Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

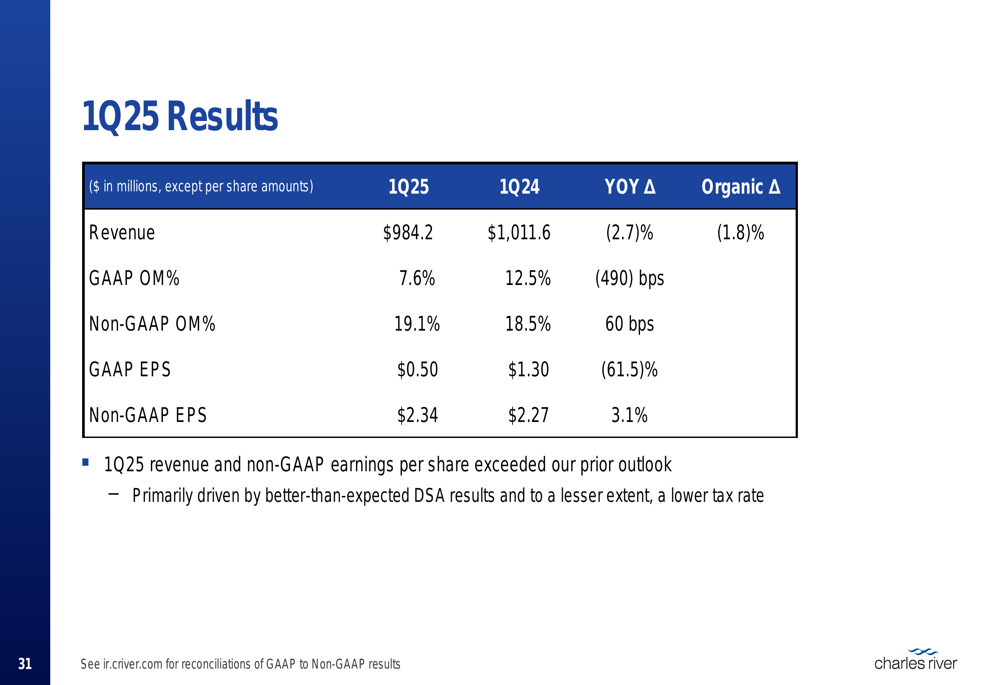

Charles River Laboratories (NYSE:CRL) reported better-than-expected first quarter 2025 results on May 7, driving shares up 17.84% in premarket trading to $136. The company outperformed its February outlook despite ongoing market challenges, with particular strength in its Discovery (NASDAQ:WBD) and Safety Assessment (DSA) segment.

The preclinical contract research organization (CRO) reported revenue of $984.2 million, representing a 2.7% year-over-year decline on a reported basis and a 1.8% decline organically. While all three business segments experienced low-single-digit organic revenue decreases, the results exceeded management’s previous expectations of a mid-single-digit organic decline.

As shown in the following summary of Q1 2025 results, the company delivered non-GAAP earnings per share of $2.34, up 3.1% from $2.27 in the prior-year period, despite the revenue decline:

Quarterly Performance Highlights

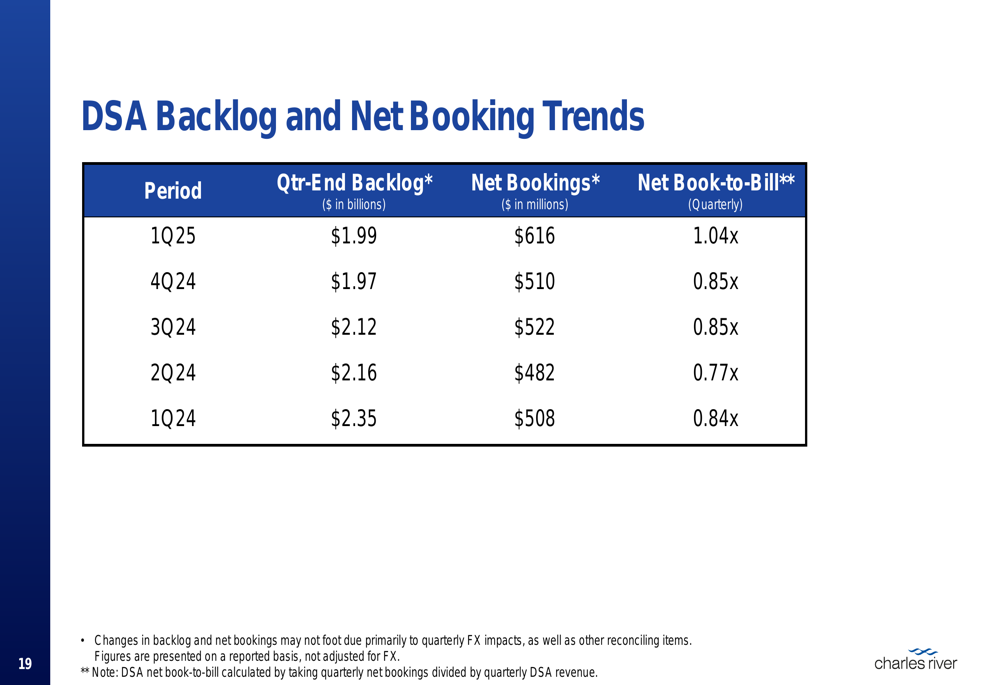

The company’s DSA segment showed encouraging signs of recovery, with the net book-to-bill ratio improving to 1.04x in Q1 2025, marking the first time this key metric has exceeded 1.0x since the second half of 2022. This improvement was primarily driven by stronger quarterly net booking activity, which reached $616 million, representing more than a 20% increase both year-over-year and sequentially.

The following chart illustrates the positive trend in DSA backlog and booking metrics:

Revenue for small and mid-sized biotech clients grew for a second consecutive quarter, while revenue from global biopharma clients declined. The company noted that incremental Q1 booking activity largely consisted of studies with quicker start dates, which is expected to benefit revenue in the first half of 2025.

