TSX futures inch lower after index closes at new all-time high

Introduction & Market Context

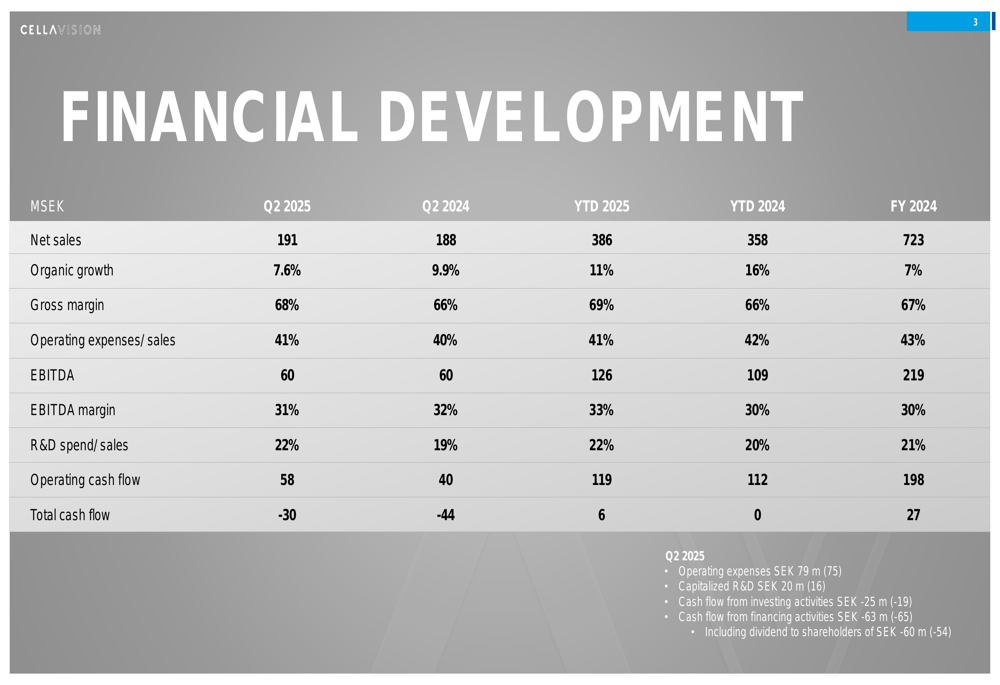

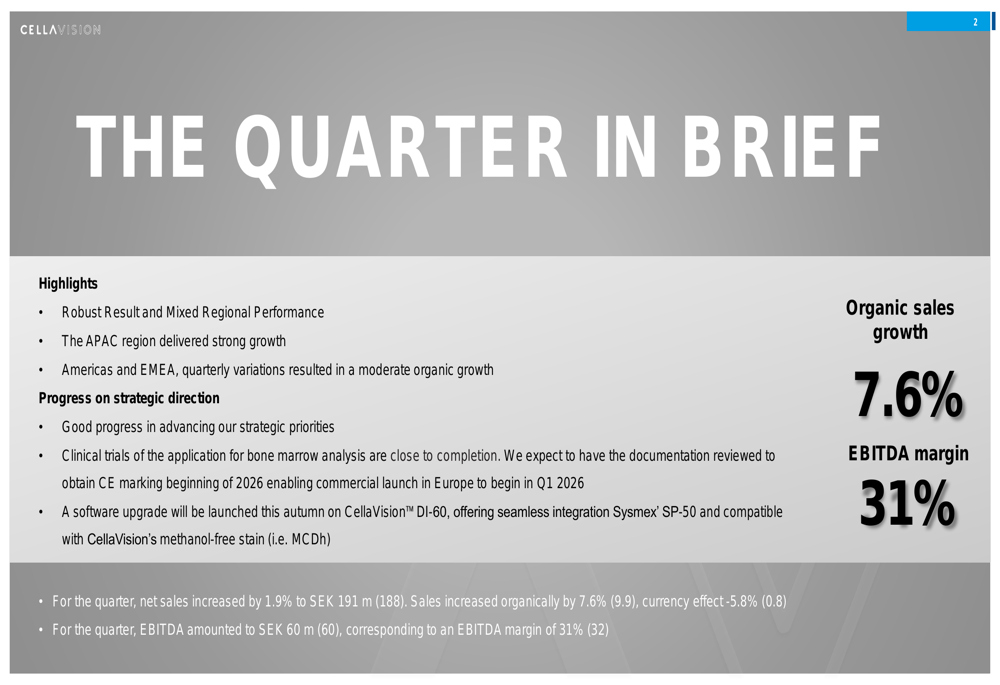

CellaVision AB (STO:CEVI) reported its second-quarter 2025 results on July 18, showing organic growth of 7.6% despite facing significant currency headwinds. The company’s stock rose 1.44% to SEK 183.2 following the presentation, reflecting investor confidence in the company’s strategic direction despite slightly missing revenue forecasts.

The medical technology company, which specializes in digital solutions for blood and bone marrow cell analysis, maintained a solid EBITDA margin of 31% while continuing to invest heavily in research and development, with R&D spending reaching 22% of sales during the quarter.

Quarterly Performance Highlights

