Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Brink’s Company (NYSE:BCO) reported solid first-quarter 2025 results on May 12, with organic revenue growth hitting the upper limit of prior guidance and digital solutions continuing their strong momentum. The company’s strategic shift toward higher-margin services appears to be paying dividends despite mixed regional performance.

Quarterly Performance Highlights

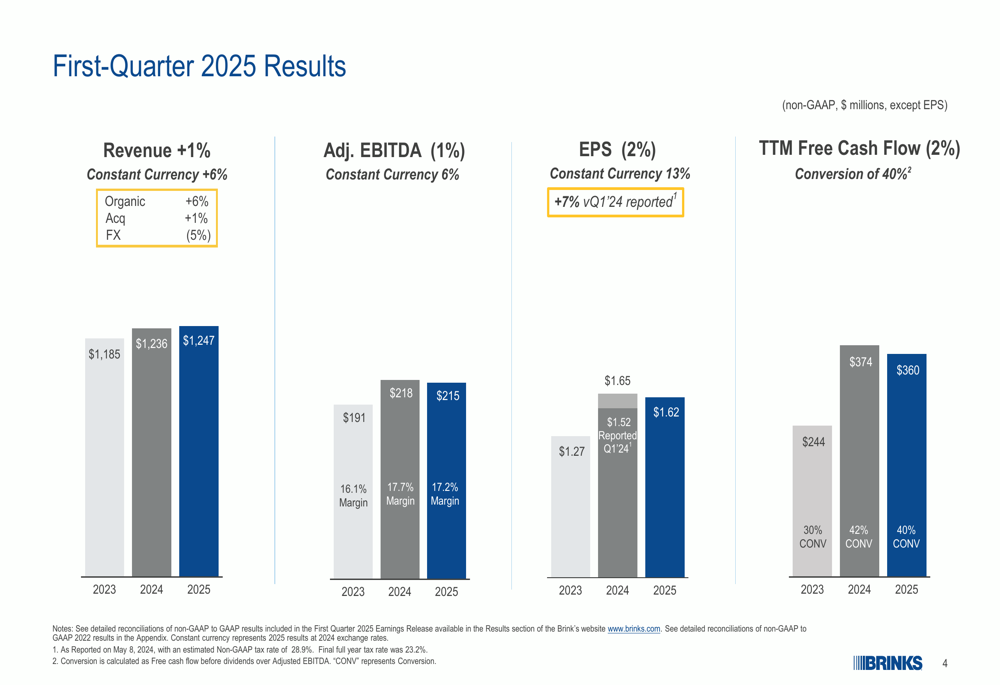

Brink’s achieved 6% organic revenue growth in Q1 2025, reaching the upper end of its guidance range. Adjusted EBITDA increased to $215 million, representing a 17.2% margin, while earnings per share reached $1.62, up 2% year-over-year or 13% on a constant currency basis.

As shown in the following chart of quarterly financial performance:

The company’s trailing twelve-month free cash flow reached $360 million with a 40% conversion rate, supporting Brink’s capital allocation priorities including share repurchases and dividend increases.

