September looms as a risk month for stocks, Yardeni says

Introduction & Executive Summary

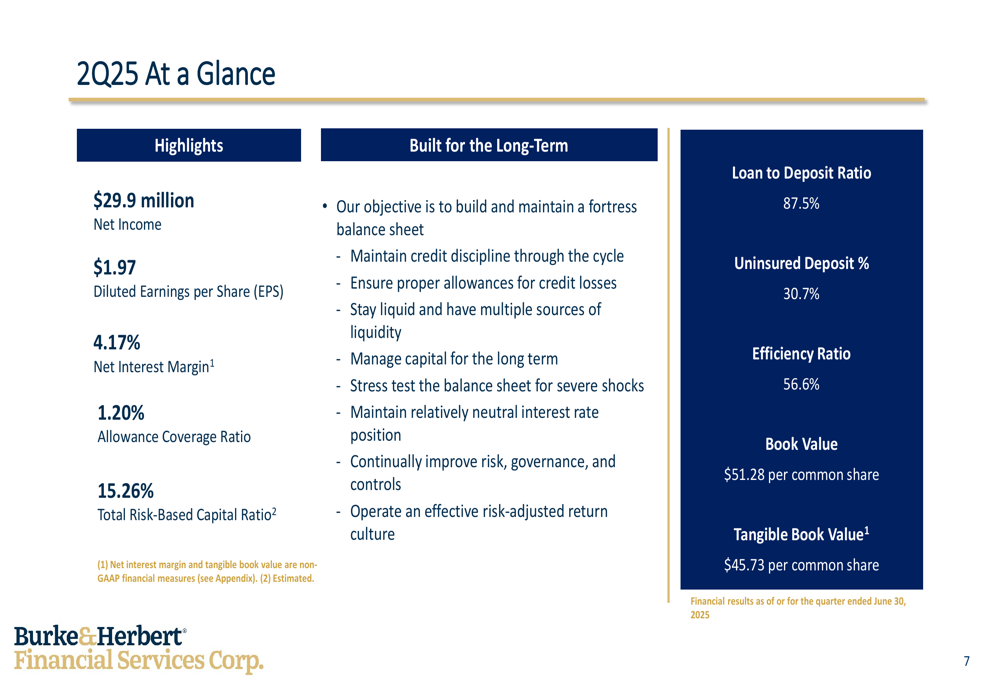

Burke & Herbert Financial Services Corp. (NASDAQ:BHRB) released its second quarter 2025 presentation on August 1, highlighting solid financial performance with $29.9 million in net income, representing a 10% increase from the previous quarter. The 173-year-old community banking institution, headquartered in Alexandria, Virginia, reported diluted earnings per share of $1.97, up from $1.80 in Q1 2025.

The bank, which operates more than 75 locations across five states, maintained strong profitability metrics with a 15.50% return on average equity and a 1.51% return on average assets. However, the presentation also revealed an increase in non-performing loans, which rose to 1.53% of total loans, up from 1.15% in the previous quarter.

As shown in the following quarterly highlights slide, Burke & Herbert achieved a net interest margin of 4.17% and maintained an efficiency ratio of 56.6%:

Quarterly Performance Highlights

The bank’s Q2 2025 financial results demonstrated continued strength in core operations. Net income applicable to common shares reached $29.7 million, up from $27.0 million in Q1 2025 and significantly improved from a loss of $17.1 million in the same quarter last year. Total (EPA:TTEF) revenue (a non-GAAP measure) increased to $87.1 million, compared to $83.0 million in the previous quarter.

Interest income remained relatively stable at $111.9 million compared to $110.8 million in Q1, while interest expense slightly decreased to $37.6 million from $37.8 million. Noninterest income showed substantial improvement, rising to $12.9 million from $10.0 million in the previous quarter, representing a 28.5% increase.

The bank’s balance sheet expanded to $8.06 billion in total assets as of June 30, 2025, up from $7.84 billion at the end of March. Book value per common share increased to $51.28, while tangible book value per share rose to $45.73, representing quarter-over-quarter improvements of 2.8% and 3.5%, respectively.

