Novo Nordisk, Eli Lilly slide after Trump comments on weight loss drug pricing

Introduction & Market Context

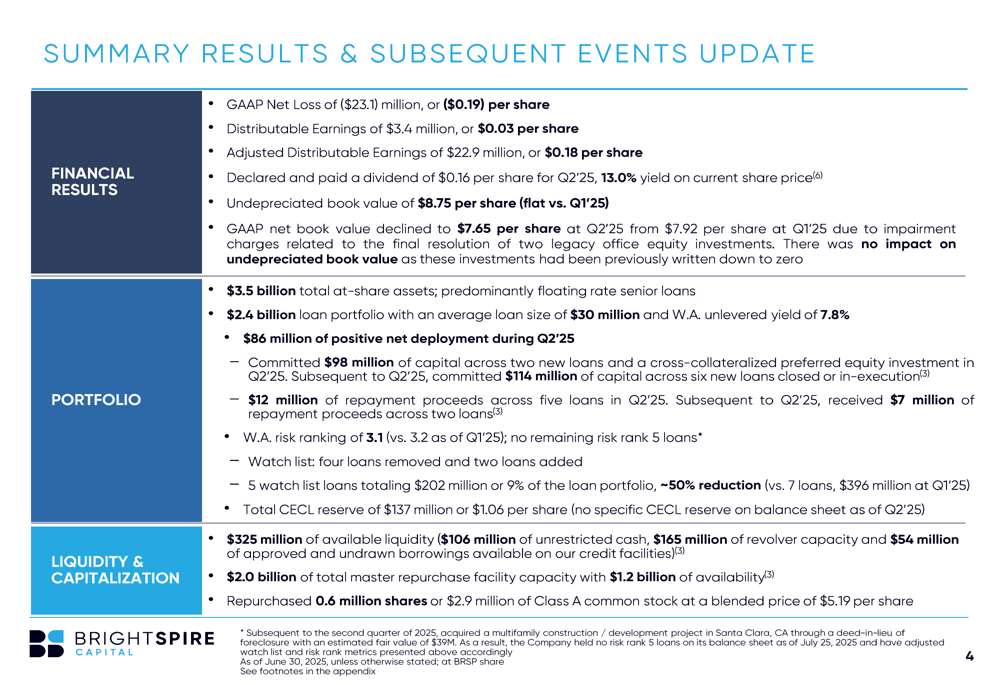

BrightSpire Capital (NYSE:BRSP) released its Q2 2025 supplemental financial report on July 29, 2025, revealing mixed results with improved adjusted distributable earnings despite a GAAP net loss. The commercial real estate investment trust, which focuses primarily on senior loans across multifamily, office, and industrial properties, maintained its quarterly dividend of $0.16 per share, representing an annualized yield of 13% based on current share prices.

The company’s stock closed at $4.97 on July 29, trading at a significant discount to its undepreciated book value of $8.75 per share. This represents a continuation of the challenging environment for commercial real estate lenders, though BrightSpire’s portfolio quality showed signs of improvement during the quarter.

