Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

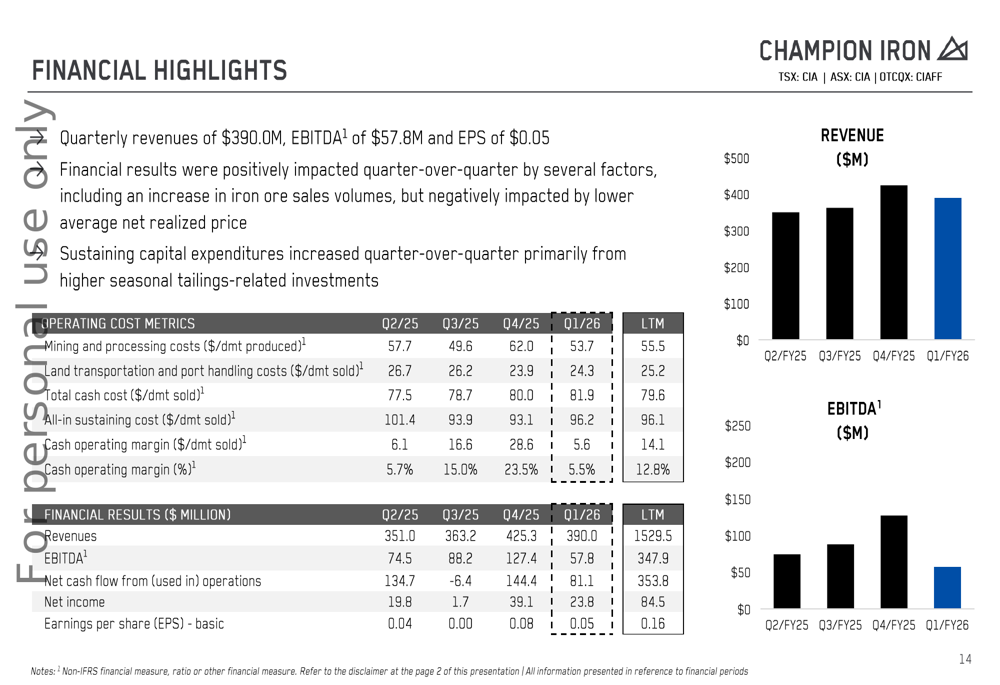

Champion Iron Ltd (ASX:CIA) reported its first quarter fiscal 2026 results on July 30, 2025, showing declining profitability despite record sales volumes as the company navigated operational challenges and softer iron ore prices. The Quebec-based iron ore producer saw its EBITDA drop to $57.8 million from $127.4 million in the previous quarter, while continuing to advance strategic growth projects aimed at producing higher-grade iron ore products.

The company’s performance took place against a backdrop of declining iron ore prices, with the P65 index averaging US$108.4 during the quarter, down 7.3% quarter-over-quarter due to reduced global steel demand, particularly in China. Despite these headwinds, Champion maintained its focus on long-term strategic initiatives designed to capitalize on the growing demand for high-purity iron ore.

