First Brands Group debt targeted by Apollo Global Management - report

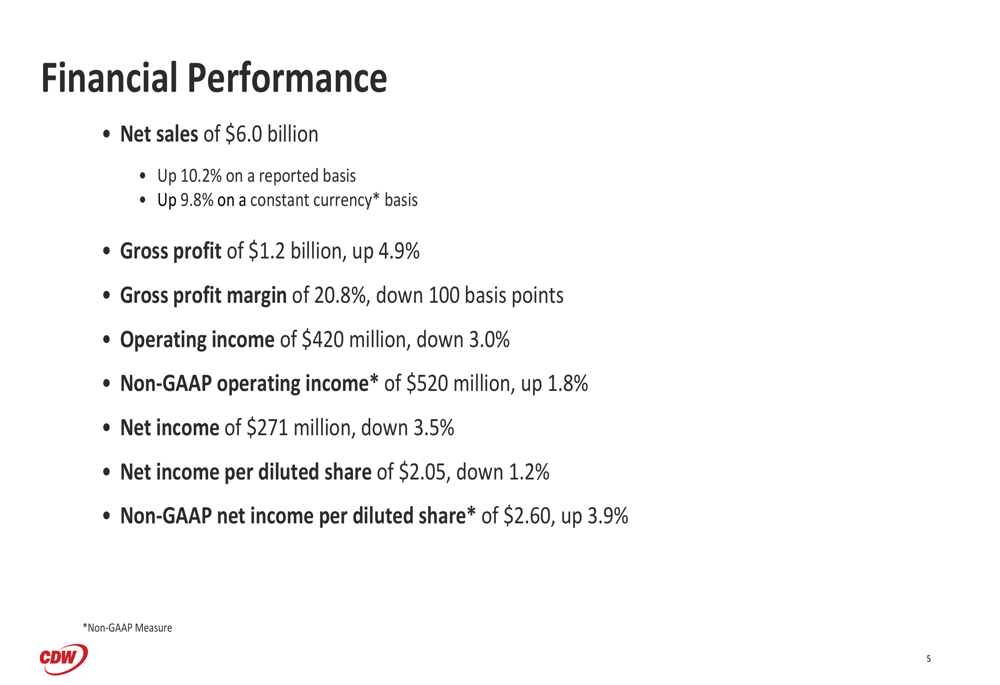

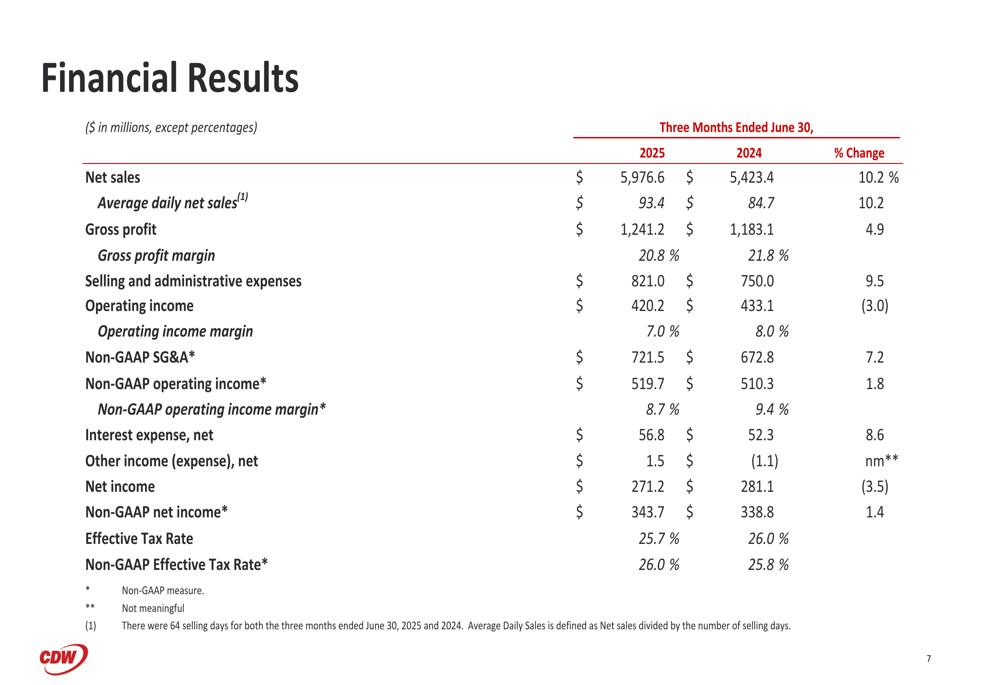

CDW Corporation (NASDAQ:CDW) reported second-quarter 2025 revenue growth of 10.2%, reaching $6.0 billion, according to its August 6 investor presentation. Despite the strong top-line performance, the company faced margin pressure with operating income declining 3.0% year-over-year to $420 million.