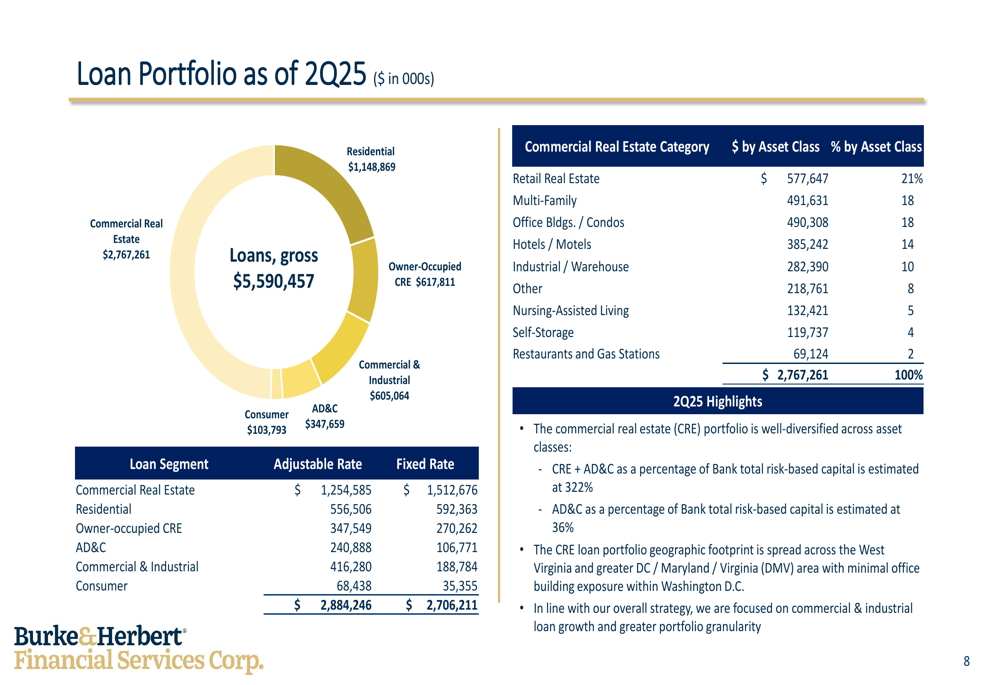

Loan and Deposit Portfolio Analysis

Burke & Herbert maintained a well-diversified loan portfolio totaling $5.59 billion as of Q2 2025. Residential loans represented the largest segment at $1.15 billion, followed by commercial real estate at $2.77 billion. The commercial real estate portfolio showed balanced diversification across various property types, with retail real estate (21%), multi-family (18%), and office buildings (18%) representing the largest segments.

The following chart illustrates the composition of the bank’s loan portfolio:

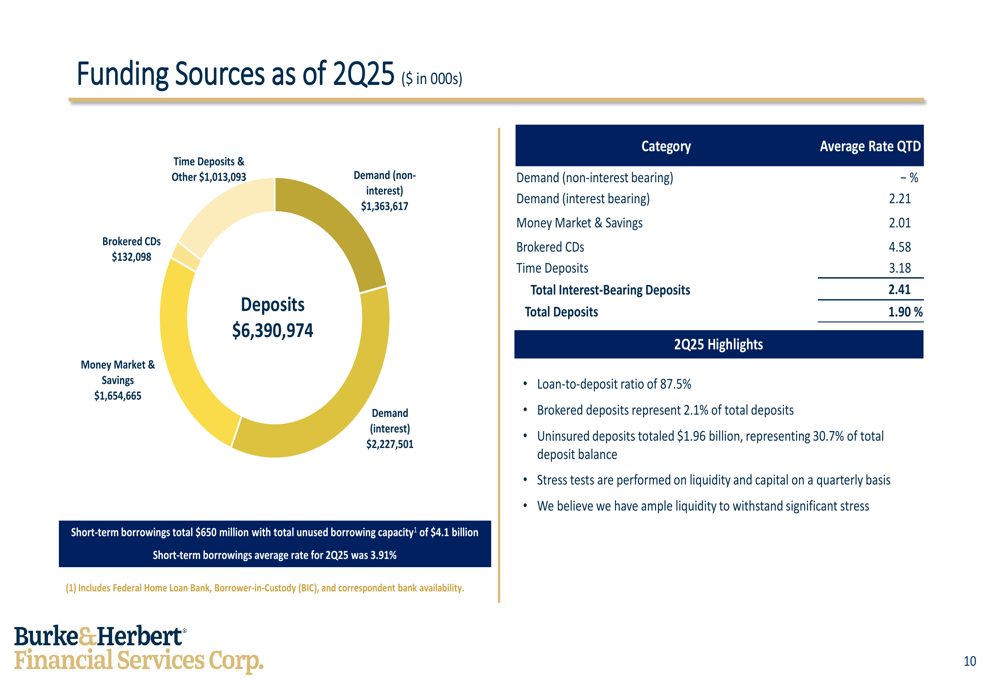

On the funding side, total deposits stood at $6.39 billion, resulting in a loan-to-deposit ratio of 87.5%. The deposit base remained stable with a healthy mix of funding sources, including $1.36 billion in non-interest-bearing demand deposits (21.3% of total deposits). Uninsured deposits totaled $1.96 billion, representing 30.7% of total deposits, while brokered deposits accounted for just 2.1%.

