Figma Shares Indicated To Open $105/$110

The Cheesecake Factory Incorporated (NASDAQ:CAKE) presented its Q1 2025 results and strategic outlook in an investor presentation on April 30, 2025, highlighting solid revenue growth, margin expansion, and ambitious expansion plans across its restaurant portfolio.

Executive Summary

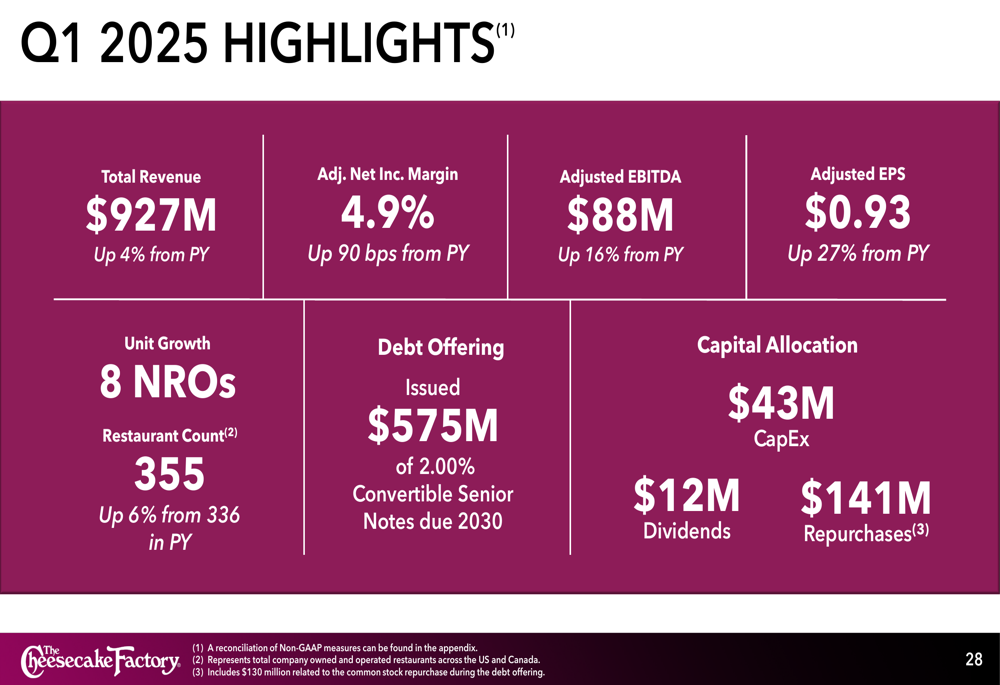

The company reported Q1 2025 total revenue of $927 million, up 4% year-over-year, with adjusted net income margin improving 90 basis points to 4.9%. Adjusted EBITDA increased 16% to $88 million, while adjusted earnings per share jumped 27% to $0.93. The restaurant operator plans to accelerate unit growth with as many as 25 new restaurants in 2025, having already opened 11 locations year-to-date.

As shown in the following financial highlights from Q1 2025:

