Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Bread Financial Holdings Inc (NYSE:BFH) reported its second quarter 2025 financial results on July 24, 2025, showcasing improved credit metrics and a stable outlook despite a challenging macroeconomic environment. The company’s stock closed at $64.20 prior to the earnings release, representing a 2.12% increase on the day and continuing its positive momentum from earlier in the year.

Quarterly Performance Highlights

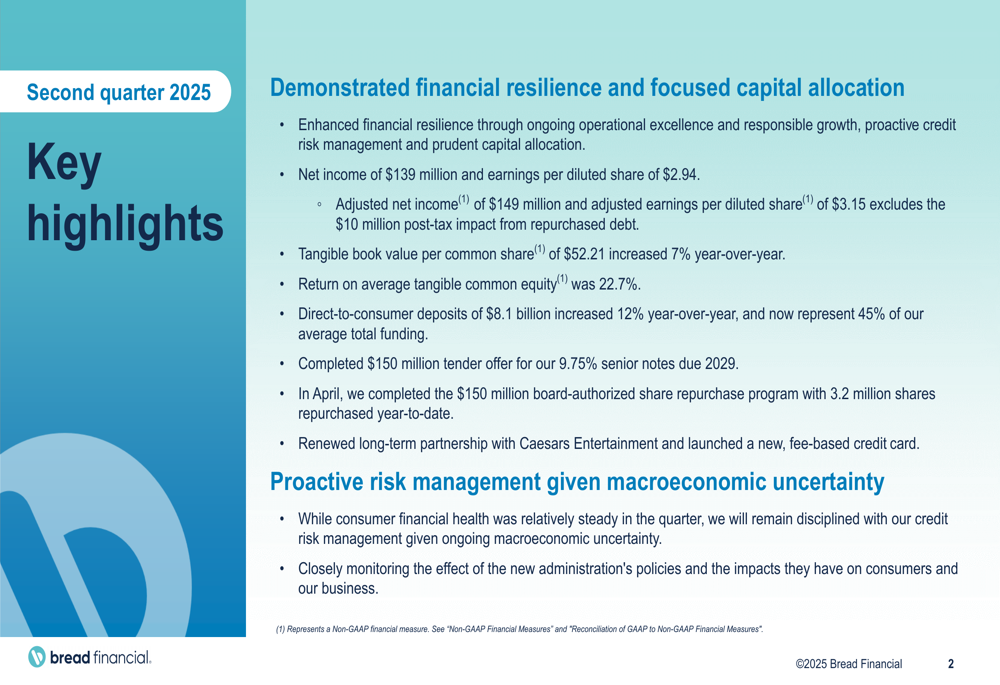

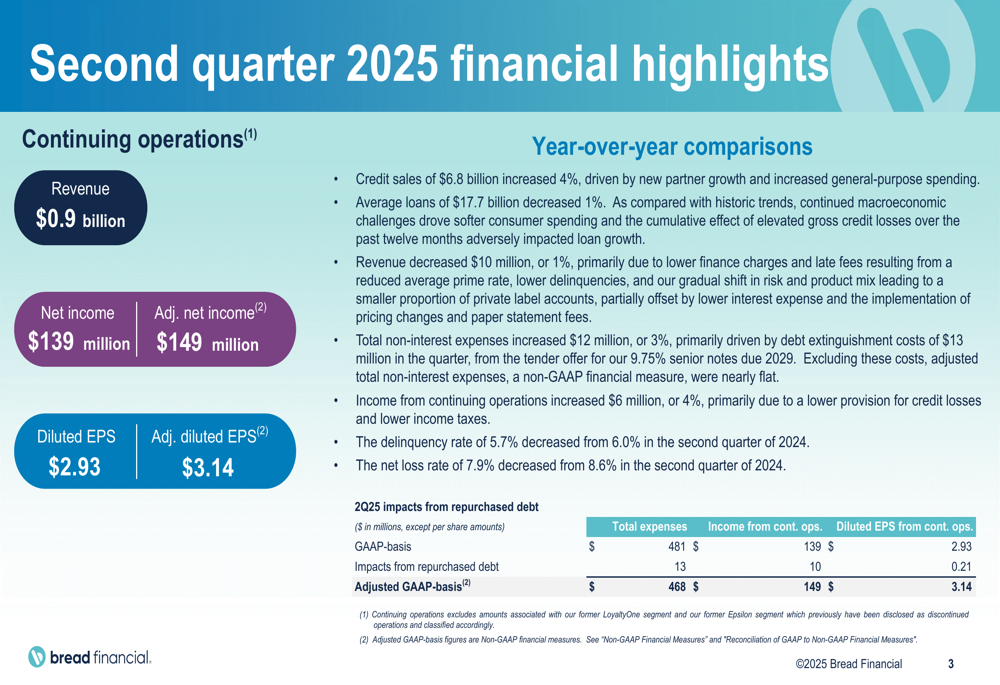

Bread Financial reported net income of $139 million for Q2 2025, representing a 4% increase compared to the same period last year. Diluted earnings per share reached $2.94, while adjusted earnings per share (excluding the impact of repurchased debt) came in at $3.15. The company’s tangible book value per common share increased 7% year-over-year to $52.21, reflecting continued value creation for shareholders.