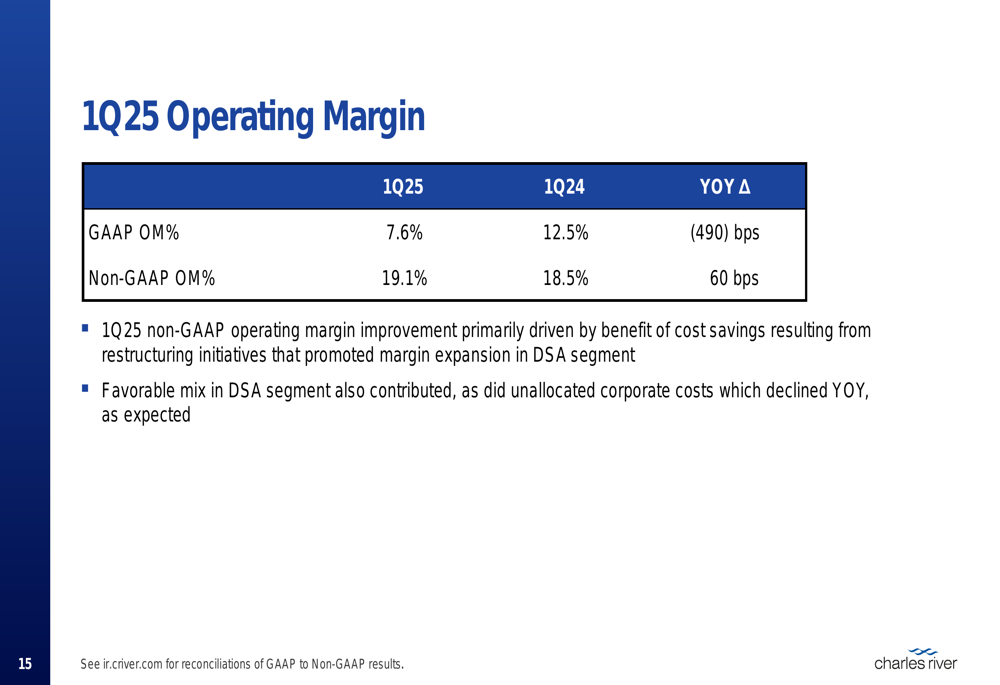

Despite the revenue decline, Charles River improved its non-GAAP operating margin to 19.1% in Q1 2025, up from 18.5% in the prior-year period. This improvement was primarily driven by cost savings resulting from restructuring initiatives and favorable mix in the DSA segment.

Strategic Initiatives

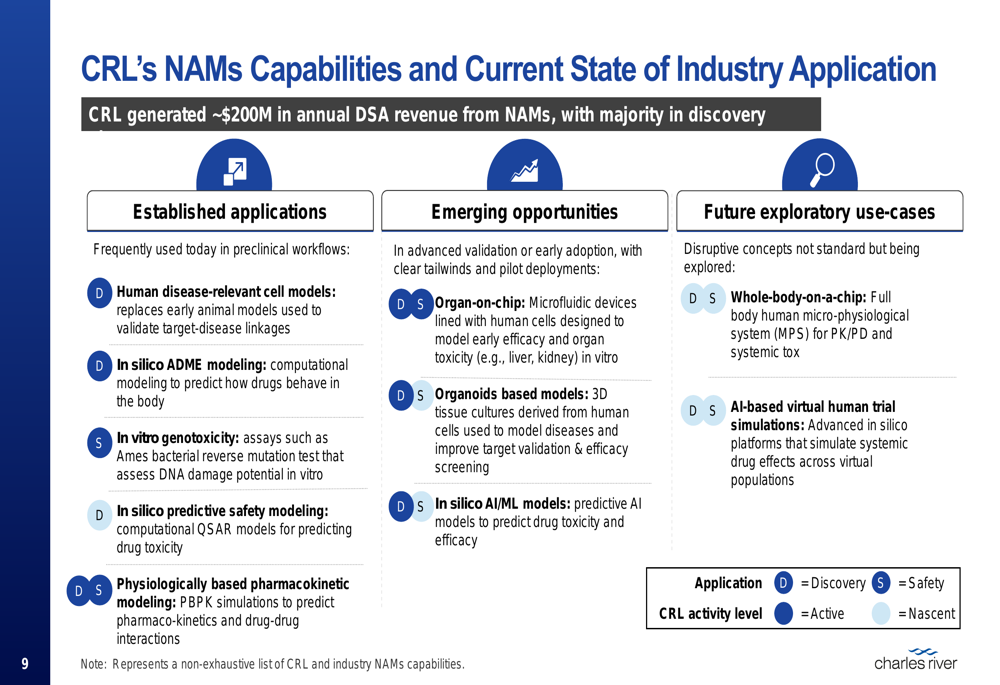

A significant portion of the presentation focused on Charles River’s response to the FDA’s recent announcement regarding the acceleration of new approach methods (NAMs) to reduce animal testing in preclinical safety assessment. The company currently generates approximately $200 million in annual DSA revenue from NAMs, with the majority coming from discovery services.

As shown in the following chart, Charles River has developed a range of NAMs capabilities across different applications, positioning itself as a leader in this evolving field:

Management emphasized that the transition to NAMs will be evolutionary rather than revolutionary, describing it as "a longer-term journey - one that is much longer than 3 to 5 years." The company believes a hybrid model that incorporates both NAMs and animal data will prove to be the best approach to ensure patient safety for regulated testing over the longer term.

The company also announced actions to enhance value creation in conjunction with new shareholder Elliott Investment Management. Charles River welcomed four new members to its Board of Directors and established a Strategic Planning and Capital Allocation Committee to undertake a comprehensive strategic review of the business to evaluate initiatives to unlock additional value.

