US stock futures dip as Nvidia earnings spark little cheer

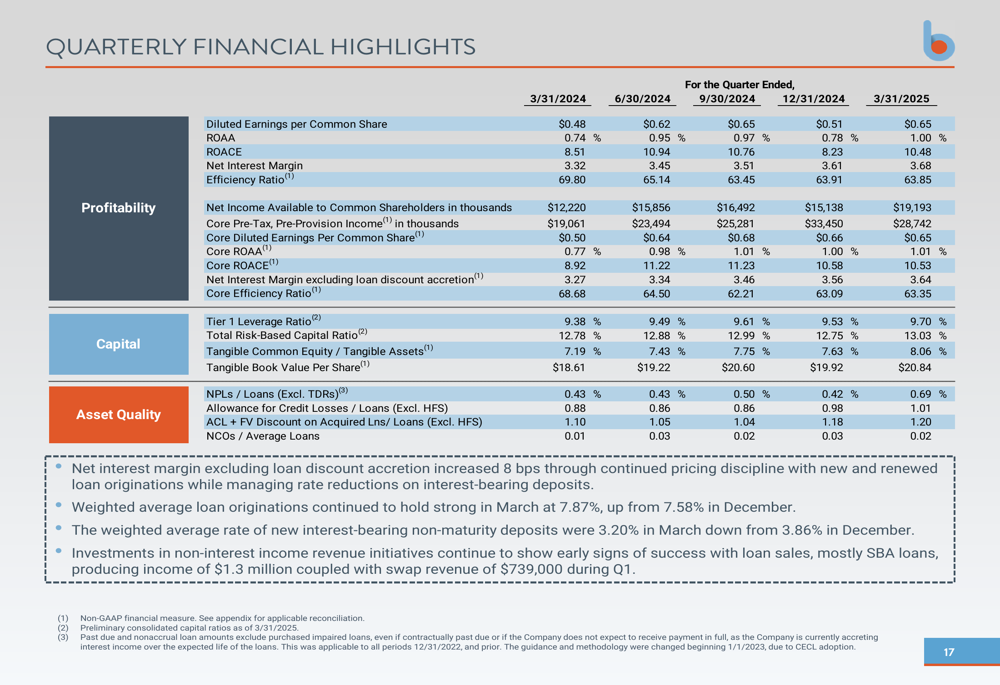

Business First Bancshares, Inc. (NASDAQ:BFST) released its first quarter 2025 earnings presentation on April 24, showing improved profitability metrics and continued execution of its growth strategy. The Louisiana-headquartered bank reported diluted earnings per share of $0.65, up from $0.51 in the previous quarter, while its net interest margin expanded to 3.68%.

Quarterly Performance Highlights

Business First reported a return on average assets (ROAA) of 1.00% for Q1 2025, improving from 0.78% in Q4 2024. Return on average common equity (ROACE) reached 10.48%, up from 8.23% in the previous quarter. The company’s net interest margin continued its upward trajectory, reaching 3.68% compared to 3.61% in Q4 2024 and 3.32% in the same quarter last year.

As shown in the following quarterly financial highlights chart, the bank has demonstrated consistent improvement in key profitability metrics over the past five quarters:

Net income available to common shareholders reached $19.2 million for the quarter, up from $15.1 million in Q4 2024. The efficiency ratio improved slightly to 63.85% from 63.91% in the previous quarter, while the core efficiency ratio improved to 63.35% from 63.09%.

