September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Caterpillar Inc (NYSE:CAT) released its second quarter 2025 financial results on August 5, showing improved performance compared to both the previous quarter and year-over-year metrics. The heavy equipment manufacturer posted an 18% increase in operating profit despite facing significant tariff pressures that are expected to impact full-year results.

The company’s shares were trading down 3.4% in premarket activity at $418.97, suggesting investors may have concerns about the impact of tariffs on future profitability despite the positive quarterly results.

Quarterly Performance Highlights

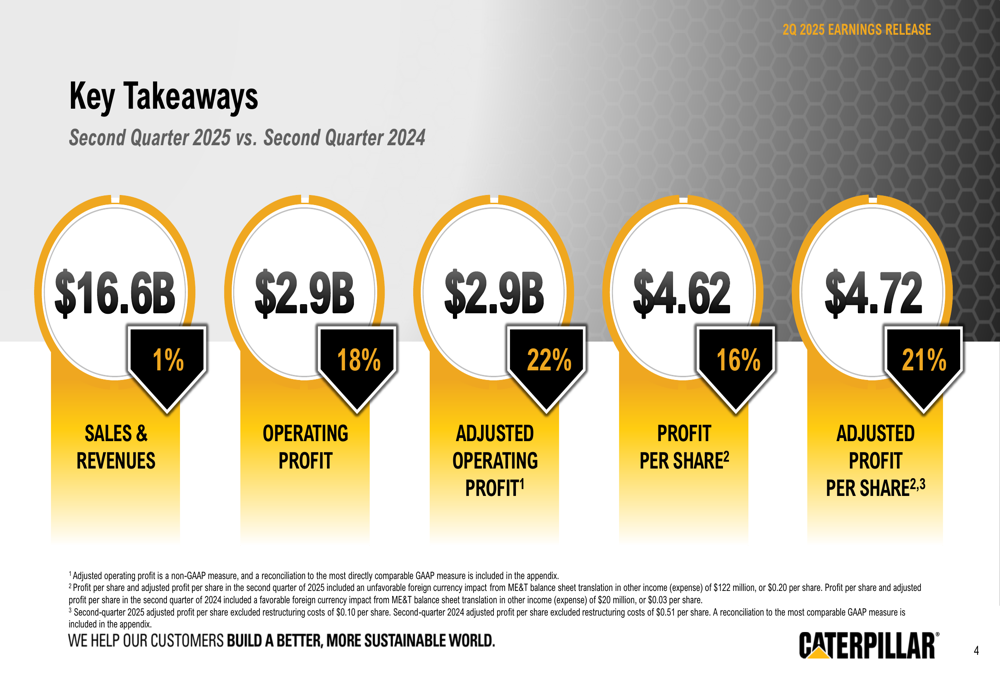

Caterpillar reported second quarter sales and revenues of $16.6 billion, representing a modest 1% increase compared to the second quarter of 2024. More impressively, operating profit rose to $2.9 billion, an 18% increase year-over-year, while adjusted operating profit climbed 22%.

As shown in the following key financial comparison:

The company’s profit per share reached $4.62, up 16% from the same period last year, while adjusted profit per share grew 21% to $4.72. This marks a significant improvement from the first quarter of 2025, when Caterpillar missed analyst expectations with an EPS of $4.25.