Quarterly Performance Highlights

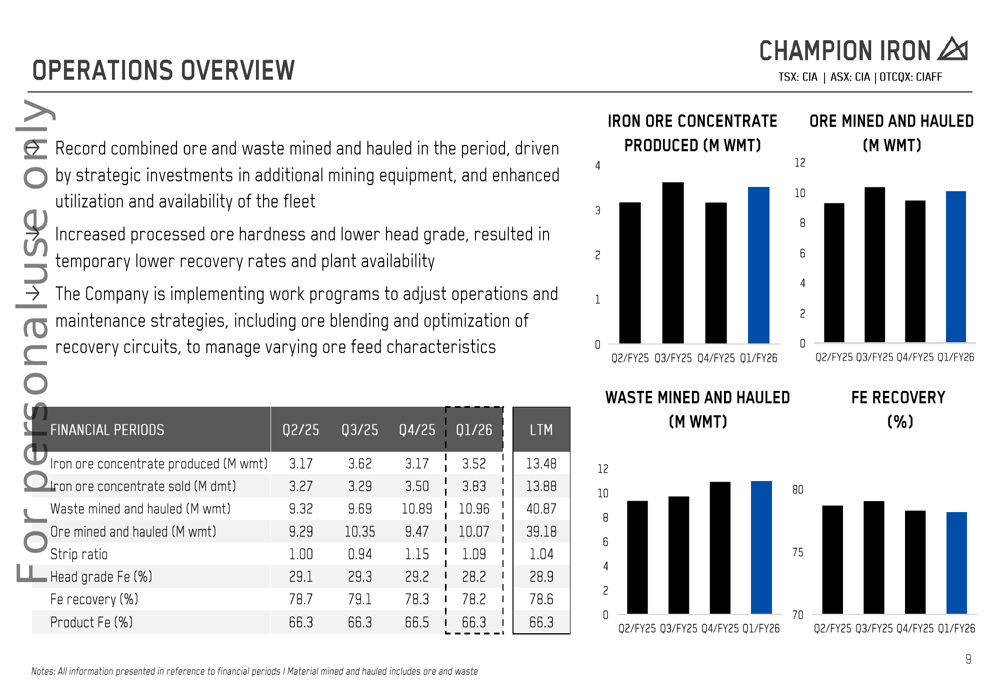

Champion Iron achieved record quarterly sales of 3.83 million dry metric tonnes (DMT) in Q1 FY2026, despite scheduled third-party rail infrastructure maintenance. However, production volumes of 3.52 million wet metric tonnes (WMT) were impacted by increased ore hardness, lower head grade, reduced plant availability, and a scheduled annual power interruption.

The company reported quarterly revenue of $390.0 million, down from $425.3 million in the previous quarter. Net income came in at $23.8 million, resulting in earnings per share of $0.05, compared to $0.08 in Q4 FY2025. This represents a continuation of the earnings challenges noted in the previous quarter, when Champion missed analyst expectations.

As shown in the following chart of quarterly financial performance:

The company’s total cash cost rose to $81.9/DMT sold, up from $80.0/DMT in the previous quarter and $76.9/DMT in the same quarter last year. This 7% year-over-year increase was primarily attributed to the drawdown of higher-cost inventory. All-in sustaining costs also increased to $96.2/DMT sold. These rising costs, combined with lower realized prices, squeezed the cash operating margin to just 5.5%, down significantly from 23.5% in the previous quarter.

Operational Challenges

Champion’s operational performance was notably affected by challenges related to ore quality and processing. The company explained that it recently encountered higher ore hardness and lower head grades due to mining in an extension of the Pignac pit, which represents about 4% of Bloom Lake’s mineral reserves but approximately 10% of the expected ore feed for FY2026.

The following operations overview illustrates the impact of these challenges on production metrics:

Mining and processing costs increased to $53.7/DMT produced, a 12% rise year-over-year, primarily due to higher stripping activities, lower production volumes, and increased maintenance requirements. Despite these challenges, the company achieved record levels of combined ore and waste mined and hauled, reflecting the benefits of strategic investments in equipment.