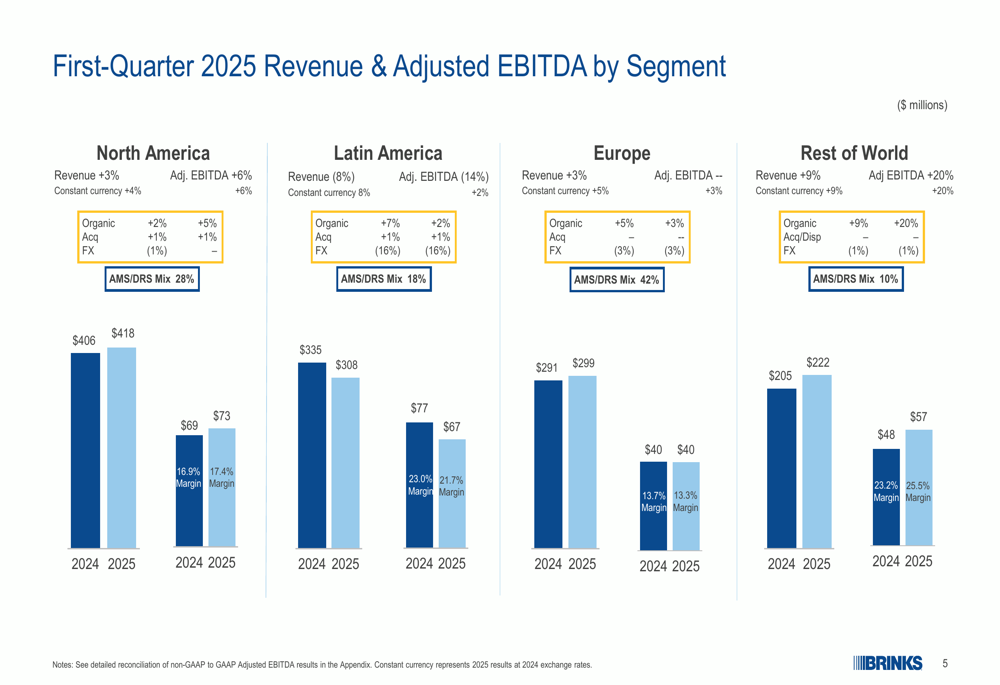

Regional performance varied significantly across markets. North America and Rest of World segments demonstrated robust growth, while Latin America faced currency headwinds despite solid underlying performance.

The following breakdown illustrates the segment performance:

"North America delivered 3% revenue growth and 6% adjusted EBITDA growth, while our Rest of World segment showed impressive 9% revenue growth and 20% EBITDA growth," noted the company in its presentation. "Latin America’s 8% revenue decline was entirely due to foreign exchange impacts, as the segment achieved 8% growth on a constant currency basis."

Strategic Initiatives

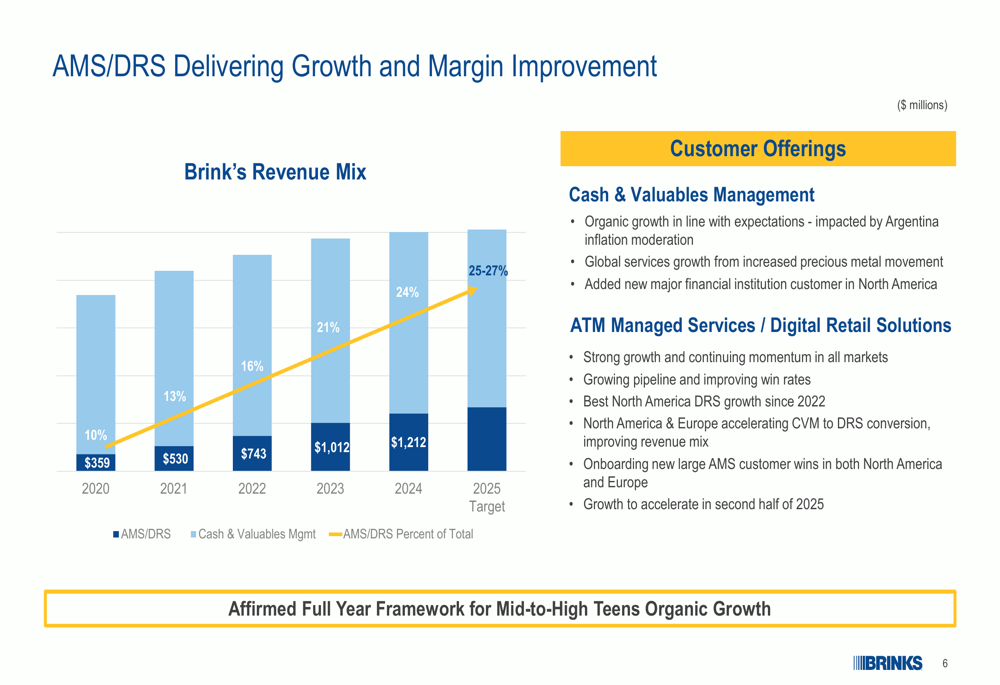

Brink’s continues to execute on its strategy of shifting toward higher-margin digital solutions. The company’s ATM Managed Services and Digital Retail Solutions (AMS/DRS) segment exceeded 20% organic growth in the quarter, maintaining the strong momentum seen in previous periods.

