Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

GPS Participacoes e Empreendimentos SA (GGPS3) released its third quarter 2025 results on November 13, showcasing continued revenue growth driven by both organic expansion and strategic acquisitions. The company’s stock closed at R$19.41, near its 52-week high of R$19.98, indicating investor confidence despite some margin pressure evident in the quarterly results.

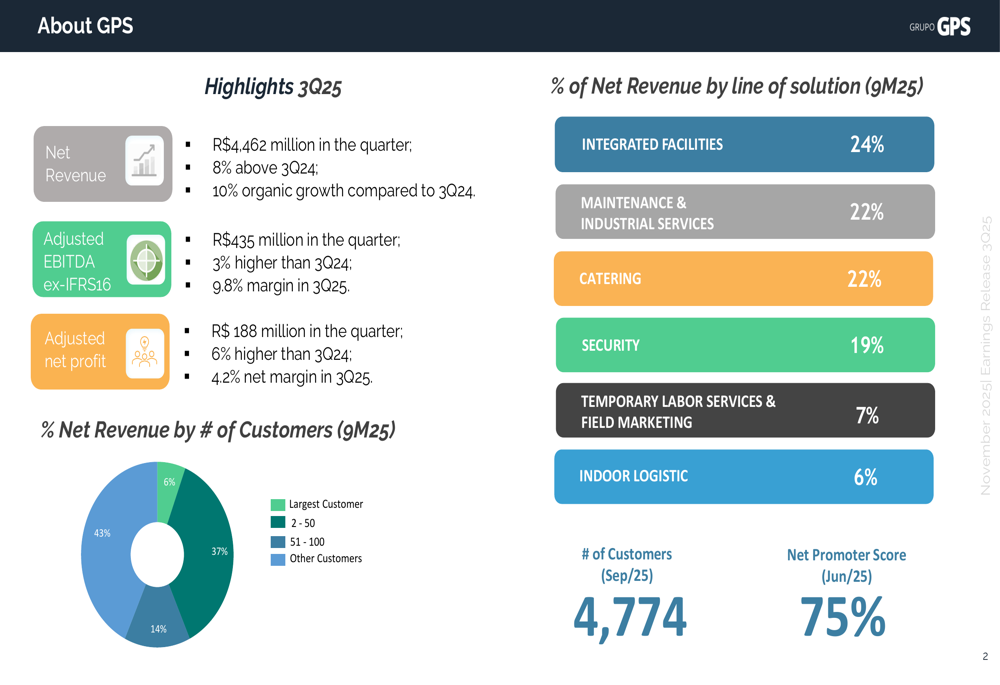

The Brazilian outsourced services provider continues to execute its growth strategy through a combination of organic expansion and an aggressive acquisition program, which has added 26 companies to its portfolio since its IPO. The company’s diversified customer base includes 4,774 clients as of September 2025, though its largest customer still accounts for 43% of net revenue.

