Cigna earnings beat by $0.04, revenue topped estimates

Brown & Brown Inc (NYSE:BRO) reported second-quarter 2025 results on July 28, showing 9.1% revenue growth but a 13.3% decline in GAAP earnings per share. The insurance broker’s stock fell 2.03% in premarket trading to $100.50 following the release, as investors reacted to the mixed performance.

Quarterly Performance Highlights

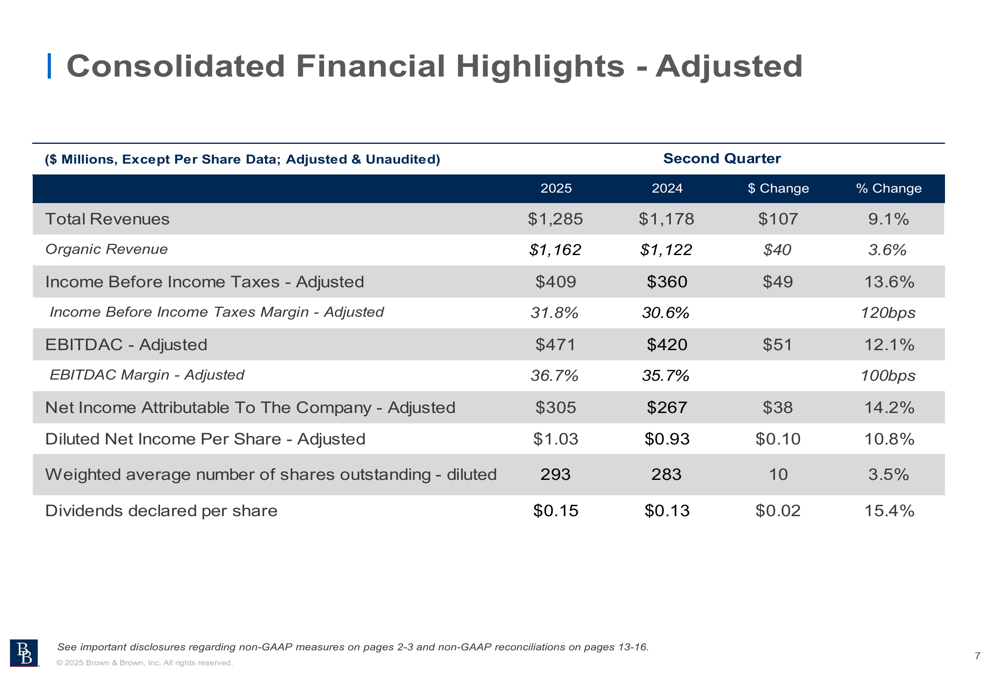

Brown & Brown delivered total revenue of $1.3 billion in Q2 2025, representing 9.1% growth compared to the same period last year. Organic revenue growth, which excludes the impact of acquisitions and dispositions, was more modest at 3.6%. The company’s adjusted EBITDAC margin improved to 36.7%, up 100 basis points year-over-year, reflecting operational efficiency gains.

However, diluted net income per share decreased 13.3% to $0.78, while adjusted diluted net income per share increased 10.8% to $1.03. This significant gap between GAAP and adjusted figures was primarily due to acquisition-related costs, amortization, and changes in estimated acquisition earn-out payables.

As shown in the following quarterly results overview:

The company completed 15 acquisitions during the quarter with annual revenue of approximately $22 million, continuing its strategy of growth through acquisition.

