September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Chegg Inc . (NYSE:CHGG) released its Q1 2025 investor presentation on May 12, 2025, revealing a company in transition as it battles significant subscriber losses while implementing strategic initiatives to stabilize its business. Despite beating its own revenue and adjusted EBITDA guidance, Chegg continues to face substantial year-over-year declines across key metrics.

The education technology company’s stock has struggled significantly, trading at just $0.69 as of May 9, 2025, down 4.15% for the day and near its 52-week low of $0.44. With a current market capitalization well below $200 million, Chegg is working to reposition itself in a challenging competitive landscape dominated by generative AI alternatives.

Quarterly Performance Highlights

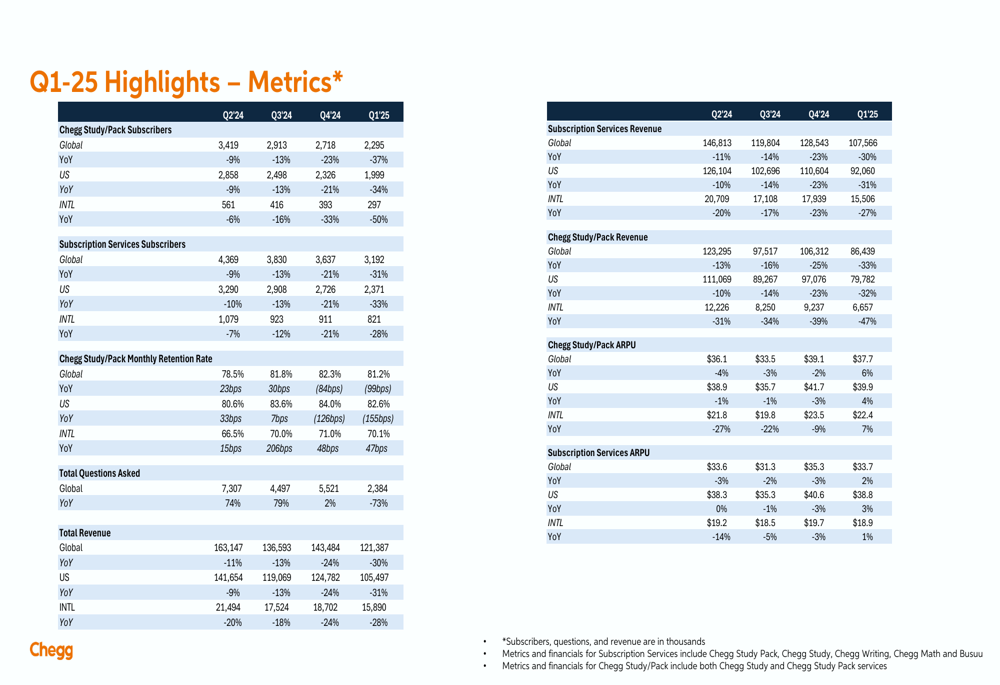

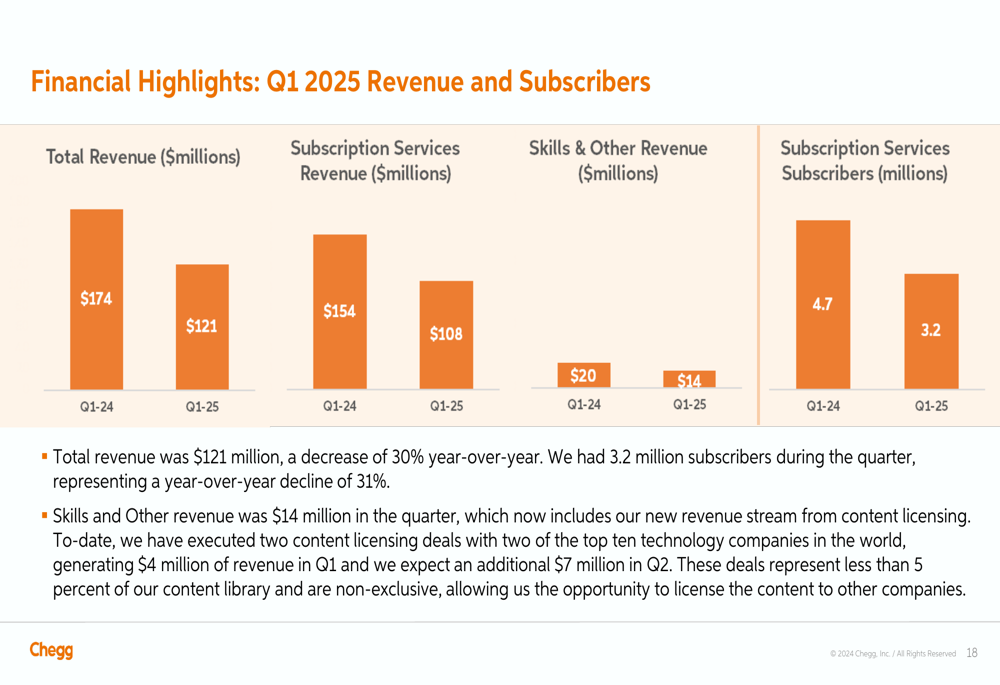

