Nvidia’s results, Tesla’s European sales, Japan trade - what’s moving markets

Introduction & Market Context

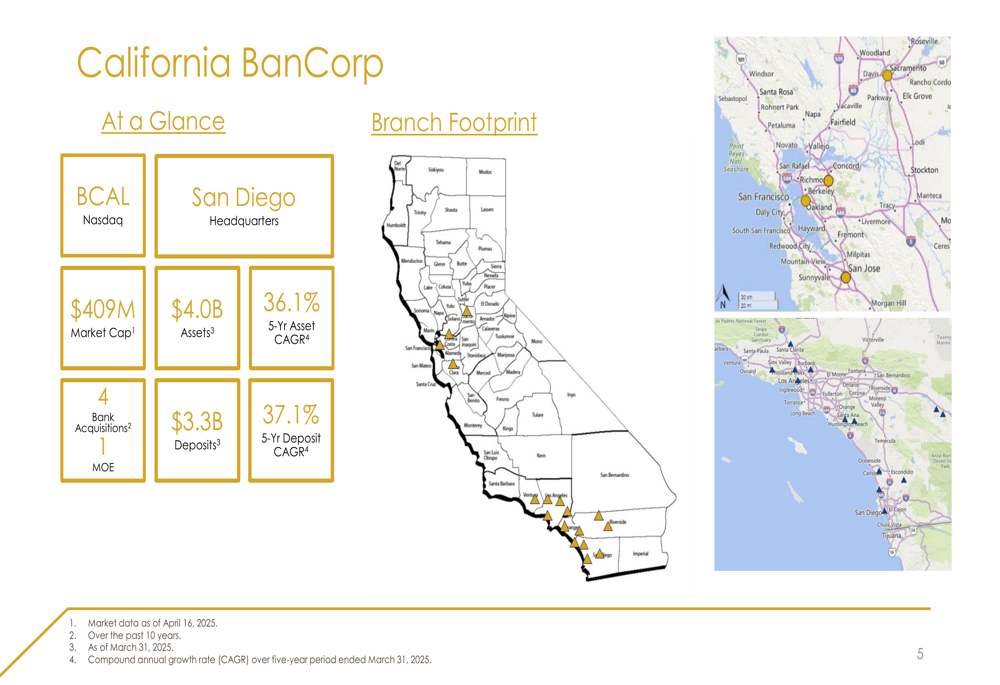

California BanCorp (NASDAQ:BCAL), formed through the merger of Southern California Bancorp and California BanCorp that closed on July 31, 2024, has released its investor presentation highlighting the bank’s financial performance and strategic positioning as of March 31, 2025. The bank operates in both Northern and Southern California, serving the small to middle-market business banking segments in what it describes as the largest banking market in the United States.

As shown in the following overview of the bank’s market position and footprint, California BanCorp has established a significant presence across the state, with a market capitalization of $409 million as of mid-April 2025:

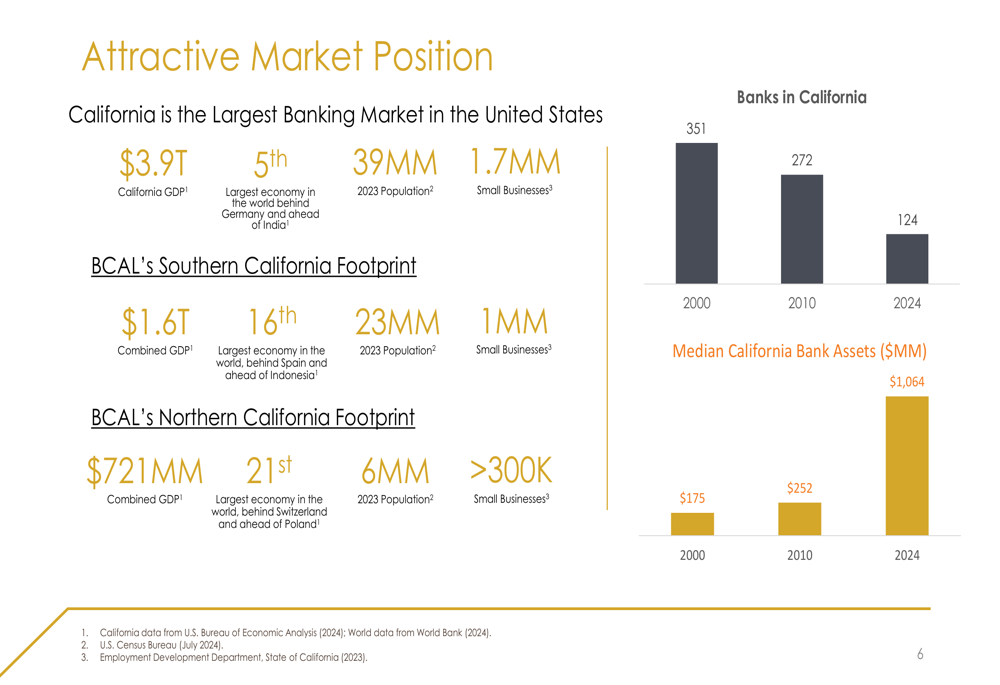

The bank operates in a market that has seen significant consolidation over the past two decades, with the number of banks in California decreasing from 351 in 2000 to just 124 in 2024, while the median bank assets have grown from $175 million to over $1 billion during the same period. This consolidation trend has created opportunities for mid-sized institutions like California BanCorp to expand their market share.

As illustrated in this chart showing the California banking market consolidation and the bank’s strategic positioning:

Quarterly Performance Highlights

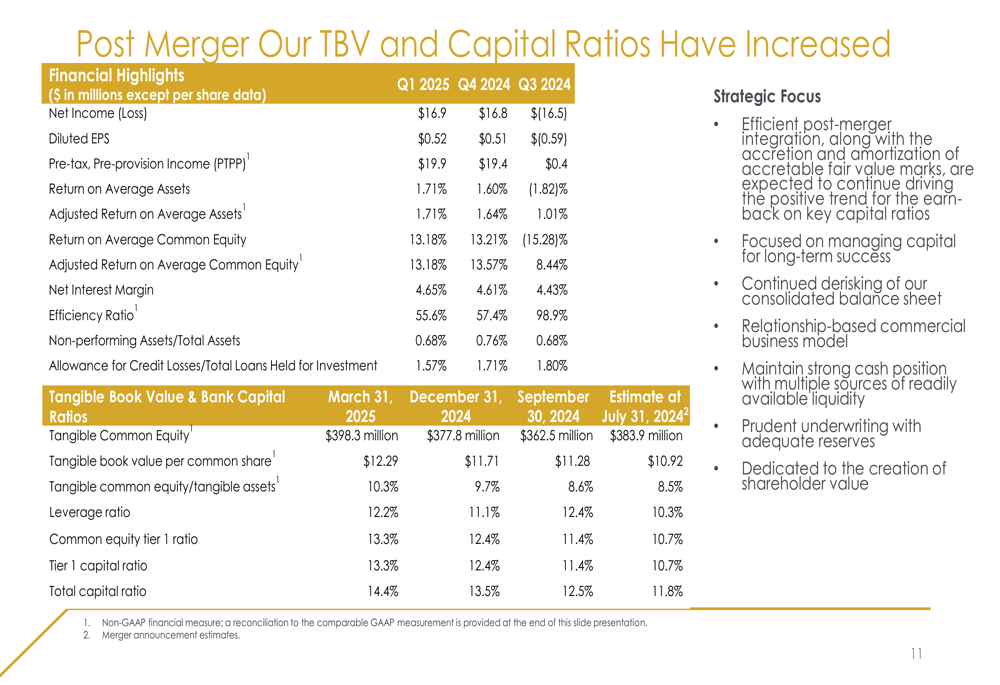

California BanCorp reported strong financial performance for the first quarter of 2025, with net income of $16.9 million, or $0.52 per diluted share, slightly up from $16.8 million, or $0.51 per diluted share, in the fourth quarter of 2024. This represents a significant improvement from the $16.5 million loss reported in the third quarter of 2024, which included merger-related expenses.

The bank’s pre-tax, pre-provision income reached $19.9 million in Q1 2025, up from $19.4 million in Q4 2024. Return on average assets improved to 1.71% from 1.60% in the previous quarter, while the efficiency ratio improved to 55.6% from 57.4%.