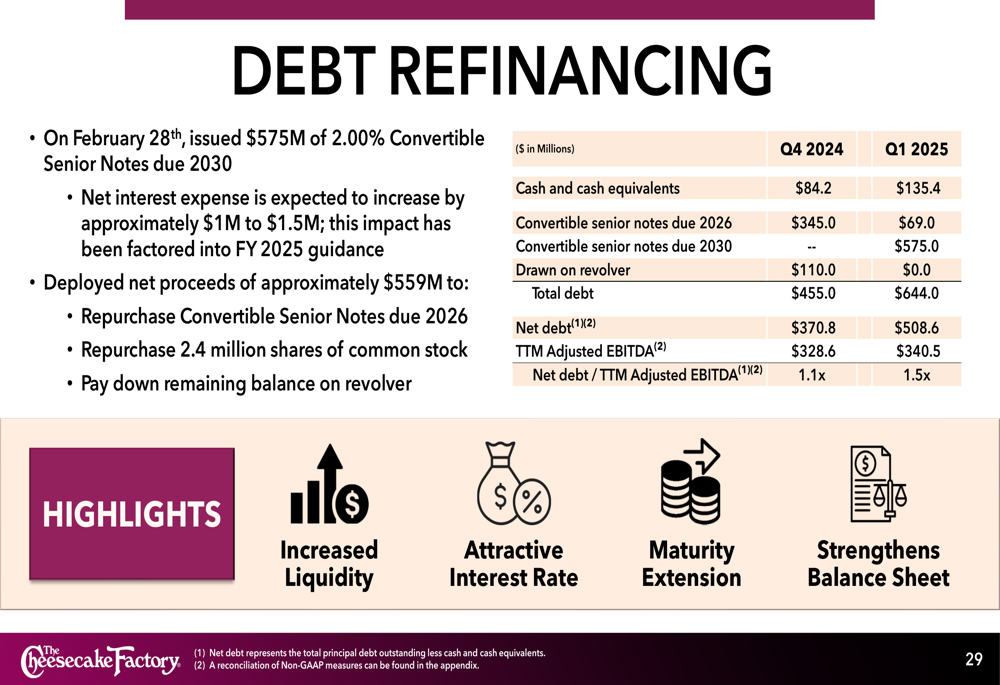

The company also completed a significant debt refinancing in Q1, issuing $575 million in convertible senior notes due 2030, which strengthened its balance sheet and increased liquidity.

Competitive Industry Position

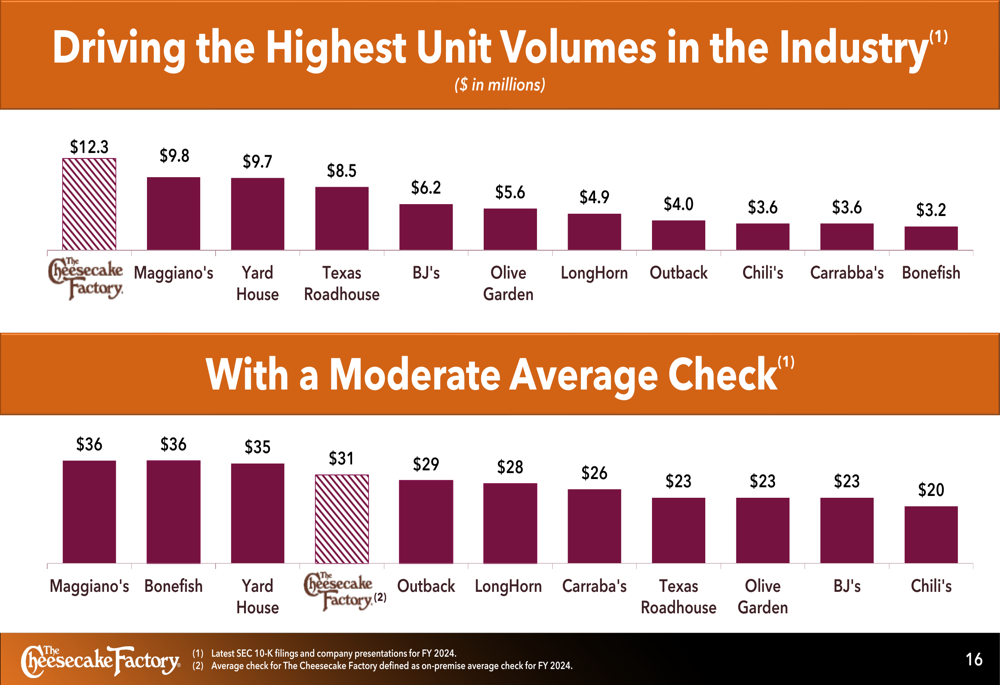

The Cheesecake Factory maintains its position as a leader in the casual dining segment with industry-leading average unit volumes of $12.3 million, significantly outpacing competitors like Maggiano’s ($9.8 million) and Yard House ($9.7 million). The company’s average check of $31 positions it in the upper-middle tier of casual dining chains.

