Intel stock spikes after report of possible US government stake

Introduction & Market Context

Brinker International (NYSE:EAT), parent company of Chili’s and Maggiano’s Little Italy, showcased exceptional performance in its fourth quarter fiscal 2025 presentation on August 13. The company reported consolidated comparable sales growth of 21.3% for Q4, with its flagship Chili’s brand leading the charge at 23.7% growth. Following the earnings announcement, Brinker’s stock rose 1.61% to close at $157.38, reflecting investor confidence in the company’s performance and strategy.

The restaurant operator’s strong quarterly results capped off an impressive fiscal year, with total annual revenue exceeding $5 billion for the first time in company history. This performance comes amid a competitive casual dining landscape where many competitors have struggled to maintain growth momentum.

Quarterly Performance Highlights

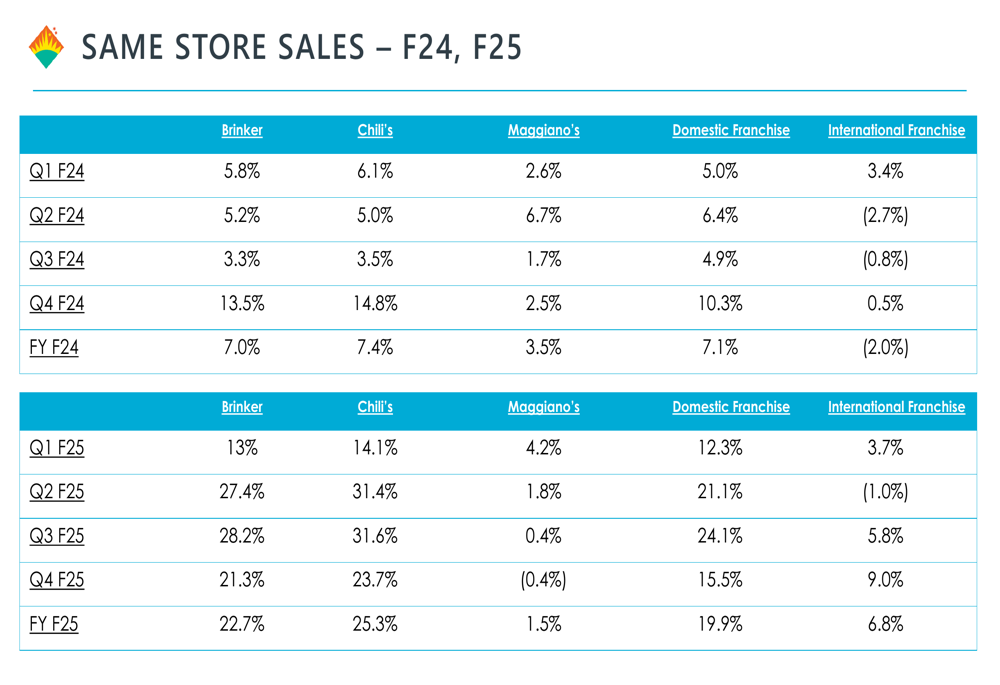

Brinker’s Q4 F25 results demonstrated remarkable same-store sales growth across most segments of its business. The company’s consolidated comparable sales increased by 21.3%, driven primarily by Chili’s robust 23.7% growth. Domestic franchises also performed well with 15.5% growth, while international franchises posted a 9.0% increase. Maggiano’s was the only segment to show a slight decline, with same-store sales decreasing by 0.4% for the quarter.

As shown in the following chart of quarterly same-store sales performance:

The full fiscal year 2025 results were equally impressive, with Brinker achieving 22.7% consolidated comparable sales growth. Chili’s led with 25.3% growth, while Maggiano’s posted a more modest 1.5% increase. Domestic and international franchises grew by 19.9% and 6.8% respectively.

