Gold prices higher, remain near record highs on rate cut bets

Carter’s Inc (NYSE:CRI) shares plummeted over 20% in after-hours trading following the release of its second quarter 2025 results on July 25, which revealed a stark contrast between modest sales growth and severely declining profitability. The children’s apparel retailer reported a 4% increase in quarterly sales but saw adjusted earnings per share collapse by 78% year-over-year.

Quarterly Performance Highlights

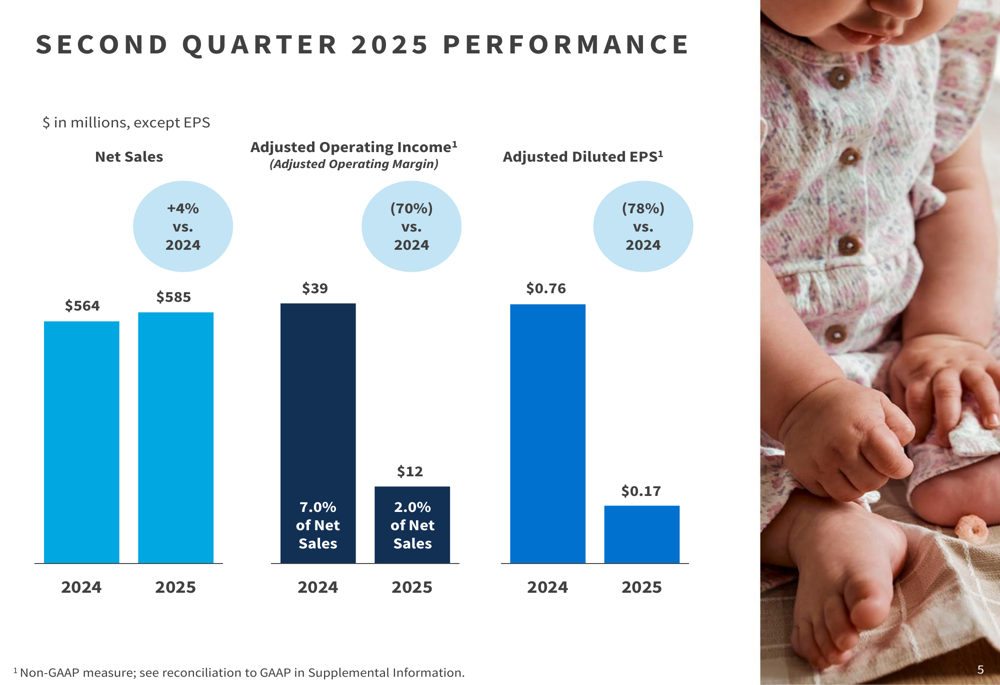

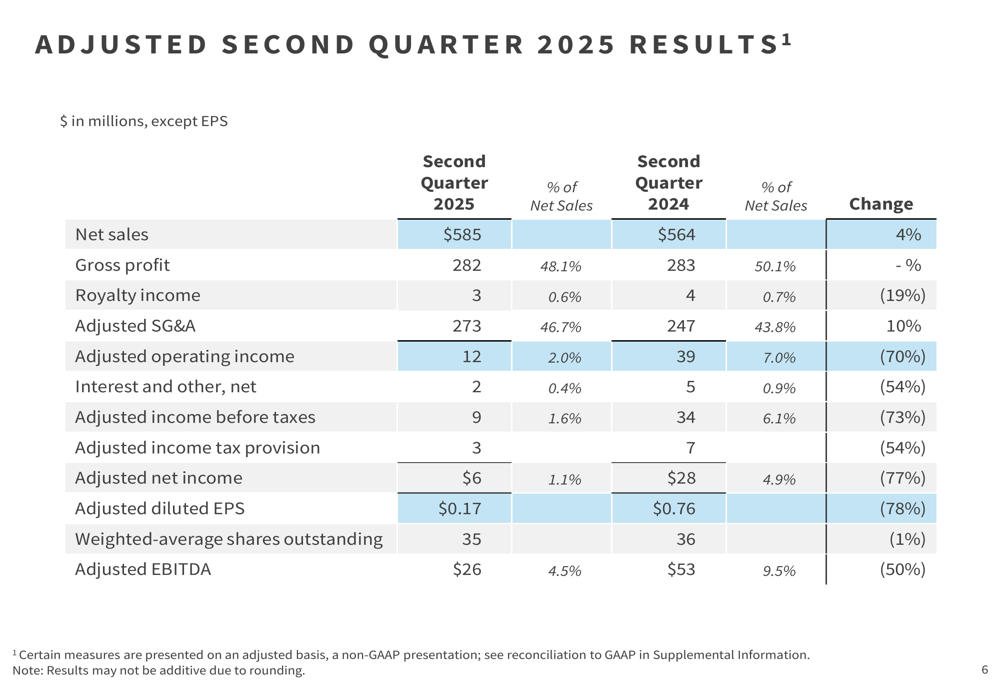

Carter’s reported second quarter net sales of $585 million, a 4% increase from $564 million in the same period last year. However, adjusted operating income plunged 70% to $12 million, representing just 2.0% of net sales compared to 7.0% in Q2 2024. Adjusted diluted earnings per share fell to $0.17, down 78% from $0.76 in the prior year period.

As shown in the following chart of quarterly performance metrics:

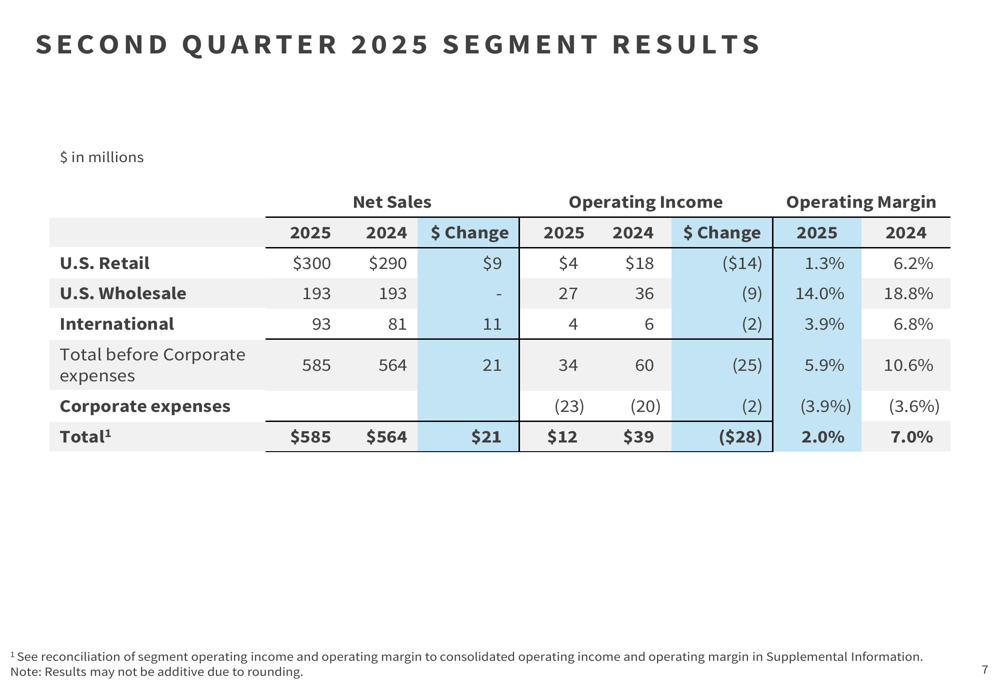

The company’s U.S. Retail segment delivered 3% net sales growth with comparable sales increasing 2%, led by strong performance in stores. The Baby category (0-24 months) was the strongest performer with 10% growth. However, operating margin in this segment declined dramatically to 1.3%, representing a 490 basis point drop from the prior year.

U.S. Wholesale segment sales remained flat year-over-year, though unit volume increased 6%. International sales showed the strongest growth at 14% (18% in constant currency), with particularly strong comparable sales in Canada (+8%) and Mexico (+19%).

The detailed segment results reveal significant margin compression across all business units:

Detailed Financial Analysis

The first half of 2025 showed even more challenging results than the quarter alone, with net sales declining 1% to $1,215 million and adjusted operating income falling 50% to $47 million. Adjusted diluted EPS for the first half decreased 54% to $0.83.

The company’s adjusted financial results for the second quarter highlight the severity of the profit decline:

Carter’s balance sheet showed $338 million in cash at quarter-end, slightly up from $317 million a year ago. However, free cash flow turned negative at -$35 million for the first half of 2025, compared to positive $67 million in the same period of 2024. The company distributed $38 million in dividends during the first half but suspended share repurchases, compared to $92 million in total capital distribution (including $34 million in share repurchases) in the first half of 2024.