The following chart illustrates The Cheesecake Factory’s industry-leading unit economics:

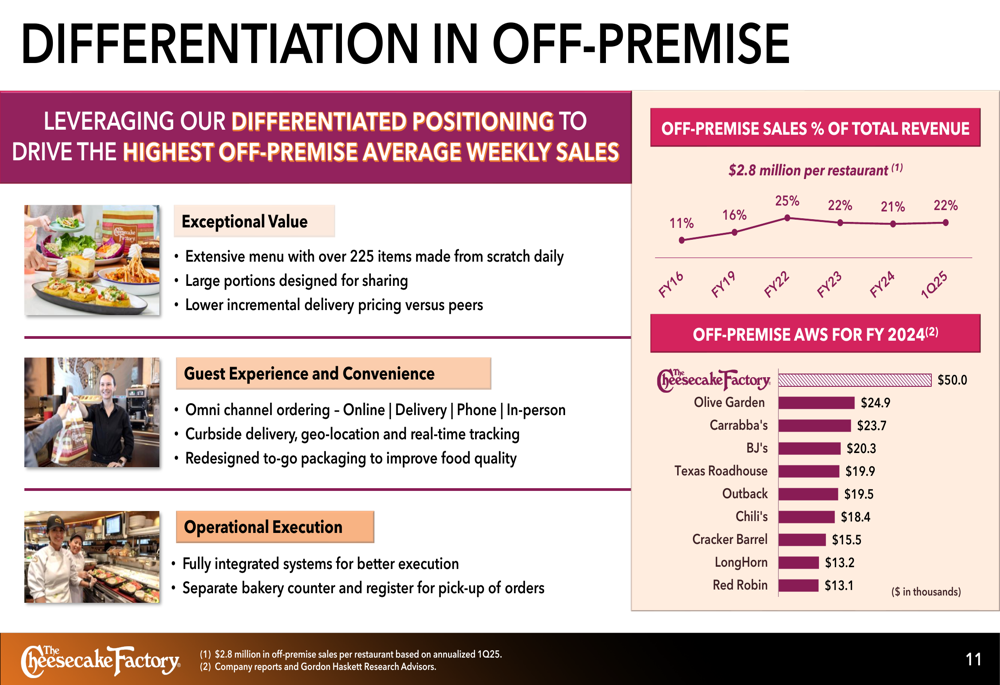

The company has also established a strong position in off-premise dining, with this channel growing from 11% of total revenue in FY16 to 22% in Q1 2025. The Cheesecake Factory’s off-premise average weekly sales of $50,000 substantially exceed competitors like Olive Garden ($24,900) and other casual dining chains.

As demonstrated in this comparative analysis of off-premise sales performance:

The company attributes its strong brand position to several factors, including its extensive menu, high-quality food preparation, and distinctive dessert offerings. Dessert sales represented 17% of total sales in FY 2024, up from 16% in FY 2019, supported by the company’s two bakery production facilities that produce 57 varieties of cheesecakes and desserts.