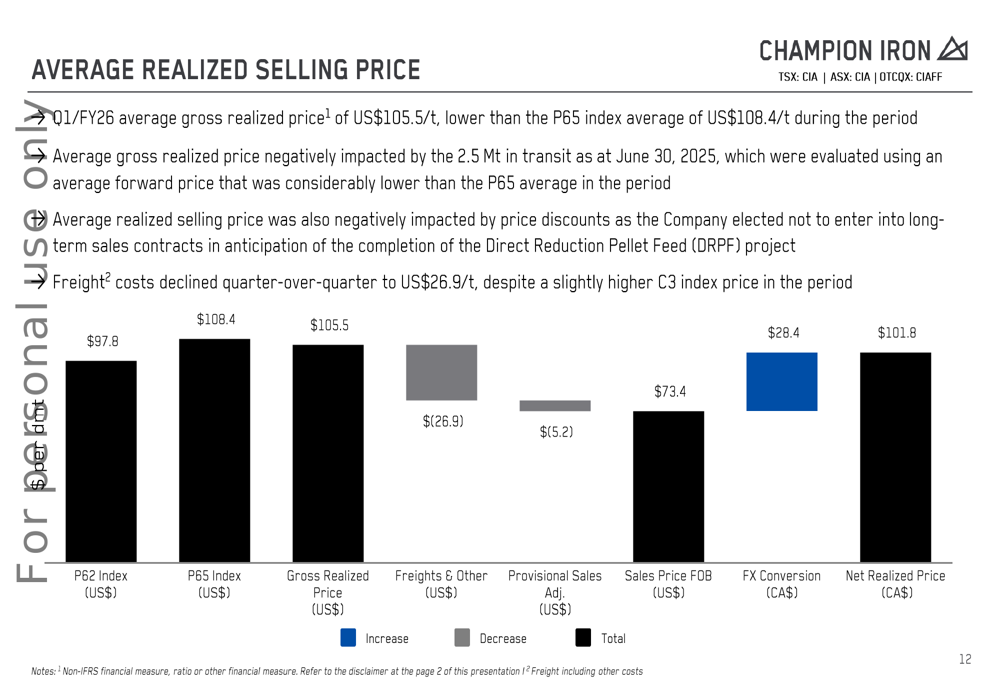

The company’s realized selling price was also negatively impacted by market conditions and provisional pricing adjustments. As shown in the following breakdown:

Champion realized an average gross price of US$105.5/t, lower than the P65 index average of US$108.4/t during the period. The average realized price was further reduced by a negative provisional pricing adjustment of US$5.2/DMT and freight costs of US$26.9/t, resulting in a net realized price of CA$101.8/DMT.

Strategic Initiatives

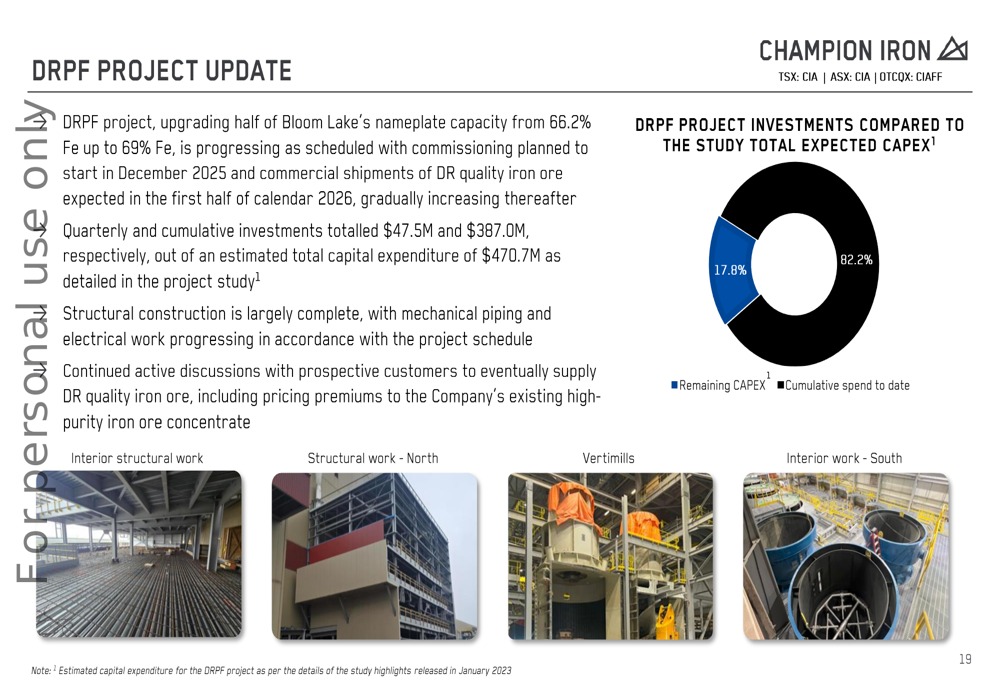

Despite current operational challenges, Champion continues to advance its key growth projects, most notably the Direct Reduction Pellet Feed (DRPF) project. This initiative aims to upgrade half of Bloom Lake’s nameplate capacity from 66.2% Fe up to 69% Fe, positioning the company to supply premium products to the growing direct reduction iron (DRI) market.

The following chart shows the progress of the DRPF project:

The company has invested $47.5 million in the DRPF project during the quarter, bringing cumulative investments to $387.0 million, or 82.2% of the estimated total capital expenditure of $470.7 million. Commissioning is planned to start in December 2025, with commercial shipments of DR quality iron ore expected in the first half of calendar 2026.

Champion also announced a significant partnership for its Kami project, entering into a definitive framework agreement with Nippon Steel Corporation and Sojitz Corporation. The Japanese partners will contribute $245 million for a combined 49% interest in the project, with Nippon taking a 30% stake and Sojitz 19%. This transaction is expected to close in two steps, with an initial contribution of $68.6 million in the second half of calendar 2025.