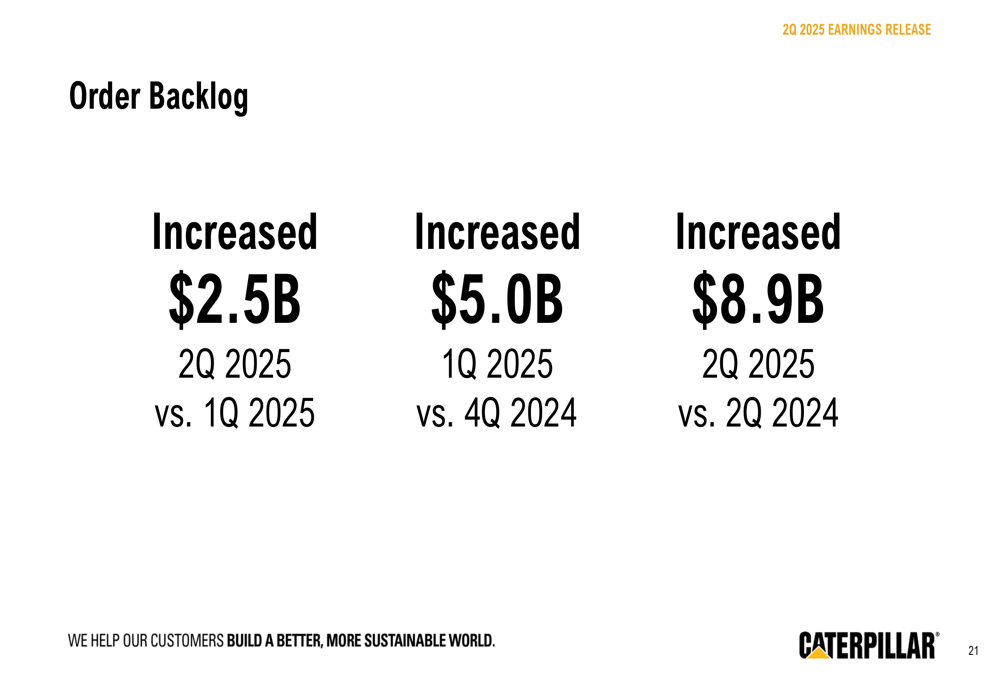

Caterpillar’s backlog grew by $2.5 billion compared to the first quarter of 2025 and increased by $8.9 billion year-over-year, indicating strong future demand despite current challenges.

Segment Analysis

Performance varied significantly across Caterpillar’s business segments, with Energy & Transportation emerging as the clear standout:

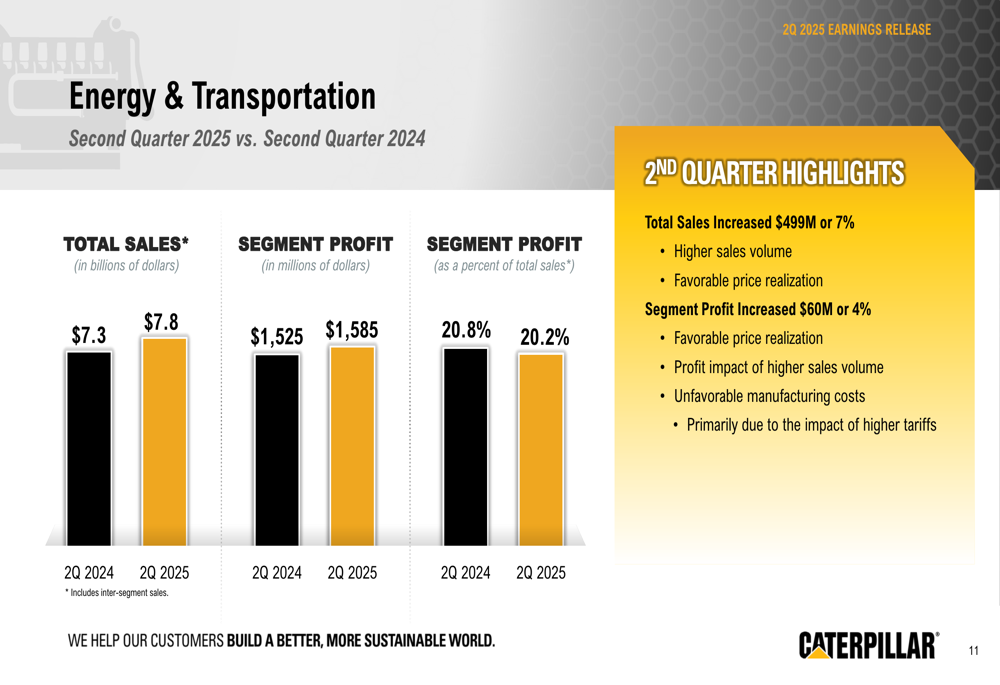

Energy & Transportation posted a 7% increase in sales to $7.8 billion and a 4% rise in segment profit to $1.6 billion. This positive performance was driven by higher sales volume and favorable price realization, though partially offset by unfavorable manufacturing costs primarily related to tariffs.

As illustrated in the segment breakdown:

In contrast, Construction Industries experienced a 7% decline in sales to $6.2 billion, with segment profit dropping 29% to $1.2 billion. The decline was attributed to unfavorable price realization, lower sales volume, and the impact of higher tariffs.

Resource Industries also faced challenges with a 4% sales decrease to $3.1 billion and a 25% profit decline to $537 million, similarly affected by unfavorable price realization and tariff impacts.

The Financial Products segment was a bright spot alongside Energy & Transportation, with revenues increasing 4% to $1.0 billion and segment profit rising 9% to $248 million.