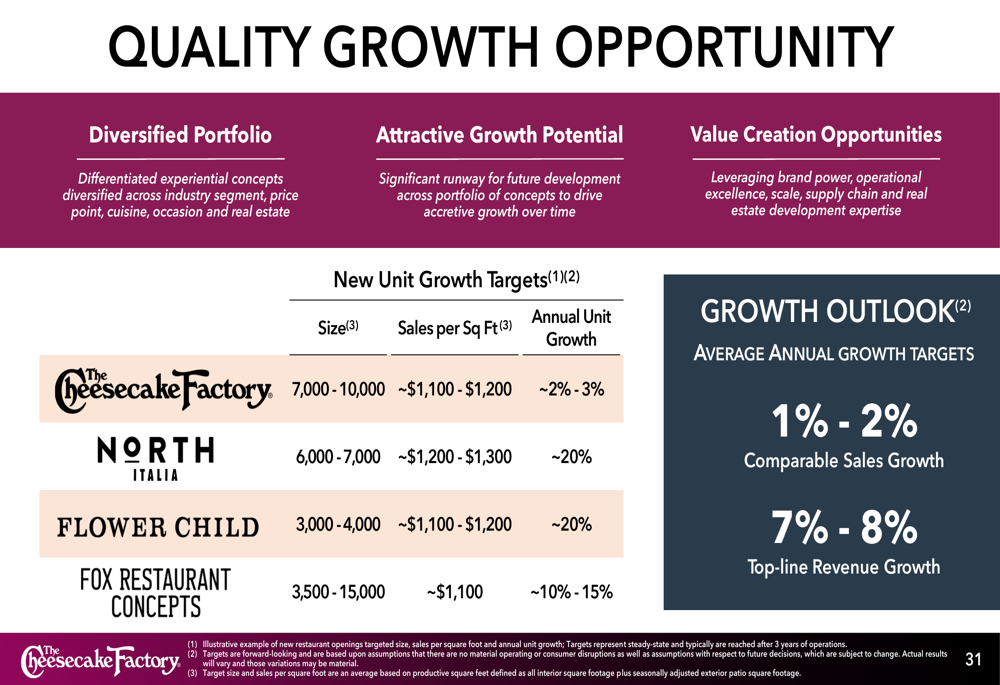

Strategic Growth Initiatives

The Cheesecake Factory is pursuing a multi-brand growth strategy, with plans to expand all concepts in its portfolio. The company currently operates 358 restaurants across the U.S. and Canada, including 215 Cheesecake Factory locations, 45 North Italia restaurants, 40 Flower Child locations, and 51 Fox Restaurant Concepts establishments. Additionally, the company has 33 international Cheesecake Factory locations through licensing agreements.

The company’s growth strategy is illustrated in this portfolio overview:

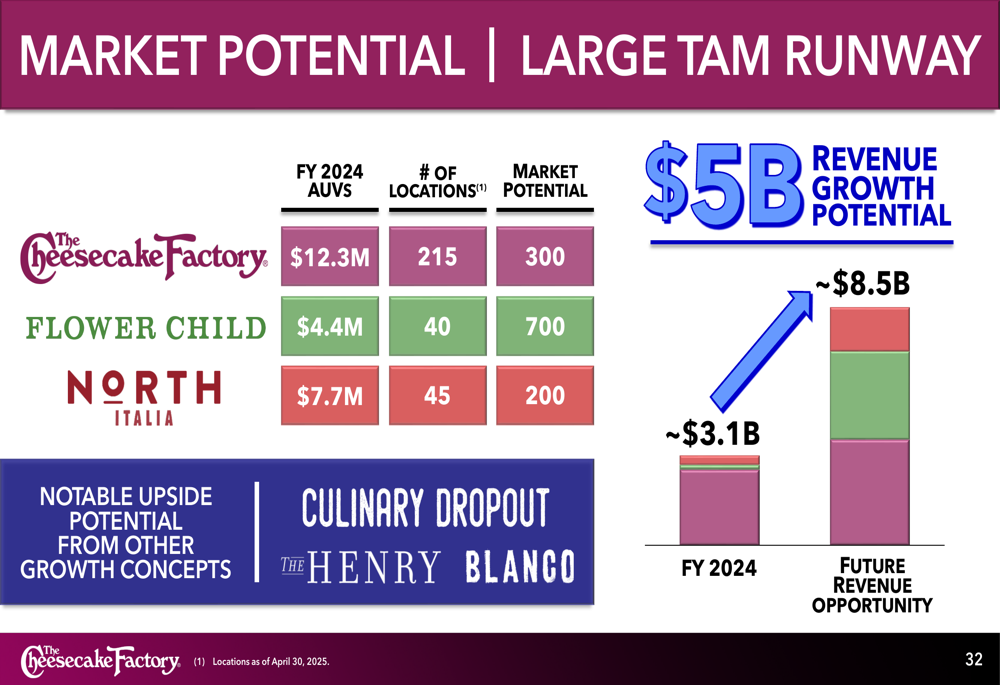

For The Cheesecake Factory brand, management sees potential for 300 domestic locations, compared to the current 215. North Italia, which targets the contemporary Italian dining segment, has potential for 200 domestic locations (currently at 45), while the health-focused fast-casual concept Flower Child could grow to as many as 700 locations from its current 40.

The market potential and growth runway are highlighted in this analysis:

The company has been steadily accelerating its new restaurant openings, from 13 in 2022 to 16 in 2023 and 23 in 2024. For 2025, the company plans to open as many as 25 new units, targeting approximately 20% annual unit growth for both North Italia and Flower Child.

