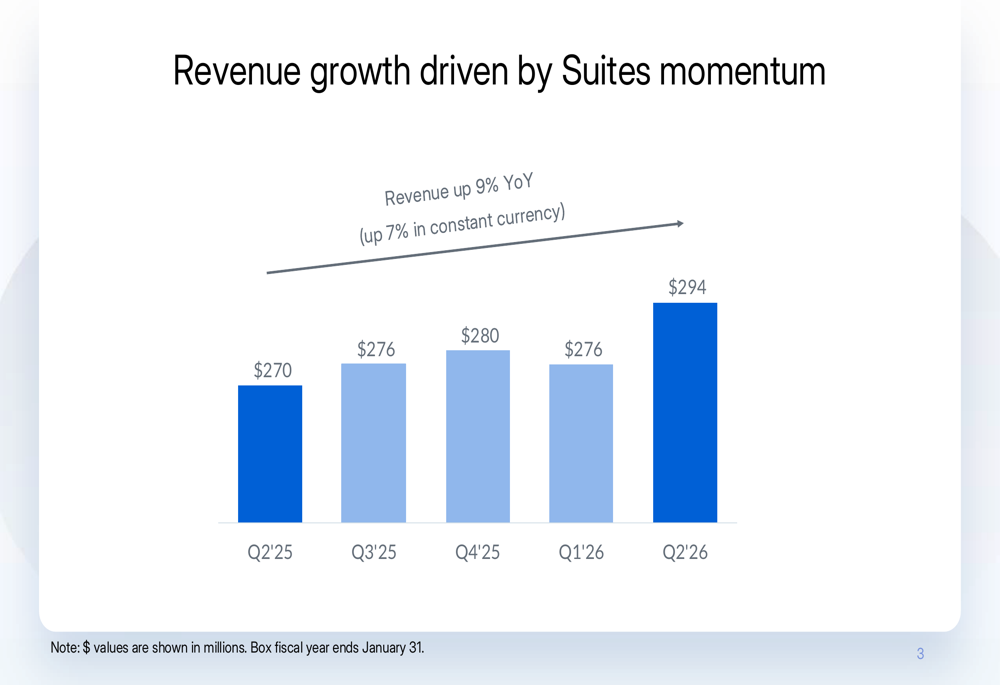

Box Inc (NYSE:BOX) released its second quarter fiscal 2026 financial results on August 26, 2025, showing accelerated revenue growth and improved profitability metrics. The content management platform provider reported revenue of $294 million, representing a 9% year-over-year increase, a significant improvement from the 4% growth reported in the previous quarter.

In after-hours trading, Box shares edged up 0.1% to $31.45, following a 0.83% decline during the regular trading session. The stock has traded between $28.00 and $38.80 over the past 52 weeks.

Quarterly Performance Highlights

Box’s Q2 FY26 revenue growth was driven by continued momentum in its Suites offerings, particularly its AI-powered content management solutions. The company reported revenue of $294 million, up 9% year-over-year, or 7% in constant currency.

As shown in the following chart of quarterly revenue growth:

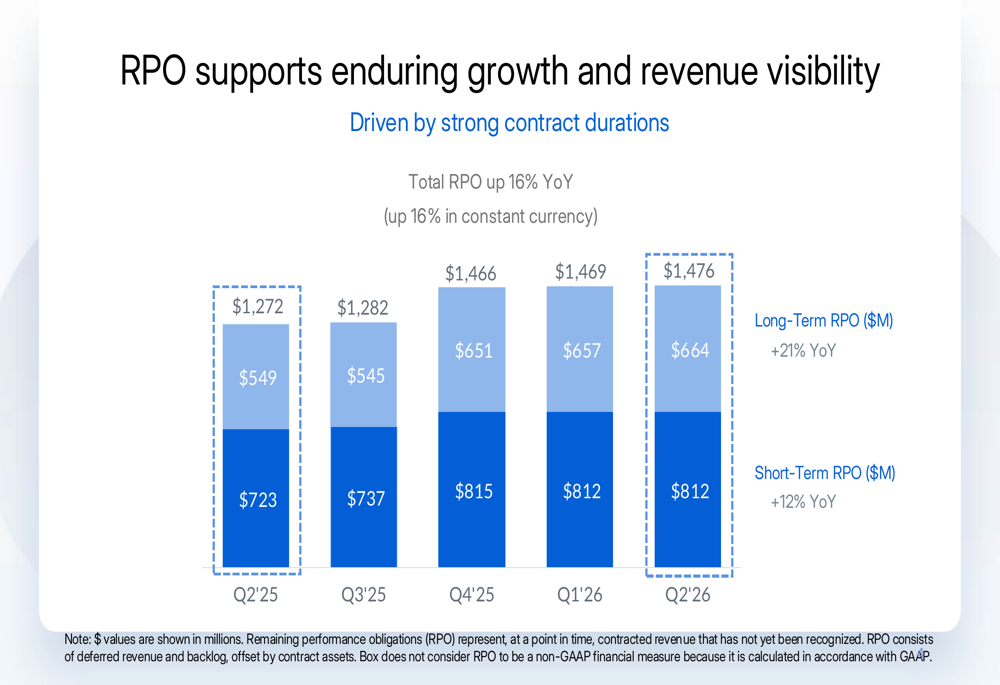

The company’s Remaining Performance Obligation (RPO), which consists of deferred revenue and backlog, reached $1.48 billion, up 16% year-over-year. This metric provides strong visibility into future revenue streams, with short-term RPO at $812 million (up 12% YoY) and long-term RPO at $664 million (up 21% YoY).

The following chart illustrates Box’s RPO growth over the past five quarters:

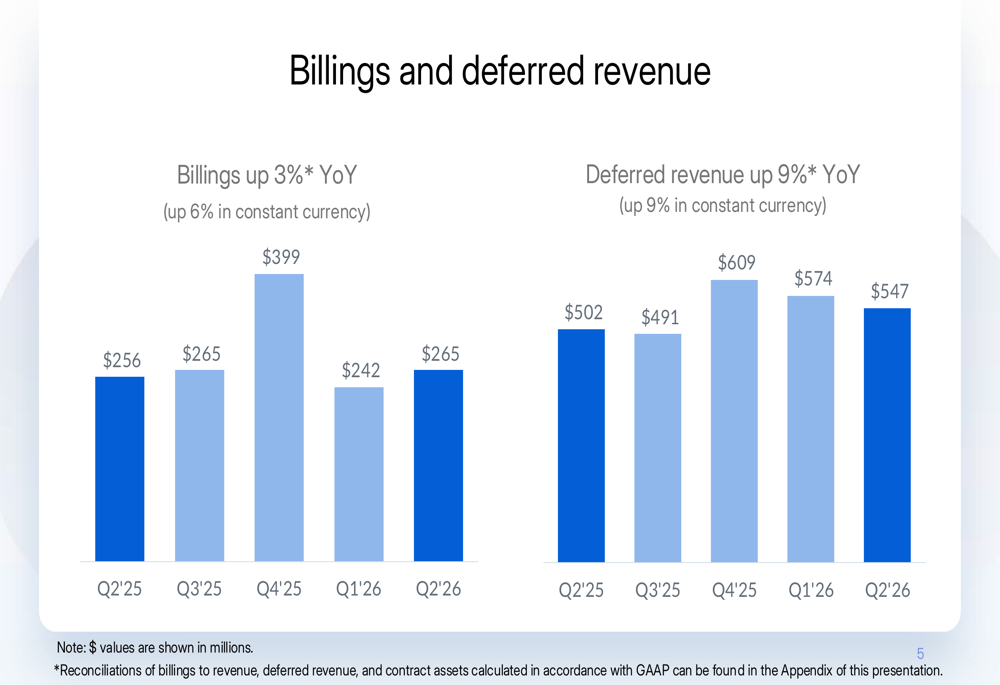

Box reported billings of $265 million, up 3% year-over-year (6% in constant currency), while deferred revenue increased 9% to $547 million. This represents a slowdown from the 27% billings growth reported in Q1, though the company maintains strong revenue visibility through its subscription model.