Quarterly Performance Highlights

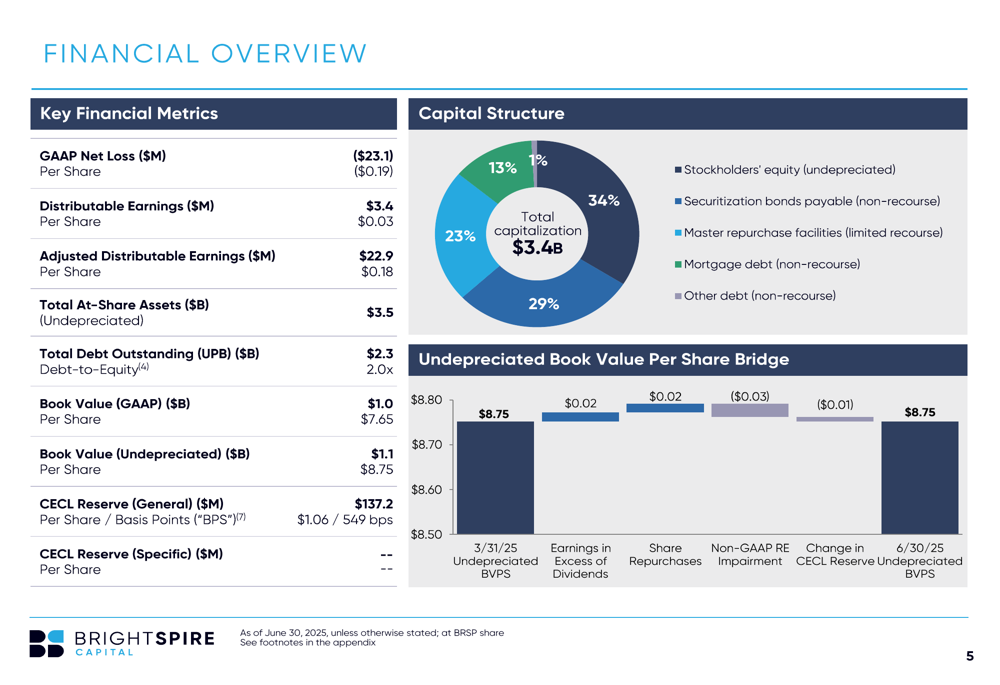

BrightSpire reported adjusted distributable earnings of $22.9 million or $0.18 per share for Q2 2025, an improvement from the $0.16 per share reported in Q1 2025. However, GAAP results showed a net loss of $23.1 million or $0.19 per share, a significant decline from the GAAP net income of $0.04 per share in the previous quarter.

As shown in the following financial overview, the company’s undepreciated book value remained stable at $8.75 per share, while GAAP book value declined to $7.65 per share from $7.92 in Q1 2025, primarily due to impairment charges related to legacy office equity investments:

The company highlighted that these impairments had no impact on undepreciated book value as the investments had been previously written down to zero. BrightSpire also repurchased 0.6 million shares of its common stock at a blended price of $5.19 per share during the quarter, demonstrating confidence in its valuation.

The following summary results slide provides a comprehensive overview of BrightSpire’s Q2 2025 performance:

Portfolio Composition & Quality

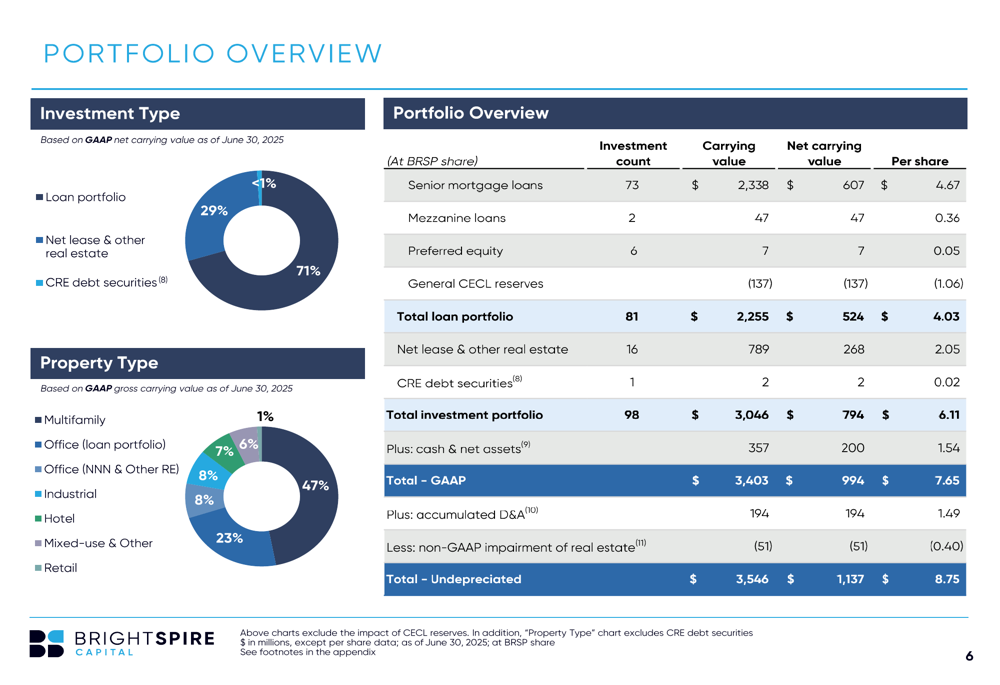

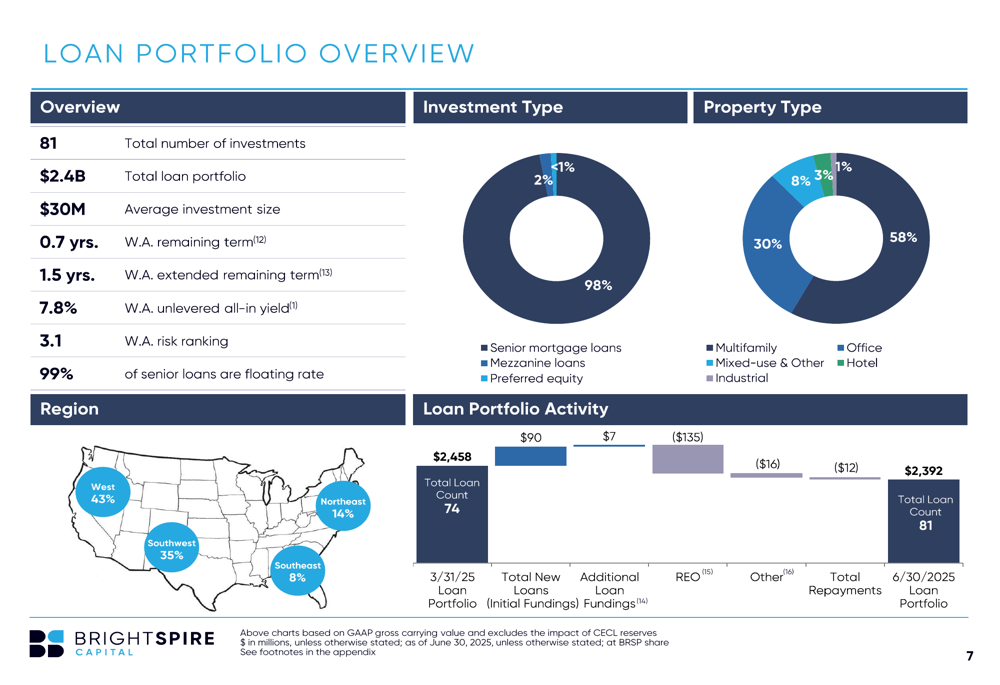

BrightSpire’s portfolio totaled $3.5 billion in undepreciated assets as of Q2 2025, with the loan portfolio accounting for $2.4 billion across 81 loans. The company maintained a diversified approach with a focus on multifamily properties (47%), followed by hotel (23%), office (14%), and industrial (8%) assets.

The portfolio overview below illustrates this diversification strategy:

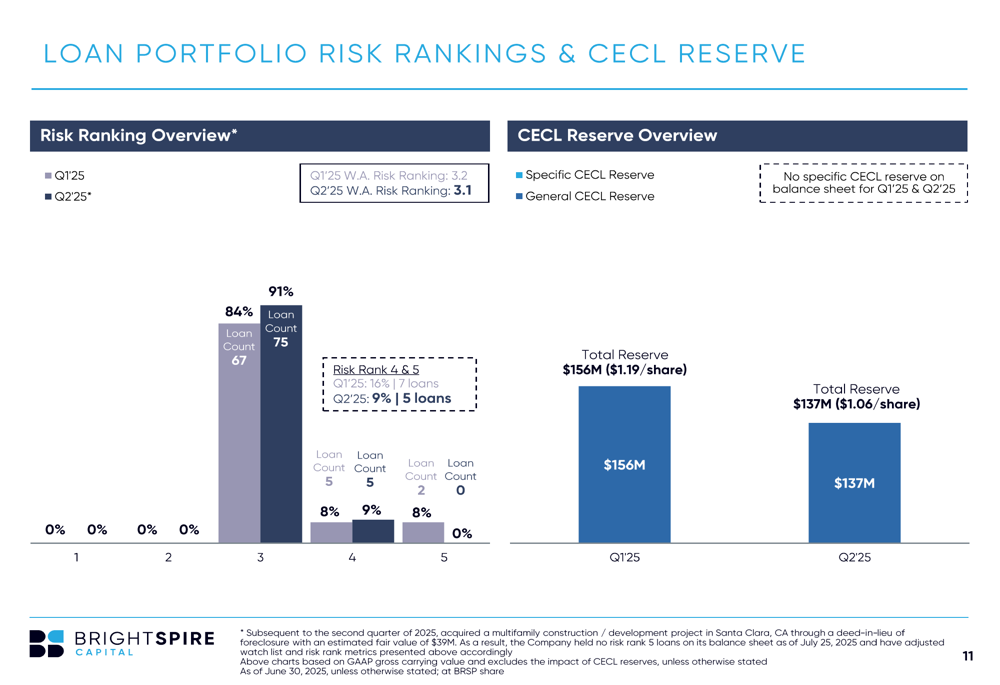

A key positive development was the improvement in the company’s weighted average risk ranking to 3.1 from 3.2 in the previous quarter, with no remaining risk rank 5 loans (the highest risk category). Additionally, the total CECL reserve decreased to $137 million ($1.06 per share) from $156 million ($1.19 per share) in Q1 2025, suggesting improved confidence in the overall portfolio quality.

The following chart illustrates the improvement in risk rankings between Q1 and Q2 2025:

The loan portfolio remained predominantly floating rate (97%), with a weighted average unlevered all-in yield of 7.8%. The average loan size was $30 million, with 89% of loans (by count) under $50 million, indicating a focus on diversification rather than concentration in large exposures.

The detailed loan portfolio overview provides further insight into the composition and regional distribution:

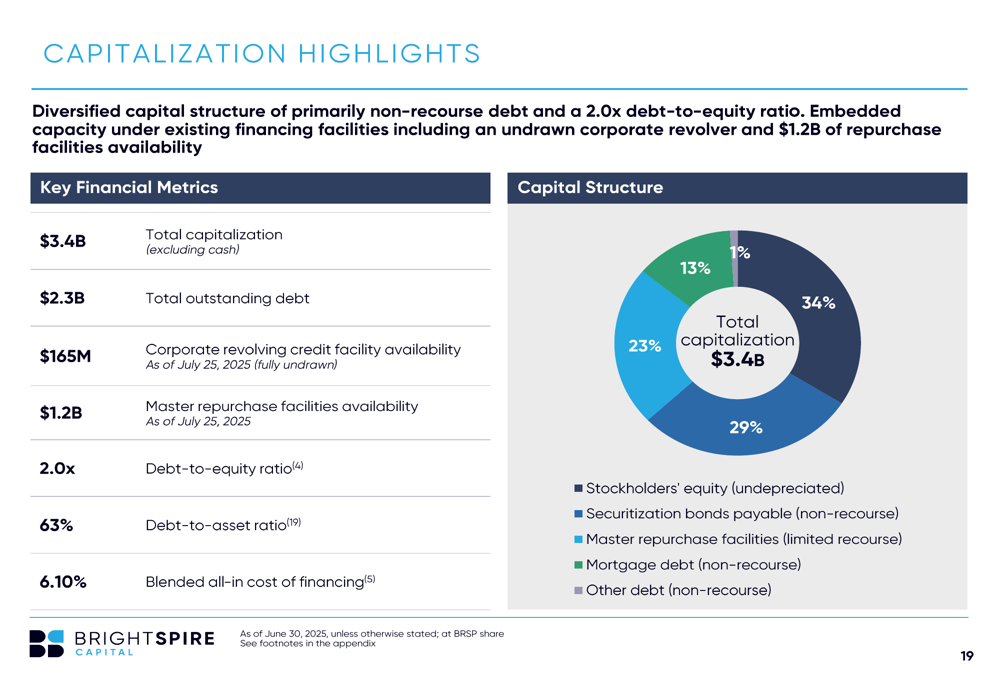

Capitalization & Liquidity

BrightSpire maintained a solid liquidity position with $325 million in total liquidity, including $106 million in unrestricted cash ($0.82 per share) and $165 million available on its corporate revolving credit facility. The company’s debt-to-equity ratio stood at 2.0x, with a weighted average all-in cost of financing of 6.10%.