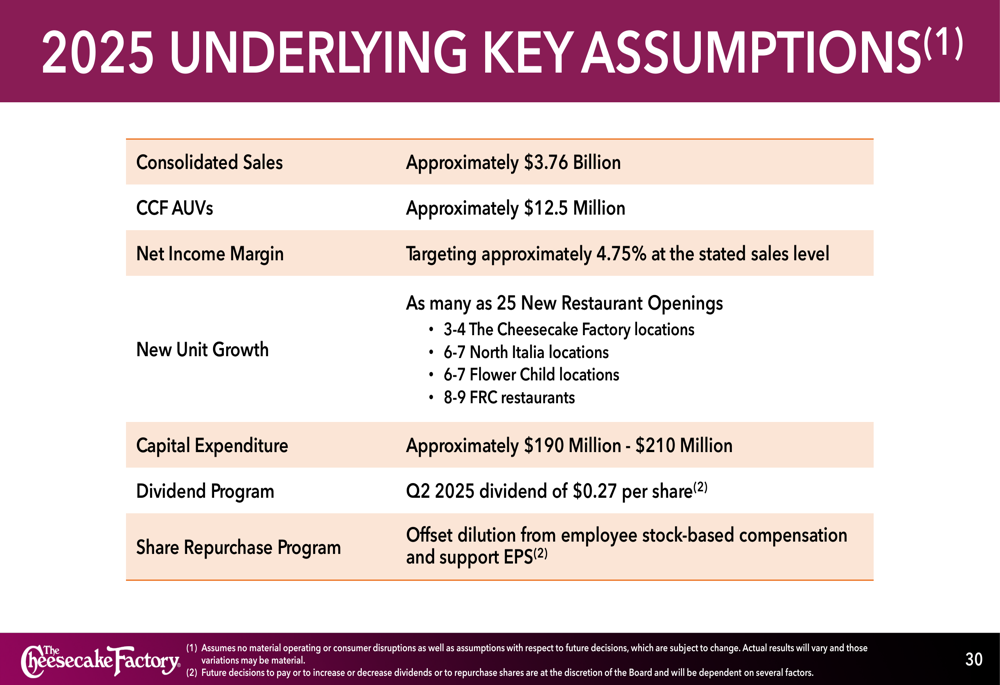

Forward-Looking Statements

For fiscal year 2025, The Cheesecake Factory projects consolidated sales of approximately $3.76 billion, with Cheesecake Factory average unit volumes of approximately $12.5 million. The company is targeting a net income margin of approximately 4.75% at the stated sales level.

The company’s 2025 outlook is summarized in these key assumptions:

Long-term, the company aims to achieve annual comparable sales growth of 1-2% and top-line revenue growth of 7-8%, driven by both new unit development and same-store sales increases. Management expects The Cheesecake Factory brand to grow units at 2-3% annually, while North Italia and Flower Child are targeted for approximately 20% annual unit growth each.