Forward-Looking Statements

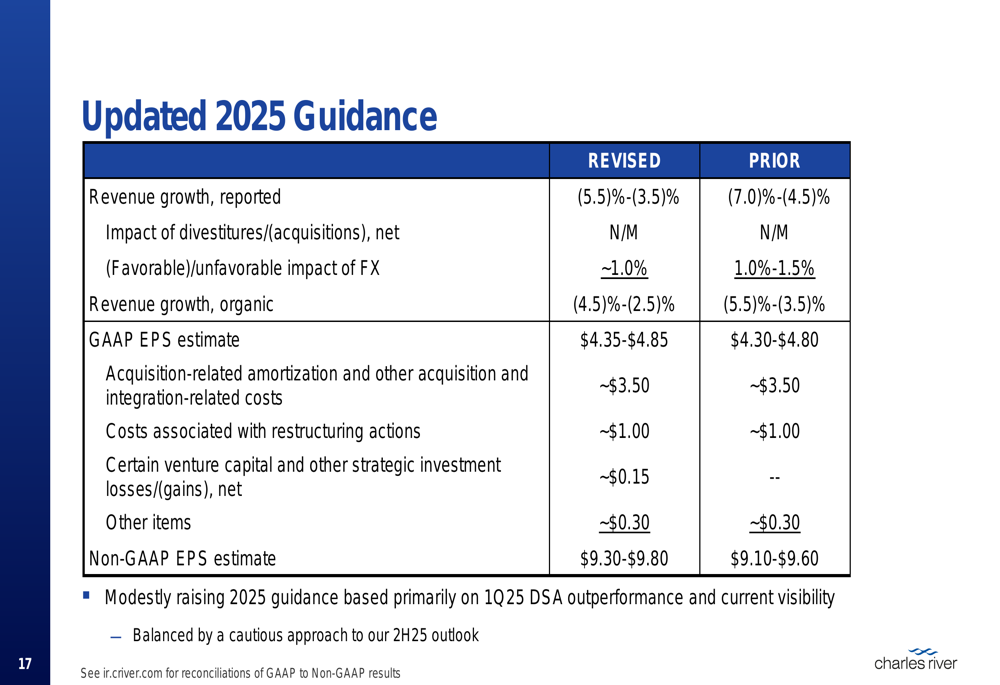

Based primarily on the Q1 DSA outperformance, Charles River modestly raised its 2025 guidance. The company now expects organic revenue to decline 2.5% to 4.5%, an improvement from its previous guidance of a 3.5% to 5.5% decline. Non-GAAP EPS guidance was raised to $9.30-$9.80, up from the previous range of $9.10-$9.60.

The following table details the updated 2025 guidance compared to prior expectations:

For the second quarter of 2025, management expects a low- to mid-single-digit decline in organic revenue year-over-year, with non-GAAP EPS projected to increase by mid- to high-single digits sequentially from the $2.34 reported in Q1 2025.