The billings and deferred revenue trends are shown in the following charts:

Profitability and Margin Performance

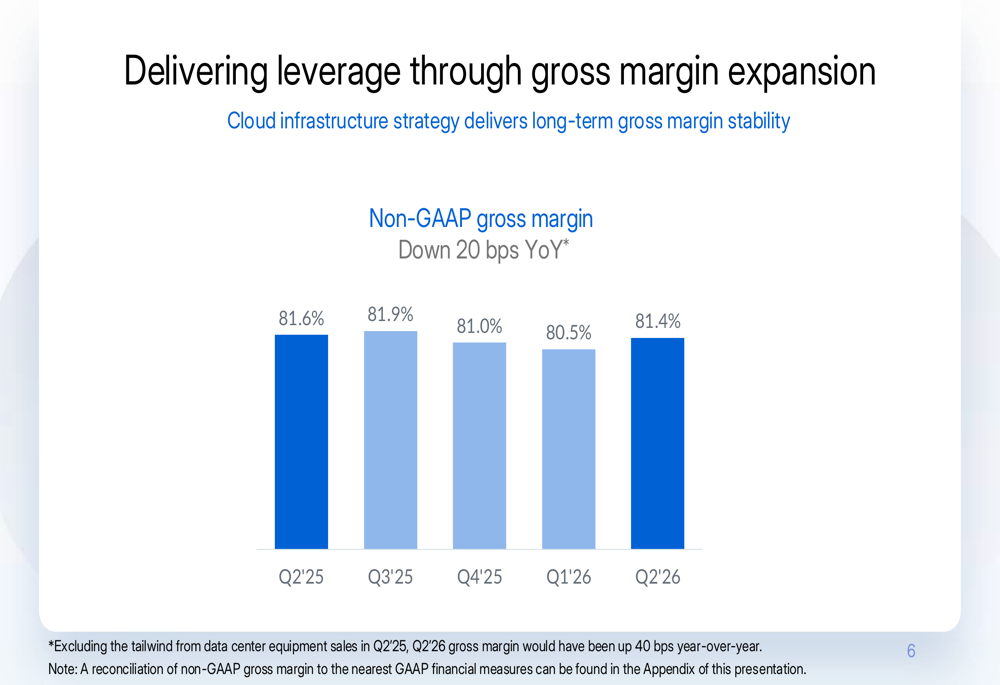

Box continues to demonstrate strong profitability metrics. The company reported a non-GAAP gross margin of 81.4% for Q2 FY26, down slightly from 81.6% in the same quarter last year. However, the company noted that excluding the tailwind from data center equipment sales in Q2’25, the gross margin would have improved by 40 basis points year-over-year.

The gross margin trend is illustrated in the following chart:

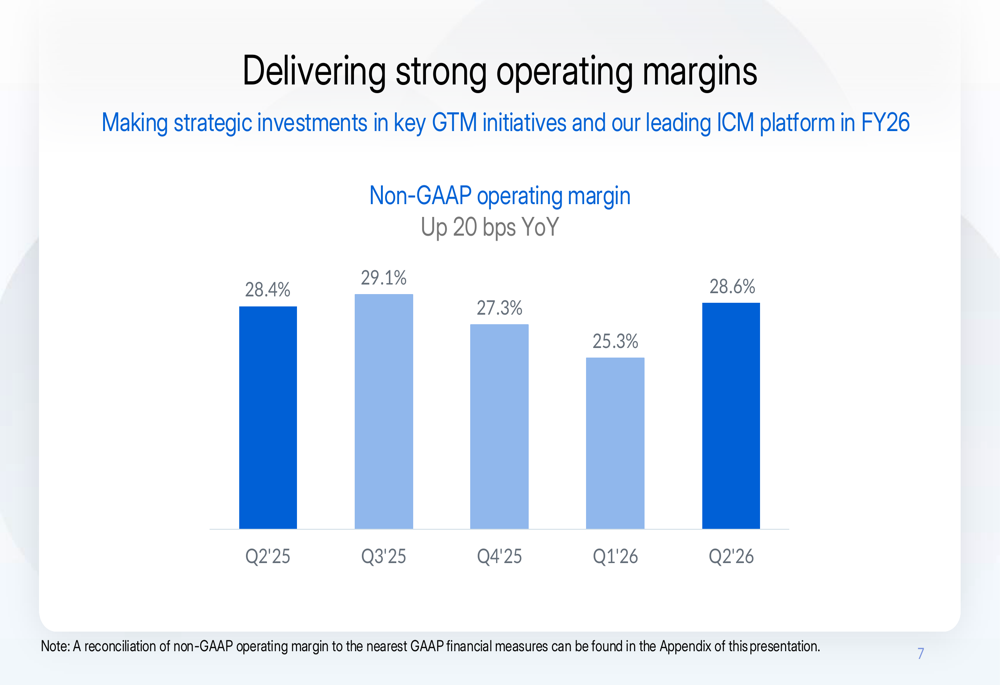

Non-GAAP operating margin improved to 28.6%, up 20 basis points from 28.4% in Q2 FY25. This improvement reflects Box’s ability to drive operational efficiency while continuing to invest in growth initiatives, particularly in go-to-market strategies and its Intelligent Content Management platform.

The operating margin performance is shown in the following chart:

Strategic Initiatives

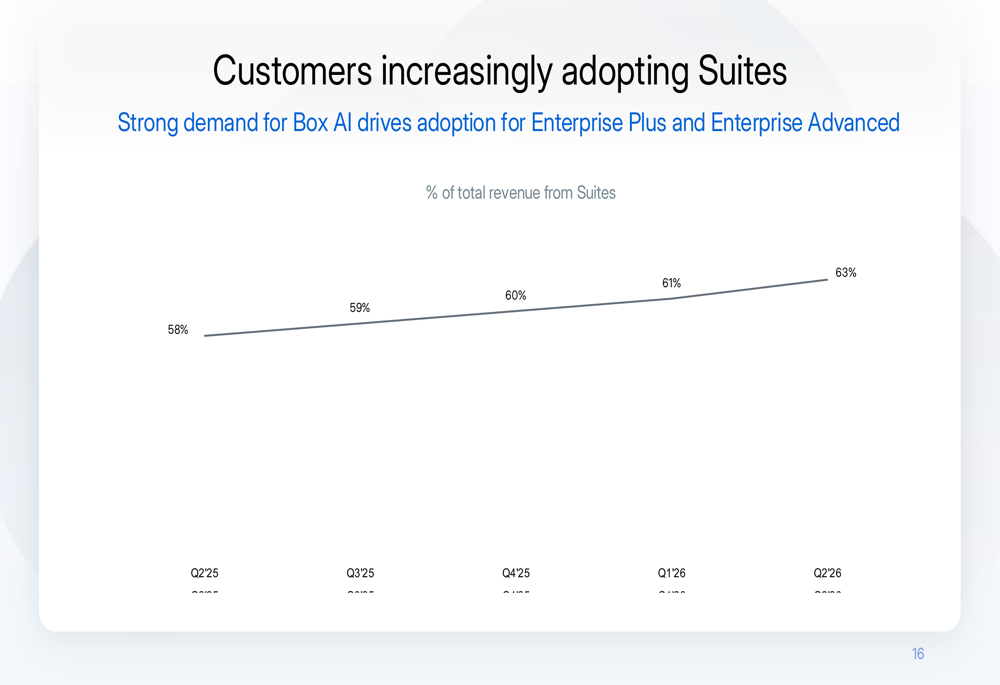

Box’s strategic focus on driving adoption of its Suites offerings continues to yield positive results. Revenue from Suites reached 63% of total revenue in Q2 FY26, up from 58% in the same quarter last year, demonstrating strong customer adoption of Box’s expanded product portfolio.

The following chart shows the steady increase in Suites adoption:

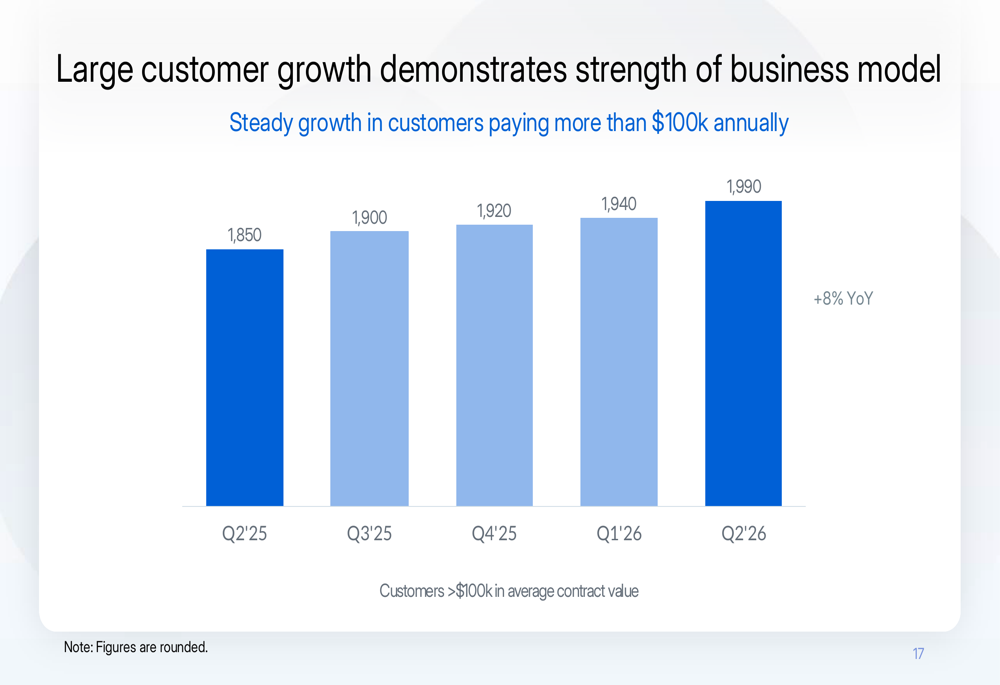

The company also reported strong growth in large customers, with 1,990 customers paying more than $100,000 annually as of Q2 FY26, an 8% increase year-over-year. This growth in the enterprise segment underscores Box’s success in expanding relationships with high-value customers.

The large customer growth trend is illustrated in the following chart:

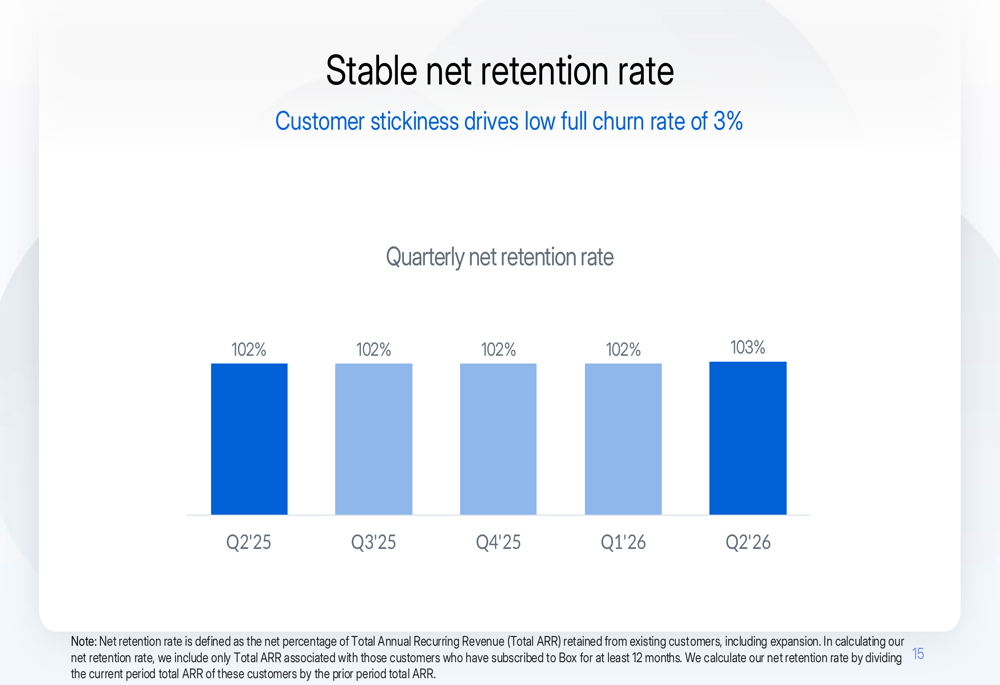

Box’s net retention rate improved to 103% in Q2 FY26, up from 102% in previous quarters, indicating successful customer expansion and strong retention. The company highlighted that its customer stickiness drives a low full churn rate of just 3%.