CellaVision reported net sales of SEK 191 million for Q2 2025, representing a modest 1.9% increase from SEK 188 million in the same period last year. While organic growth reached 7.6%, this was partially offset by a negative currency effect of 5.8%.

The company maintained its profitability with an EBITDA of SEK 60 million, unchanged from Q2 2024, though the EBITDA margin slightly decreased to 31% from 32%. Gross margin improved to 68% from 66% in the comparable period.

As shown in the following comprehensive financial development table:

Operating cash flow showed significant improvement, increasing to SEK 58 million from SEK 40 million in Q2 2024. The company also reported a negative total cash flow of SEK 30 million, which included a dividend payment to shareholders of SEK 60 million.

Regional Performance Analysis

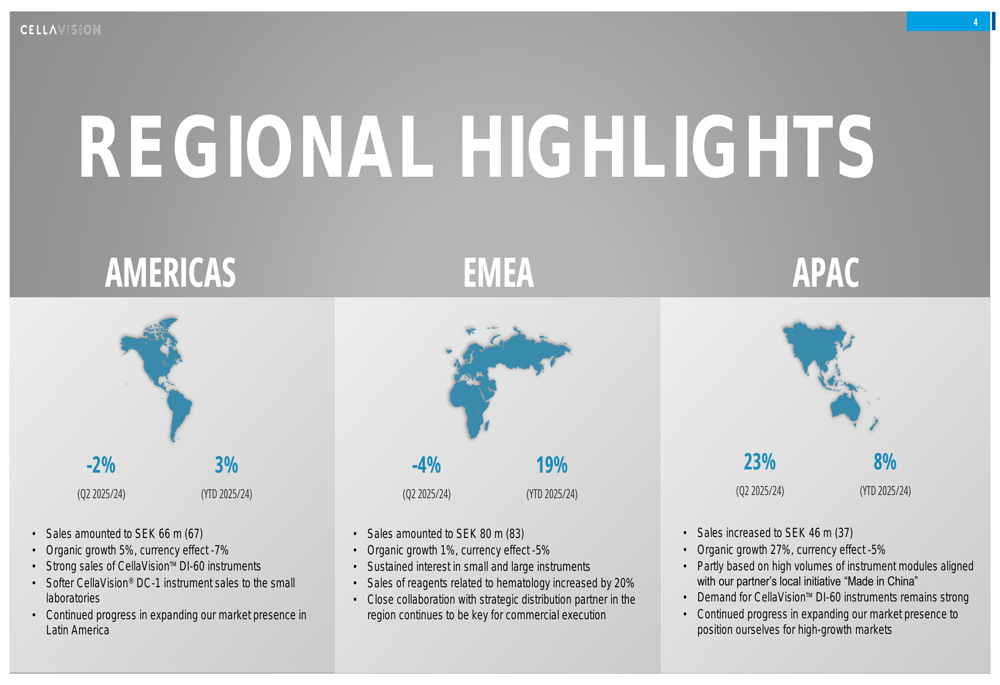

CellaVision’s performance varied significantly across regions, with APAC emerging as the standout performer while Americas and EMEA faced challenges primarily due to currency effects.

