Eos Energy stock falls after Fuzzy Panda issues short report

Carter’s Inc (NYSE:CRI) revealed a significant restructuring plan in its third-quarter 2025 presentation on October 27, as the children’s apparel retailer grapples with flat sales and declining profits. The company plans to close 150 low-margin stores and reduce office-based roles by 15% amid ongoing margin pressures.

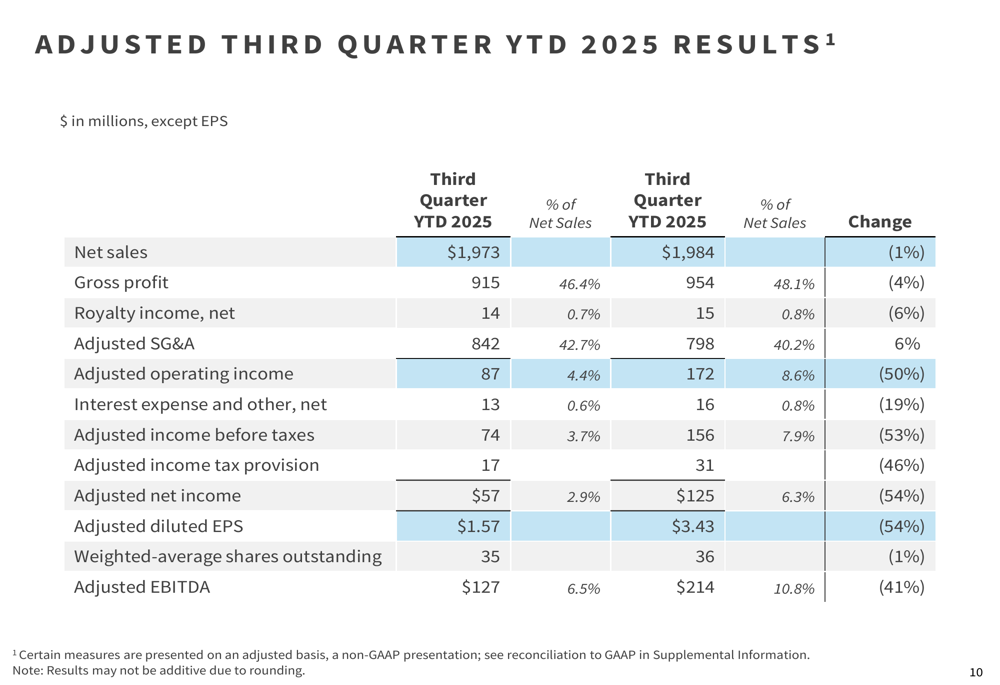

Quarterly Performance Highlights

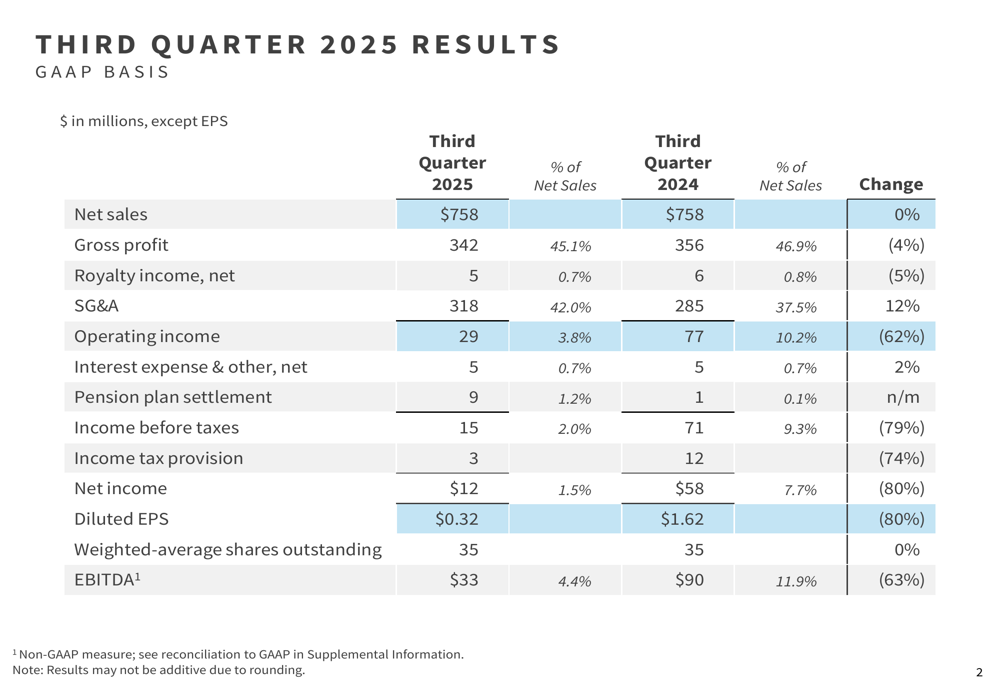

Carter’s reported third-quarter net sales of $758 million, unchanged from the same period in 2024, falling short of analyst expectations of $771.17 million. Despite the revenue miss, adjusted earnings per share of $0.74 exceeded forecasts of $0.72, though this represents a 55% decline from $1.64 in the third quarter of 2024.