The stock closed at $165.24 on August 5, down 4.01% ahead of the earnings release, with minimal activity in pre-market trading.

Quarterly Performance Highlights

CDW’s second quarter showed robust revenue growth across most business segments, though profitability metrics revealed some challenges. Net sales increased 10.2% on a reported basis and 9.8% on a constant currency basis compared to Q2 2024.

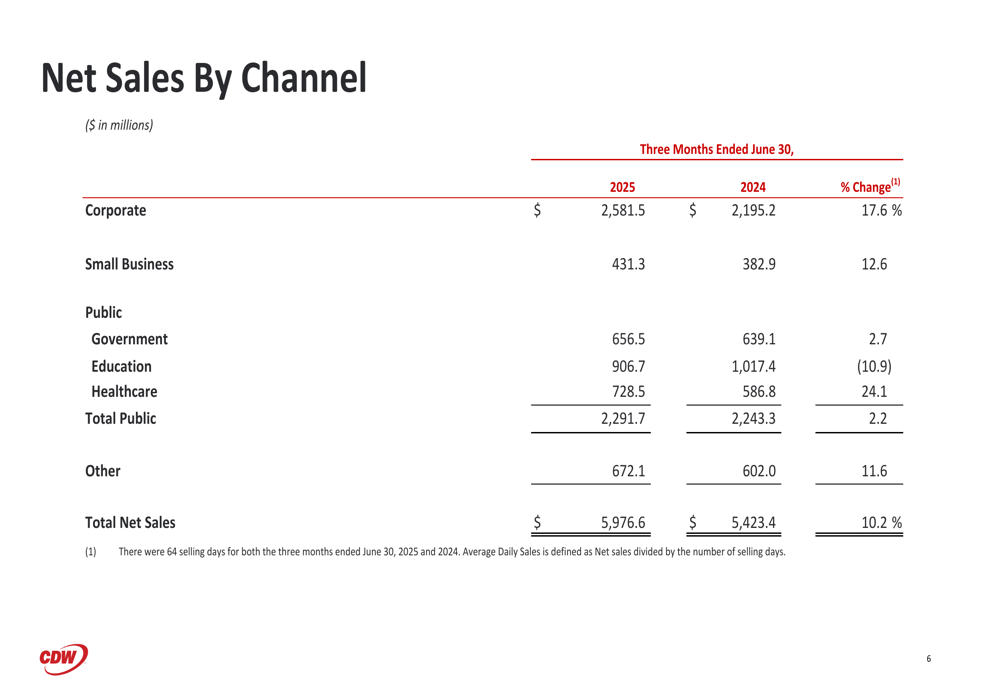

The company’s growth was primarily driven by strong performance in the corporate and healthcare segments. Corporate sales surged 17.6% to $2.58 billion, while the healthcare segment grew 24.1% to $728.5 million. However, the education segment declined 10.9% to $906.7 million, partially offsetting these gains.

"Our second quarter results demonstrate our ability to navigate a complex market environment while delivering solid top-line growth," said the company in its presentation. The results show CDW continuing to outpace the broader IT market, consistent with its stated goal of exceeding U.S. IT growth by 200-300 basis points.

Detailed Financial Analysis

While revenue growth was strong, CDW’s profitability metrics showed some pressure. Gross profit increased 4.9% to $1.24 billion, but gross profit margin contracted 100 basis points to 20.8% compared to 21.8% in the prior year period. Operating income decreased 3.0% to $420.2 million, with operating income margin declining to 7.0% from 8.0% a year earlier.

The company’s non-GAAP metrics painted a somewhat better picture, with non-GAAP operating income increasing 1.8% to $519.7 million, though non-GAAP operating margin still contracted to 8.7% from 9.4%.