The APAC region delivered exceptional growth of 23% year-over-year, with sales increasing to SEK 46 million from SEK 37 million. Organic growth in the region reached an impressive 27%, partially offset by a 5% negative currency effect. This strong performance was partly driven by high volumes of instrument modules aligned with the company’s partner’s "Made in China" initiative.

In contrast, the Americas region experienced a 2% decline in sales to SEK 66 million, despite achieving 5% organic growth that was more than offset by a 7% negative currency effect. EMEA similarly faced challenges with a 4% decline in sales to SEK 80 million, as 1% organic growth was countered by a 5% negative currency effect.

The regional breakdown is illustrated in the following slide:

Product Group Breakdown

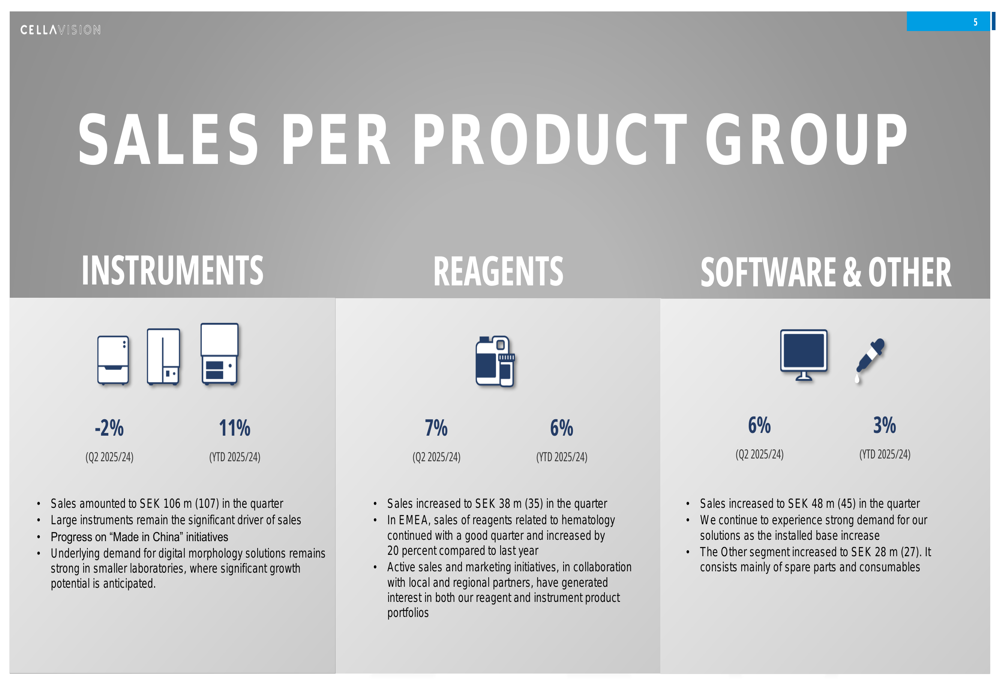

CellaVision’s product portfolio performance showed mixed results across its three main categories: Instruments, Reagents, and Software (ETR:SOWGn) & Other.

Instrument sales, which account for the largest portion of revenue, declined slightly by 2% year-over-year to SEK 106 million. Despite this, the company noted that large instruments remain the significant driver of sales, with progress on "Made in China" initiatives contributing to performance.

Reagent sales showed healthy growth of 7%, increasing to SEK 38 million from SEK 35 million in Q2 2024. Particularly strong performance was seen in EMEA, where reagent sales related to hematology increased by 20% compared to the previous year.

