Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

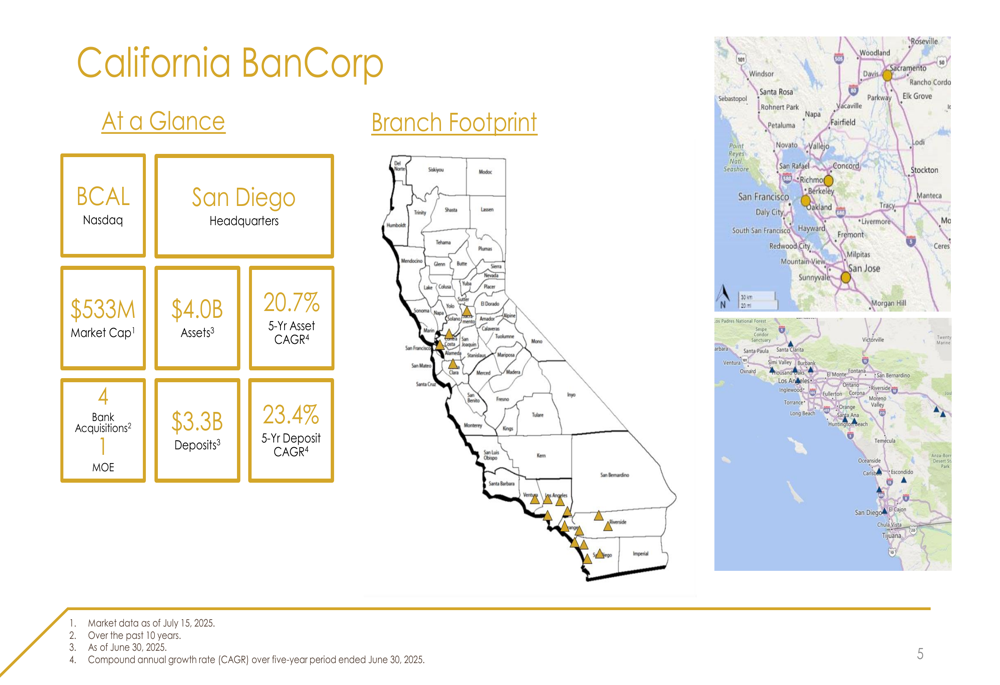

California Bancorp (NASDAQ:BCAL), operating as California Bank of Commerce, presented its Q2 2025 investor slides highlighting the bank’s strategic position in California’s robust economy while reporting mixed financial results. The bank, which completed a merger between Southern California Bancorp and California BanCorp in July 2024, continues to leverage its expanded footprint across the state’s key commercial banking markets.

As shown in the following snapshot of the bank’s market position and branch network, California Bancorp has established a significant presence in both Northern and Southern California regions:

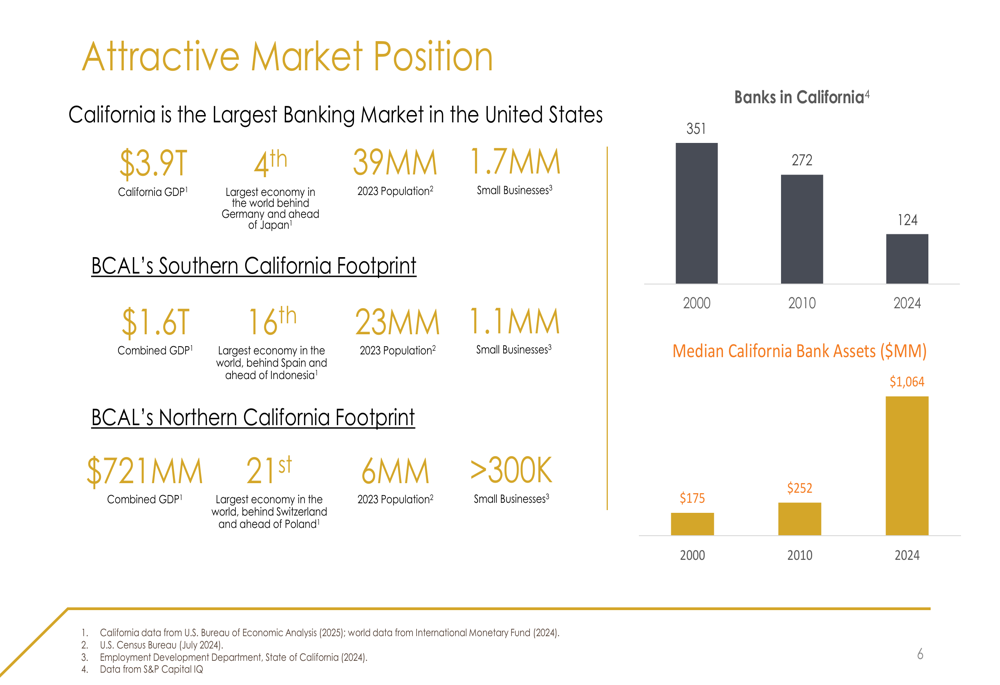

With a market capitalization of $533 million as of mid-July 2025, the bank has achieved impressive growth metrics, including a five-year asset CAGR of 20.7% and a five-year deposit CAGR of 23.4%. The bank’s strategic positioning is particularly notable given California’s economic significance as the world’s fourth-largest economy and the largest banking market in the United States.

The following chart illustrates California Bancorp’s attractive market position within California’s robust economy:

Quarterly Performance Highlights

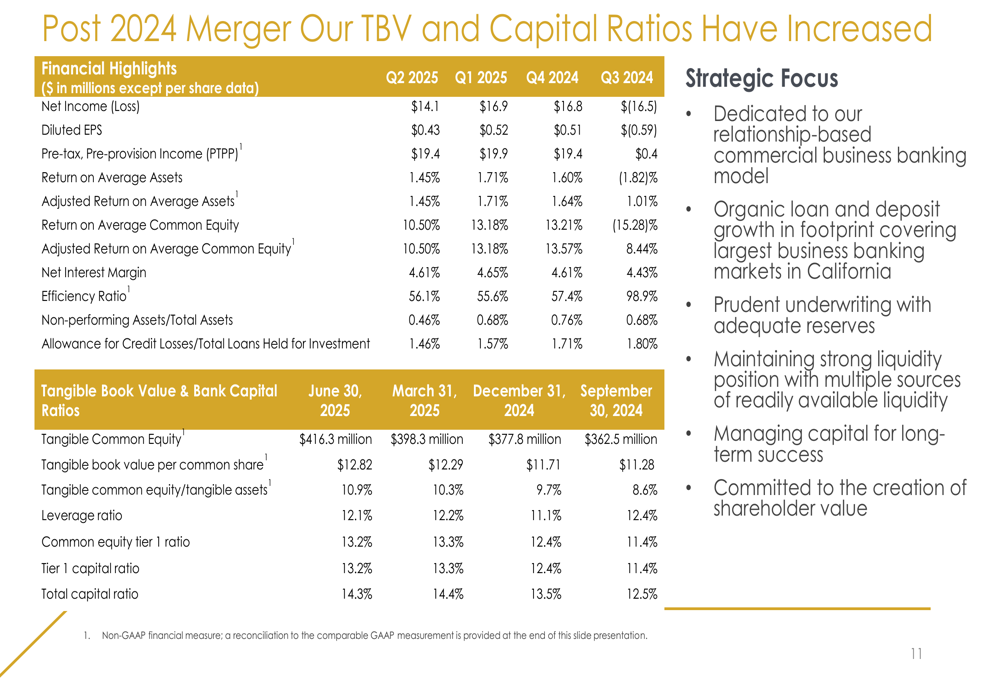

California Bancorp reported net income of $14.1 million for Q2 2025, down from $16.9 million in the previous quarter. Diluted earnings per share decreased to $0.43 from $0.52 in Q1 2025. Despite this quarterly decline, the bank’s pre-tax, pre-provision income remained relatively stable at $19.4 million compared to $19.9 million in the previous quarter.