These key financial metrics are summarized in the following table, showing the consistent improvement in performance since the merger:

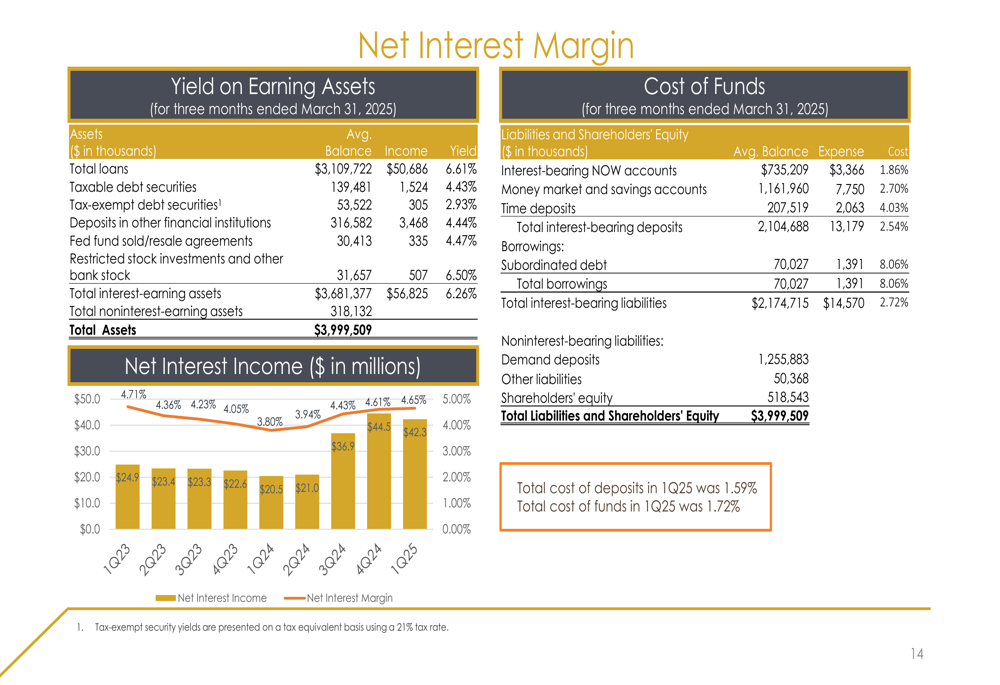

Net interest margin, a critical measure of banking profitability, continued its upward trend, reaching 4.65% in Q1 2025, compared to 4.61% in Q4 2024 and 4.43% in Q3 2024. This improvement reflects the bank’s ability to manage its yield on earning assets and cost of funds effectively in the current interest rate environment.

The following chart illustrates the bank’s net interest income and margin trends over the past nine quarters:

Balance Sheet Strength and Capital Position

As of March 31, 2025, California BanCorp reported total assets of $3.98 billion, slightly down from $4.03 billion at the end of 2024. Total (EPA:TTEF) loans stood at $3.07 billion, while deposits totaled $3.34 billion. The bank maintains a strong capital position, with all regulatory capital ratios well above the requirements to be considered "well-capitalized."

The bank’s tangible book value per share has shown consistent growth since the merger, increasing from $10.92 at the time of merger closing to $12.29 as of March 31, 2025. Similarly, the tangible common equity to tangible assets ratio improved to 10.3% from 8.5% at merger closing.