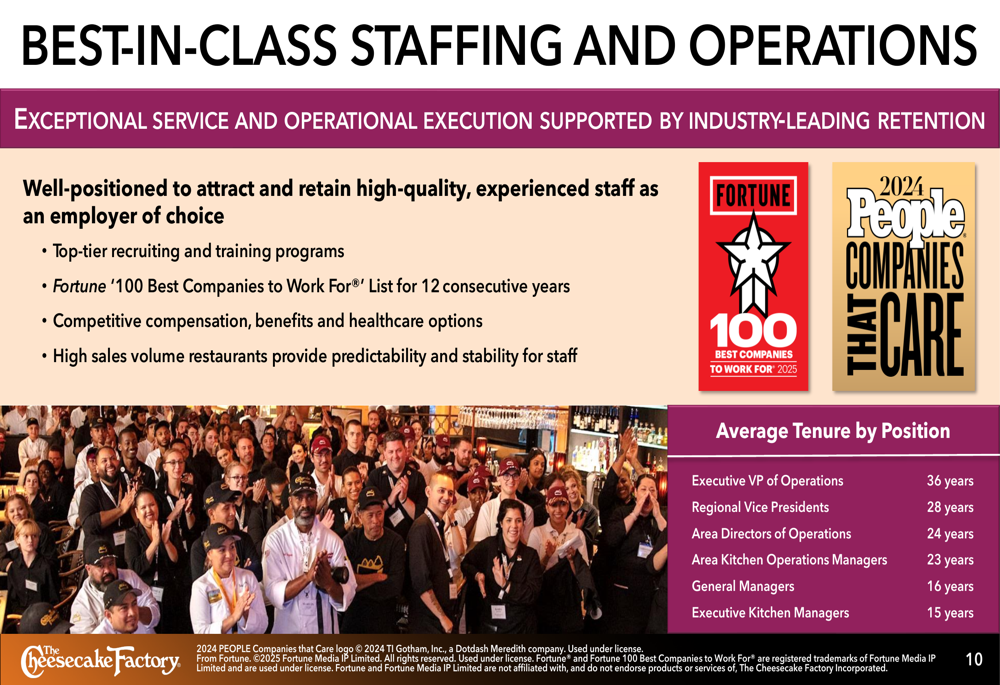

Operational Excellence

The Cheesecake Factory attributes much of its success to operational excellence and strong employee retention. The company has been named to Fortune’s "100 Best Companies to Work For" list for 12 consecutive years. Management highlighted impressive tenure statistics, with Executive VPs of Operations averaging 36 years with the company and General Managers averaging 16 years.

The following slide illustrates the company’s industry-leading staff retention:

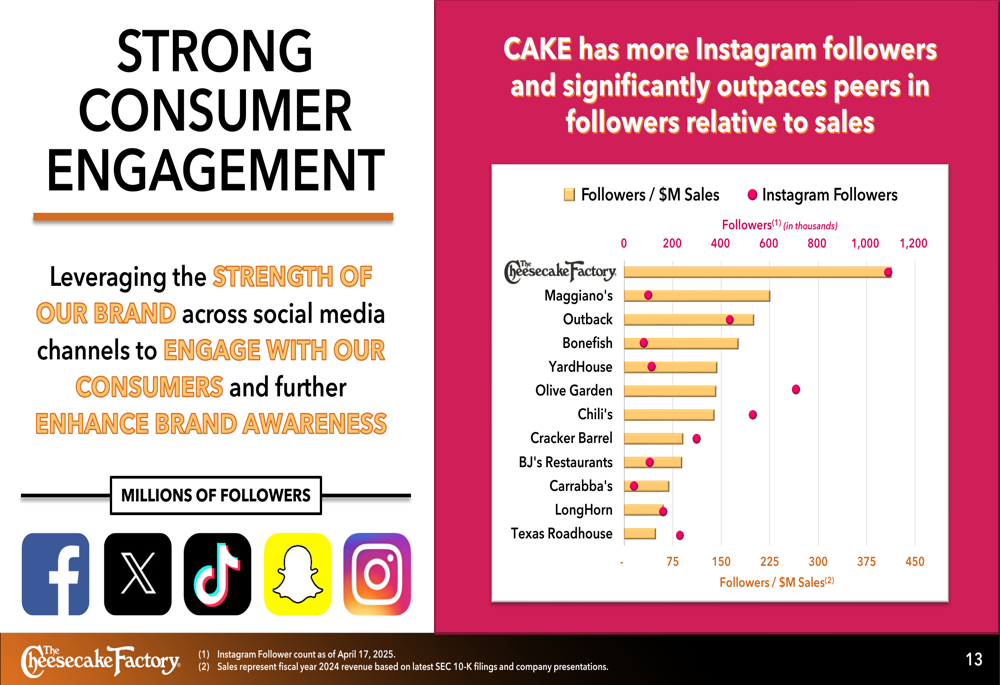

The company has also built strong consumer engagement through social media, with over 1.2 million Instagram followers. According to the presentation, The Cheesecake Factory outpaces its peer group in social media followers per million dollars of sales, helping to enhance brand awareness and drive customer engagement.

The Cheesecake Factory’s investor presentation demonstrates the company’s strong competitive position in the casual dining segment, supported by industry-leading unit economics, operational excellence, and a diversified growth strategy. With accelerating unit development across multiple concepts and solid financial performance, management appears confident in the company’s ability to deliver long-term growth and shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.