The Software & Other category grew by 6% to SEK 48 million, driven by strong demand for solutions as the installed base increases. The breakdown by product group is detailed in the following slide:

Strategic Initiatives & Outlook

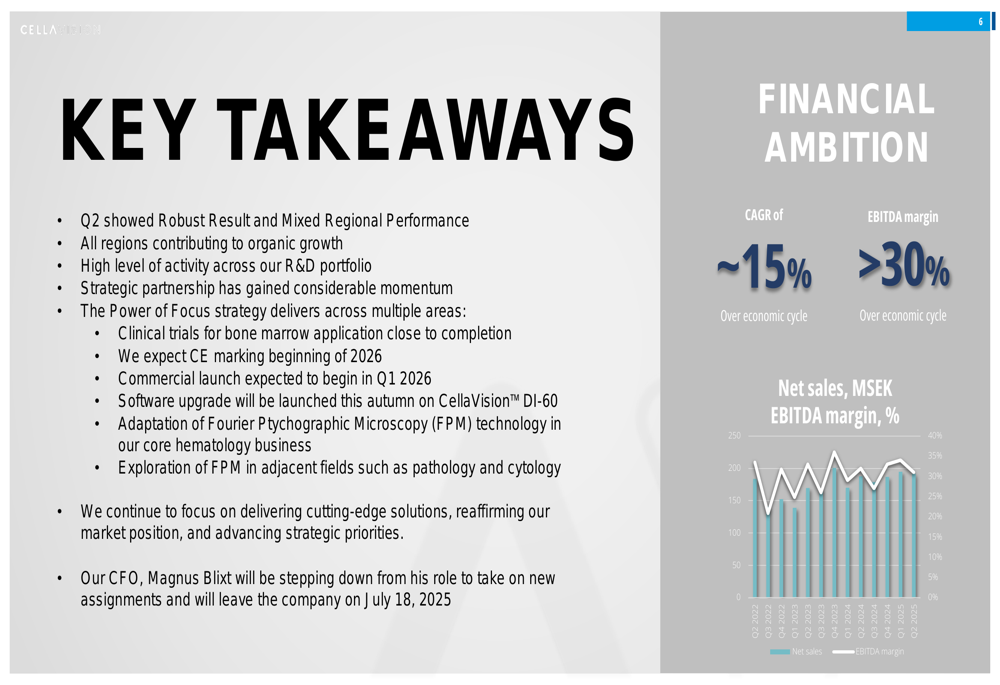

CellaVision highlighted several key strategic initiatives that are progressing well. Most notably, clinical trials for the company’s bone marrow analysis application are nearing completion, with CE marking expected by early 2026 and commercial launch anticipated in Q1 2026. This represents a significant expansion opportunity for the company.

Additionally, CellaVision plans to launch a software upgrade for its DI-60 system this autumn, offering seamless integration with Sysmex’s SP-50 and compatibility with CellaVision’s methanol-free stain.

The company is also advancing its technology through adaptation of Fourier Ptychographic Microscopy (FPM) in its core hematology business, while exploring applications in adjacent fields such as pathology and cytology.

On the management front, CFO Magnus Blixt will be stepping down from his role to pursue new opportunities, with his departure scheduled for July 18, 2025.

The following slide summarizes the key takeaways and strategic direction:

Financial Ambitions & Market Position

CellaVision reaffirmed its long-term financial ambitions, targeting a compound annual growth rate (CAGR) of approximately 15% over the economic cycle, along with an EBITDA margin exceeding 30%. The company’s current performance remains aligned with these targets, with the Q2 2025 EBITDA margin at 31%.

The company’s focus on innovation is evident in its R&D spending, which increased to 22% of sales in Q2 2025 from 19% in the same period last year. This investment is expected to drive future growth through new product developments and enhancements.

Despite slightly missing the revenue forecast of SEK 193.7 million mentioned in recent earnings coverage, CellaVision’s stock has shown resilience, trading at SEK 183.2 following the presentation. This represents a significant recovery from its 52-week low of SEK 147.8, though still well below its 52-week high of SEK 302.

The company’s Q2 highlights, including the 7.6% organic growth and strategic progress, are summarized in the following slide:

As CellaVision continues to execute its "Power of Focus" strategy, the company appears well-positioned to capitalize on growth opportunities in digital morphology, particularly with the upcoming bone marrow application launch and ongoing expansion in high-growth markets like China. However, currency headwinds and regional variations remain factors to monitor in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.