The following chart illustrates the company’s revenue mix evolution:

The AMS/DRS business now represents 25% of total revenue, up from just 10% in 2020, and is on track to reach the company’s 2025 target of 25-27%. This shift is significant as these services typically generate higher margins and more recurring revenue than traditional cash management operations.

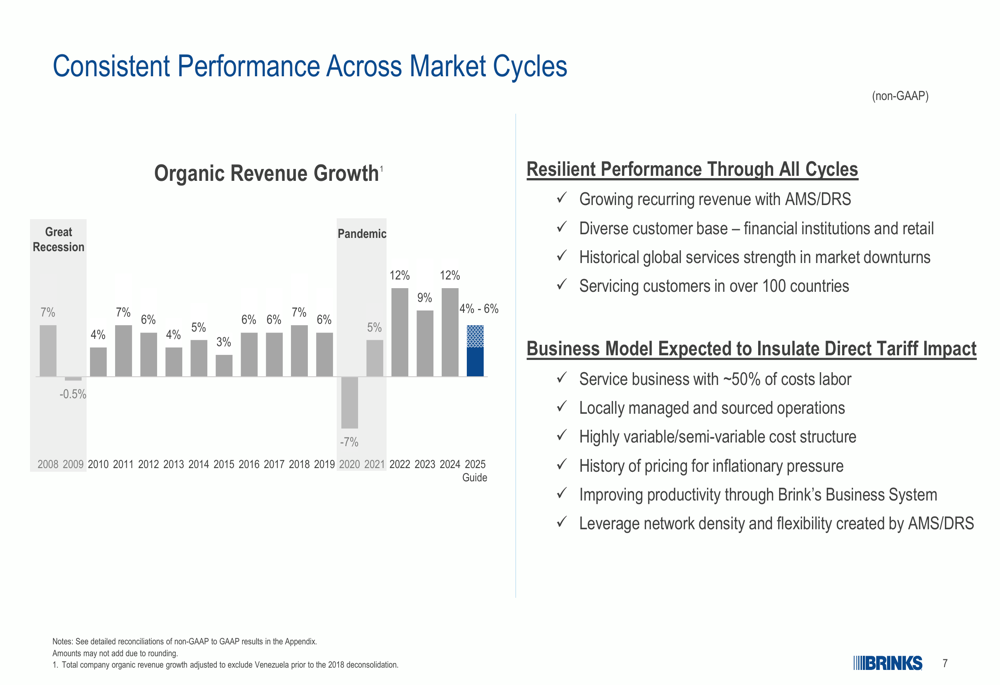

Brink’s also highlighted its resilience across economic cycles, noting consistent organic growth through both the Great Recession and the COVID-19 pandemic:

This long-term performance trend supports the company’s assertion that its business model provides insulation from direct tariff impacts and broader economic volatility.