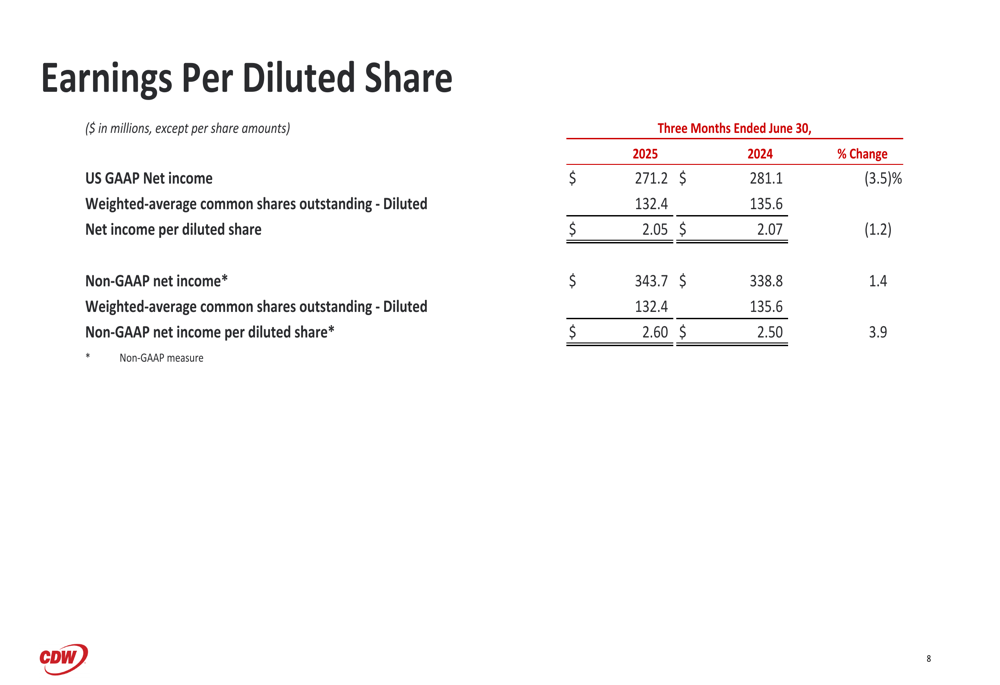

Earnings per diluted share declined 1.2% to $2.05, while non-GAAP earnings per diluted share increased 3.9% to $2.60. This represents a sequential decline from Q1 2025, when the company reported earnings per share of $2.15.

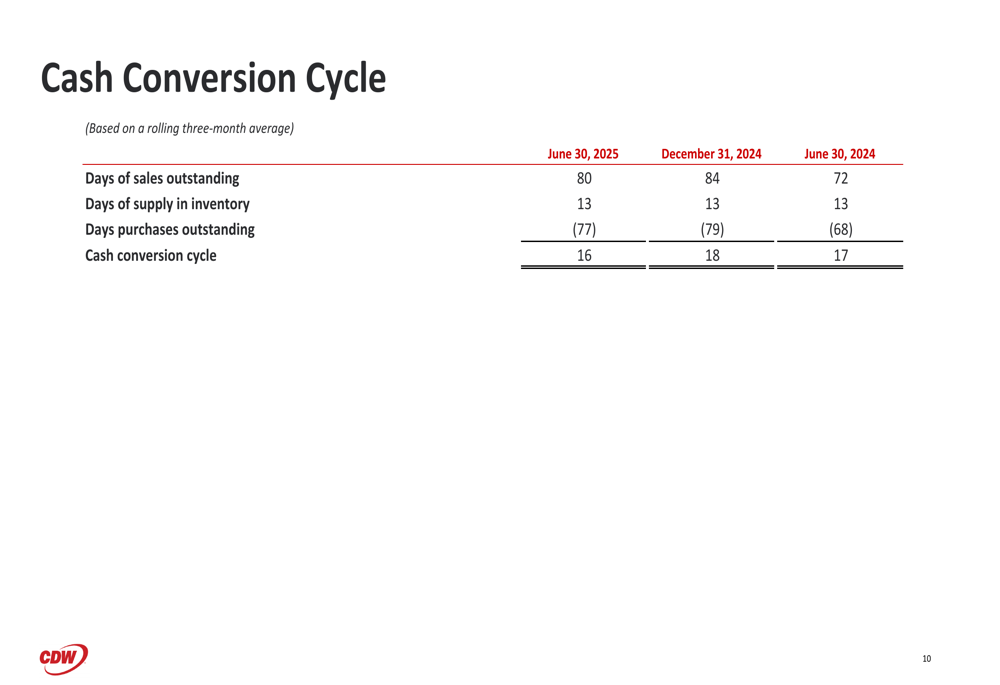

The company’s cash conversion cycle stood at 16 days as of June 30, 2025, an improvement from 18 days at the end of 2024 and slightly better than the 17 days reported a year earlier. This indicates efficient working capital management despite the challenging environment.