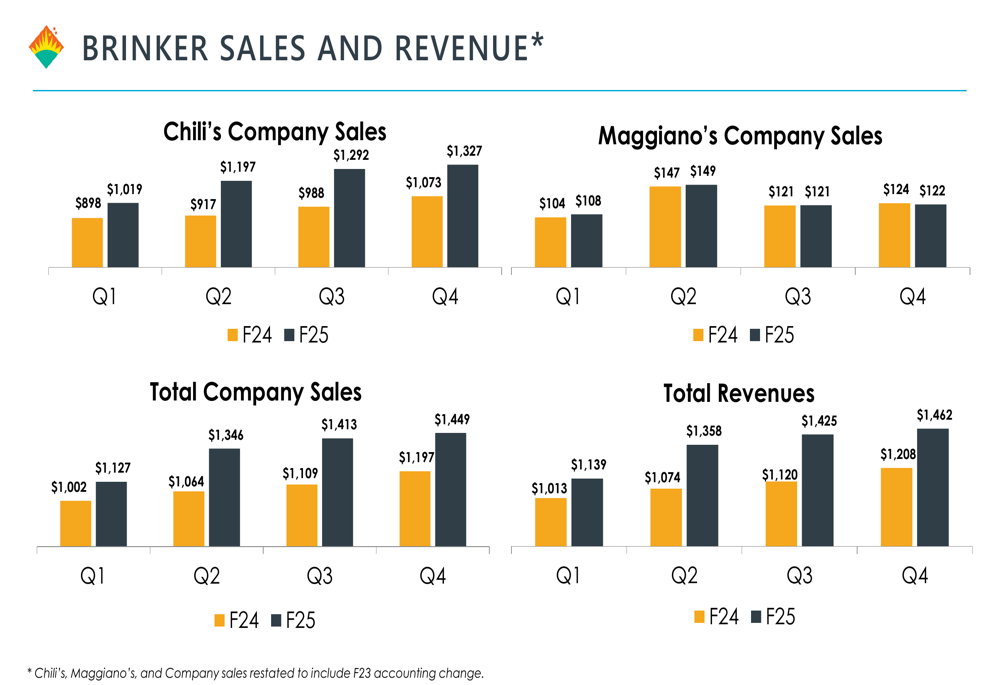

Total revenue for Q4 F25 reached $1.462 billion, representing a 21.9% increase from $1.208 billion in the same quarter last year. This aligns with the $1.44 billion reported in the earnings announcement. For the full fiscal year, Brinker’s revenue performance showed consistent quarterly growth as illustrated in the following chart:

Detailed Financial Analysis

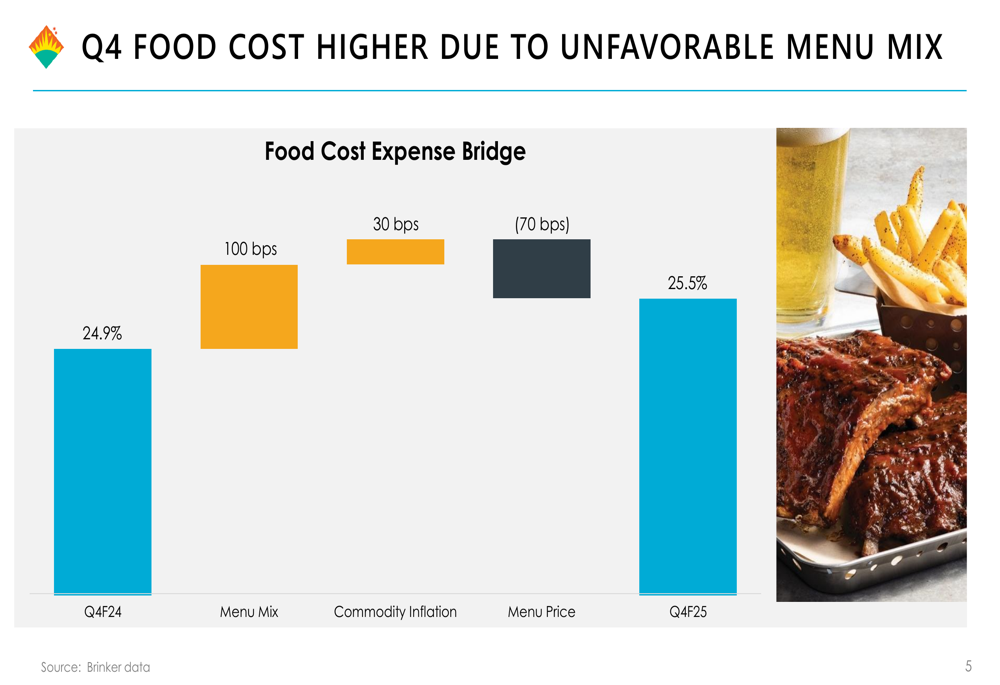

Despite strong top-line growth, Brinker faced some margin pressures in certain areas. Food costs as a percentage of sales increased from 24.9% in Q4 F24 to 25.5% in Q4 F25. This 60 basis point increase was primarily driven by unfavorable menu mix (contributing 100 basis points) and commodity inflation (adding 30 basis points), partially offset by menu price increases (reducing costs by 70 basis points).

The following chart details these food cost dynamics:

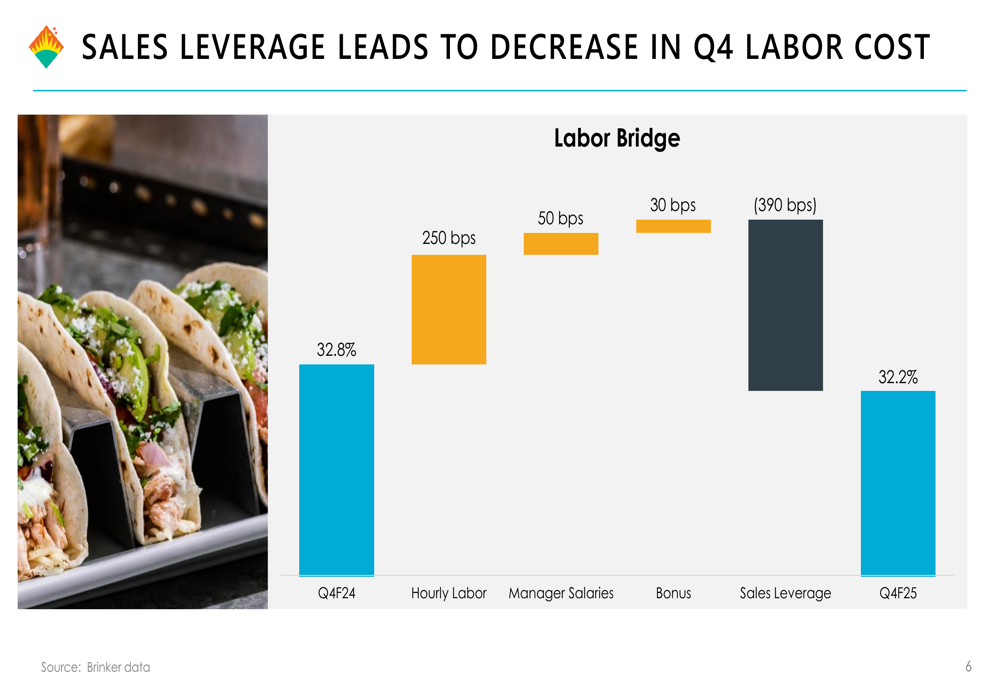

However, the company successfully leveraged its strong sales to improve other cost metrics. Labor costs decreased from 32.8% to 32.2% of sales, as sales leverage of 390 basis points more than offset increases in hourly labor (250 basis points), manager salaries (50 basis points), and bonuses (30 basis points).

