Dollar rebounds despite Fed independence worries; euro slips

Introduction & Market Context

The Chefs’ Warehouse (NASDAQ:CHEF) presented its second quarter 2025 earnings results on July 30, showing continued momentum following its strong first quarter performance. The specialty food distributor’s stock rose 2.99% in premarket trading to $63.40, reflecting positive investor sentiment toward the company’s financial results and operational improvements.

The company’s Q2 performance builds on its Q1 2025 results, which had already exceeded Wall Street expectations with EPS of $0.25 versus a forecasted $0.20. The latest presentation demonstrates CHEF’s ability to maintain growth momentum while improving operational efficiency and strengthening its balance sheet.

Quarterly Performance Highlights

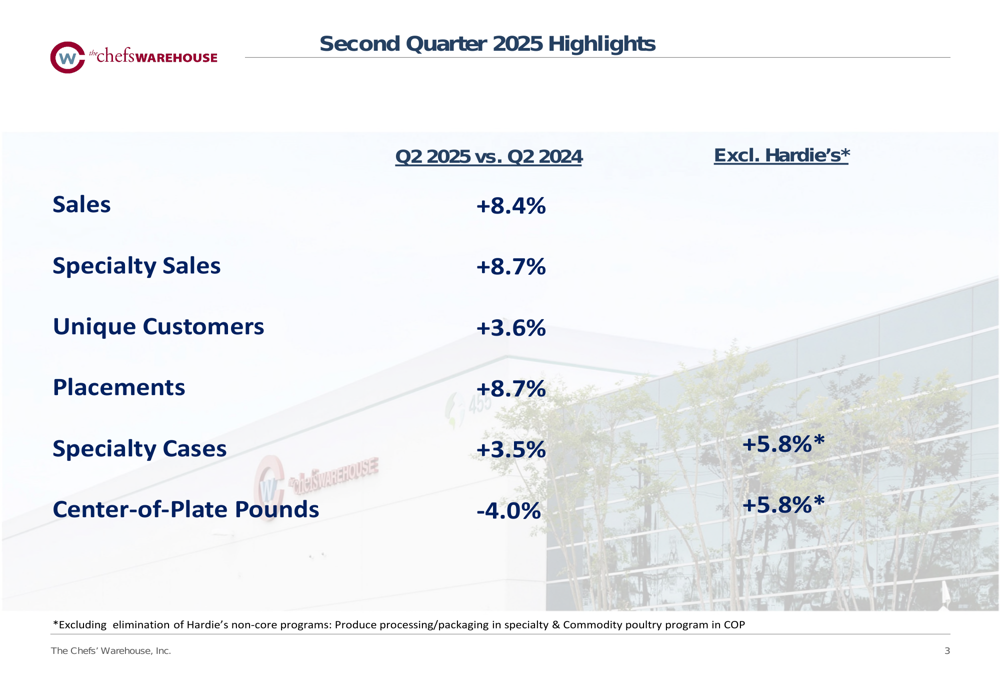

Chefs’ Warehouse reported solid growth across key metrics for the second quarter of 2025 compared to the same period in 2024. Net sales increased by 8.4%, driven primarily by an 8.7% rise in specialty sales. The company also expanded its customer base, with unique customers growing by 3.6% and placements up by 8.7%.

As shown in the following summary of Q2 2025 performance metrics:

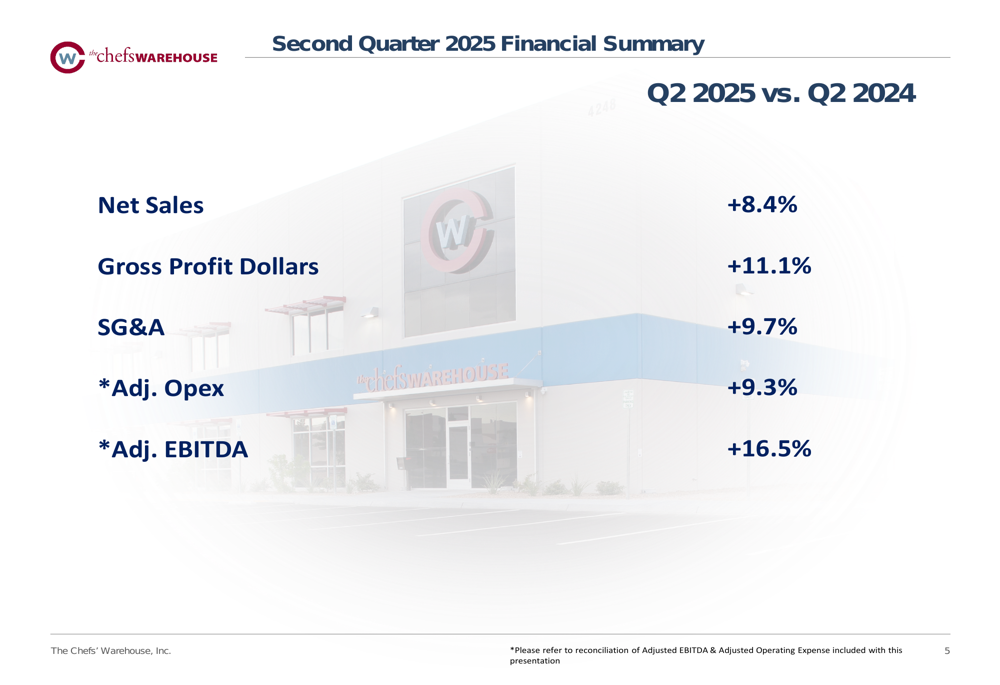

Gross profit dollars increased by 11.1%, outpacing sales growth and indicating improved margins. This translated to a 16.5% increase in adjusted EBITDA, reflecting the company’s ability to grow profitably while managing expenses. SG&A expenses increased by 9.7%, while adjusted operating expenses rose by 9.3%.

The financial summary below highlights these key metrics:

Operational Efficiency Improvements

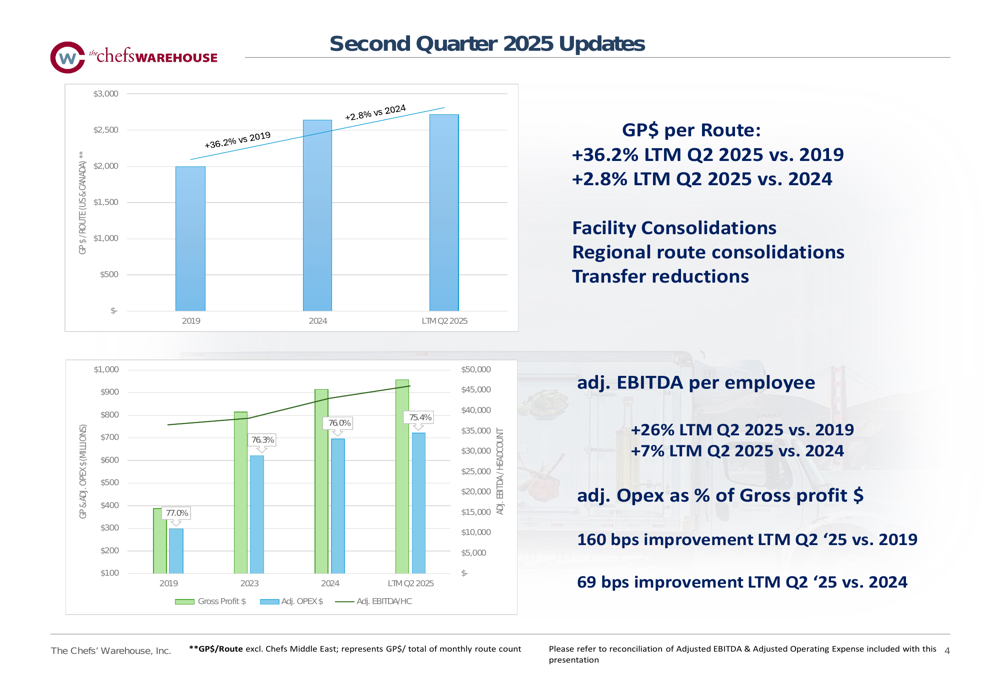

A significant driver of Chefs’ Warehouse’s improved profitability has been its focus on operational efficiency. The company has made notable progress in optimizing its distribution network and improving productivity metrics.