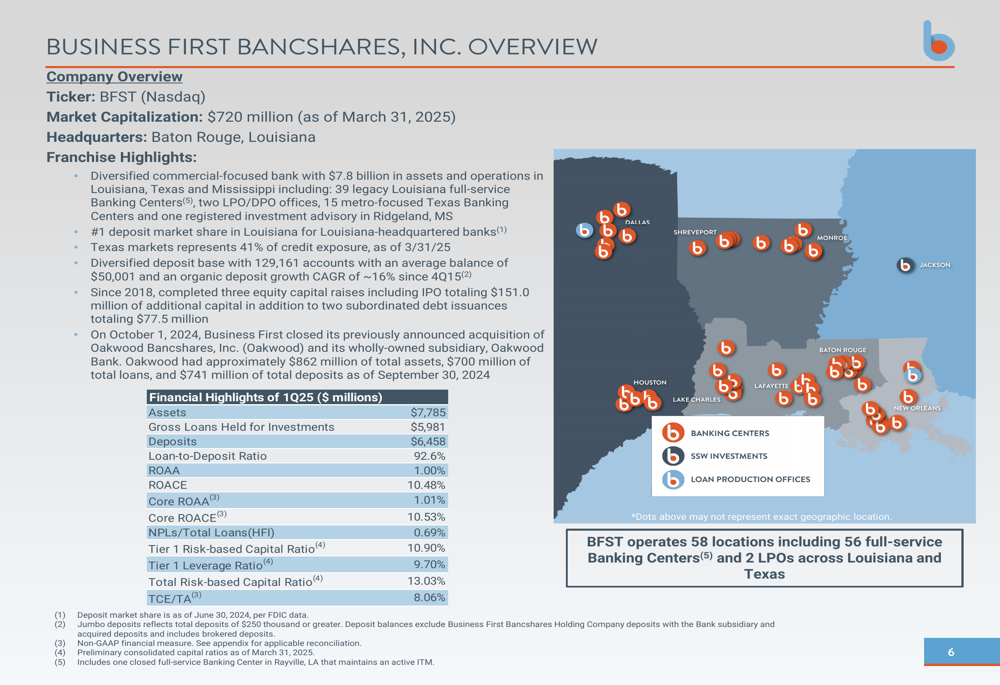

Company Overview and Strategic Positioning

Business First Bancshares operates as a diversified commercial-focused bank with $7.8 billion in assets across Louisiana, Texas, and Mississippi. The bank maintains 58 locations and holds the #1 deposit market share in Louisiana among Louisiana-headquartered banks. Texas markets represent 41% of the bank’s credit exposure as of March 31, 2025.

The following overview highlights the bank’s key financial metrics and geographic footprint:

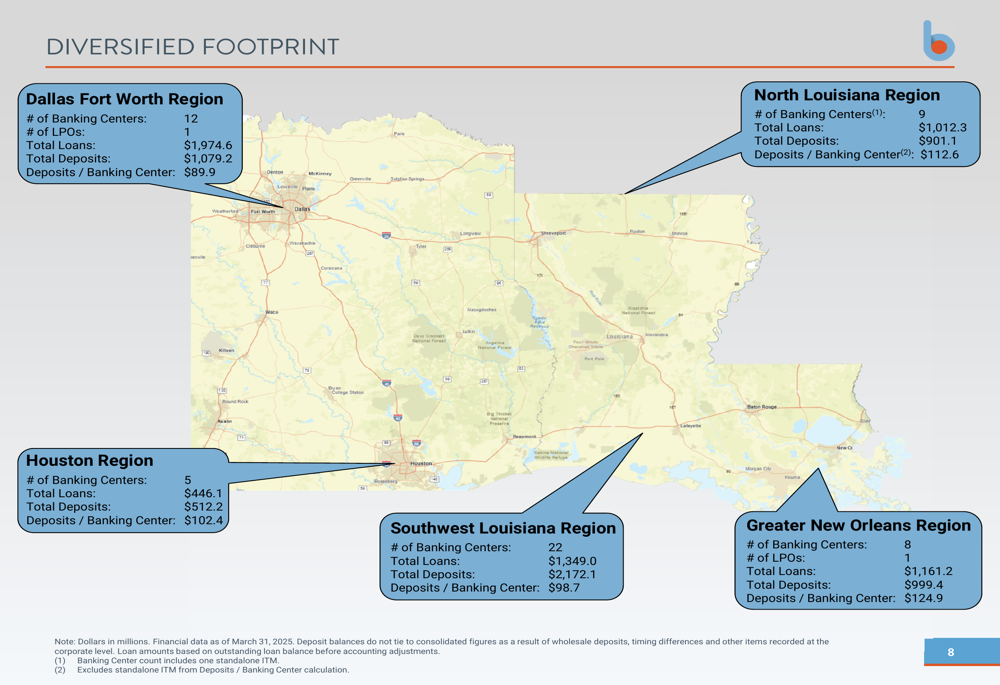

The bank’s diversified footprint spans multiple regions, with significant presence in Dallas-Fort Worth, North Louisiana, Houston, Southwest Louisiana, and Greater New Orleans. This regional diversification provides stability and multiple growth avenues.