The company’s profitability metrics showed significant pressure across the board, with adjusted operating income falling 49% to $39 million and adjusted net income dropping 55% to $27 million compared to the prior year.

As shown in the following financial overview from the presentation:

On a GAAP basis, the results were even more challenging, with operating income declining 62% to $29 million and net income falling 80% to $12 million. The company’s EBITDA also decreased substantially, down 63% to $33 million compared to the same quarter last year.

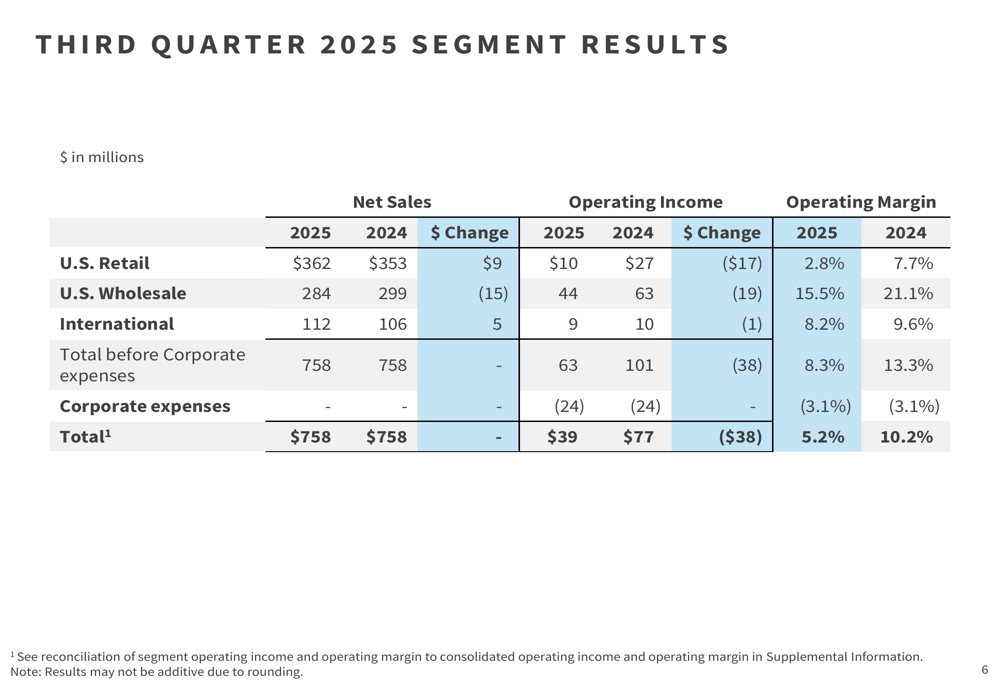

Segment performance revealed mixed results across the business. The U.S. Retail segment posted a 3% increase in net sales, with comparable sales growing 2% for the second consecutive quarter. However, operating margin compressed significantly to 2.8%, down 490 basis points from the prior year. The U.S. Wholesale segment experienced a 5% decline in sales, while International operations showed strength with 5% sales growth.