Tariff Impact and Mitigation Strategies

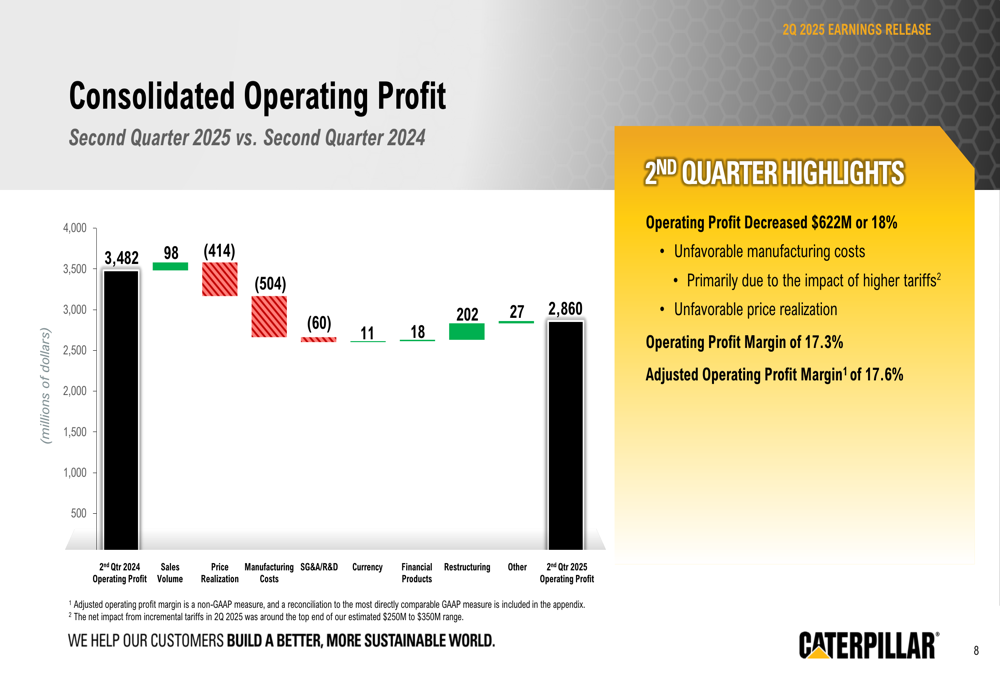

A significant theme throughout the presentation was the impact of tariffs on Caterpillar’s operations. The company expects net incremental tariffs of approximately $1.3 billion to $1.5 billion for the full year 2025, with $400 million to $500 million anticipated in the third quarter alone.

The waterfall chart below illustrates how various factors affected operating profit, with manufacturing costs (including tariffs) creating a $504 million headwind:

Despite these challenges, Caterpillar maintained strong cash flow, generating $2.4 billion in Machinery, Energy & Transportation (ME&T) free cash flow during the quarter, only slightly below the $2.5 billion generated in Q2 2024.

The company returned approximately $1.5 billion to shareholders through $800 million in share repurchases and dividends, including a 7% increase in the quarterly dividend—marking the fifth consecutive year with a high single-digit quarterly increase.

Forward Guidance and Outlook

Looking ahead, Caterpillar provided a cautiously optimistic outlook for the remainder of 2025:

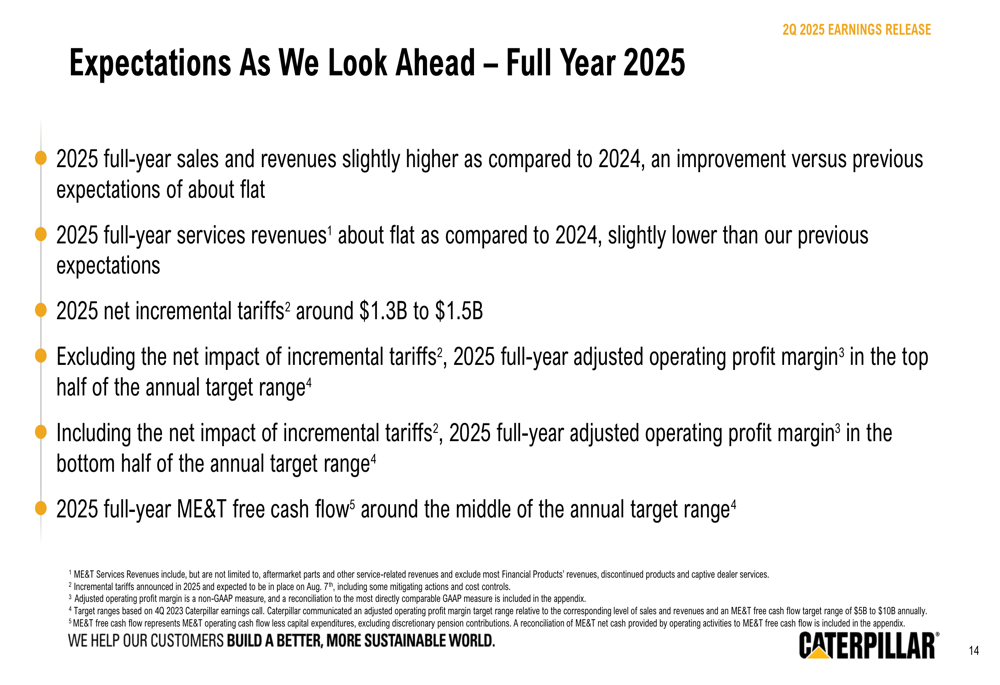

The company expects full-year 2025 sales and revenues to be slightly higher compared to 2024, an improvement from the previous quarter’s guidance of "flat to slightly down." However, due to the significant tariff impact, Caterpillar anticipates its full-year adjusted operating profit margin will fall in the bottom half of its annual target range.

For the third quarter specifically, Caterpillar projects moderate sales growth compared to Q3 2024, though adjusted operating profit margin is expected to be lower year-over-year due to tariff impacts.

The company’s backlog growth provides some confidence in future demand, as illustrated in this chart:

Market Reaction and Analyst Perspectives

Despite the positive year-over-year performance, Caterpillar’s stock was trading down 3.4% in premarket activity, suggesting investors may be focusing on the tariff headwinds and margin pressure rather than the revenue and profit growth.

The reaction follows a challenging first quarter when Caterpillar missed analyst expectations, posting an EPS of $4.25 against forecasts of $4.35 and revenues of $14.25 billion versus expectations of $14.58 billion.

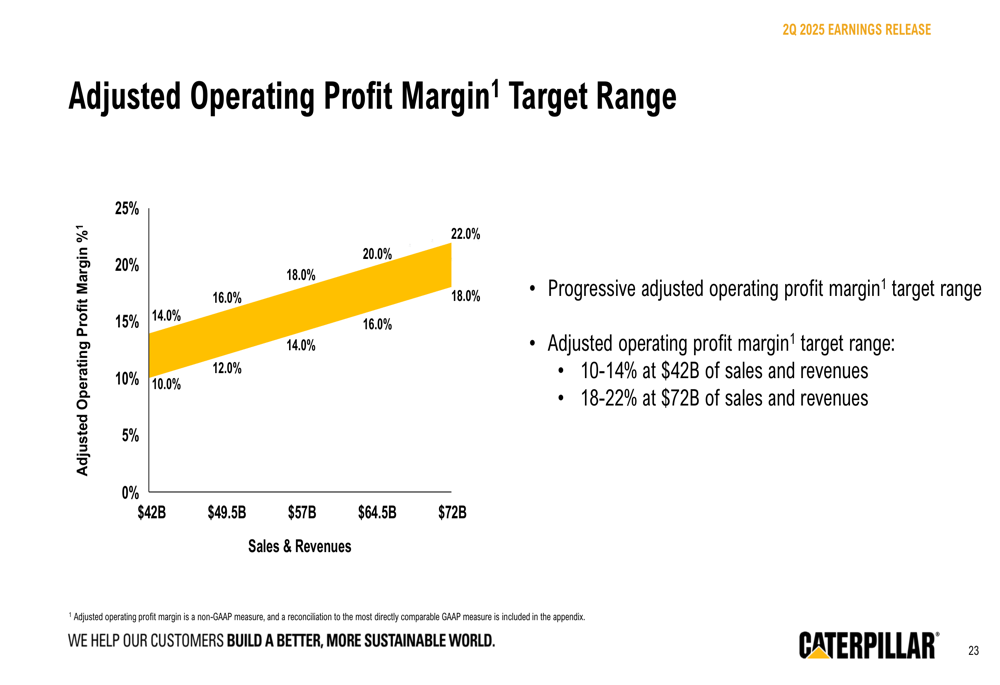

The company’s progressive adjusted operating profit margin target range provides context for evaluating performance against long-term goals:

While Caterpillar demonstrated resilience in Q2 2025 with improved metrics across most categories, the ongoing tariff situation remains a significant concern for both the company and investors as they look toward the second half of the year. The strong backlog growth, however, suggests potential for continued revenue momentum if the company can effectively manage the tariff-related cost pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.