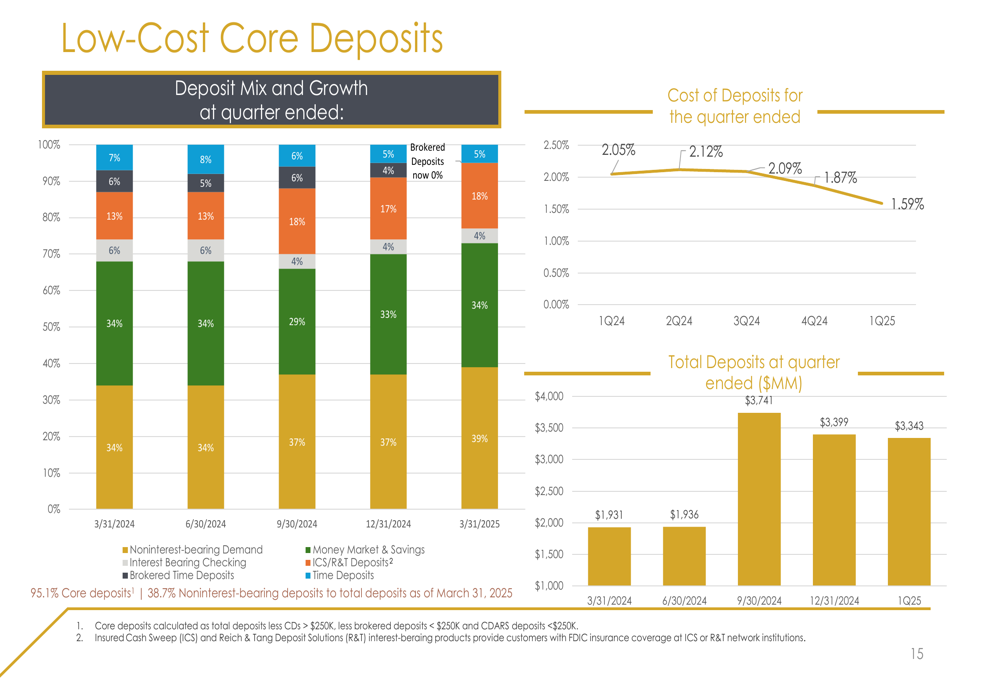

California BanCorp has maintained a favorable deposit mix, with 38.7% of total deposits being noninterest-bearing as of March 31, 2025. This low-cost core deposit base has helped the bank reduce its overall cost of deposits to 1.59% in Q1 2025, down from 1.87% in Q4 2024 and 2.09% in Q3 2024.

The following chart shows the bank’s deposit mix and cost trends:

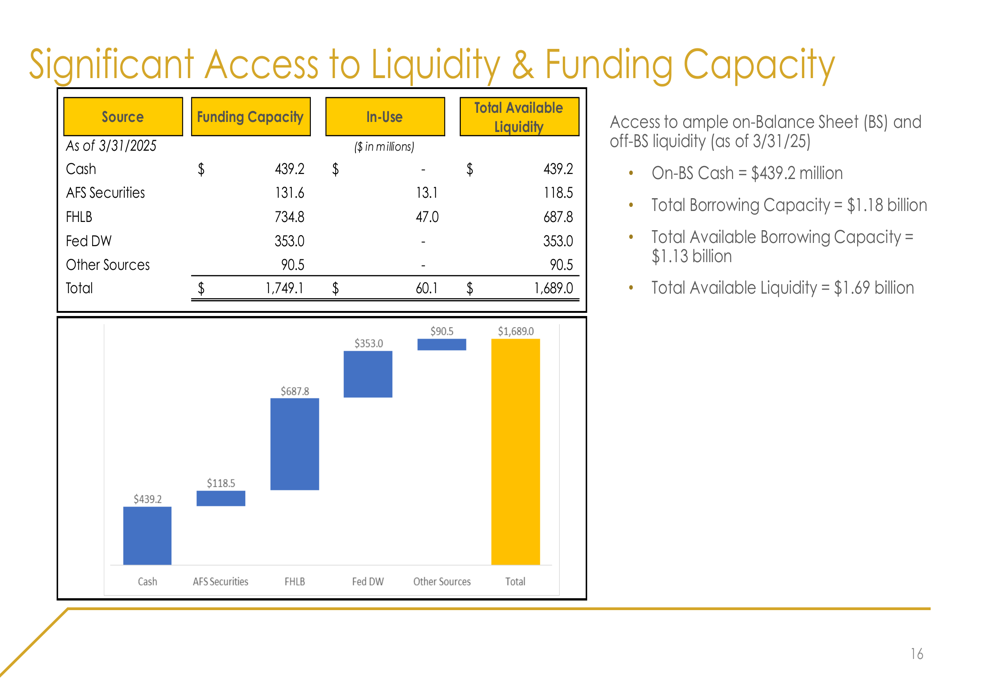

The bank also maintains significant liquidity, with total available liquidity of $1.69 billion as of March 31, 2025, including $439.2 million in cash and $1.13 billion in available borrowing capacity. This strong liquidity position provides flexibility for future growth opportunities.