The detailed segment breakdown illustrates these trends:

Carter’s CEO highlighted positive momentum in key categories, noting: "We are seeing growth in our better and best categories of business." The baby category showed particular strength with high single-digit growth in Q3, marking the fifth consecutive quarter of growth in this segment. The company also reported success in attracting Gen Z consumers, with a 17% increase over the last twelve months.

Strategic Restructuring Initiatives

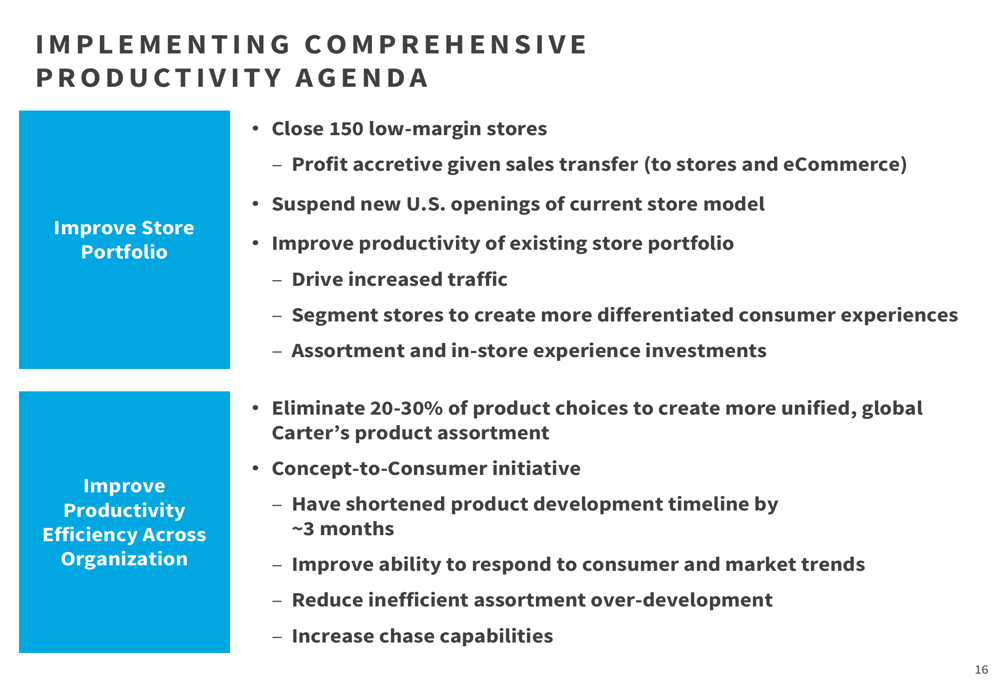

In response to the profit challenges, Carter’s announced a comprehensive productivity agenda focused on cost reduction and operational efficiency. The plan includes closing 150 low-margin stores, suspending new U.S. store openings of the current model, and reducing office-based roles by approximately 15%.

The company’s restructuring strategy aims to address margin pressures while maintaining focus on core strengths:

Additionally, Carter’s plans to streamline its product assortment by eliminating 20-30% of product choices to create a more unified global product line. Management indicated this would help improve inventory management and supply chain efficiency.