The net retention rate trend is shown in the following chart:

Capital Allocation and Cash Position

Box ended the quarter with $760 million in cash, cash equivalents, restricted cash, and short-term investments, down from $792 million at the end of Q1 FY26. The change was primarily driven by $46 million in cash from operations, offset by $65 million in financing activities, including share repurchases.

During Q2, Box repurchased approximately 1.2 million shares of its Class A common stock for approximately $40 million. As of July 31, 2025, the company had approximately $112 million remaining in its board-approved buyback authorization.

Forward-Looking Statements

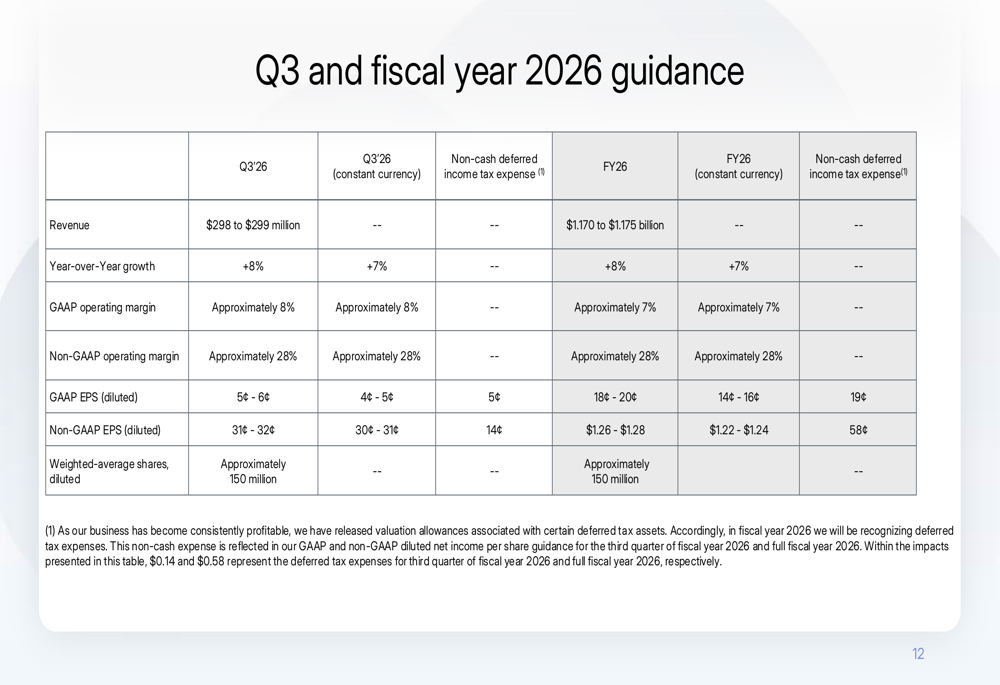

Box provided guidance for both the third quarter and full fiscal year 2026, projecting continued growth and stable margins. For Q3 FY26, the company expects revenue between $298 million and $299 million, representing 8% year-over-year growth (7% in constant currency). Non-GAAP operating margin is expected to be approximately 28%, with non-GAAP diluted EPS between $0.31 and $0.32.

For the full fiscal year 2026, Box raised its revenue guidance to between $1.170 billion and $1.175 billion, representing 8% year-over-year growth (7% in constant currency). The company expects to maintain a non-GAAP operating margin of approximately 28% for the full year, with non-GAAP diluted EPS between $1.26 and $1.28.

The detailed guidance is presented in the following table:

Conclusion

Box’s Q2 FY26 financial results demonstrate accelerating revenue growth and continued progress in its strategic initiatives. The company’s focus on Suites adoption, large customer expansion, and maintaining strong profitability metrics positions it well for sustained growth. With raised full-year guidance and improving customer retention metrics, Box appears confident in its ability to execute on its long-term strategy in the intelligent content management market.

The company’s consistent performance across key financial and operational metrics, combined with its strategic investments in AI-driven solutions, suggests Box is successfully navigating the competitive landscape while delivering value to both customers and shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.