The following capitalization highlights provide a comprehensive view of the company’s capital structure:

The company’s master repurchase facilities had $1.2 billion in availability, providing significant dry powder for future investments. BrightSpire reported positive net deployment of $86 million during Q2 2025, with $12 million in repayment proceeds across five loans during the quarter and an additional $7 million received subsequent to quarter-end.

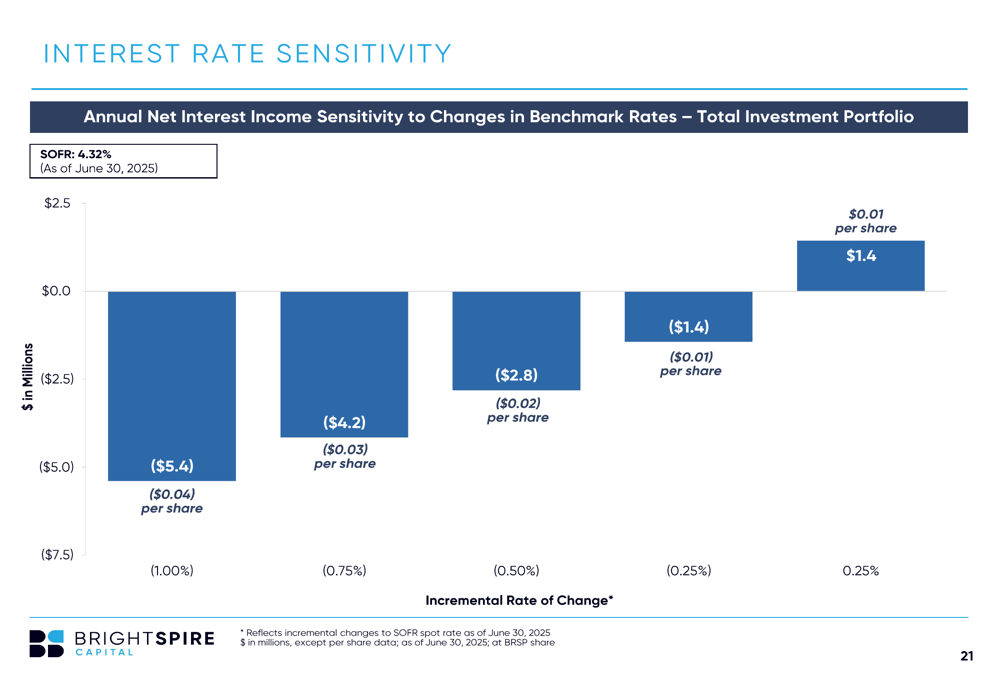

Interest Rate Sensitivity & Outlook

Given the predominantly floating-rate nature of BrightSpire’s loan portfolio, the company’s earnings are sensitive to changes in benchmark interest rates. The following chart illustrates the potential impact of rate changes on annual net interest income:

The analysis shows that a 25 basis point increase in rates would add approximately $1.4 million ($0.01 per share) to annual net interest income, while a 25 basis point decrease would reduce it by the same amount. This relatively balanced sensitivity suggests the company has effectively managed its interest rate exposure.

Looking ahead, BrightSpire’s loan portfolio has a weighted average fully extended remaining term of approximately 1.5 years, with maturities spread across 2025 through 2028 and beyond. This staggered maturity profile provides opportunities for reinvestment at potentially higher yields if market conditions improve.

Conclusion

BrightSpire Capital’s Q2 2025 results present a mixed picture, with improved adjusted distributable earnings and portfolio quality metrics offset by a GAAP net loss due to legacy asset impairments. The company’s maintained dividend of $0.16 per share (13% annualized yield) and stable undepreciated book value of $8.75 per share provide some stability for investors, particularly given the current share price of around $5, which represents a significant discount to book value.

The improved risk rankings and reduced CECL reserves suggest the company is making progress in addressing portfolio challenges, though the commercial real estate market continues to present headwinds. With solid liquidity and available financing capacity, BrightSpire appears positioned to navigate the current environment while seeking selective growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.