Segment Performance Analysis

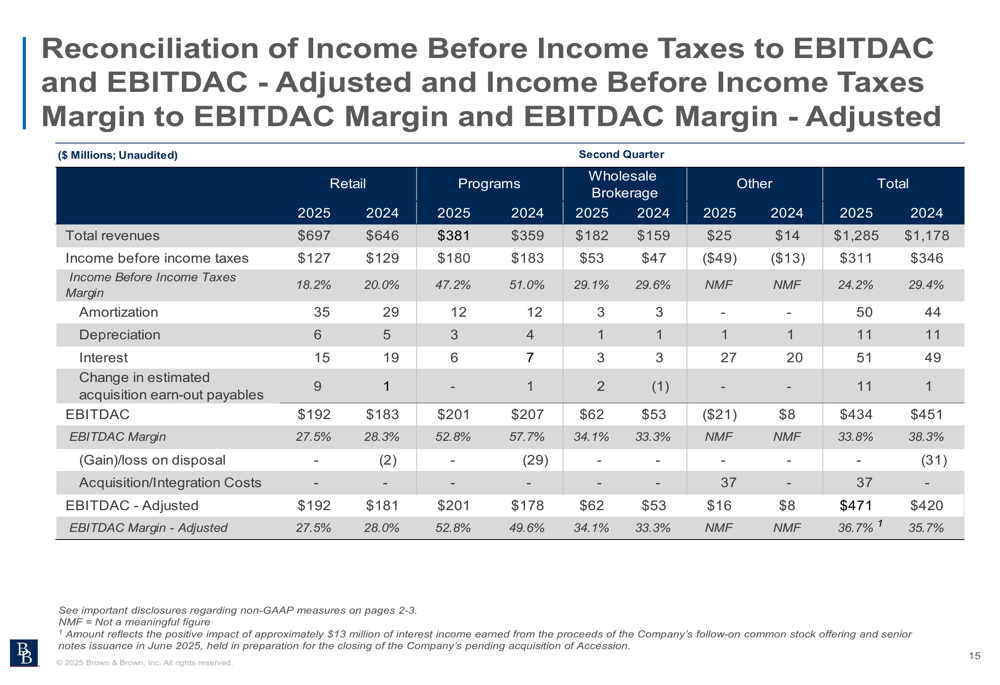

Brown & Brown’s business is divided into three main segments, each showing different organic growth rates in Q2 2025. The Retail segment, which is the largest by revenue, posted 3.0% organic growth. The Programs segment led with 4.6% organic growth, while Wholesale Brokerage achieved 3.9% organic growth.

The following segment breakdown illustrates these growth rates:

The Programs segment demonstrated the strongest performance with adjusted EBITDAC increasing 12.9% to $201 million and margins expanding to 52.8% from 49.6% in the prior year. This improvement was driven by organic revenue growth and higher profit-sharing contingent commissions.

The detailed financial results for the Programs segment show:

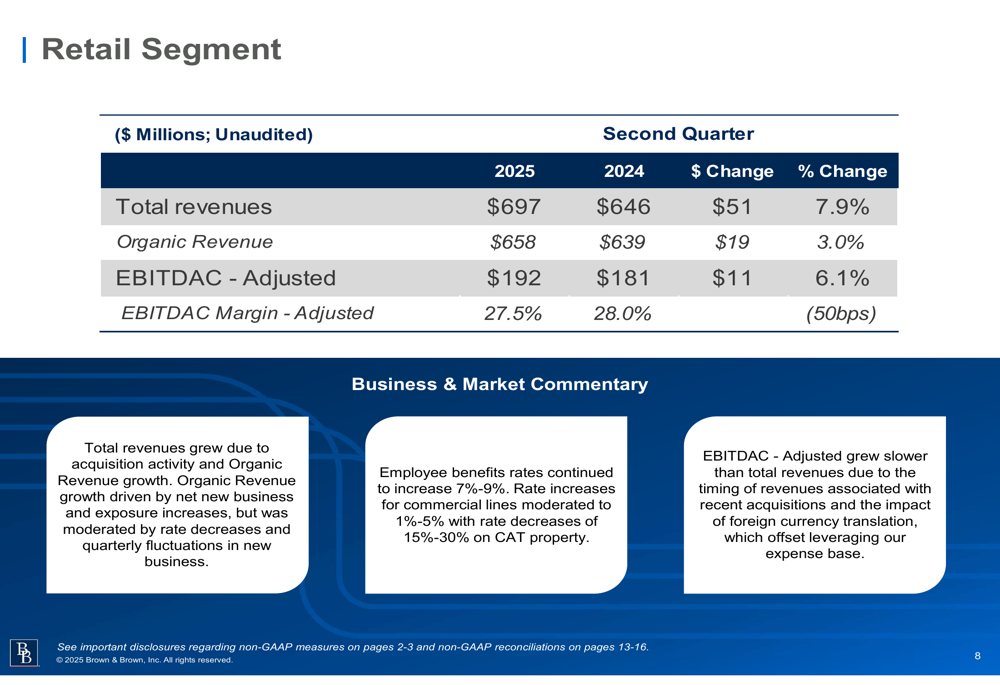

The Retail segment, which accounts for more than half of the company’s revenue, saw total revenues increase 7.9% to $697 million. However, its adjusted EBITDAC margin decreased slightly to 27.5% from 28.0% in Q2 2024. The company attributed this to "the timing of revenues associated with recent acquisitions and the impact of foreign currency translation."

The Wholesale Brokerage segment delivered the strongest total revenue growth at 14.5%, reaching $182 million. Its adjusted EBITDAC increased 17.0% to $62 million, with margins improving to 34.1% from 33.3%.

Detailed Financial Analysis

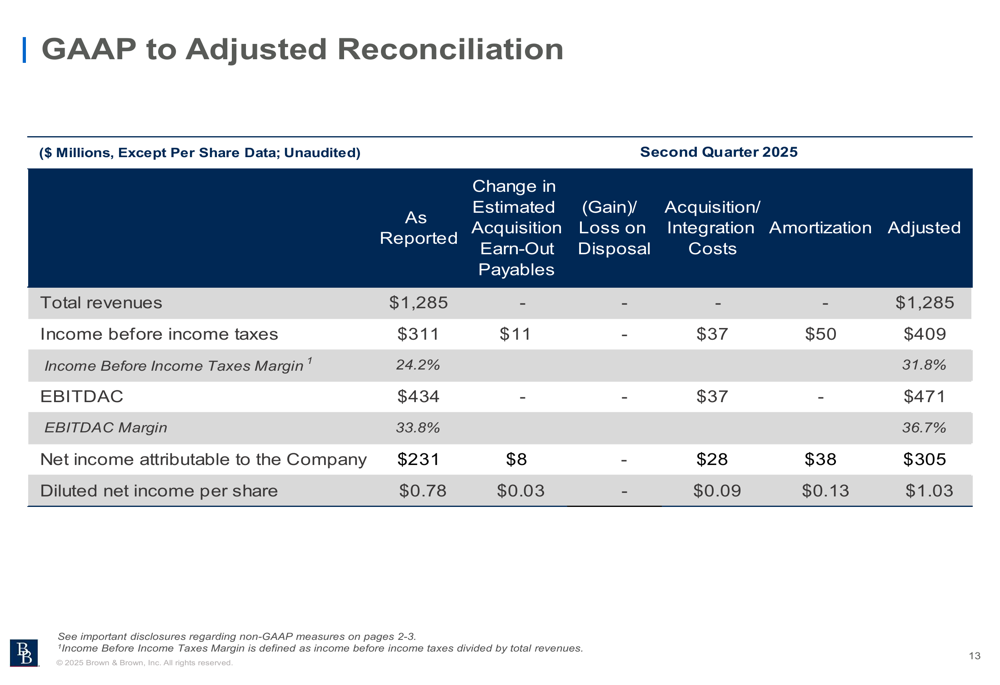

The consolidated financial highlights reveal the extent of adjustments made to Brown & Brown’s GAAP results. The company reported $311 million in income before income taxes under GAAP accounting, but after adjustments for acquisition costs, amortization, and changes in estimated acquisition earn-out payables, the adjusted figure rose to $409 million.

