Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Century Aluminum Company (NASDAQ:CENX) released its first quarter 2025 earnings presentation on May 7, showing mixed financial results with lower profitability but improved balance sheet metrics and a positive outlook for Q2. The company’s stock reacted negatively, falling 3.89% during regular trading and an additional 4.8% in aftermarket trading to $15.06.

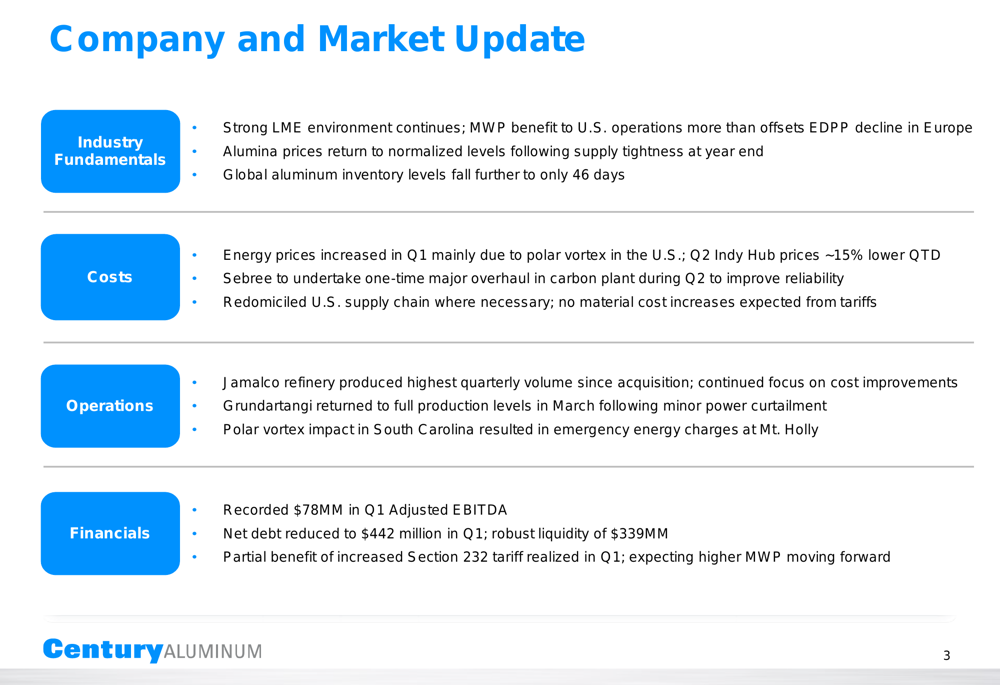

The aluminum producer highlighted strong industry fundamentals with global inventory levels falling to just 46 days of consumption, while emphasizing the strategic importance of its planned new U.S. smelter project backed by Department of Energy funding. The company is operating in a market environment characterized by supply deficits in both the U.S. and European markets, with the U.S. primary aluminum market short approximately 4.2 million tonnes annually.