The bank’s financial performance metrics are comprehensively detailed in the following slide:

Notably, tangible book value per common share increased to $12.82 from $12.29 in the previous quarter, representing a positive trend in shareholder value. The bank’s efficiency ratio slightly increased to 56.1% from 55.6%, indicating a minor decrease in operational efficiency.

Net interest margin, a key profitability metric for banks, slightly decreased to 4.61% from 4.65% in Q1 2025, while asset quality improved with non-performing assets to total assets decreasing to 0.46% from 0.68% in the previous quarter.

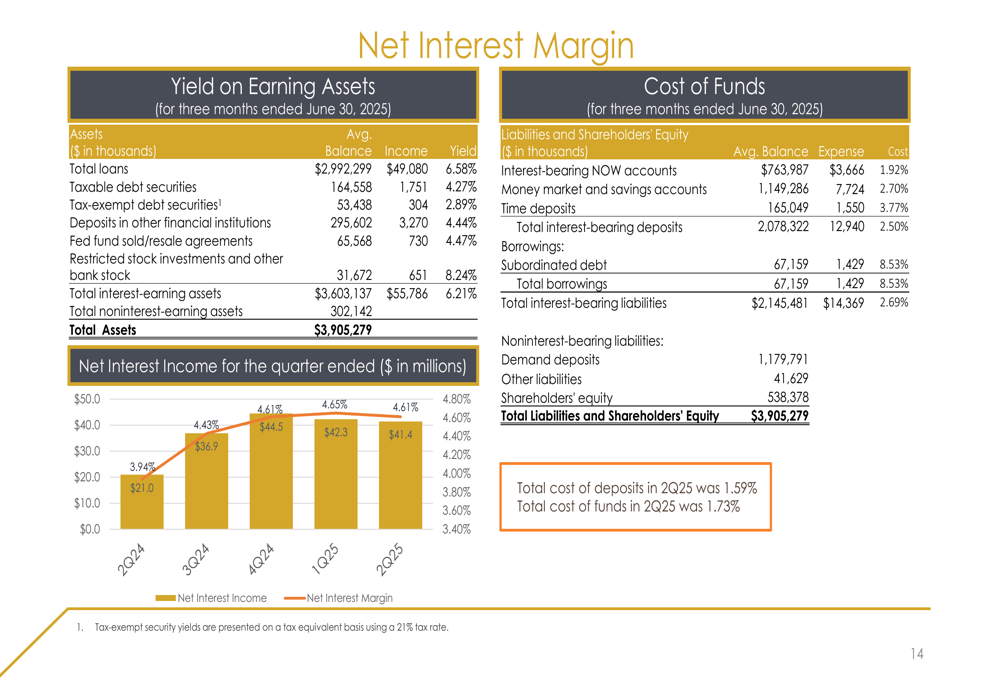

The following chart illustrates the bank’s net interest income trend over recent quarters:

Strategic Initiatives

California Bancorp continues to focus on its relationship-based commercial business banking model, emphasizing organic loan and deposit growth while maintaining prudent underwriting standards. The bank’s strategic vision centers on leveraging its experienced leadership team and established reputation to expand its commercial banking franchise.