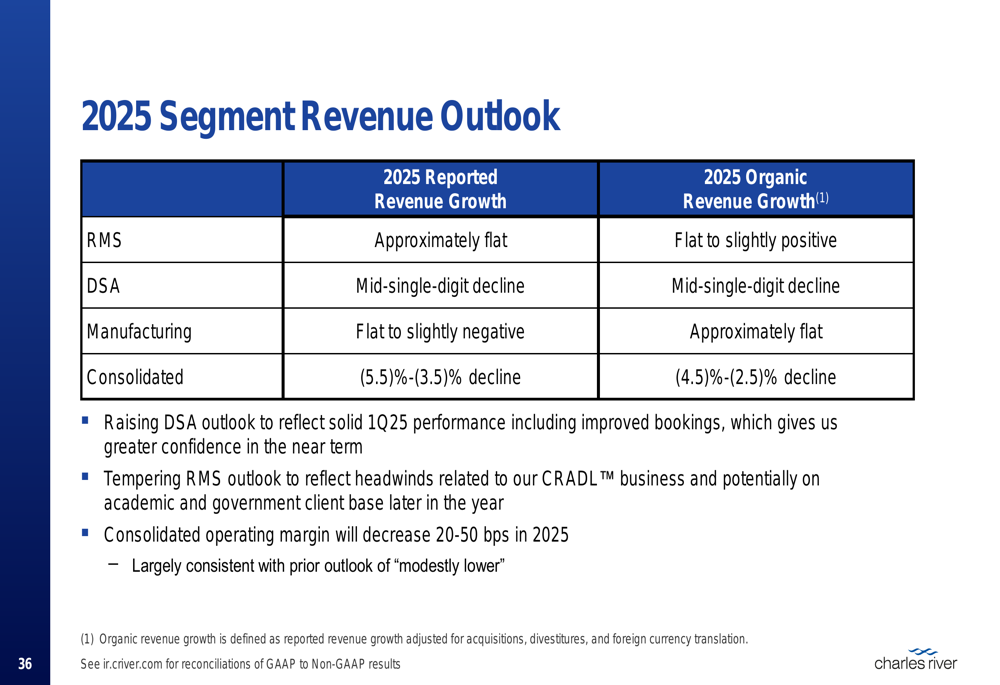

The company also provided a segment-specific outlook for 2025, raising its DSA forecast while tempering expectations for the Research Models and Services (RMS) segment due to concerns about potential NIH budget cuts:

Detailed Financial Analysis

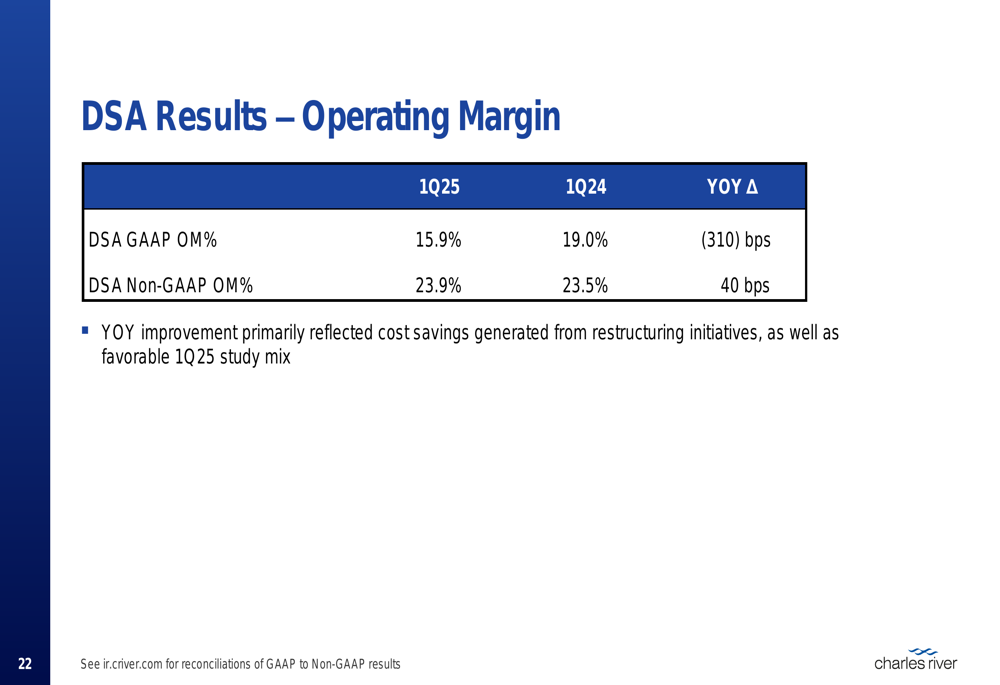

Charles River’s DSA segment, which accounts for approximately 60% of total revenue, reported $592.6 million in Q1 2025 revenue, down 2.1% on a reported basis and 1.4% organically from the prior-year period. Despite the revenue decline, the segment’s non-GAAP operating margin improved by 40 basis points to 23.9%, reflecting cost savings from restructuring initiatives and favorable study mix.