Quarterly Performance Highlights

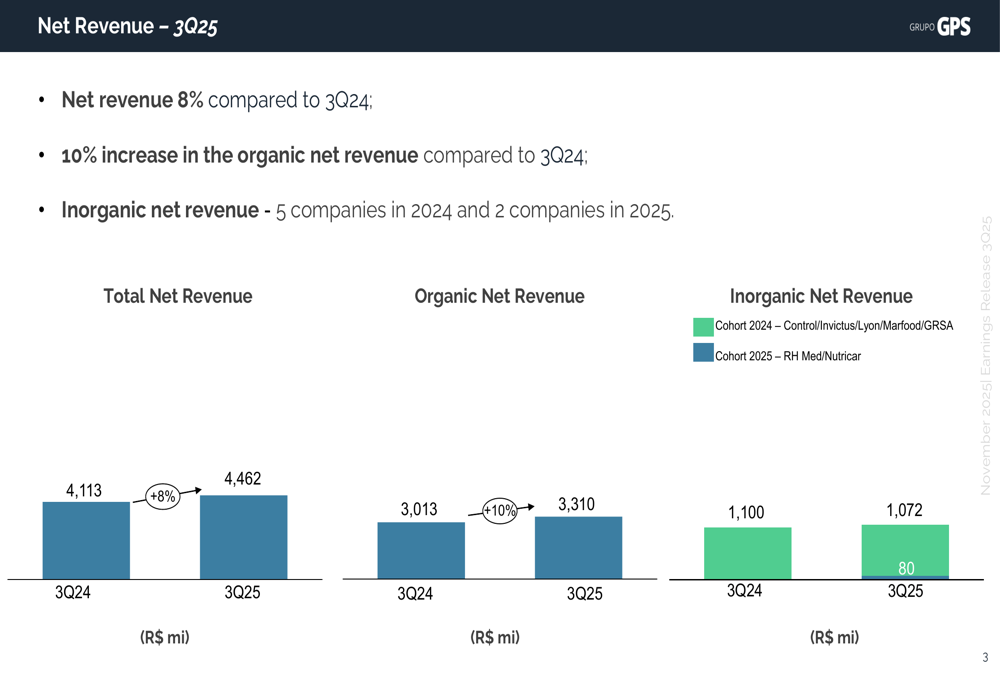

GPS Participacoes reported net revenue of R$4,462 million for Q3 2025, representing an 8% increase compared to the same period last year. The company achieved 10% organic growth, while inorganic revenue from acquisitions contributed to the overall performance.

As shown in the following chart detailing the company’s Q3 revenue breakdown:

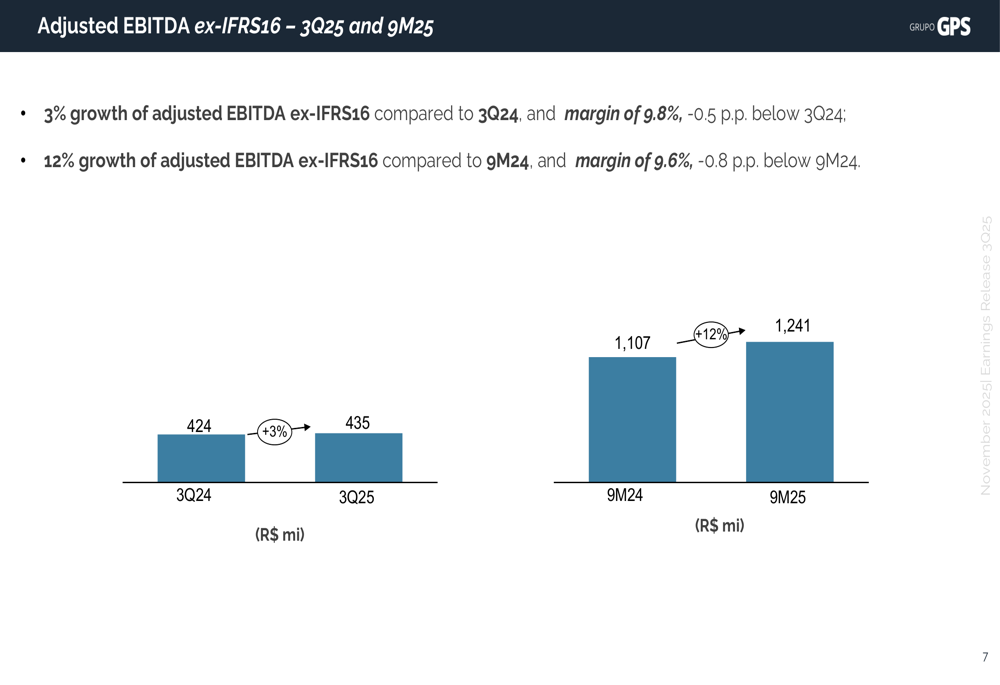

The company’s adjusted EBITDA excluding IFRS16 effects reached R$435 million, a 3% increase from Q3 2024. However, the EBITDA margin contracted slightly to 9.8%, down 0.5 percentage points year-over-year, highlighting some pressure on profitability despite revenue growth.

The quarterly EBITDA performance is illustrated in this chart:

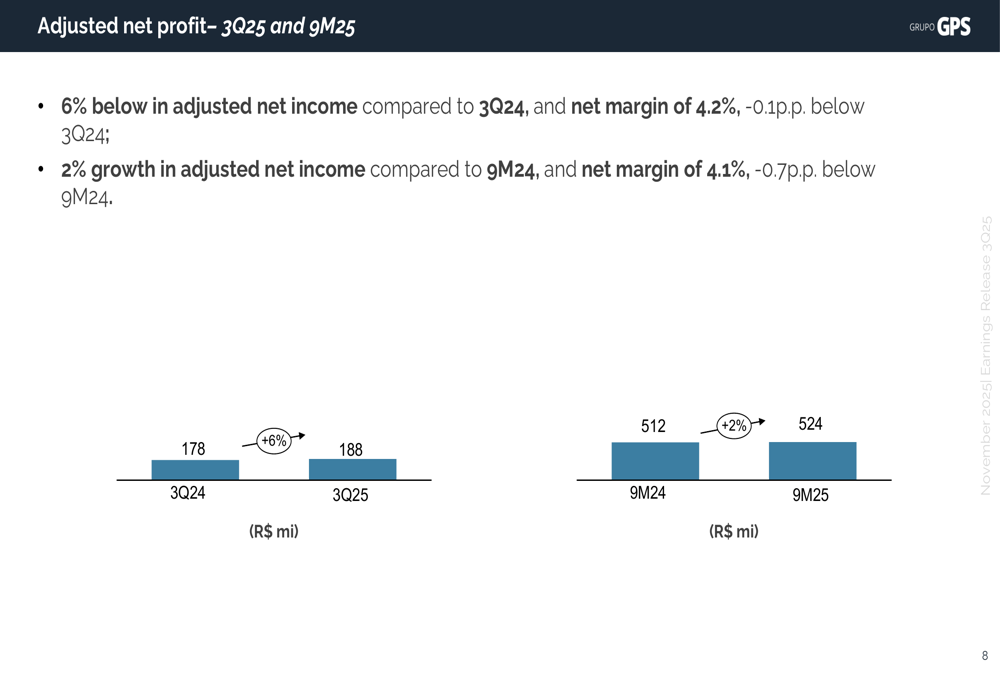

Adjusted net profit grew 6% to R$188 million, with a net margin of 4.2%, representing a minor decline of 0.1 percentage points compared to the previous year. This demonstrates the company’s ability to grow its bottom line despite margin challenges.

The net profit trends can be seen in the following visualization:

Detailed Financial Analysis

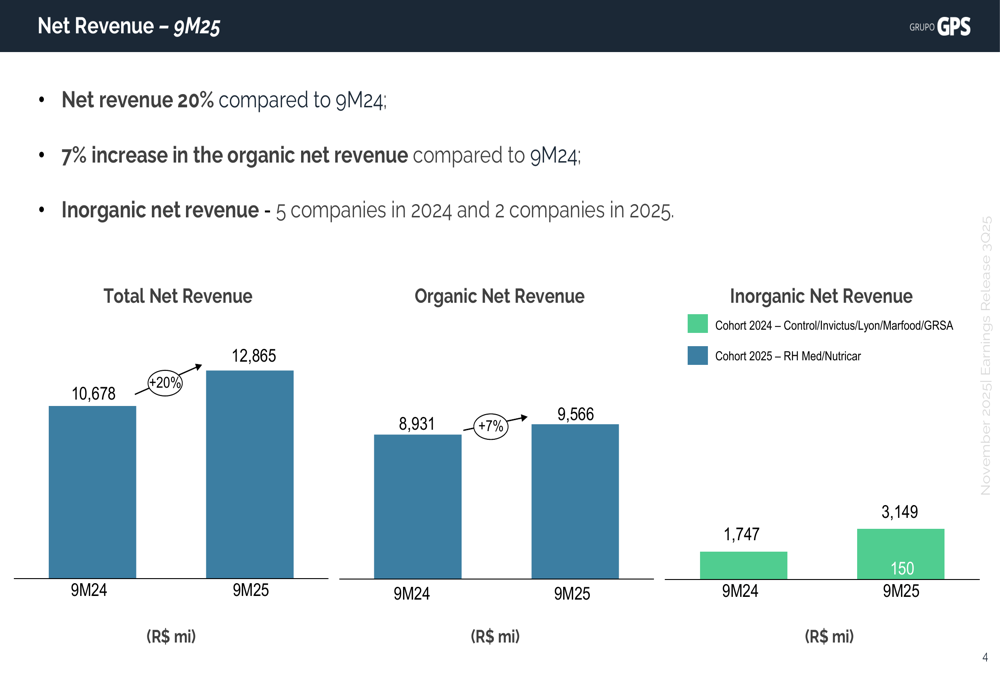

For the first nine months of 2025, GPS Participacoes achieved even stronger growth, with net revenue reaching R$12,865 million, a 20% increase compared to the same period in 2024. Organic growth for the nine-month period stood at 7%, while acquisitions contributed significantly to the overall revenue expansion.

