Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

BrightView Holdings (NYSE:BV), the largest commercial landscaping services company in the United States, presented its third quarter fiscal 2025 earnings results on August 7, 2025. The company’s stock closed at $16.28 on August 6, up 0.99% ahead of the earnings announcement, and has shown resilience with a 52-week range of $11.81 to $18.89.

Following a strong second quarter where BrightView exceeded expectations with 3% revenue growth and a 13% year-over-year increase in adjusted EBITDA, the third quarter results showed mixed performance with declining revenue but continued margin expansion and operational improvements.

Quarterly Performance Highlights

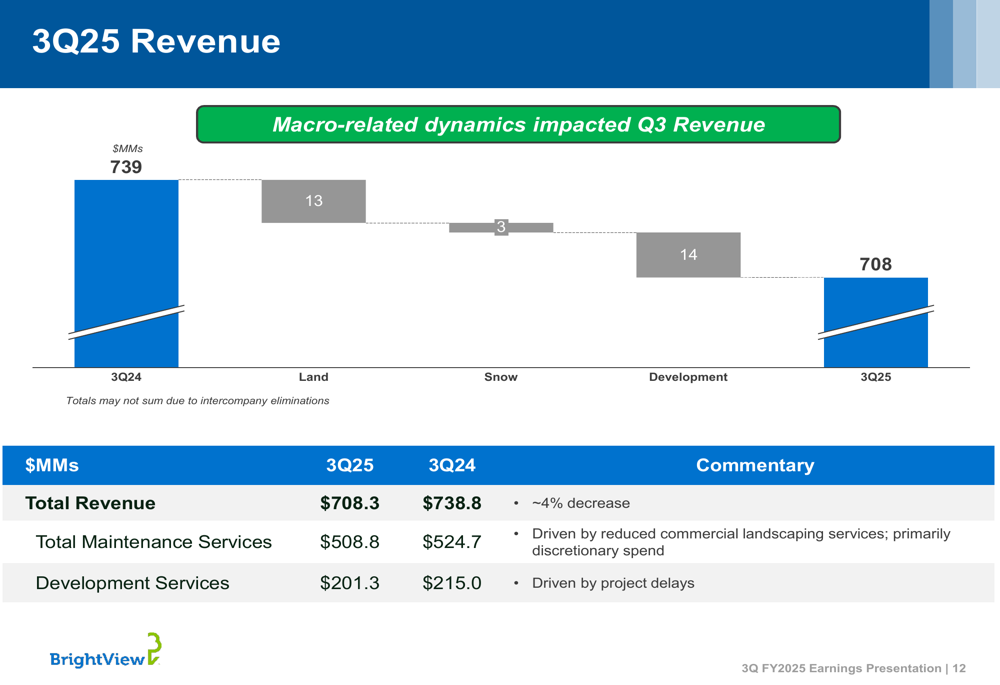

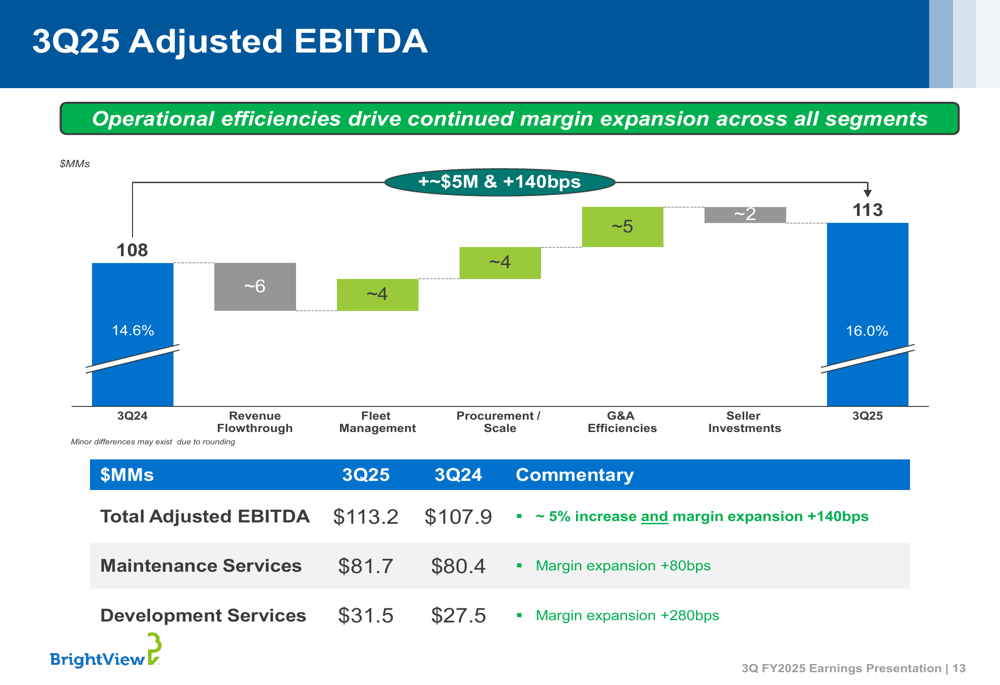

BrightView reported third quarter revenue of $708.3 million, representing a 4% decrease from $738.8 million in the same period last year. Despite this revenue decline, the company achieved adjusted EBITDA of $113.2 million, a 5% increase from $107.9 million in Q3 2024, with margins expanding by 140 basis points.