Detailed Financial Analysis

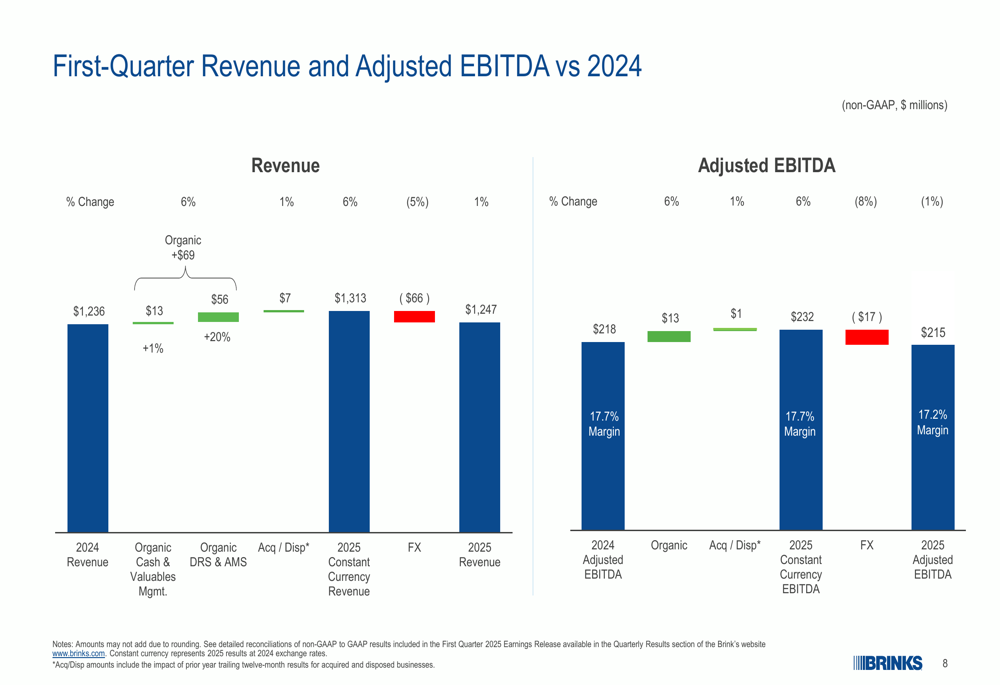

A closer examination of the year-over-year performance reveals the significant impact of foreign exchange on results. While reported revenue grew just 1%, constant currency growth reached 6%, with organic growth contributing $69 million offset by a $66 million foreign exchange headwind.

The following chart breaks down these changes:

Similarly, adjusted EBITDA growth of 1% (6% in constant currency) reflected $13 million in organic growth offset by $17 million in foreign exchange impacts.

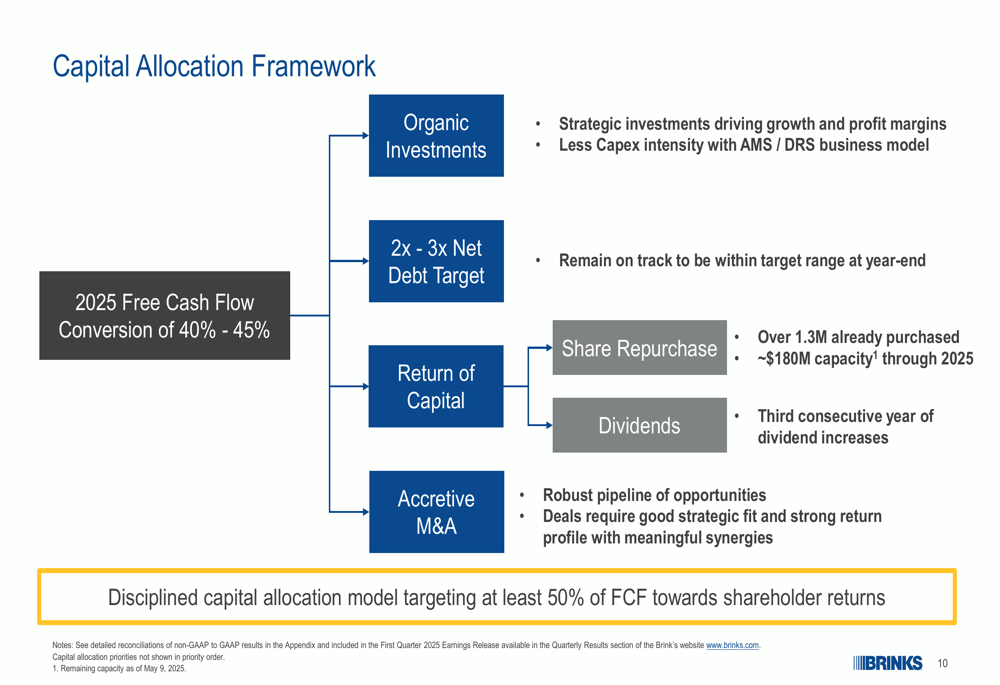

The company’s capital allocation framework remains focused on balancing growth investments with shareholder returns:

Brink’s has already repurchased over 1.3 million shares year-to-date and increased its quarterly dividend for the third consecutive year. The company targets allocating at least 50% of free cash flow to shareholder returns while maintaining a net debt ratio of 2-3x, which it expects to achieve by year-end.