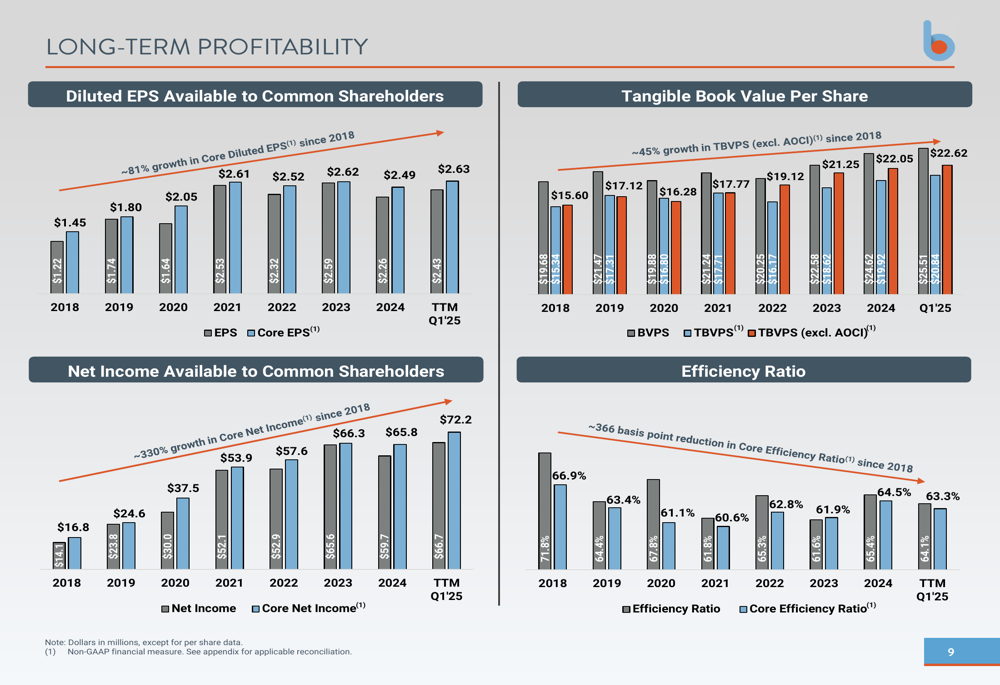

Long-Term Growth Strategy

Business First has demonstrated consistent long-term growth through both organic initiatives and strategic acquisitions. Since 2018, the bank has achieved approximately 81% growth in core diluted EPS, 45% growth in tangible book value per share, and 330% growth in core net income.

The following chart illustrates the bank’s long-term profitability trends:

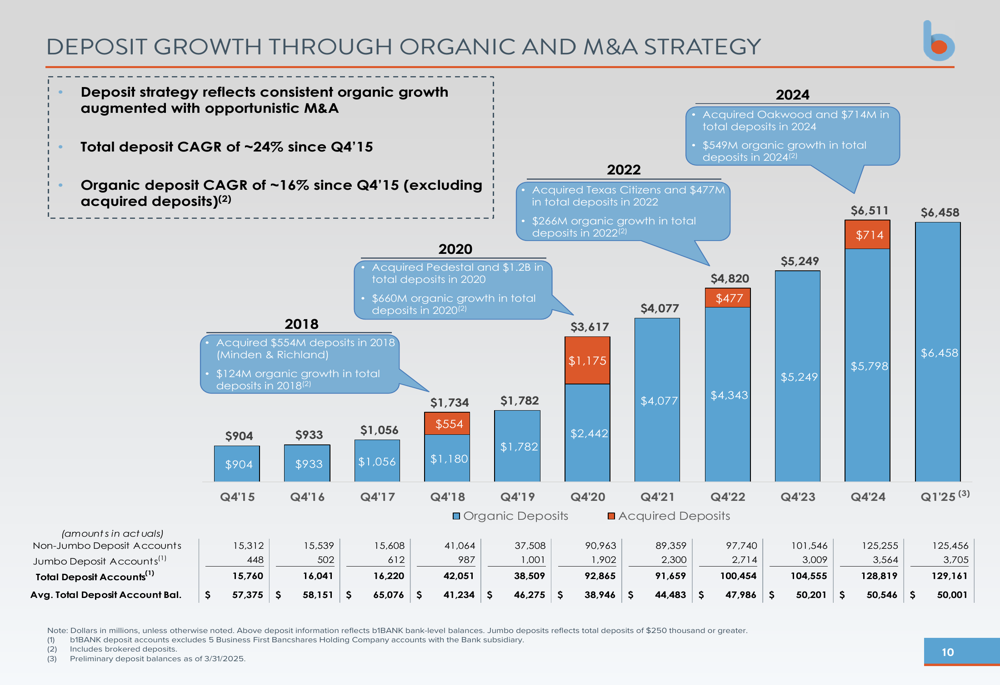

A key component of the bank’s growth strategy has been its deposit growth, which has shown a compound annual growth rate (CAGR) of approximately 24% since Q4 2015. Organic deposit growth, excluding acquired deposits, has maintained a CAGR of approximately 16% during the same period.