Strategic Initiatives

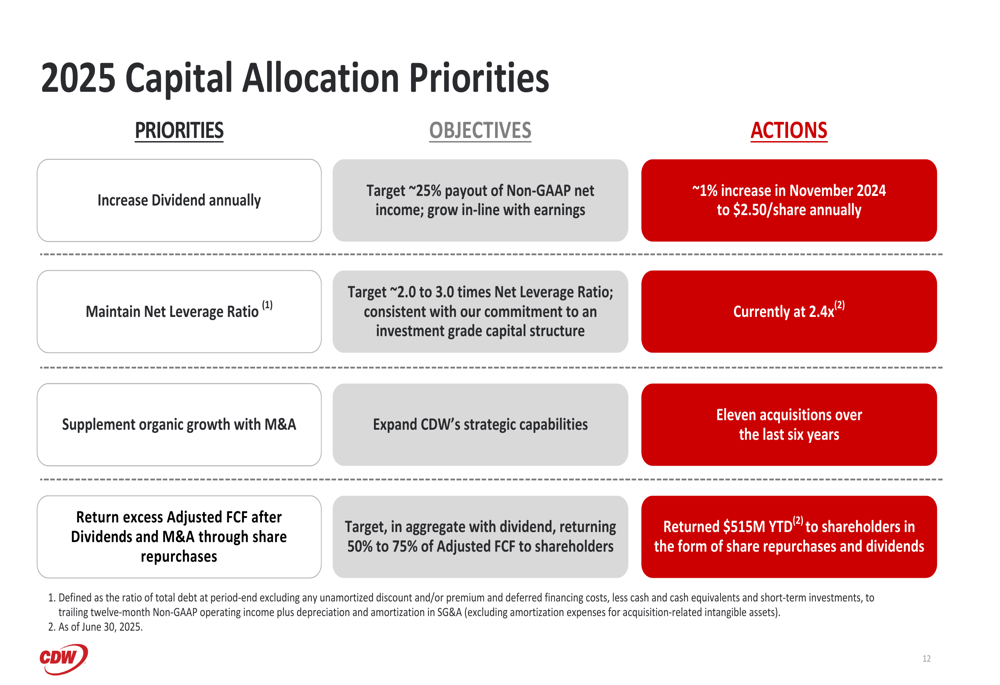

CDW outlined its capital allocation priorities for 2025, maintaining a balanced approach to shareholder returns and strategic investments. The company increased its dividend by approximately 1% in November 2024 to $2.50 per share annually, targeting a payout of about 25% of non-GAAP net income.

The company is maintaining a net leverage ratio of 2.4x, within its target range of 2.0-3.0x, consistent with its commitment to an investment-grade capital structure. CDW also highlighted its continued focus on M&A, noting eleven acquisitions over the past six years to expand its strategic capabilities.

"We returned $515 million year-to-date to shareholders in the form of share repurchases and dividends," the company stated in its presentation, demonstrating its commitment to returning 50-75% of adjusted free cash flow to shareholders.