Quarterly Performance Highlights

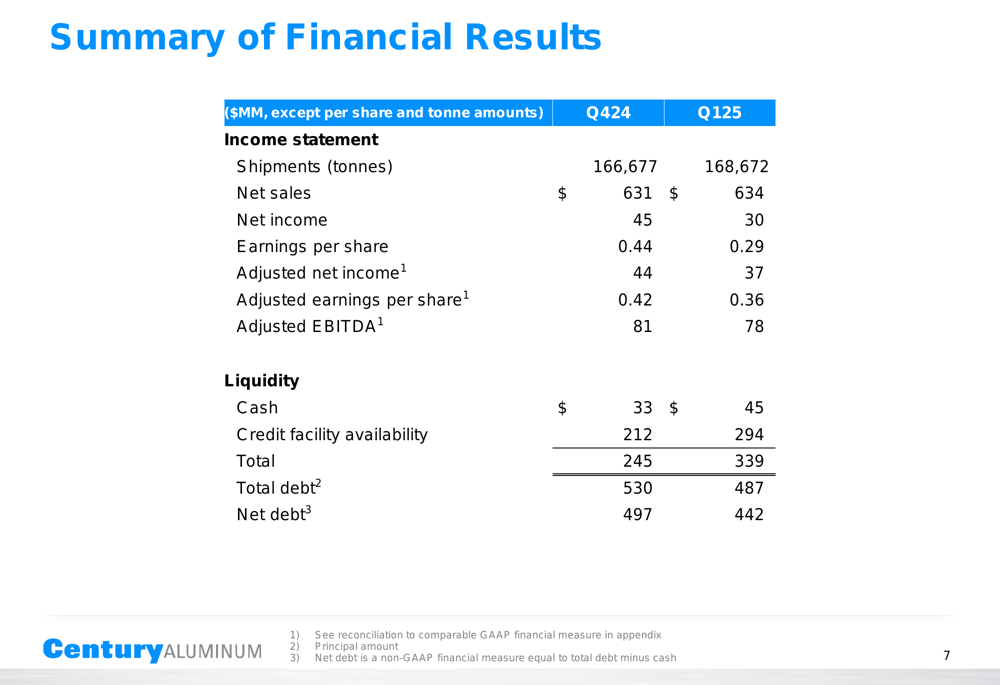

Century Aluminum reported Q1 2025 net income of $29.7 million or $0.29 per share, down from $45.2 million or $0.44 per share in Q4 2024. Adjusted earnings per share came in at $0.36, compared to $0.42 in the previous quarter. Adjusted EBITDA was $78 million, slightly below the $81 million reported in Q4 2024.

Despite the profit decline, the company showed operational improvements with shipments increasing to 168,672 tonnes in Q1 from 166,677 tonnes in Q4. Net sales rose marginally to $634 million from $631 million in the previous quarter.

As shown in the following summary of financial results:

The company significantly strengthened its balance sheet during the quarter, reducing total debt from $530 million to $487 million and net debt from $497 million to $442 million. Cash increased to $45 million from $33 million, while credit facility availability expanded to $294 million from $212 million, bringing total liquidity to $339 million.