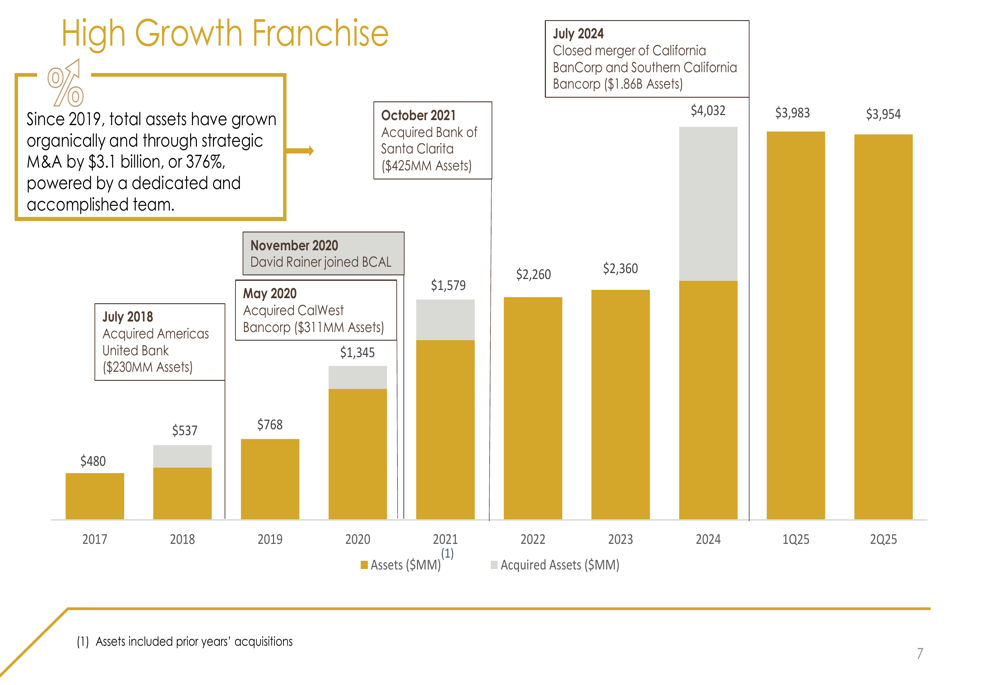

The bank’s growth strategy has been impressive, as illustrated in the following chart showing asset growth since 2017:

Since 2019, total assets have grown by $3.1 billion, representing a 376% increase through both organic growth and strategic acquisitions. The merger between California BanCorp and Southern California Bancorp in 2024 significantly expanded the bank’s asset base and market reach.

California Bancorp’s strategic focus on commercial banking is supported by its diverse loan portfolio and high-touch relationship management approach. The bank maintains commercial offices that offer a full array of banking services, with average deposits per branch of $236.6 million as of June 30, 2025.