Chegg reported Q1 2025 total revenue of $121.4 million, surpassing previous guidance but still representing a 30% year-over-year decline. The company’s subscriber base continued its downward trajectory, with global Chegg Study/Pack subscribers falling 37% year-over-year to 2.3 million.

As shown in the following detailed metrics table:

Despite the subscriber decline, Chegg maintained relatively stable average revenue per user (ARPU), with Subscription Services ARPU actually increasing 2% year-over-year to $33.7. The company generated approximately $16 million in free cash flow during the quarter, demonstrating continued operational efficiency despite revenue challenges.

The financial performance is further illustrated in this revenue and subscriber chart:

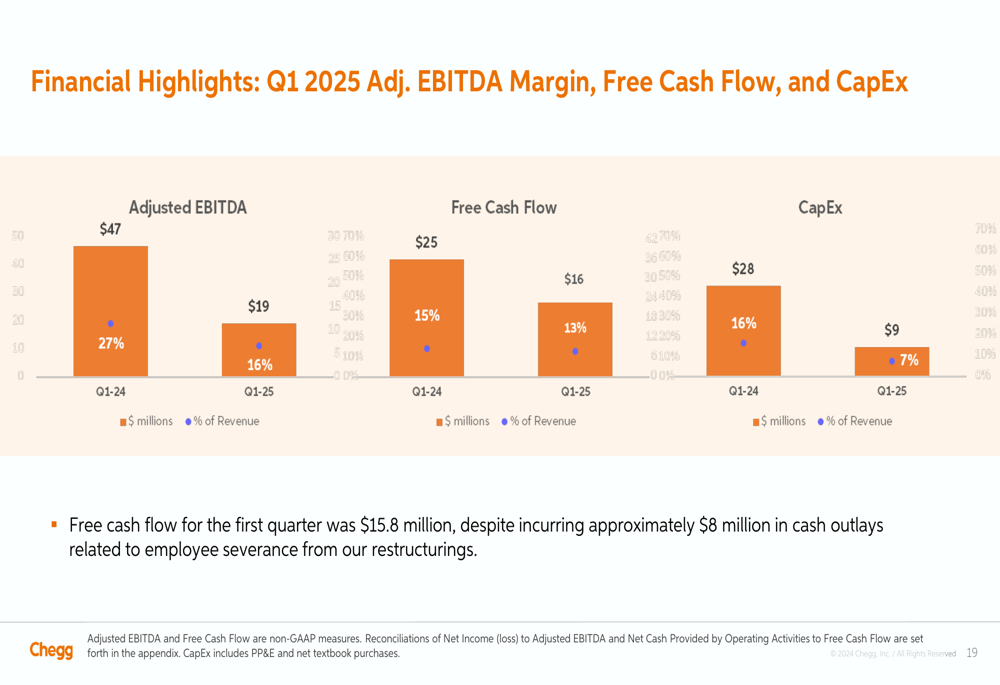

Adjusted EBITDA came in at $19.3 million for Q1 2025, down from $46.7 million in the prior year period but exceeding guidance. Free cash flow remained positive at $15.9 million, despite incurring approximately $8 million in cash outlays related to employee severance.