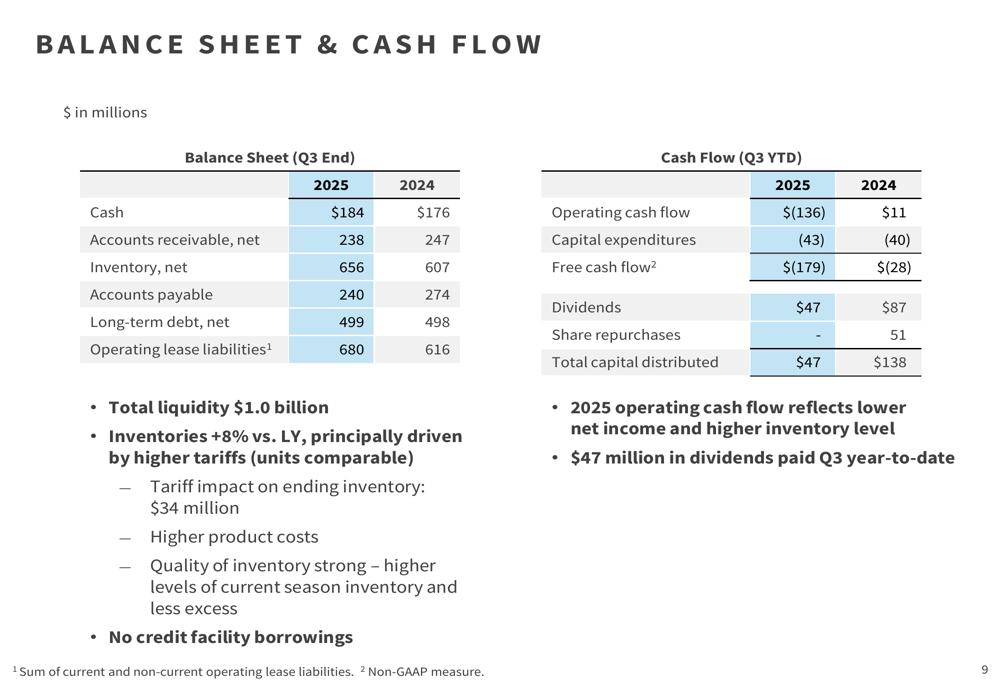

The company’s balance sheet remains relatively strong despite operational challenges, with $184 million in cash and total liquidity of $1.0 billion. However, inventories increased 8% compared to last year, primarily driven by higher tariff costs.

Tariff Impact and Mitigation Strategies

A significant factor affecting Carter’s performance is the impact of higher tariffs. The company paid approximately $110 million in U.S. import duties in 2024, representing about a 13% effective duty rate. Management addressed the tariff challenges during the earnings call, with CFO Richard Westenberger stating: "It is our intent to cover the vast majority of this incremental tariff impact."

Mitigation strategies include cost-sharing with vendors, selective price increases, and operational efficiencies. The company’s presentation indicated these efforts would be crucial to maintaining competitiveness in the challenging retail environment.

Forward-Looking Statements

Despite current challenges, Carter’s provided a cautiously optimistic outlook for the future. For Q4 2025, the company expects a gross margin rate of approximately 43%. Looking further ahead to fiscal year 2026, management anticipates growth in both net sales and earnings, supported by pricing strategies and an expected low single-digit retail comp in Q4.

The company also plans to increase marketing spend by approximately $16 million to drive consumer engagement and support its strategic initiatives. Testing of new store concepts is planned to help revitalize the retail channel performance.

Market Reaction

Following the earnings release and presentation, Carter’s stock experienced a significant decline in pre-market trading, dropping 8.78% to $29.51. This reaction reflects investor concerns about the revenue miss and the extensive restructuring needed to address profitability challenges.

The stock is now trading closer to its 52-week low of $23.38 than its high of $58.13, highlighting the market’s cautious stance on the company’s turnaround prospects. According to the earnings article, Carter’s maintains strong fundamentals with a current ratio of 2.2, indicating robust liquidity with assets well exceeding short-term obligations.

Carter’s comprehensive restructuring plan represents a significant strategic shift as the company works to stabilize performance and position itself for future growth amid challenging market conditions. The effectiveness of these initiatives will be closely watched by investors in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.