Forward-Looking Statements

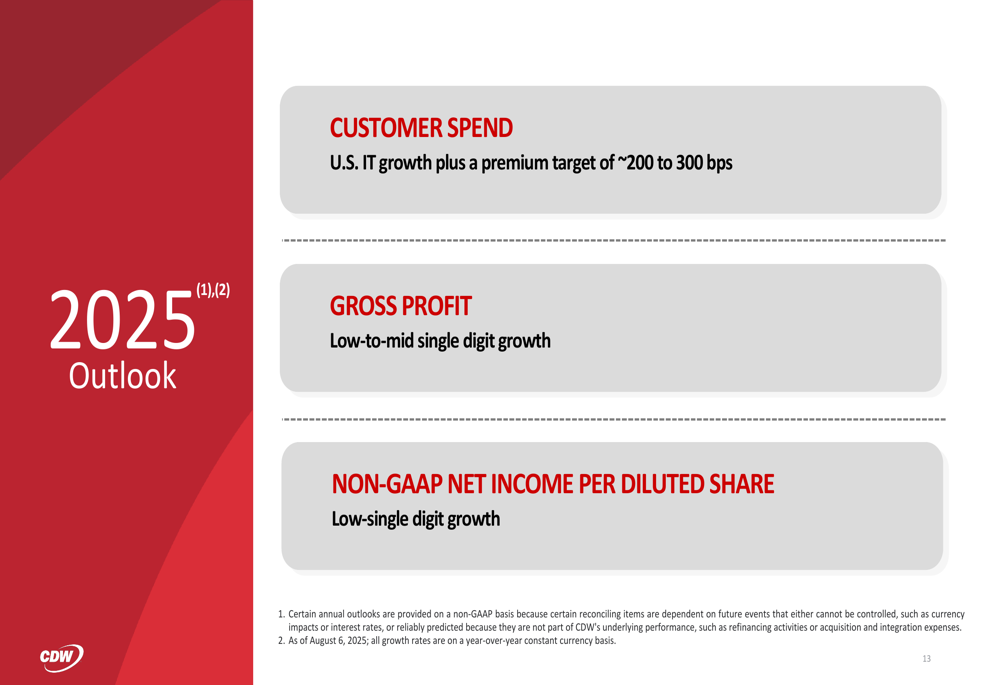

CDW maintained its full-year 2025 outlook despite the mixed second-quarter results. The company continues to expect customer spend to exceed U.S. IT growth by approximately 200-300 basis points, with low-to-mid single-digit growth in gross profit and low-single-digit growth in non-GAAP net income per diluted share.

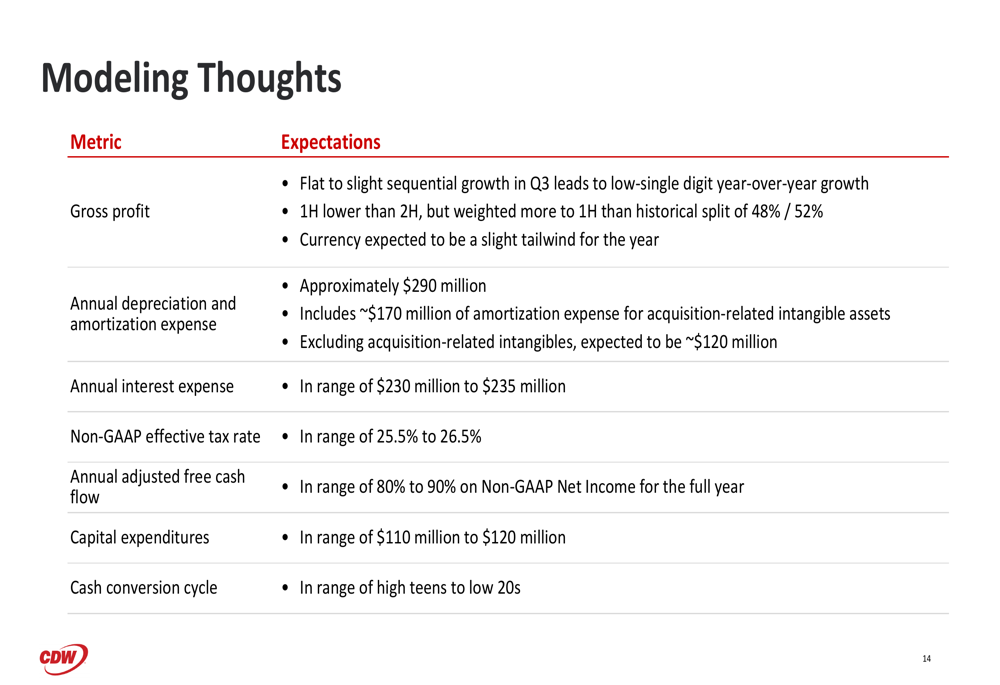

For modeling purposes, CDW provided additional guidance, expecting flat to slight sequential growth in gross profit for Q3 2025, leading to low-single-digit year-over-year growth. The company anticipates annual interest expense in the range of $230-235 million and a non-GAAP effective tax rate between 25.5% and 26.5%.

The maintained outlook suggests management confidence in second-half performance despite the margin pressure experienced in Q2. This aligns with comments from the Q1 earnings call, where CEO Chris Leahy emphasized the company’s resilience in uncertain times.

CDW’s ability to deliver on its full-year targets will likely depend on improvements in the education segment and maintaining the strong momentum seen in corporate and healthcare markets, while addressing the margin pressures that impacted Q2 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.