As illustrated in this labor cost breakdown:

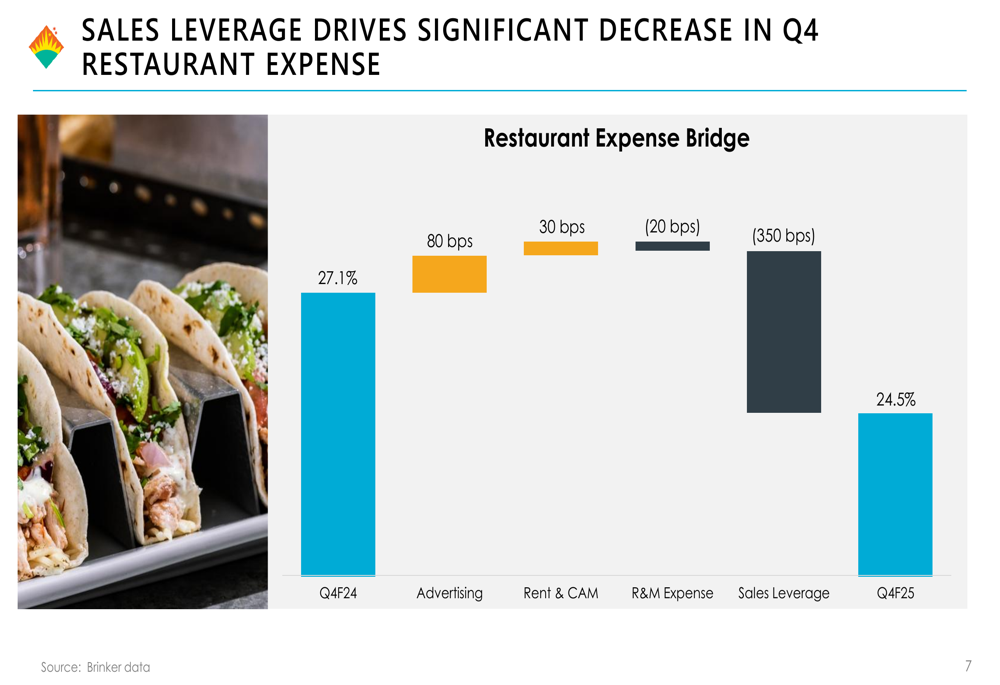

Restaurant expenses saw the most significant improvement, decreasing from 27.1% to 24.5% of sales. While advertising costs increased by 80 basis points and rent and common area maintenance rose by 30 basis points, these were more than offset by a 20 basis point decrease in repair and maintenance expenses and, most significantly, a 350 basis point benefit from sales leverage.

The following chart shows these restaurant expense factors:

These margin improvements contributed to Brinker’s restaurant operating margin of 17.8% for Q4, representing a 260 basis point improvement year-over-year as noted in the earnings report.

Strategic Initiatives & Margin Management

Brinker’s presentation reveals a strategic focus on leveraging strong sales growth to offset inflationary pressures. While the company has implemented menu price increases to partially counter rising costs, the significant sales volume growth has been the primary driver of margin improvements.

The company’s differentiated performance between its two main brands highlights both opportunities and challenges. Chili’s continues to be the growth engine, with consistent double-digit comparable sales increases across all quarters of fiscal 2025. Maggiano’s, while profitable, has shown more modest growth and experienced a slight decline in the fourth quarter.

CEO Kevin Hockman emphasized in the earnings call that the company is "at a much different Chili’s today than we were three years ago," highlighting the brand’s transformation. The presentation data supports this assertion, with Chili’s demonstrating exceptional growth momentum.

Forward-Looking Statements

Looking ahead to fiscal 2026, Brinker has provided revenue guidance of $5.6-5.7 billion and adjusted diluted EPS between $9.90 and $10.50. The company expects positive same-store sales to continue in all quarters.

The presentation suggests Brinker will continue focusing on operational efficiency to manage costs. While commodity inflation and labor costs remain challenges, the company’s ability to drive strong sales growth has proven effective in maintaining and improving margins.

Brinker also plans to remodel approximately 10% of its restaurant fleet annually, with continued investment in technology improvements and restaurant development. These initiatives aim to sustain the momentum demonstrated throughout fiscal 2025, particularly at the Chili’s brand.

With a strong financial position, including a reduced debt load of over $570 million in the past three years and a lease-adjusted leverage ratio of 1.7x, Brinker appears well-positioned to execute its growth strategy while navigating ongoing industry challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.