As shown in the following revenue breakdown chart, both maintenance and development segments experienced revenue declines:

The revenue decrease was attributed to macro-related dynamics affecting both the maintenance and development segments. However, the company’s focus on operational efficiencies drove continued margin expansion across all segments, as illustrated in the adjusted EBITDA performance:

BrightView’s maintenance services segment reported adjusted EBITDA of $81.7 million (up from $80.4 million in Q3 2024) with an 80 basis point margin expansion, while development services achieved $31.5 million (up from $27.5 million) with an impressive 280 basis point margin improvement.

Strategic Initiatives

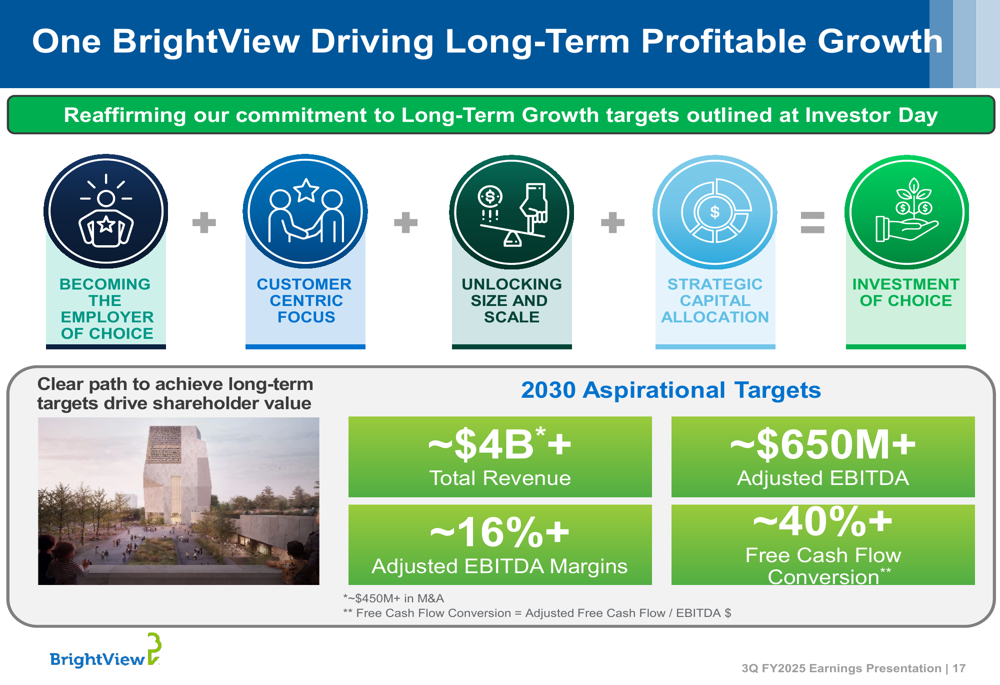

CEO Dale Asplund highlighted the company’s "One BrightView" strategy as the driving force behind the transformation and improved profitability. This approach focuses on four key pillars that aim to position BrightView as an investment of choice:

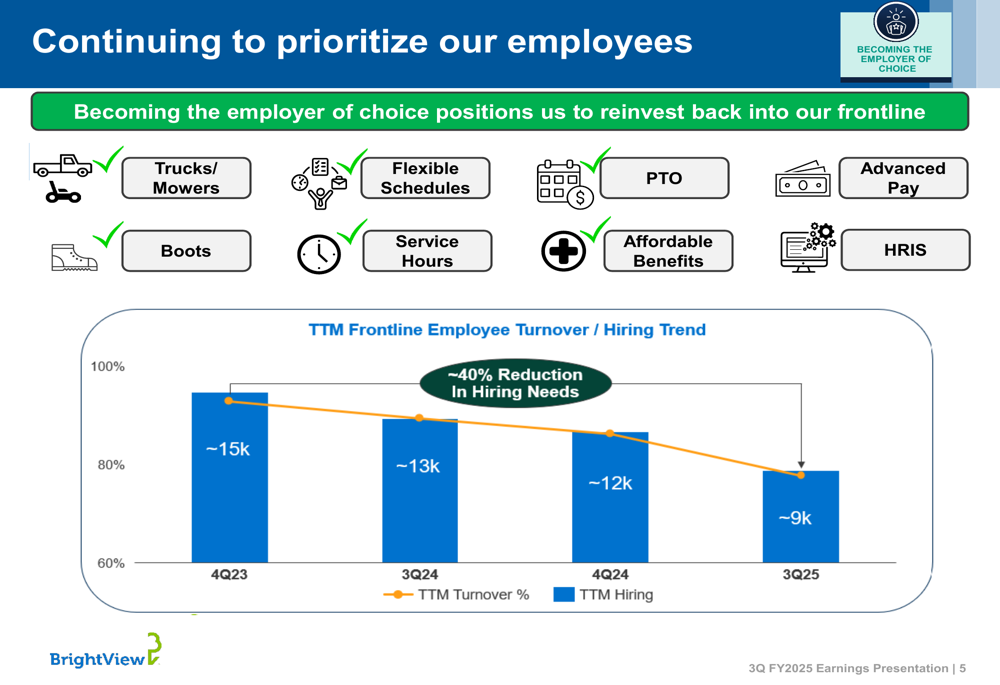

A critical component of BrightView’s strategy is reducing employee turnover, which has resulted in approximately 40% reduction in hiring needs compared to previous years. This focus on becoming an "employer of choice" has led to improved operational efficiency and customer service:

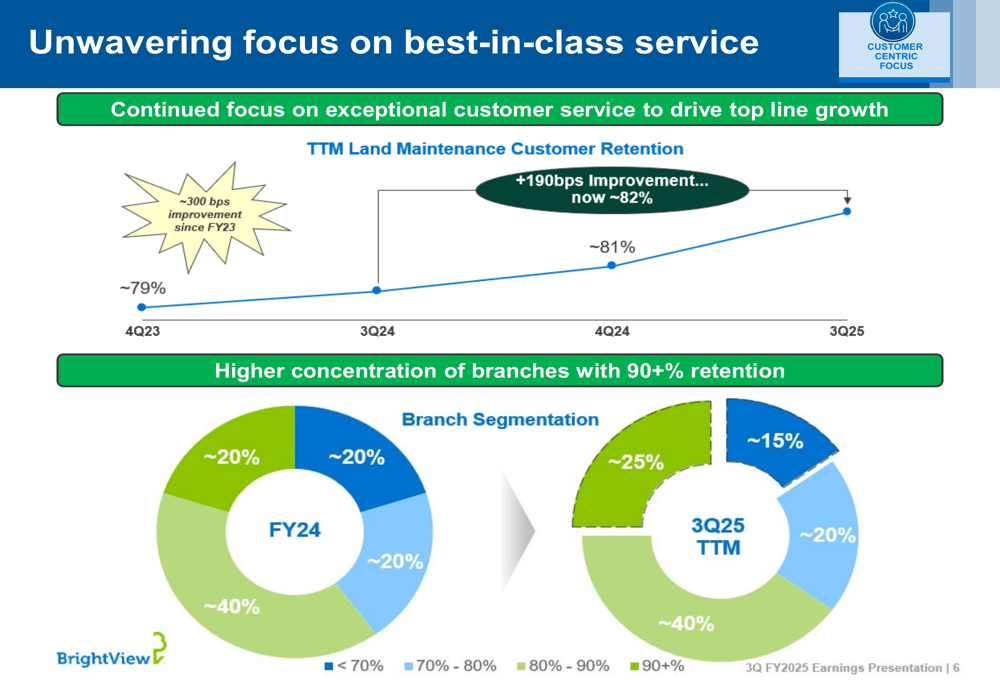

The company’s customer-centric approach has yielded positive results, with maintenance customer retention improving by 190 basis points to approximately 82% in Q3 2025:

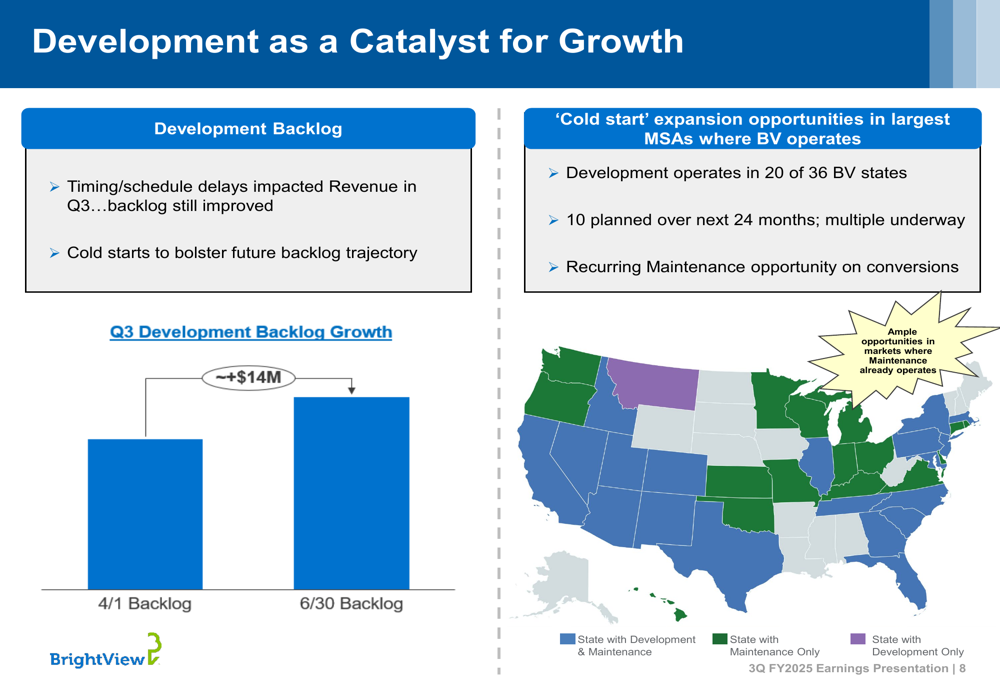

BrightView is also leveraging its development business as a catalyst for growth, with plans to expand into 10 new markets over the next 24 months through cold starts, creating additional opportunities for recurring maintenance revenue:

Financial Analysis

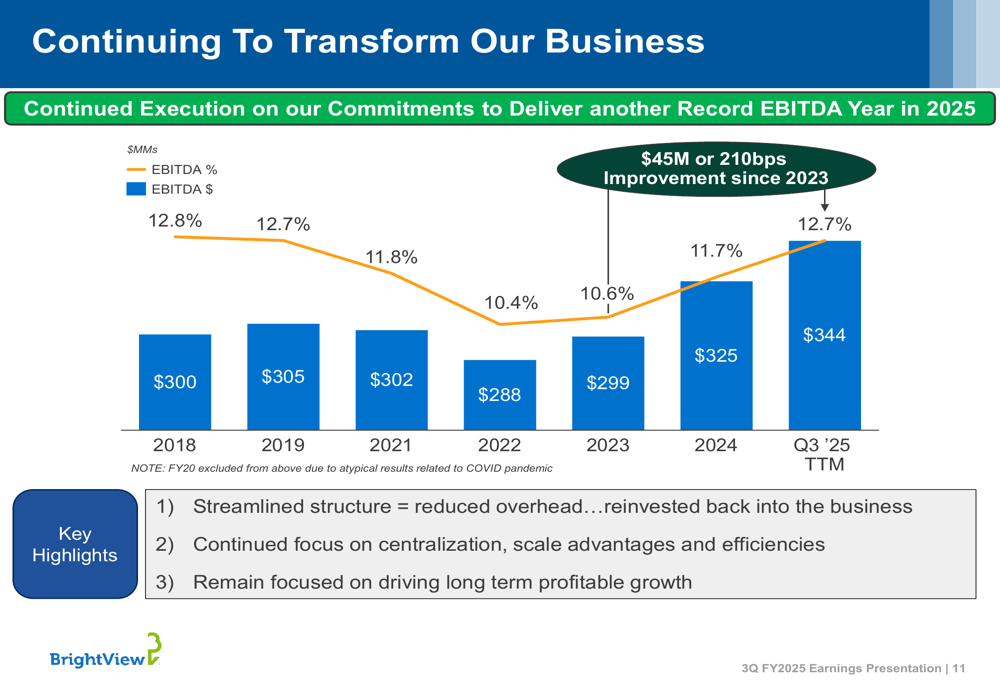

Despite revenue challenges, BrightView continues to demonstrate strong financial performance in key metrics. The company has achieved consistent EBITDA growth since 2023, with trailing twelve-month adjusted EBITDA reaching $344 million, representing a $45 million or 210 basis point improvement since 2023:

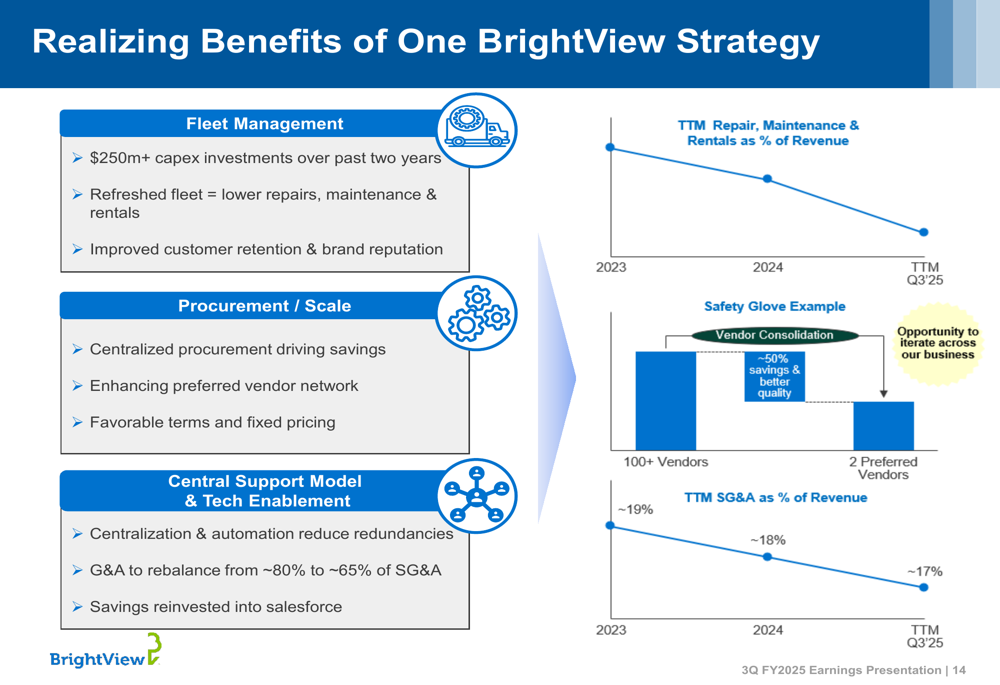

The company’s focus on operational efficiencies through its One BrightView strategy has yielded tangible benefits, including reduced fleet maintenance costs and lower SG&A expenses as a percentage of revenue:

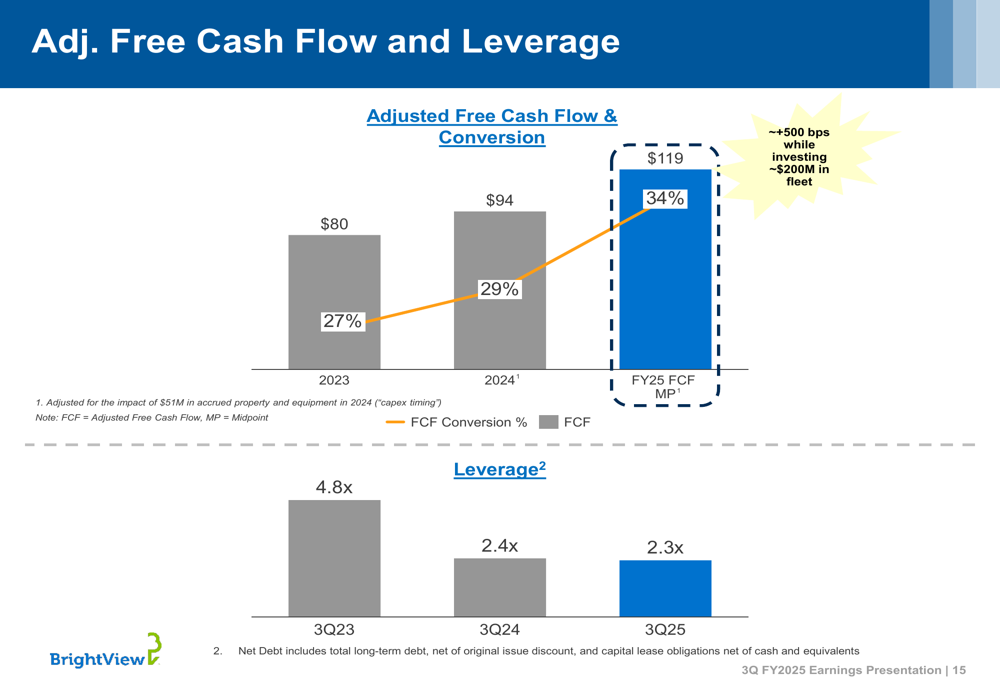

Free cash flow has shown significant improvement, increasing from $94 million with 29% conversion in 2024 to a projected $119 million with 34% conversion in fiscal 2025. Simultaneously, BrightView has reduced its leverage ratio from 4.8x in Q3 2023 to 2.3x in Q3 2025:

Forward-Looking Statements

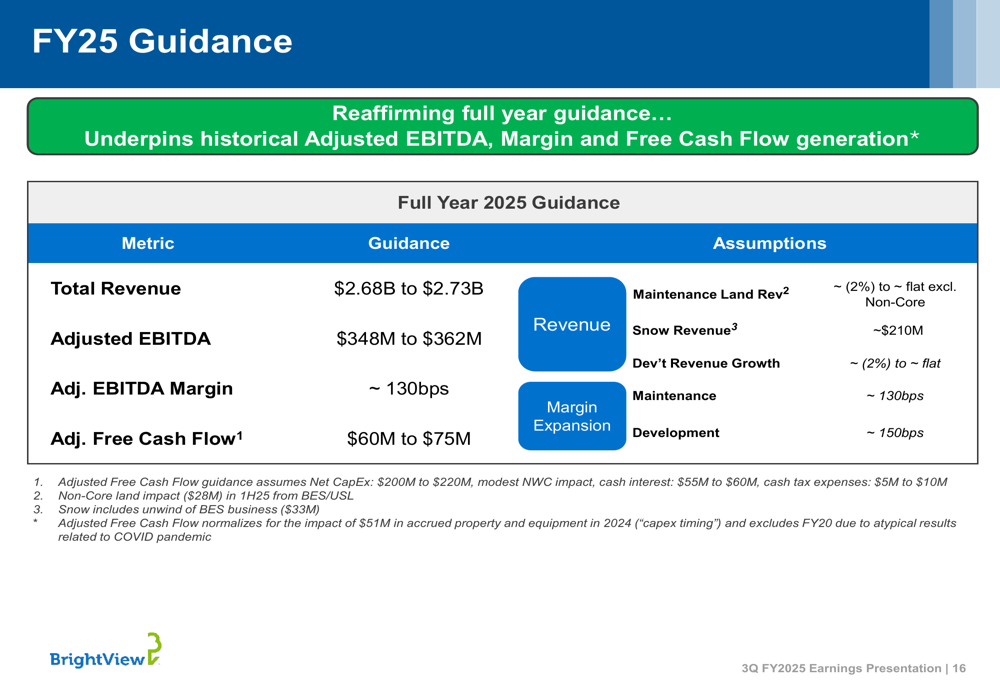

BrightView reaffirmed its full-year fiscal 2025 guidance, projecting total revenue between $2.68 billion and $2.73 billion, and adjusted EBITDA between $348 million and $362 million:

This guidance aligns with the company’s previous forecast and supports the projection of record adjusted EBITDA for fiscal 2025, with continued margin expansion of approximately 130 basis points.

Looking further ahead, BrightView outlined ambitious long-term targets for 2030, including approximately $4 billion in total revenue, adjusted EBITDA margins exceeding 16%, and free cash flow conversion above 40%:

CFO Brett Urban emphasized the company’s focus on long-term profitable growth, noting that the strategic investments in fleet refresh and technology are expected to support these growth initiatives while maintaining financial discipline.

In conclusion, while BrightView faces near-term revenue challenges, the company’s third quarter results demonstrate that its strategic focus on operational efficiency, employee retention, and customer service is yielding improved profitability and positioning the company for sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.