Detailed Financial Analysis

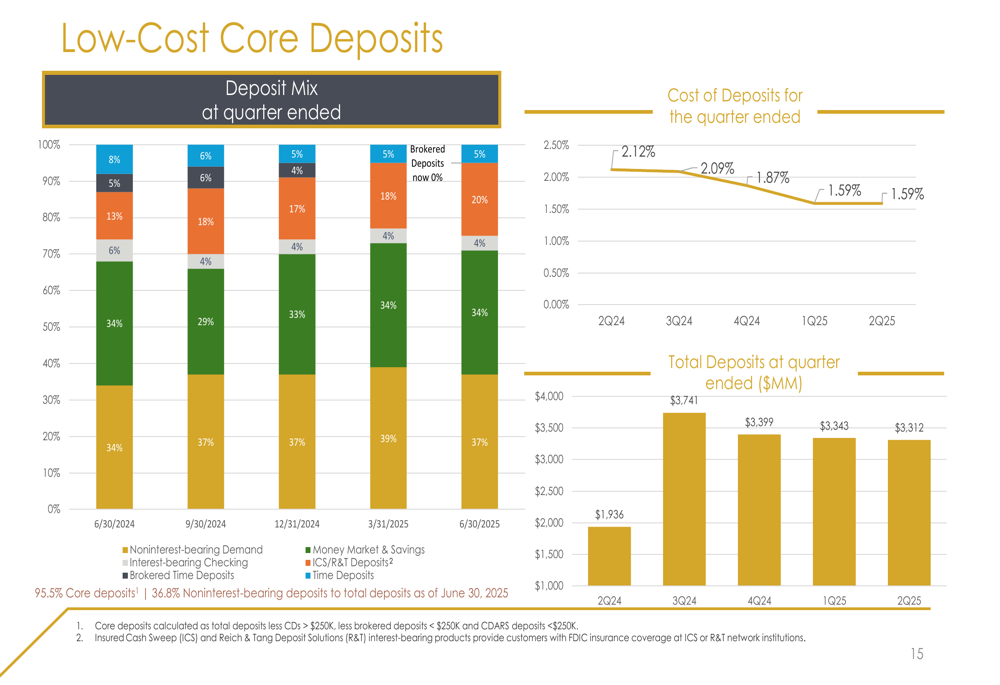

California Bancorp’s balance sheet remains strong with total assets of $3.95 billion as of June 30, 2025. The bank’s deposit base is particularly noteworthy, with noninterest-bearing deposits comprising 36.8% of total deposits, contributing to a relatively low overall cost of funds.

The following chart illustrates the bank’s deposit mix and trends:

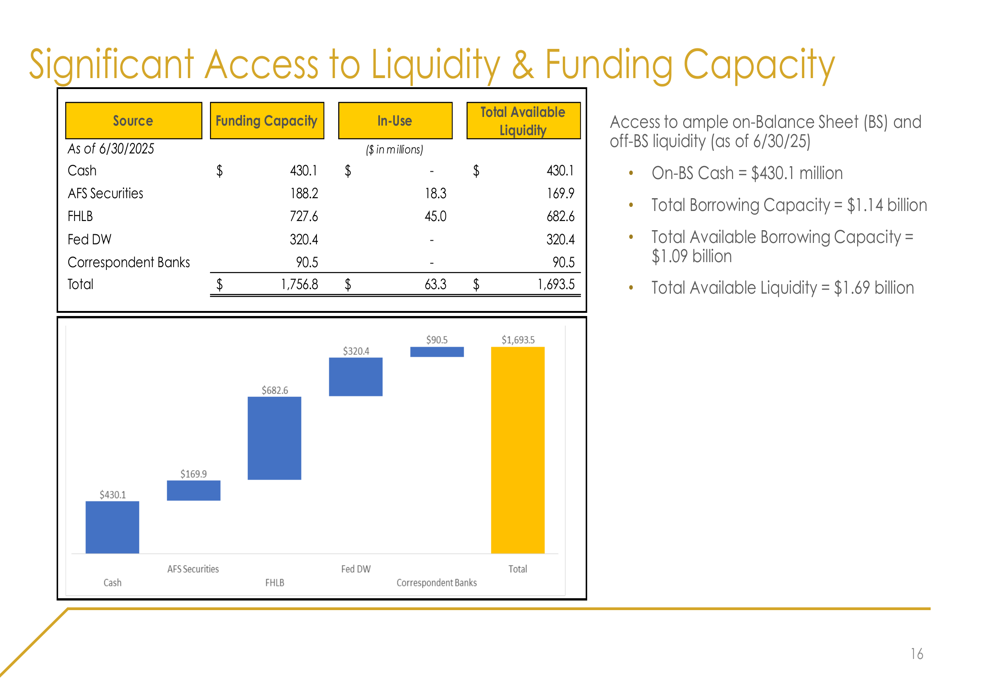

The bank maintains a strong liquidity position with $1.69 billion in total available liquidity as of June 30, 2025, providing significant flexibility to support growth and navigate market fluctuations:

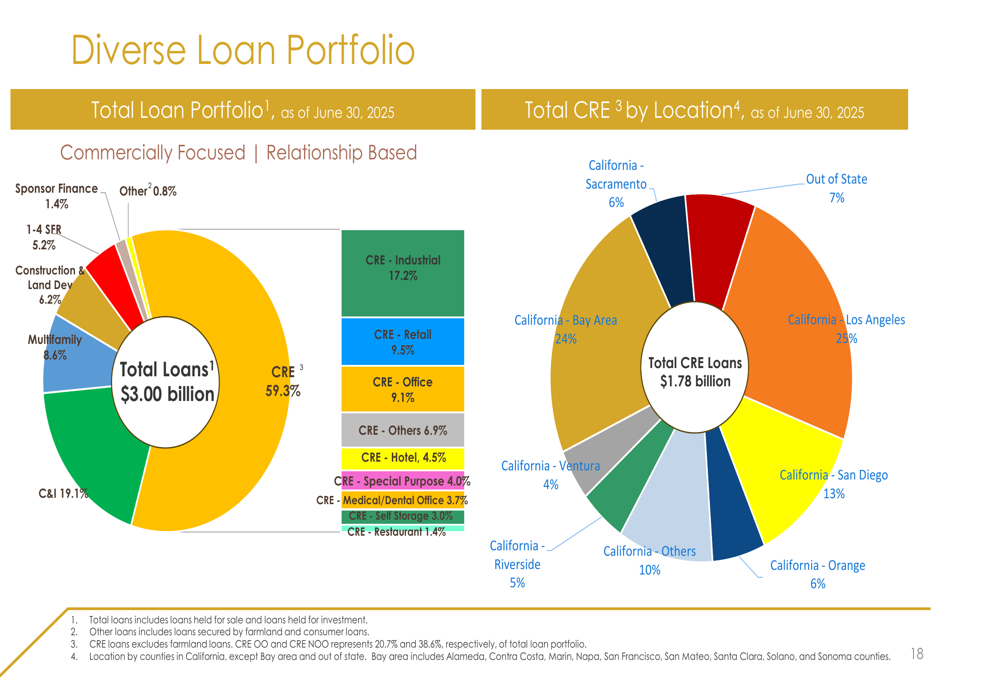

California Bancorp’s loan portfolio is well-diversified across various commercial sectors, with commercial real estate (CRE) representing 59.3% of the total loan portfolio, followed by commercial and industrial (C&I) loans at 19.1%, and multifamily loans at 8.6%:

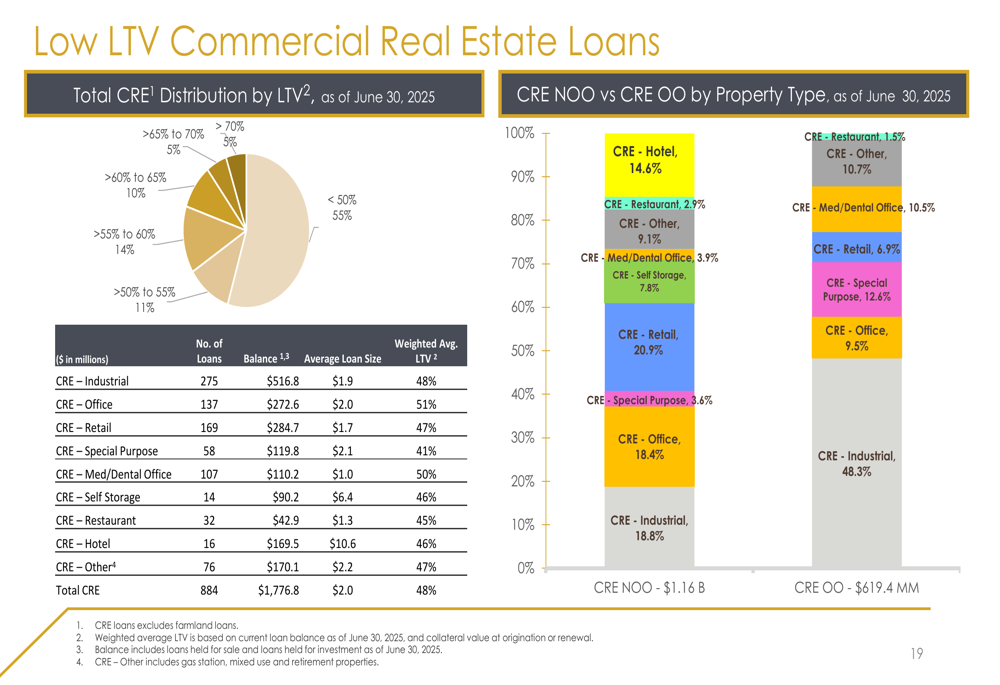

The bank’s CRE portfolio is characterized by low loan-to-value ratios, indicating conservative underwriting practices and reduced risk exposure:

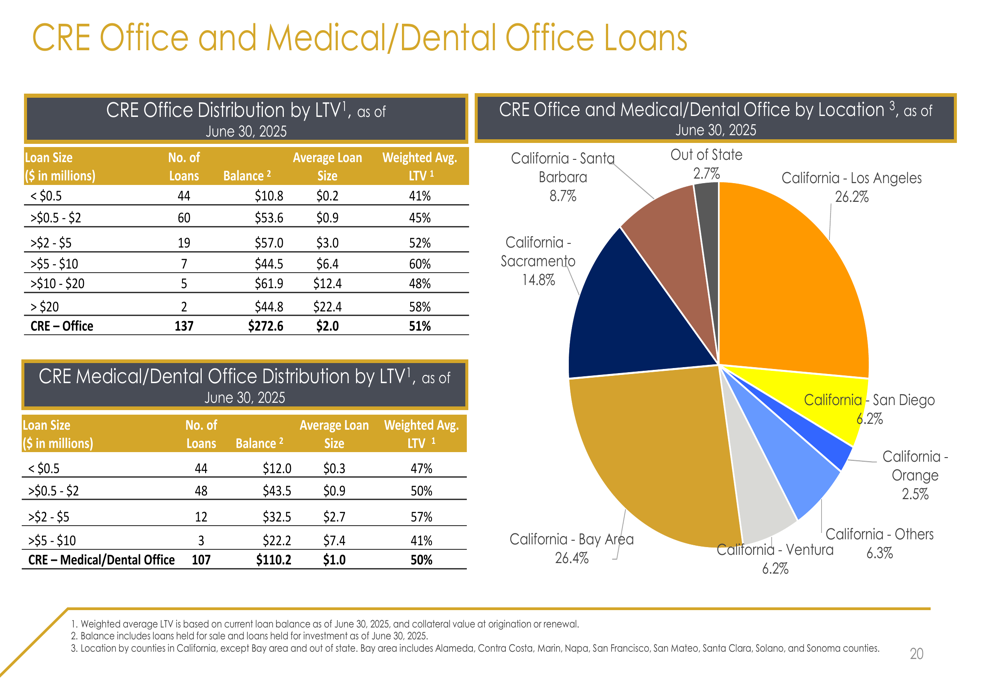

Additionally, the bank’s office loan exposure, a segment that has faced challenges in the post-pandemic environment, shows diversification by location and property type:

Forward-Looking Statements

Looking ahead, California Bancorp remains committed to maintaining a strong liquidity position, prudent underwriting standards, and effective capital management to support long-term growth and shareholder value creation. The bank’s strategic focus includes continued expansion of its commercial banking franchise across California’s key markets.

The bank’s capital position remains robust, with all regulatory capital ratios exceeding the thresholds to be considered "well-capitalized." The tangible common equity to tangible assets ratio improved to 10.9% from 10.3% in the previous quarter, reflecting the bank’s strong capital foundation.

California Bancorp’s credit quality metrics also show positive trends, with the allowance for credit losses to total loans held for investment at 1.46%, down from 1.57% in the previous quarter, reflecting the bank’s confidence in its loan portfolio quality.

As California’s banking landscape continues to consolidate, with the number of banks decreasing from 351 in 2000 to just 124 in 2024, California Bancorp is well-positioned to capitalize on market opportunities and continue its growth trajectory through both organic expansion and potential strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.