Inventory levels increased 3% year-over-year to $619 million, though the company noted that unit inventory was down 1%, with the increase primarily driven by higher tariff costs.

Strategic Initiatives

Carter’s is implementing several initiatives to improve its operating model, including shortening the product development process by approximately three months, enhancing chase capabilities, leveraging AI technology, and strengthening consumer insights to improve assortment performance. The company is also conducting a comprehensive assessment of its retail store portfolio and developing a new fleet segmentation strategy.

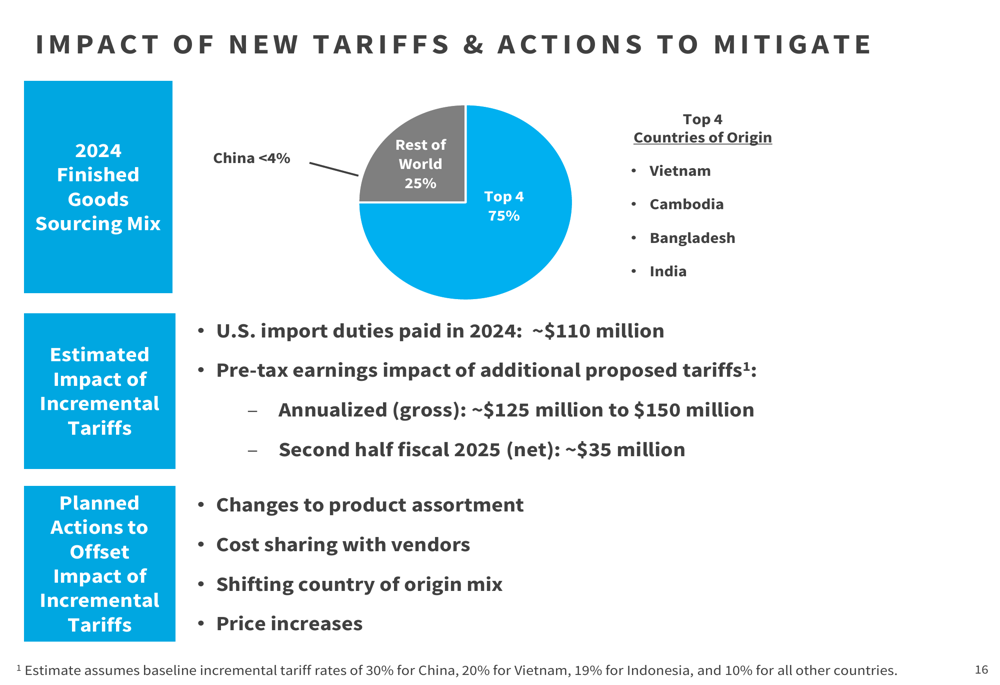

A major challenge facing the company is the impact of new tariffs. Carter’s estimates that the additional proposed tariffs could impact pre-tax earnings by approximately $125-150 million on an annualized basis, with a net impact of approximately $35 million in the second half of fiscal 2025.

The company presented its sourcing mix and tariff mitigation strategies as follows:

To offset the tariff impact, Carter’s plans to implement changes to its product assortment, share costs with vendors, shift its country of origin mix, and implement price increases. The company currently sources less than 4% of its finished goods from China, with Vietnam, Cambodia, Bangladesh, and India representing its top four sourcing countries.

Forward-Looking Statements

The significant stock decline following the earnings release reflects investor concerns about the company’s profitability trajectory and ability to mitigate tariff impacts. According to the fundamentals data, Carter’s stock fell 19.69% on the day of the announcement, with after-market trading showing a further decline to $26.15, representing a 20.15% drop from the previous close.

This reaction comes after Carter’s had already suspended its forward guidance during the Q1 2025 earnings call due to leadership transition and tariff uncertainties. The new CEO, Douglas C. Palladini, is leading the company through these challenges while implementing operational improvements.

The company’s focus on its core brands (Carter’s and OshKosh B’gosh) and emerging brands (little planet, Otter Avenue, and Skip Hop) remains central to its strategy, along with its exclusive brand partnerships with major retailers. However, the severe margin compression and profit decline suggest significant headwinds that will require substantial operational improvements and successful tariff mitigation strategies to overcome in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.