The reconciliation between GAAP and adjusted figures is detailed below:

These adjustments significantly impact the earnings per share figures, with GAAP diluted EPS of $0.78 increasing to $1.03 on an adjusted basis. The prior year comparison shows similar adjustments:

The company’s organic revenue calculation, which is a key metric for investors assessing underlying business performance, shows how acquisitions contributed to overall growth:

Market Environment and Strategic Outlook

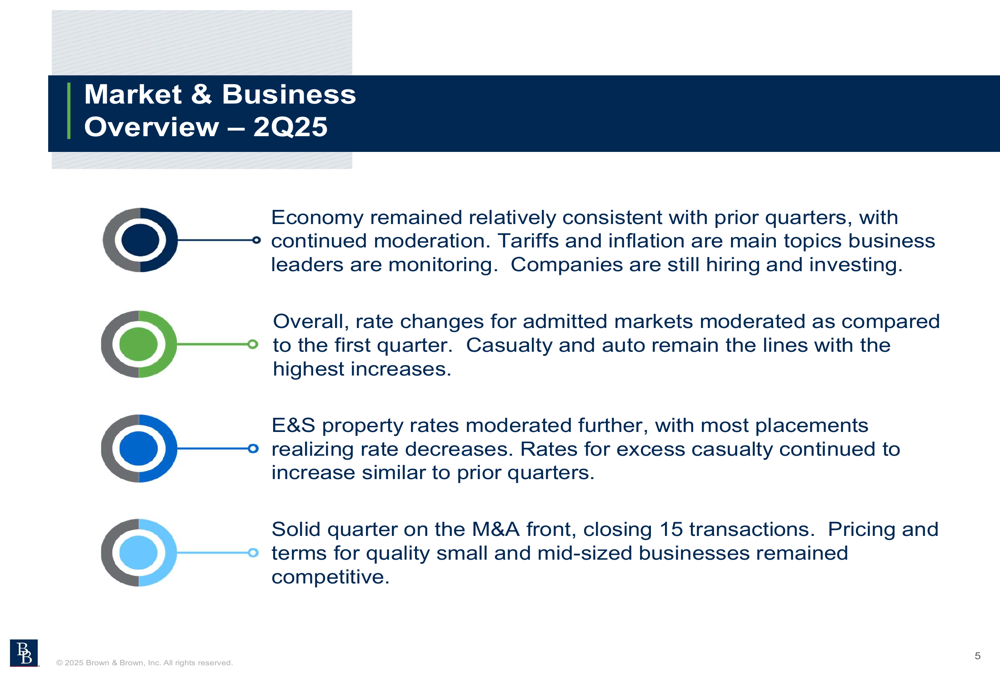

Brown & Brown reported that the economic environment remained consistent with prior quarters, with companies still hiring and investing despite ongoing monitoring of tariffs and inflation. In the insurance market, rate changes for admitted markets moderated compared to Q1 2025, with casualty and auto lines showing the highest increases. E&S property rates continued to moderate further.

The company noted that its Accession acquisition is on track to close August 1st, representing a significant strategic move. Management expects to remain an active acquirer of businesses going forward.

Forward-Looking Statements

Looking ahead, Brown & Brown expects admitted rate changes to remain consistent with those seen in Q2. The company anticipates continued decreases in catastrophe property rates, subject to storm claim activity. Management believes the company is well-positioned for the second half of 2025, though business investment levels may be impacted by trade negotiations, economic expansion, inflation, and interest rate changes.

The cautious outlook aligns with the company’s Q1 2025 guidance, where it projected low to mid-single-digit organic growth. The current quarter’s 3.6% organic growth falls within this range but represents a moderation from the 11.6% revenue growth reported in Q1.

The market reaction to Brown & Brown’s results suggests investors may be concerned about the declining GAAP earnings and the sustainability of growth in a moderating rate environment. However, the company’s continued acquisition strategy and margin improvements on an adjusted basis indicate management’s focus on long-term value creation despite near-term challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.