The bank’s funding composition is detailed in the following chart:

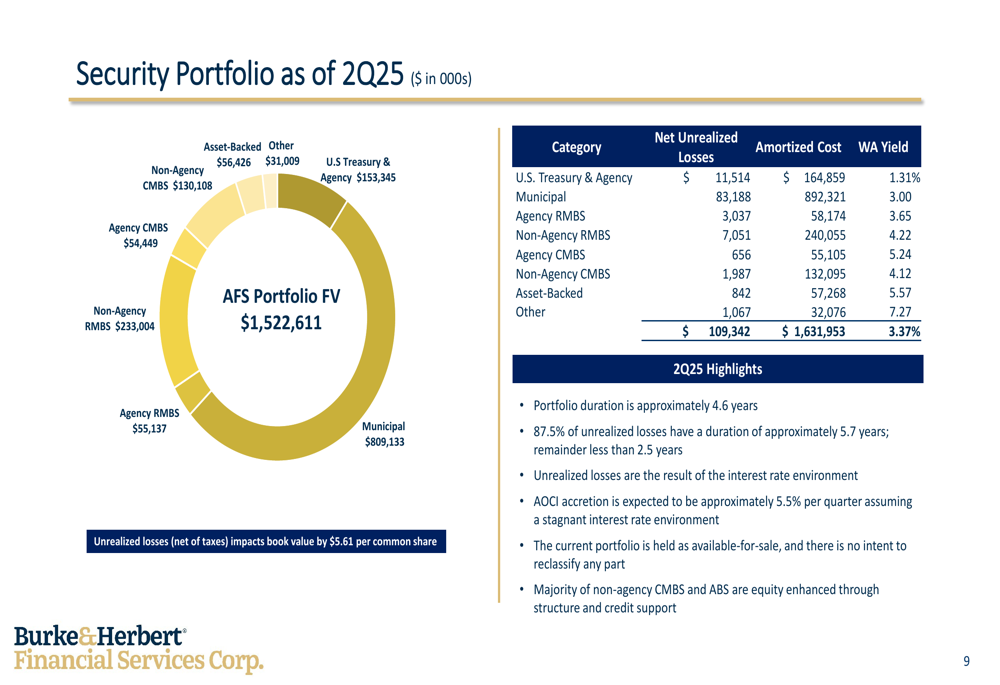

The securities portfolio, valued at $1.52 billion (fair value), consisted primarily of municipal securities ($809 million) and non-agency residential mortgage-backed securities ($233 million). The portfolio had total net unrealized losses of $109.3 million, which impacted book value by $5.61 per common share. The weighted average yield on the securities portfolio was 3.37%, with a duration of approximately 4.6 years.