The following chart demonstrates this deposit growth trajectory:

M&A Strategy and Execution

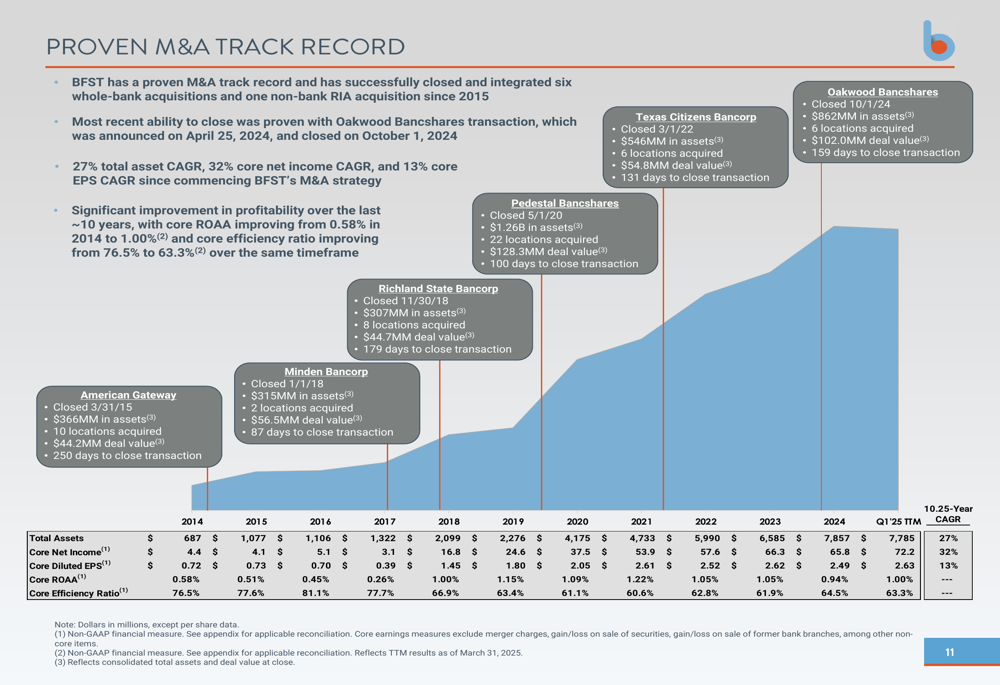

Business First has established a proven track record in mergers and acquisitions, having successfully closed and integrated six whole-bank acquisitions and one non-bank RIA acquisition since 2015. The most recent acquisition was Oakwood Bancshares, which closed on October 1, 2024.

These strategic acquisitions have contributed significantly to the bank’s growth, resulting in a 27% total asset CAGR, 32% core net income CAGR, and 13% core EPS CAGR since commencing its M&A strategy.

The following slide details the bank’s acquisition history and impact:

Balance Sheet and Liquidity Management

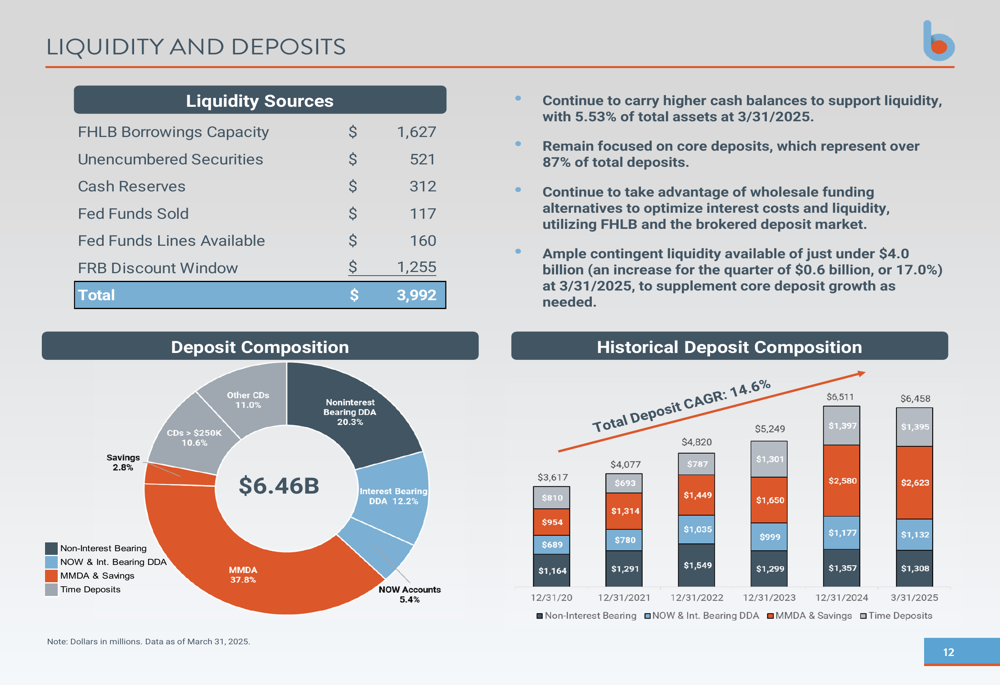

As of March 31, 2025, Business First reported total assets of $7.8 billion, gross loans held for investment of $6.0 billion, and total deposits of $6.5 billion, resulting in a loan-to-deposit ratio of 92.6%.