Forward-Looking Statements

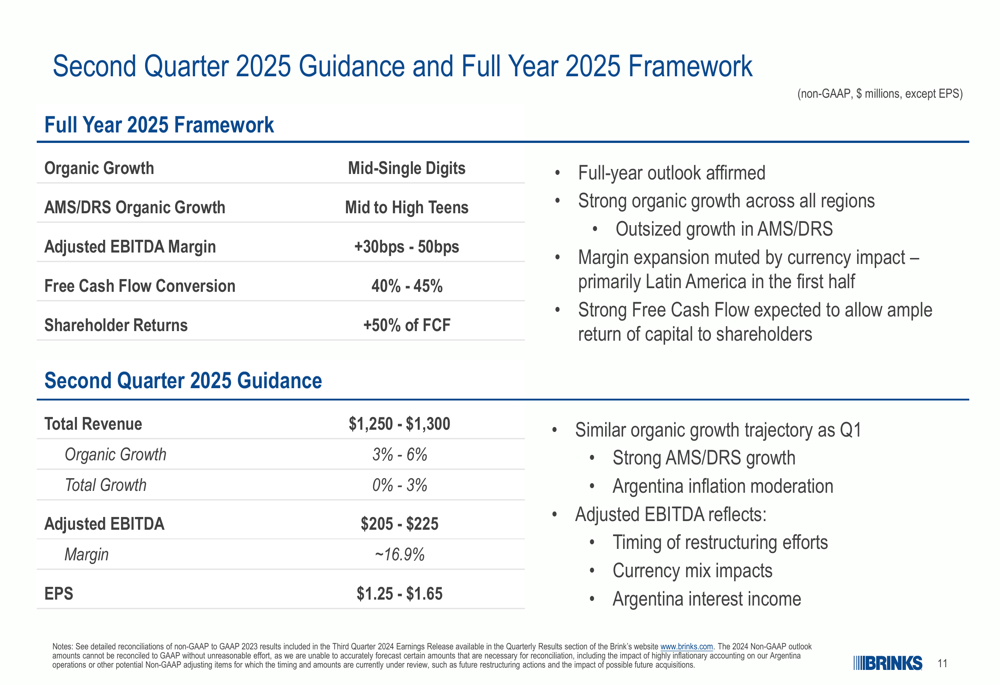

Despite mixed regional performance, Brink’s reaffirmed its full-year 2025 framework, projecting mid-single-digit organic growth with AMS/DRS organic growth in the mid to high teens. The company expects adjusted EBITDA margin expansion of 30-50 basis points and free cash flow conversion of 40-45%.

For the second quarter of 2025, Brink’s provided the following guidance:

The company expects Q2 2025 revenue between $1.25 billion and $1.3 billion, representing organic growth of 3-6% but total growth of just 0-3% due to foreign exchange impacts. Adjusted EBITDA is projected at $205-225 million with a margin of approximately 16.9%, while EPS guidance ranges from $1.25 to $1.65.

Market Context

Brink’s stock closed up 1.99% at $94.40 on the day of the earnings release, though it declined 1.51% to $92.98 in after-hours trading. This follows a pattern seen in the previous quarter, when the stock rose 4.39% despite missing EPS and revenue forecasts.

The market appears to be responding positively to the company’s strategic shift toward digital solutions and its consistent execution despite currency headwinds. With a 52-week range of $80.21 to $115.91, Brink’s stock is currently trading in the middle of its yearly range.

The Q1 2025 results suggest improvement from Q4 2024, when the company reported EPS of $2.12 (missing the $2.48 forecast) and revenue of $1.26 billion (below the expected $1.3 billion). The reaffirmed full-year guidance indicates management confidence in the company’s trajectory despite previous quarter challenges.

Brink’s continues to position itself as a resilient player in the cash management and digital solutions space, with a proven track record of performance across economic cycles and a clear strategy focused on higher-margin services.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.