As shown in the following key highlights from the company’s presentation:

Credit sales increased 4% year-over-year to $6.8 billion, showing accelerated growth compared to the 1% increase reported in Q1 2025. However, average loans decreased slightly by 1% to $17.7 billion, continuing the trend observed in previous quarters but at a more moderate pace. Revenue saw a marginal decline of 1% compared to Q2 2024.

The detailed financial performance for the quarter is illustrated in the following summary:

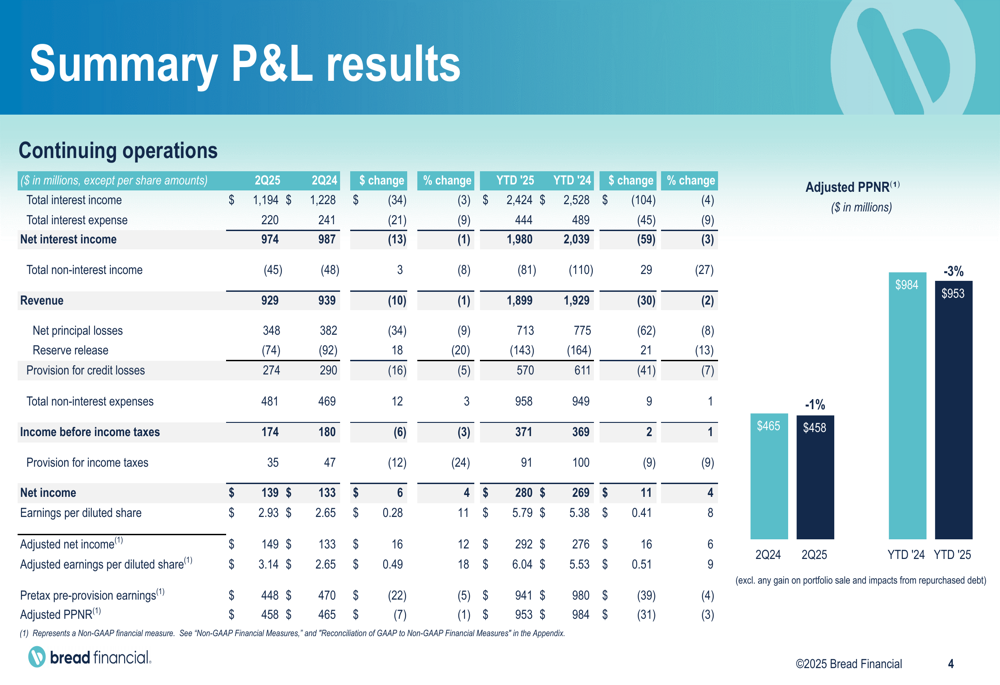

Return on average tangible common equity remained robust at 22.7%, demonstrating Bread Financial’s ability to generate strong returns despite economic headwinds. The company’s P&L results showed resilience across key metrics:

Credit Quality Improvements

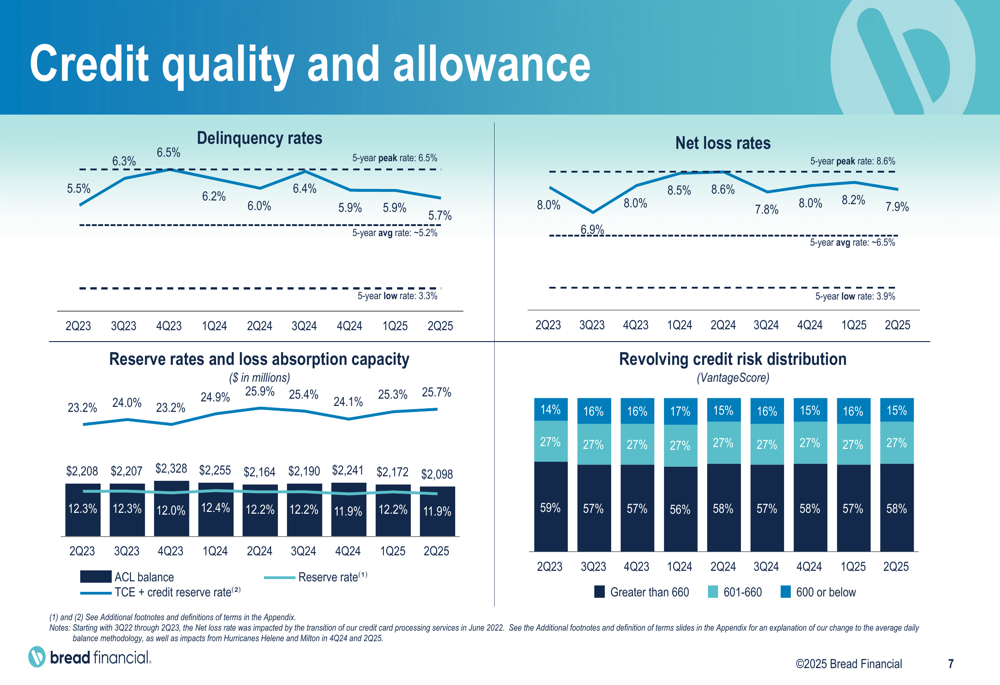

One of the most notable aspects of Bread Financial’s Q2 2025 results was the improvement in credit quality metrics. The delinquency rate decreased to 5.7% from 6.0% in Q2 2024, while the net loss rate improved to 7.9% from 8.6% in the same period last year. These improvements suggest that the company’s risk management strategies are proving effective despite ongoing macroeconomic uncertainties.

The following chart illustrates the trends in credit quality metrics:

The company maintains a strong allowance for credit losses with a reserve rate of 11.9%, providing substantial coverage for potential future losses. This conservative approach to credit risk management positions Bread Financial well to navigate any potential economic challenges in the coming quarters.

Capital Position and Shareholder Returns

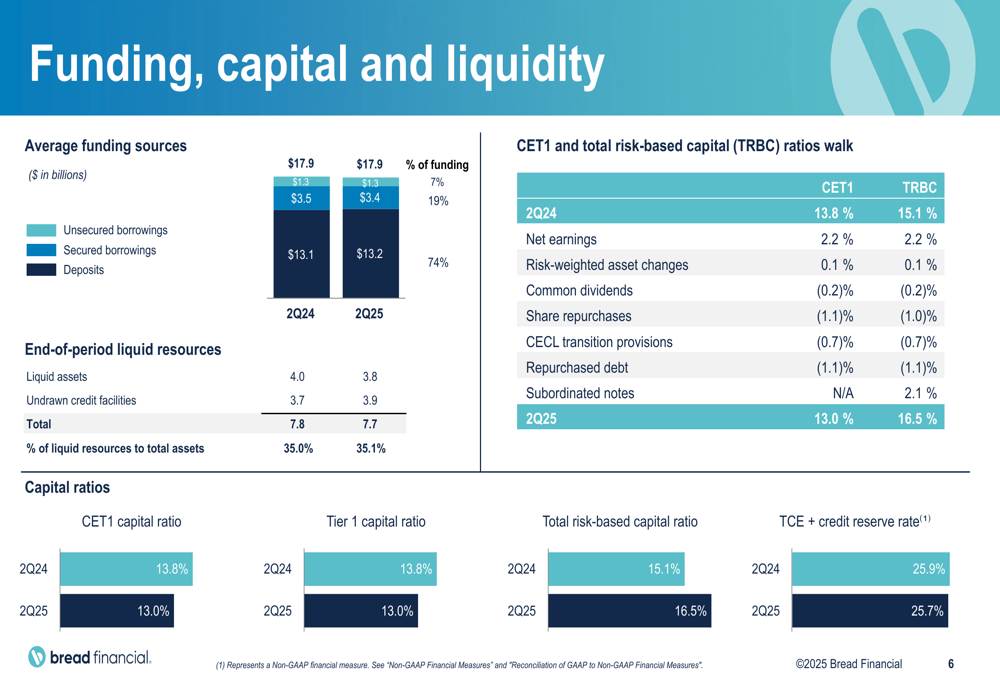

Bread Financial continued to demonstrate financial resilience through prudent capital allocation and a strong balance sheet. The company’s CET1 capital ratio stood at 13.0% at the end of Q2 2025, well above regulatory requirements, while the total risk-based capital ratio was 16.5%.