The bank maintains strong liquidity with multiple sources totaling nearly $4.0 billion, including FHLB borrowing capacity, unencumbered securities, cash reserves, Fed funds, and Federal Reserve discount window access. This represents an increase of $0.6 billion, or 17.0%, from the previous quarter.

The following chart details the bank’s liquidity sources and deposit composition:

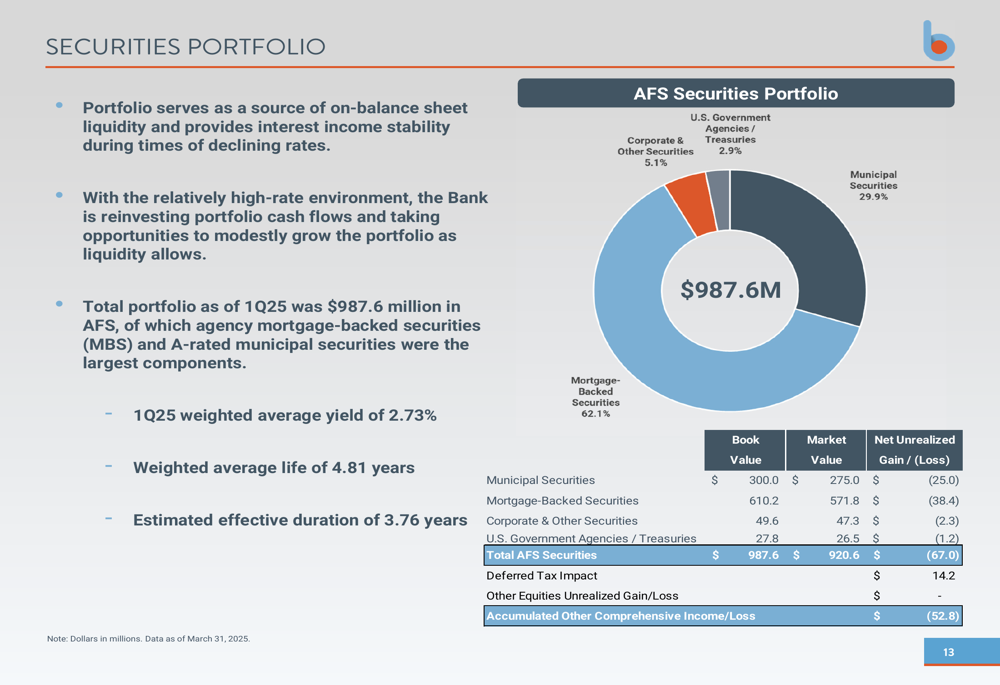

The bank’s securities portfolio, which serves as a source of on-balance sheet liquidity, totaled $987.6 million in available-for-sale (AFS) securities as of Q1 2025. The portfolio has a weighted average yield of 2.73%, a weighted average life of 4.81 years, and an estimated effective duration of 3.76 years.

Credit Quality and Loan Portfolio

Business First reported flat loan balances for the quarter, with a slight 0.03% annualized decrease. Real estate construction loans decreased by $36.8 million, while residential real estate loans increased by $49.8 million.

The allowance for credit losses plus fair value discount on acquired loans stood at $71.7 million, representing 1.20% of total loans. Non-performing loans to total loans increased to 0.69% from 0.42% in the previous quarter.

Forward Outlook

The bank continues to focus on optimizing its branch network and developing noninterest revenue opportunities. Weighted average loan originations remained strong at 7.87% in March, up from 7.58% in December, while the weighted average rate of new interest-bearing non-maturity deposits decreased to 3.20% in March from 3.86% in December.

Noninterest income initiatives are showing early signs of success, with loan sales (mostly SBA (LON:SBA) loans) producing $1.3 million in income and swap revenue contributing $739,000 during Q1 2025.

Despite the positive Q1 results, Business First’s stock has declined since its Q4 2024 earnings announcement, when it traded at $27.69 following an 8.84% post-earnings surge. According to the latest data, the stock is currently trading at $23.64, suggesting investors may be reassessing the bank’s valuation despite its improved profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.