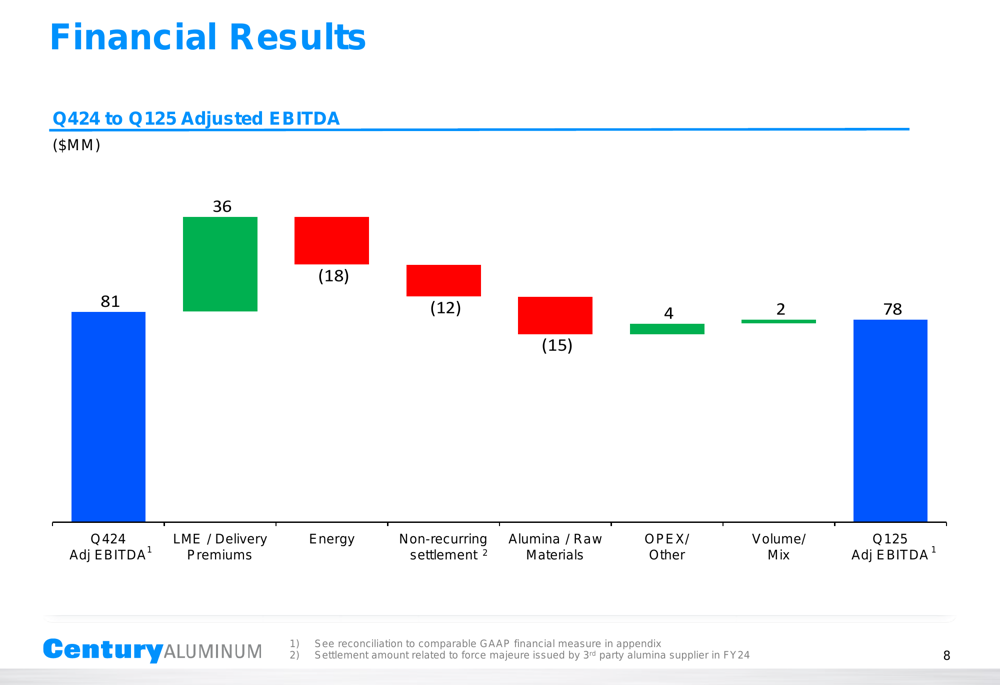

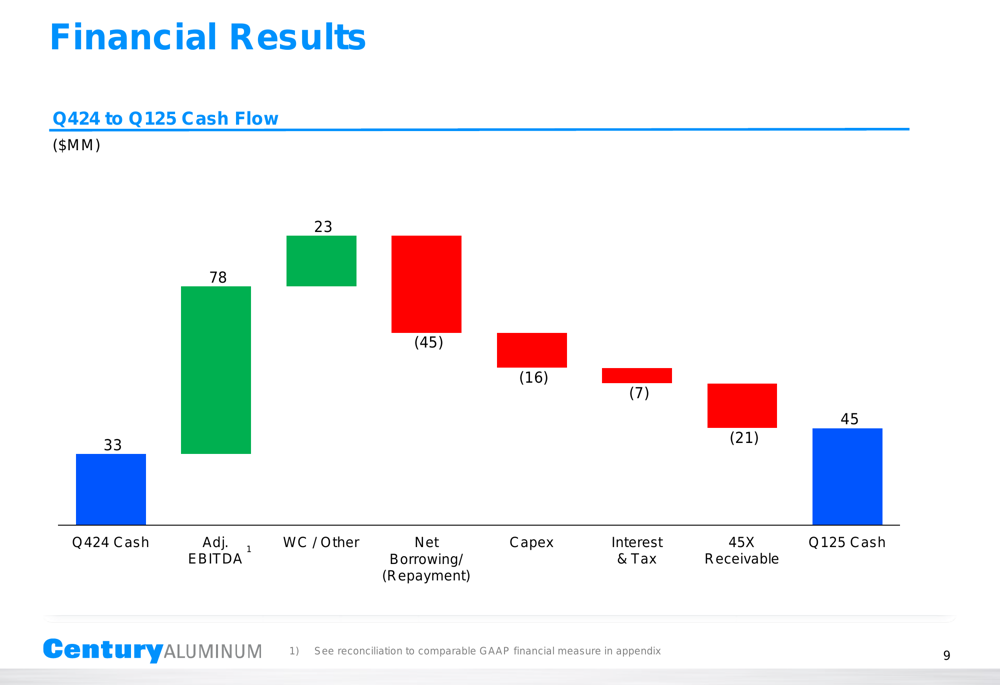

The following chart illustrates the factors contributing to the quarter-over-quarter change in Adjusted EBITDA:

The $3 million decrease in Adjusted EBITDA from Q4 2024 to Q1 2025 was primarily driven by higher energy costs (-$18 million) due to the polar vortex, higher alumina and raw material costs (-$15 million), and a non-recurring settlement (-$12 million). These negative factors were largely offset by benefits from higher LME prices and delivery premiums (+$36 million), operational improvements (+$4 million), and favorable volume/mix effects (+$2 million).

The company’s cash flow dynamics for the quarter are illustrated in this waterfall chart:

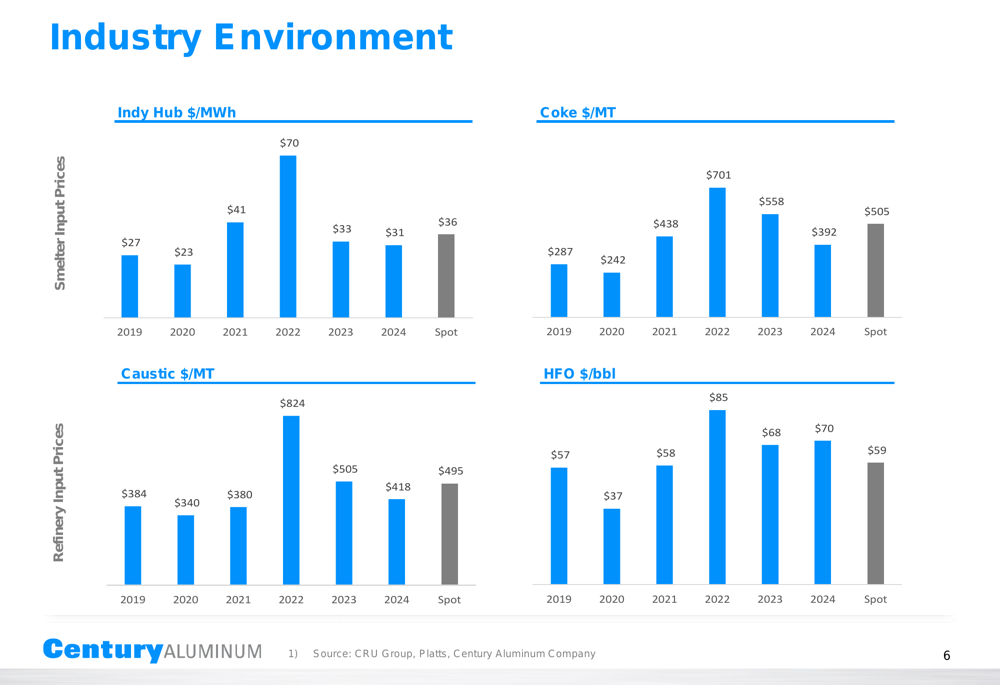

Industry Environment

Century Aluminum operates in a market characterized by strong fundamentals, with global aluminum inventory levels falling to just 46 days. The company noted that the Section 232 tariff rate increased to 25% effective March 12, 2025, providing additional support for U.S. operations.

The following chart shows key industry metrics including LME aluminum prices, alumina prices, regional premiums, and power rates:

The company highlighted that the U.S. Midwest Premium (MWP) has benefited its U.S. operations, offsetting the decline in European Duty Paid Premium (EDPP). Alumina (OTC:AWCMY) prices have returned to more normalized levels after previous volatility.

Century also provided insight into the global supply-demand balance, showing that markets are nearly balanced in 2025, with China balanced at 43.3 million tonnes and the world ex-China balanced at approximately 30.5 million tonnes. However, both the U.S. and EU markets continue to face significant supply deficits.