The company’s funding, capital, and liquidity position is detailed in the following slide:

Direct-to-consumer deposits reached $8.1 billion, representing a 12% increase year-over-year and accounting for 45% of average total funding. This growth in the deposit base provides Bread Financial with a stable and cost-effective funding source.

In terms of shareholder returns, the company completed a $150 million share repurchase program in April, with a total of 3.2 million shares repurchased year-to-date. Additionally, Bread Financial completed a $150 million tender offer for senior notes due 2029, demonstrating its commitment to optimizing its capital structure.

Strategic Initiatives and Partnerships

Bread Financial continues to focus on four key strategic areas to drive long-term growth and value creation. These include responsible growth, managing to the macroeconomic and regulatory environment, disciplined capital allocation and risk management, and operational excellence.

The company’s strategic priorities are outlined in the following slide:

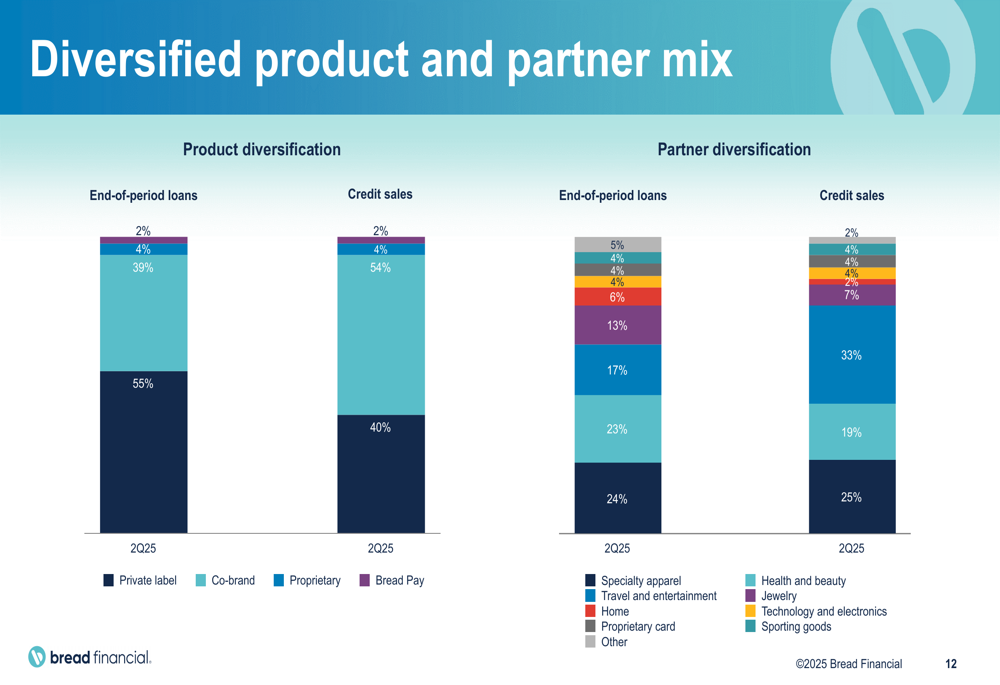

On the partnership front, Bread Financial renewed its relationship with Caesars (NASDAQ:CZR) Entertainment and launched a new, fee-based credit card. This renewal builds on the company’s diversified product and partner mix, which spans across various industries including specialty apparel, travel and entertainment, and home goods.

The company’s diversified business model is illustrated in the following breakdown:

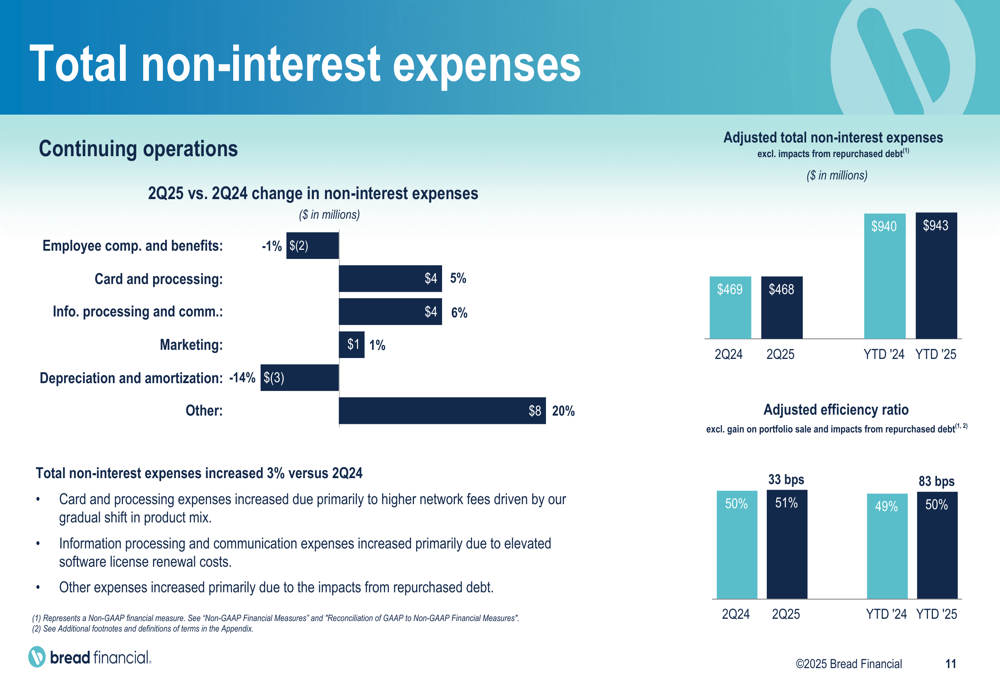

Bread Financial’s operational efficiency remains a focus area, with the company maintaining disciplined expense management despite inflationary pressures. Total (EPA:TTEF) non-interest expenses increased by 3% compared to Q2 2024, with the main drivers being higher network fees due to product mix shifts and elevated software license renewal costs.

The breakdown of non-interest expenses is shown in the following chart:

2025 Financial Outlook

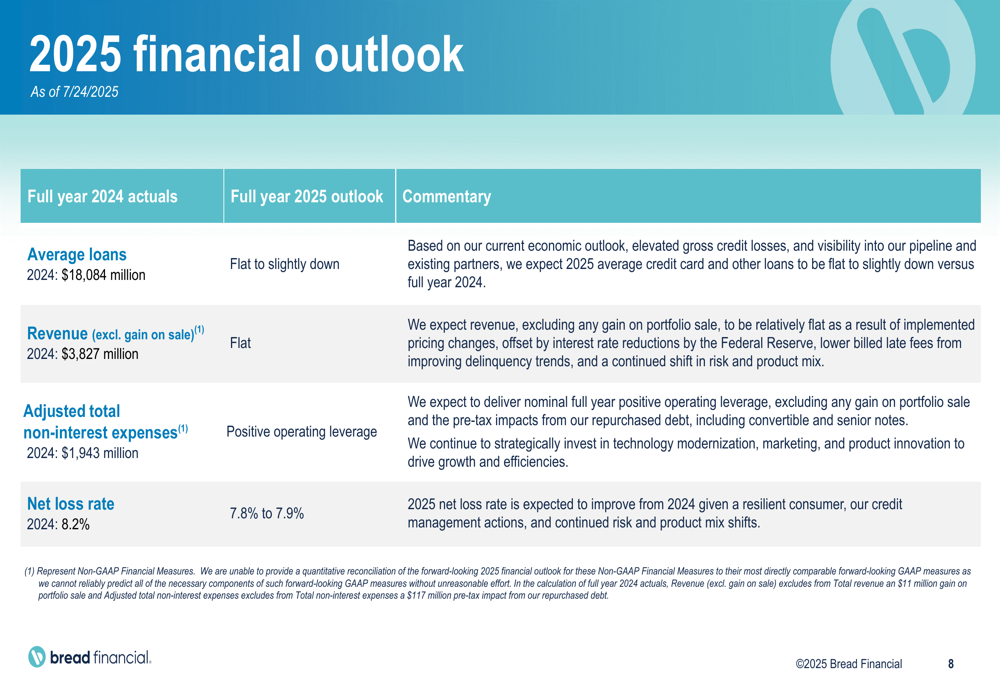

Looking ahead, Bread Financial provided a stable outlook for the full year 2025. The company expects average loans to be flat to slightly down compared to 2024, while revenue (excluding gain on sale) is projected to remain flat. Management anticipates positive operating leverage for adjusted total non-interest expenses and forecasts the net loss rate to improve to 7.8%-7.9% from 8.2% in 2024.

The company’s financial outlook is summarized in the following slide:

Management commentary suggests that revenue is expected to remain relatively flat, with pricing changes and interest rate reductions being offset by lower delinquency fees. The company continues to monitor the macroeconomic environment closely, particularly consumer financial health and the potential impact of policy changes.

Bread Financial’s performance in Q2 2025 demonstrates its ability to navigate challenging economic conditions while maintaining strong capital levels and improving credit metrics. With a focus on operational excellence, disciplined capital allocation, and strategic partnerships, the company appears well-positioned to deliver stable results for the remainder of 2025 despite ongoing macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.