Gross profit dollars per route have increased by 36.2% compared to 2019 and by 2.8% compared to 2024. Similarly, adjusted EBITDA per employee has grown by 26% versus 2019 and 7% versus 2024. These improvements have been achieved through facility consolidations, regional route consolidations, and transfer reductions.

The following chart illustrates these operational efficiency gains:

These efficiency improvements have translated into better expense management, with adjusted operating expenses as a percentage of gross profit improving by 160 basis points compared to 2019 and 69 basis points compared to 2024.

Capital Allocation and Debt Reduction

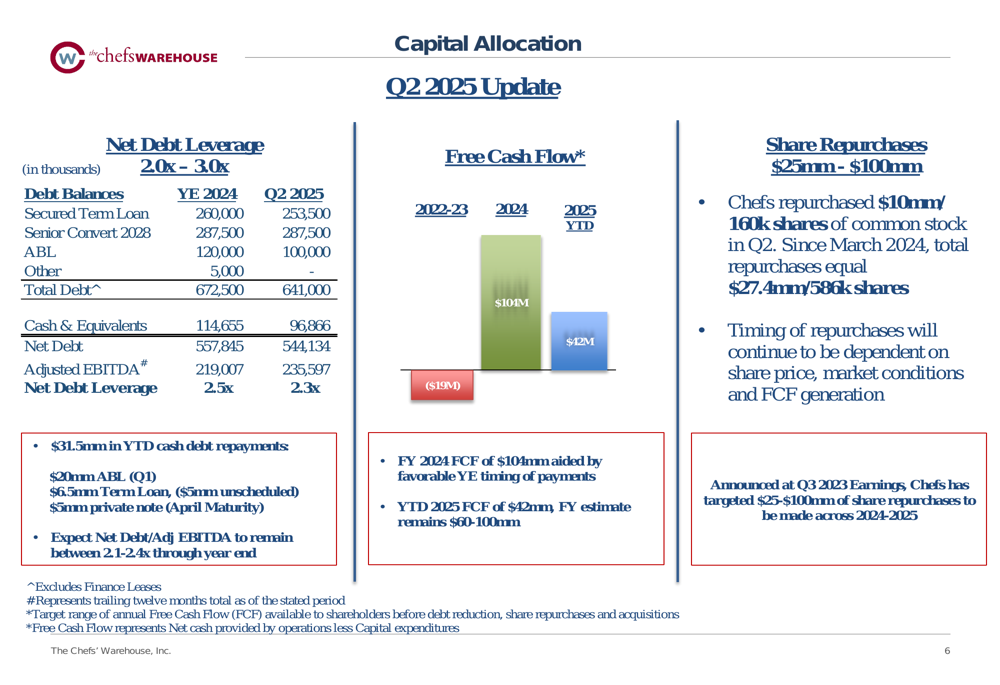

Chefs’ Warehouse has maintained a disciplined approach to capital allocation, focusing on debt reduction and shareholder returns. The company’s net debt leverage ratio improved from 2.5x at the end of 2024 to 2.3x in Q2 2025, moving toward the lower end of its target range of 2.0x to 3.0x.

During the second quarter, CHEF repurchased $10 million worth of common stock, representing approximately 160,000 shares. Since March 2024, the company has repurchased a total of $27.4 million worth of shares, or approximately 586,000 shares.

The company has also made significant progress in debt reduction, with $31.5 million in year-to-date cash debt repayments, including $20 million in ABL (asset-based lending) in Q1, $6.5 million in term loans ($5 million of which was unscheduled), and $5 million in private notes that matured in April.

Free cash flow generation has been strong, with $42 million generated year-to-date in 2025, following $104 million in 2024. Management expects full-year 2025 free cash flow to be between $60 million and $100 million.