As illustrated in this breakdown of the bank’s liquidity sources:

Strategic Growth Initiatives

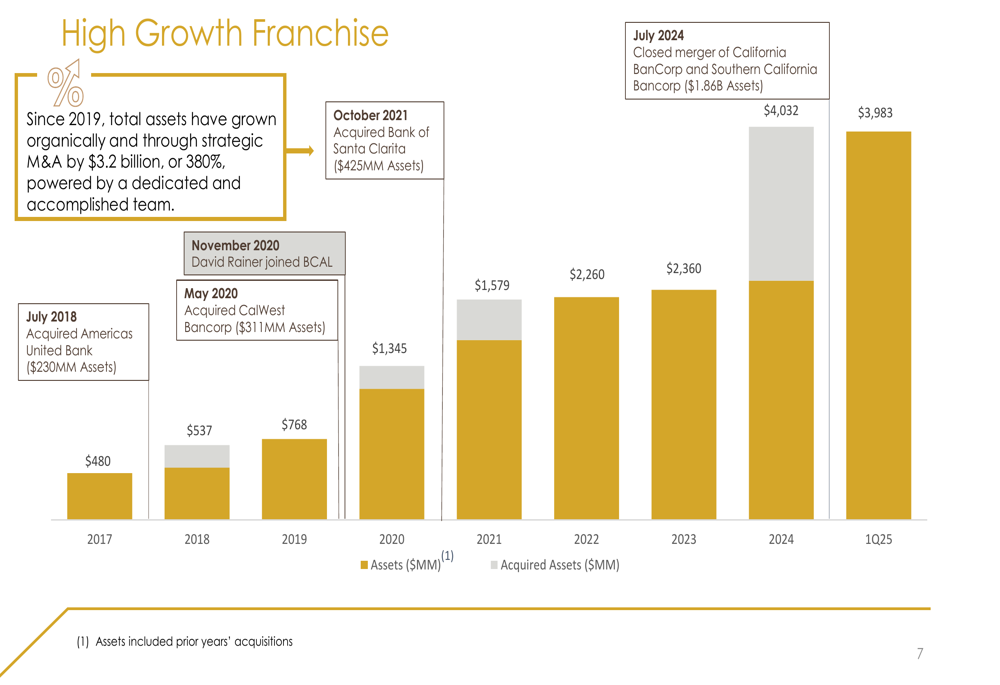

California BanCorp has demonstrated a strong growth trajectory through both organic expansion and strategic acquisitions. Since 2019, the bank’s total assets have grown by $3.2 billion, or 380%, through a combination of organic growth and four strategic acquisitions or mergers.

The bank’s growth strategy is illustrated in the following chart, showing the impact of acquisitions including Americas United Bank (2018), CalWest Bancorp (2020), Bank of Santa Clarita (2021), and the recent merger with Southern California Bancorp (2024):

The bank’s leadership team brings extensive banking experience, with CEO Steven Shelton and Executive Chairman David Rainer each having over 40 years in the industry. The management team is focused on efficient post-merger integration, managing capital, continued de-risking of the loan portfolio, and maintaining a relationship-based commercial business model.

Forward-Looking Statements

Looking ahead, California BanCorp is positioning itself to capitalize on the ongoing consolidation in the California banking market. The bank’s strategic focus includes maintaining its strong capital position, continuing to improve operational efficiency, and seeking opportunistic growth through both organic expansion and potential acquisitions.

The bank’s loan portfolio shows a diverse mix of commercial real estate, commercial and industrial, and residential loans, with a significant portion of the portfolio set to reprice within the next three years. This repricing schedule could provide opportunities for yield enhancement in different interest rate environments.

California BanCorp’s stock closed at $13.06 on April 23, 2025, with a 52-week range of $11.87 to $18.49. The stock was trading down 1.84% in premarket trading on April 24, 2025, at $12.82.

As the bank continues to integrate its recent merger and execute on its strategic initiatives, investors will be watching for continued improvements in profitability metrics, deposit growth, and asset quality in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.