Strategic Initiatives

A major focus of Century Aluminum’s presentation was its planned new U.S. aluminum smelter project, which has received a commitment of up to $500 million in grant funding from the U.S. Department of Energy. The company is currently evaluating locations in the Mississippi/Ohio River Basins for this facility.

The following slide details the strategic rationale and timeline for this major expansion:

This project addresses the significant supply deficit in the U.S. primary aluminum market, which is currently short approximately 4.2 million tonnes annually. The company emphasized that there are only four operating smelters in the U.S. despite it being the second-largest aluminum consumer globally.

The new smelter project is expected to have a 4-6 year timeline until first metal production, with near-term milestones including site selection, energy sourcing, and detailed engineering work. This initiative aligns with national security interests by reshoring production capacity of this critical mineral.

Century also provided an overview of its current production capacity and utilization rates:

The company’s aluminum facilities are currently operating at 70% of their total capacity of 1,020 kMT, while its carbon anode facility in the Netherlands is at 100% capacity and the Jamalco bauxite mining and alumina refinery in Jamaica is operating at 80% capacity.

Forward-Looking Statements

For Q2 2025, Century Aluminum projects Adjusted EBITDA of $80-90 million, representing an improvement from the $78 million reported in Q1. This outlook is based on several assumptions, including an LME aluminum price of $2,513/MT, U.S. Midwest Premium of $866/MT, and European Duty Paid Premium of $220/MT.

The following slide details the company’s Q2 outlook and key assumptions:

The projected improvement in Q2 Adjusted EBITDA is expected to be driven by favorable movements in LME and delivery premiums (+$10 million), energy costs (+$10 million), and volume/mix effects (+$5 million), partially offset by raw materials costs (-$5 to -$10 million) and other operational expenses (-$10 to -$15 million).

For the full year 2025, Century provided the following financial assumptions:

The company expects total aluminum shipments of 700 kMT for the full year, with depreciation and amortization of $85-90 million, SG&A expenses of $45-50 million, and interest expense of $40-45 million. Capital expenditures are projected at $45-50 million for sustaining capex and $25-30 million for investment capex.

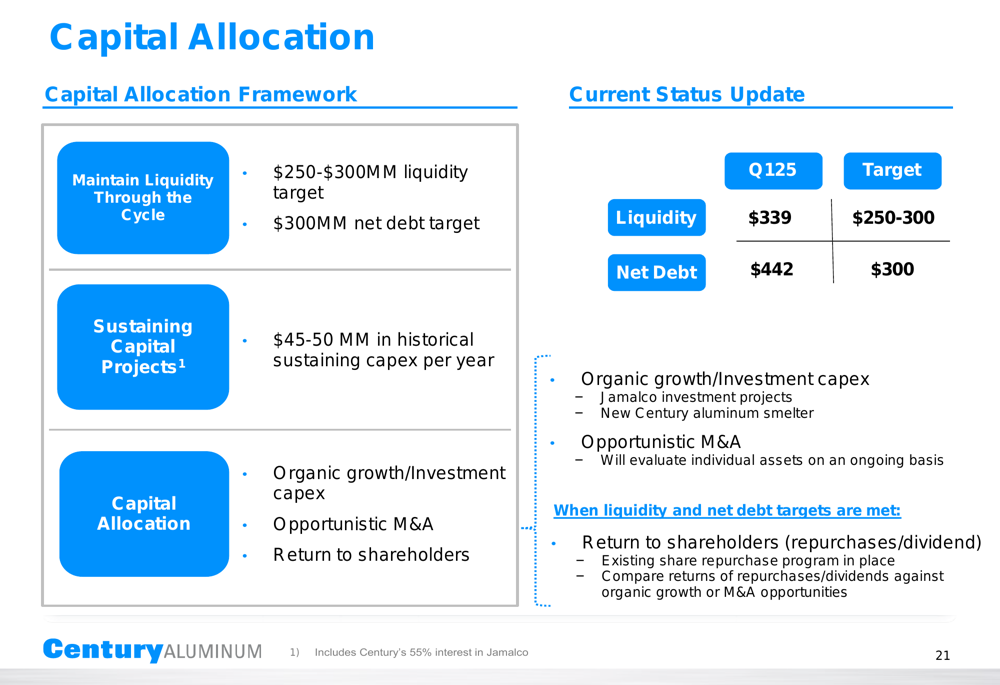

Century Aluminum continues to focus on its capital allocation framework, with current priorities on improving liquidity and reducing net debt. The company has set targets of $250-300 million for liquidity (versus $339 million in Q1) and $300 million for net debt (versus $442 million in Q1). Once these targets are met, the company plans to return capital to shareholders through repurchases or dividends.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.