Financial Position

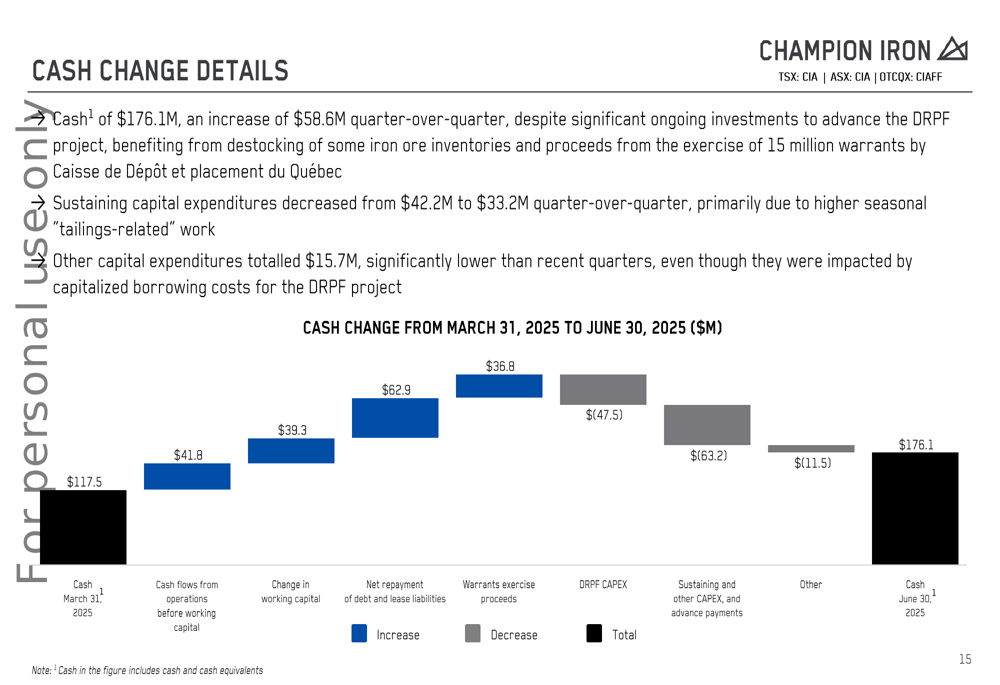

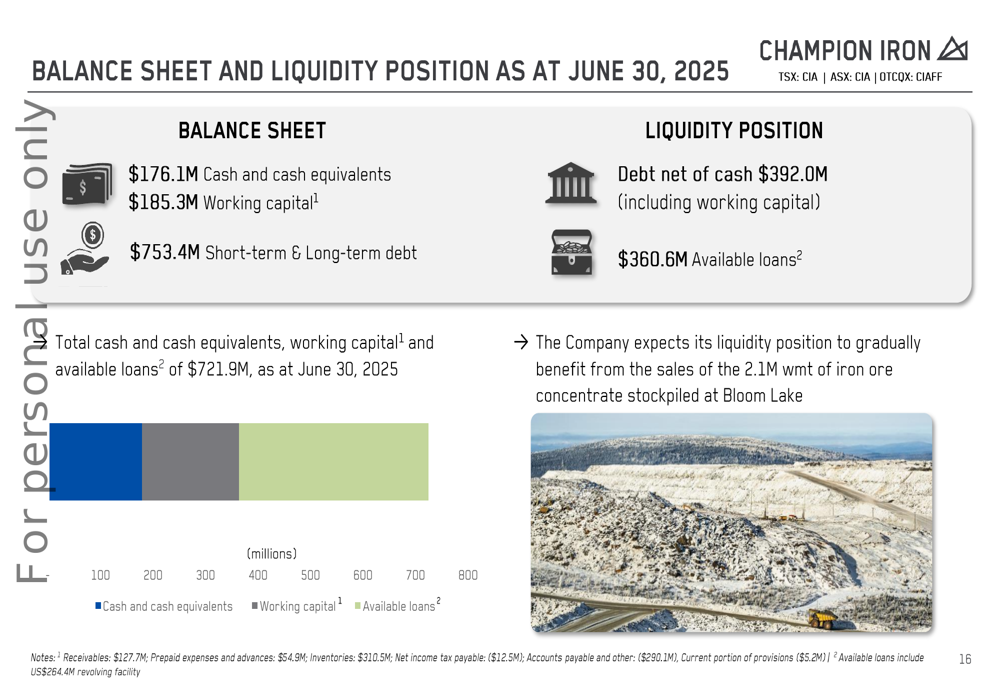

Despite operational challenges, Champion strengthened its financial position during the quarter. Cash and cash equivalents increased by $58.6 million to $176.1 million, while working capital stood at $185.3 million. The following waterfall chart illustrates the key drivers of the cash position improvement:

The company’s liquidity position remains solid, with total available cash, working capital, and undrawn loan facilities totaling $721.9 million as of June 30, 2025:

After the quarter end, Champion completed a successful offering of US$500 million in Senior Unsecured Notes due 2032, which was upsized from the initially announced US$450 million due to strong investor demand. The notes carry an interest rate of 7.875%, payable semi-annually. Proceeds were used to repay the Term Loan of US$230 million and US$105 million outstanding balance from the Revolving Facility, extending debt maturities with minimal impact on the company’s net debt position.

Market Outlook

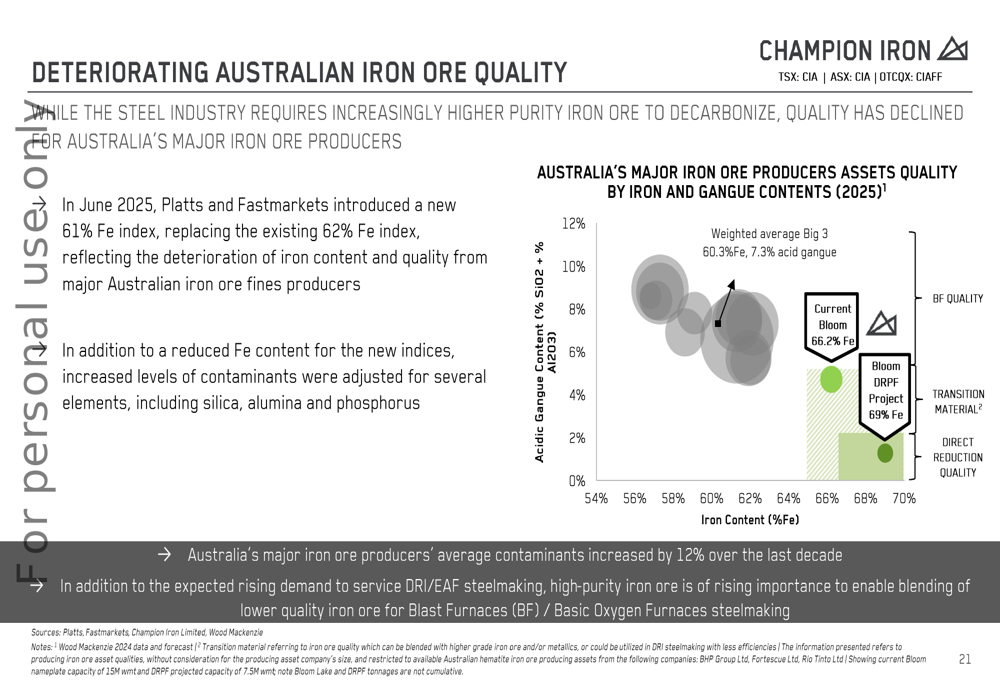

Champion highlighted a significant market trend that supports its strategic focus on high-grade iron ore products: the deteriorating quality of Australian iron ore at a time when the steel industry requires increasing purity. The company noted that in June 2025, industry price reporting agencies Platts and Fastmarkets introduced a new 61% Fe index, replacing the existing 62% Fe index, reflecting this quality deterioration.

The following chart illustrates Champion’s competitive positioning in terms of iron ore quality:

According to the company, Australia’s major iron ore producers have seen average contaminants increase by 12% over the last decade. This trend creates opportunities for Champion’s high-purity products, both for the growing DRI/EAF steelmaking segment and for blending with lower-quality iron ore in traditional blast furnace operations.

As Champion navigates current operational challenges and market headwinds, its strategic investments in higher-grade products and expanded partnerships position the company to potentially benefit from these industry trends in the coming years, though investors will be watching closely to see if the company can reverse the recent trend of declining profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.