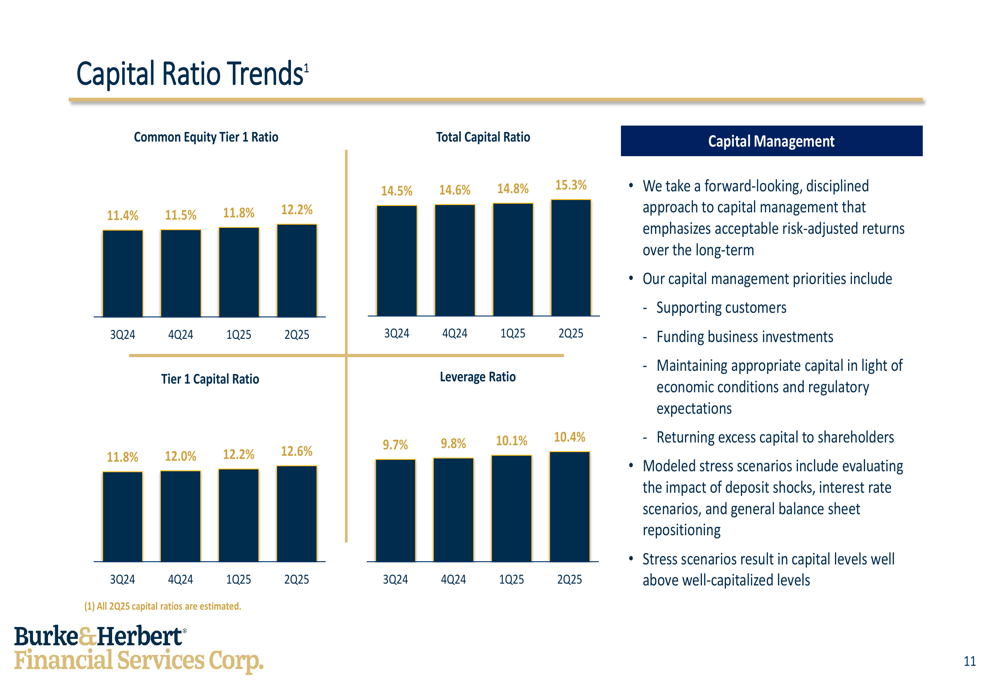

Capital and Asset Quality Trends

Burke & Herbert continued to strengthen its capital position during the quarter, with all regulatory capital ratios showing improvement. The Common Equity Tier 1 ratio increased to 12.2% from 11.8% in Q1 2025, while the Total Capital Ratio rose to 15.3% from 14.8%. These improving trends reflect the bank’s disciplined approach to capital management and strong earnings retention.

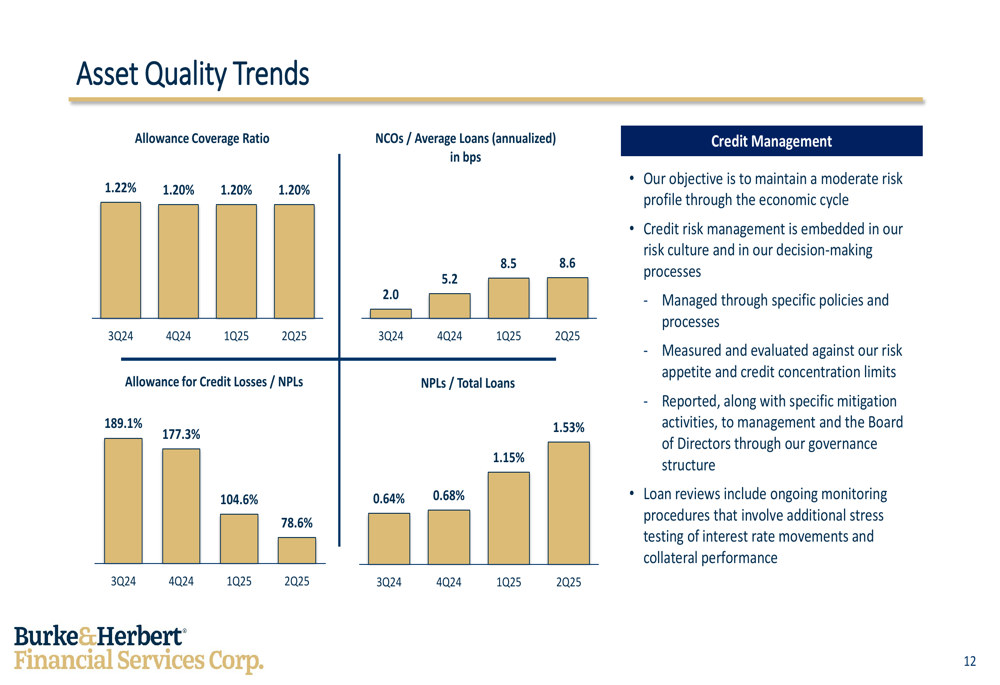

Despite the overall strong performance, asset quality metrics showed some deterioration. While the allowance coverage ratio remained stable at 1.20%, non-performing loans increased to 1.53% of total loans, up from 1.15% in the previous quarter. Consequently, the allowance for credit losses to non-performing loans ratio declined to 78.6% from 104.6% in Q1 2025.

Net charge-offs to average loans (annualized) remained relatively stable at 8.6 basis points, compared to 8.5 basis points in the previous quarter, suggesting that while more loans are being classified as non-performing, the actual loss experience has not significantly changed.

Strategic Positioning and Outlook

Burke & Herbert continues to position itself as a quintessential community bank with a relationship-driven business model. The bank’s strategic priorities include maintaining and expanding its trusted advisor relationship model, pursuing new market opportunities, and delivering a full suite of expected products and services.

The presentation emphasized the bank’s long-term approach to business, focusing on maintaining a moderate risk profile through economic cycles. Management highlighted their commitment to building a fortress balance sheet with disciplined credit standards, strong liquidity, and effective capital management.

With more than 173 years of history and a multi-generational customer base, Burke & Herbert leverages its reputation and local decision-making capabilities to compete effectively in its markets. The bank’s presence in the high-growth Washington D.C. metropolitan area provides opportunities for continued expansion and deeper market penetration.

While the increase in non-performing loans bears watching, the bank’s strong capital position, consistent profitability, and disciplined risk management approach suggest it is well-positioned to navigate potential challenges in the economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.