The nine-month revenue performance is detailed in this chart:

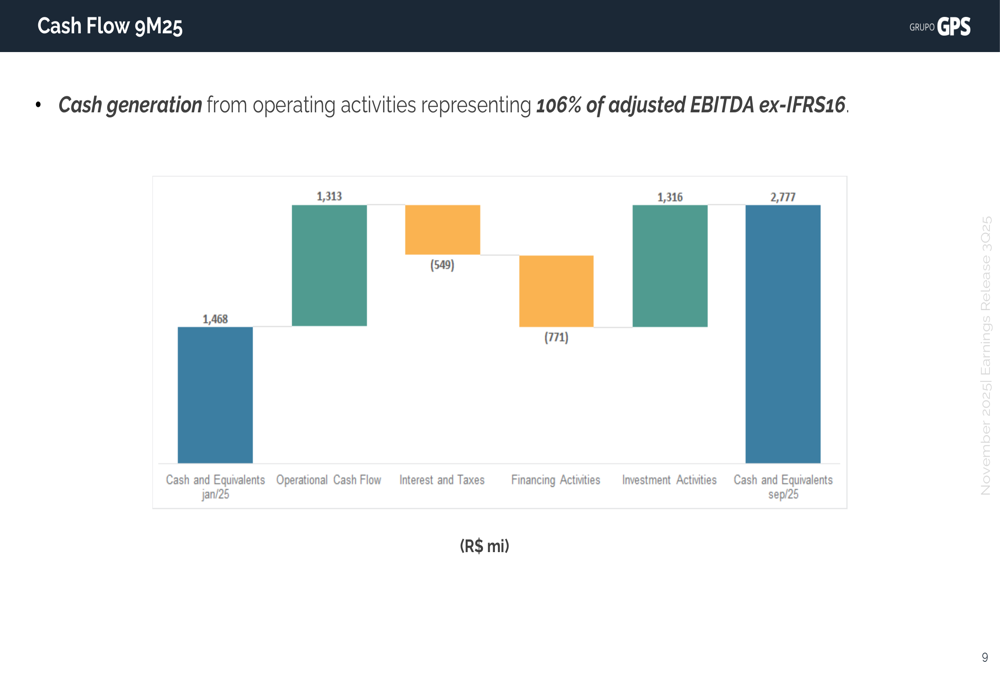

The company demonstrated robust cash generation, with operating cash flow of R$1,313 million for the first nine months of 2025, representing 106% of adjusted EBITDA. This strong cash conversion highlights the company’s operational efficiency and provides resources for its ongoing acquisition strategy.

The cash flow breakdown for the nine-month period is illustrated here:

GPS Participacoes has also improved its financial position, with the net debt to adjusted EBITDA ratio decreasing to 1.5x at the end of Q3 2025, down 0.3 percentage points compared to Q3 2024. The company’s loan portfolio has a duration of 32 months, providing financial stability for future growth initiatives.

Strategic Initiatives & M&A Activity

The company’s acquisition strategy remains a key driver of growth. In 2024, GPS Participacoes acquired companies with a combined gross revenue of R$4.2 billion, while in 2025 so far, it has added companies with gross revenue of R$412 million.

Since its IPO, the company has acquired 26 companies representing R$8.5 billion in gross revenue. These acquisitions span multiple sectors, including facilities and security (8 companies), temporary labor and field marketing (5), maintenance and industrial services (8), logistics (2), and catering (3).

The following chart provides a comprehensive overview of the company’s key performance indicators:

Forward-Looking Statements

According to the earnings call transcript, GPS Participacoes expects organic growth of 8-10% annually and aims to stabilize margins at 10% by early 2026. The company’s M&A pipeline includes approximately 10 companies with a combined revenue of R$2 billion, focusing primarily on security, cleaning, and catering sectors.

Management acknowledged the challenges in achieving their target 10% EBITDA margin but emphasized it as a priority. As executive Maria Bernhoeft stated during the earnings call, "We hope that all of this will take place throughout the year 2026, with 10% that we have had historically in revenue and an upside in margin somewhat beyond the 10%."

While GPS Participacoes continues to demonstrate strong revenue growth and cash generation, investors will be watching closely to see if the company can successfully address margin pressure while integrating its numerous acquisitions. The slight decline in EBITDA and net margins, despite revenue growth, suggests that balancing expansion with profitability remains a key challenge for the company moving forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.