The RMS segment generated $213.1 million in revenue, down 3.5% reported and 2.5% organically year-over-year. The decline was primarily driven by timing of non-human primate (NHP) shipments in China and lower revenue for the Cell Solutions business. The segment’s non-GAAP operating margin decreased by 50 basis points to 27.1%.

The Manufacturing segment reported $178.5 million in revenue, down 3.6% reported and 2.2% organically. The decline was driven primarily by lower commercial revenue in the CDMO business and a slow start for Biologics Testing. The segment’s non-GAAP operating margin declined by 220 basis points to 23.1% due principally to lower commercial revenue in the CDMO business.

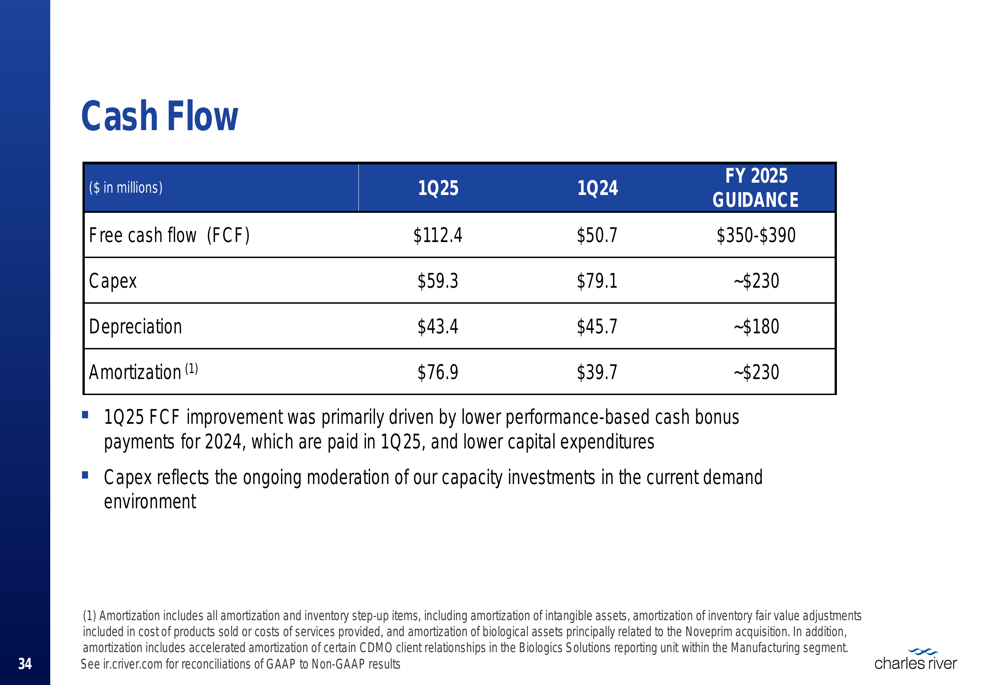

Free cash flow improved to $112.4 million in Q1 2025, primarily driven by lower performance-based cash bonus payments for 2024 and lower capital expenditures:

The company completed the repurchase of $350 million in common stock during Q1 2025, reflecting management’s belief that the company is significantly undervalued. At the end of Q1, Charles River had outstanding debt of $2.5 billion with approximately 60% at a fixed interest rate, resulting in gross leverage of 2.5x and net leverage of 2.4x.

In conclusion, Charles River Laboratories delivered better-than-expected Q1 2025 results despite ongoing market challenges, with particular strength in its DSA segment. The company is positioning itself as a leader in the transition to new approach methods while undertaking a strategic review to enhance shareholder value. With signs of stabilization in the market and improved booking trends, management has raised its full-year guidance, though it remains cautious about the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.