The following chart details the company’s capital allocation strategy and debt reduction progress:

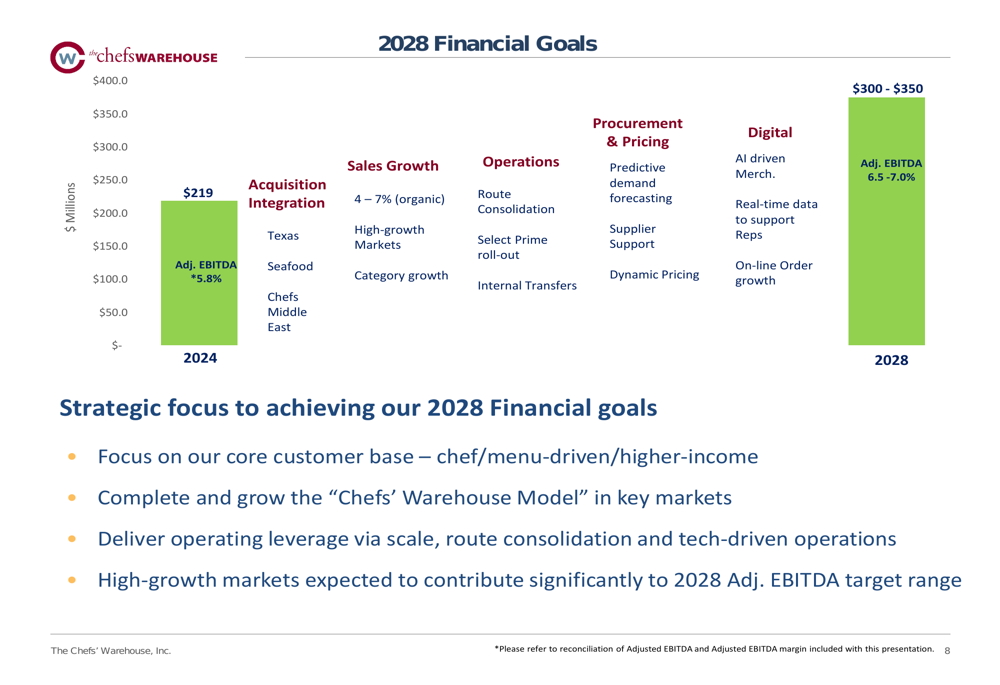

Long-term Financial Goals

Looking ahead, Chefs’ Warehouse has outlined ambitious financial goals for 2028, targeting adjusted EBITDA of $300-350 million with a margin of 6.5-7.0%. This represents significant growth from the 2024 adjusted EBITDA of $219 million with a 5.8% margin.

The company’s strategy to achieve these goals includes:

1. Organic sales growth of 4-7%, focusing on high-growth markets and category expansion

2. Integration of acquisitions, particularly in Texas, Seafood, and Chefs’ Middle East

3. Operational improvements through route consolidation, Select Prime roll-out, and internal transfers

4. Enhanced procurement and pricing strategies, including predictive demand forecasting and dynamic pricing

5. Digital transformation with AI-driven merchandising and real-time data to support representatives

The following slide illustrates the company’s 2028 financial goals and growth strategy:

Conclusion

Chefs’ Warehouse’s Q2 2025 presentation demonstrates the company’s ability to deliver strong financial results while improving operational efficiency and strengthening its balance sheet. The 8.4% sales growth and 16.5% increase in adjusted EBITDA reflect the success of its strategic initiatives.

The company’s focus on operational efficiency, as evidenced by improvements in gross profit per route and adjusted EBITDA per employee, has contributed to margin expansion. Meanwhile, its disciplined approach to capital allocation, including debt reduction and share repurchases, has strengthened its financial position.

With a clear strategy for achieving its 2028 financial goals, Chefs’ Warehouse appears well-positioned for continued growth and profitability. The positive premarket stock movement suggests that investors share this optimistic outlook for the specialty food distributor’s future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.