Strategic Initiatives

Chegg is actively pursuing several strategic initiatives to combat subscriber losses and diversify revenue streams. The company has expanded its business-to-institution efforts from 5 pilots to 15 and secured content licensing deals with "two of the top ten technology companies in the world," generating $4 million in Q1 revenue with an additional $7 million expected in Q2.

The company is leveraging its AI capabilities to differentiate itself in the market, emphasizing its education-specific approach:

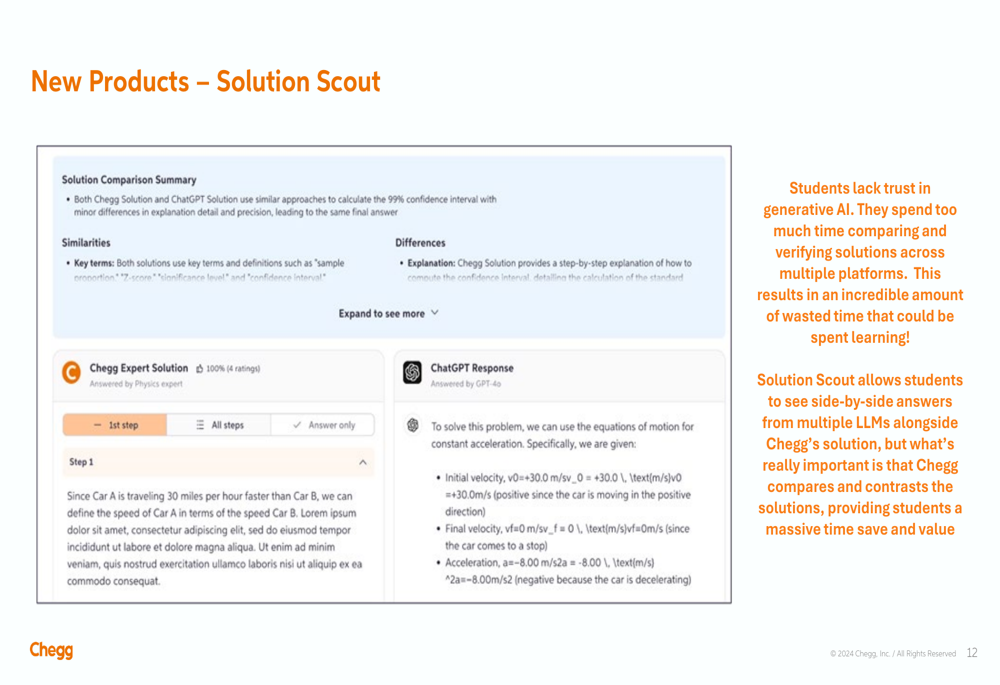

A key new product introduction is Solution Scout, which addresses student skepticism about generative AI by comparing solutions from different AI sources alongside Chegg’s expert solutions:

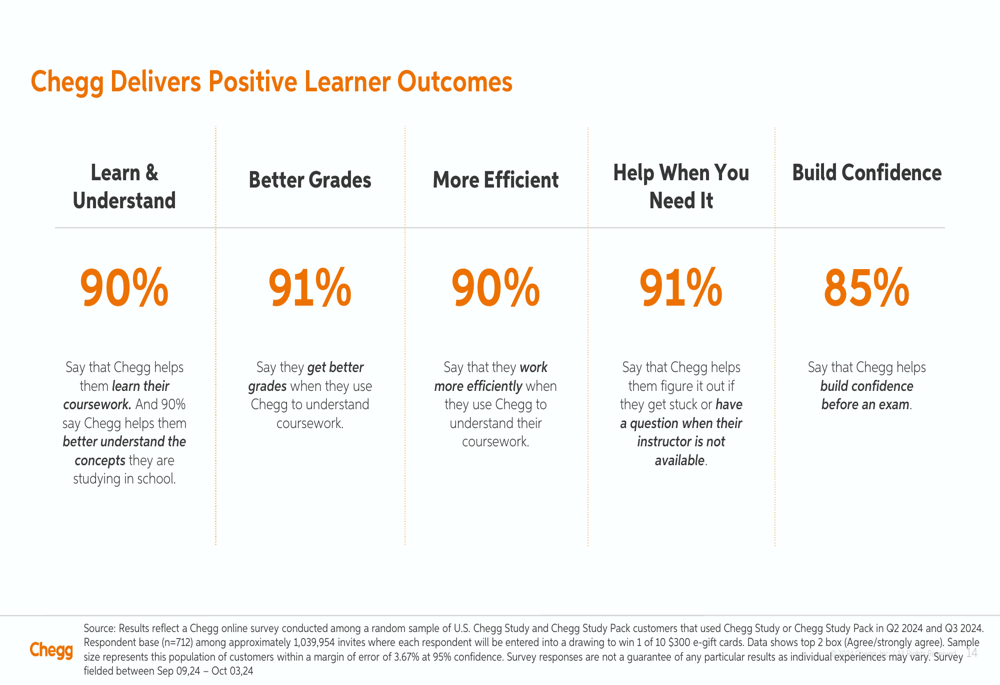

Chegg continues to highlight strong student satisfaction metrics, with over 90% of users reporting that the platform helps them learn coursework, achieve better grades, work more efficiently, and overcome learning obstacles:

Detailed Financial Analysis

The company’s financial position shows a mix of challenges and prudent management. Chegg ended Q1 with $126 million in cash and investments and a net cash balance of $64 million after opportunistically repurchasing $65.2 million in aggregate principal amount of its 2026 convertible notes.

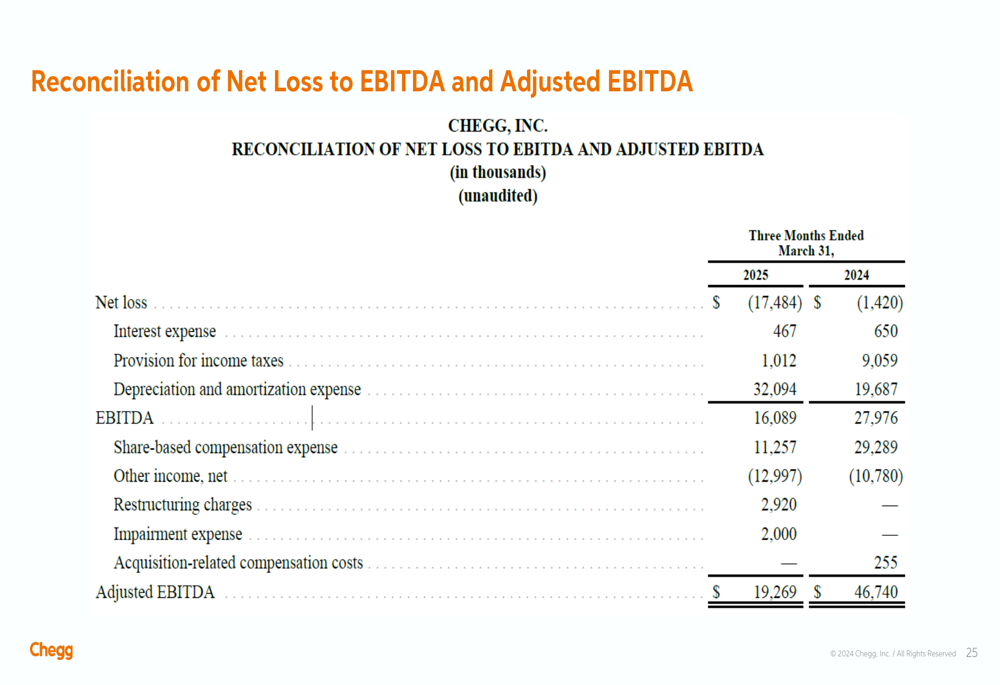

A detailed reconciliation of net loss to adjusted EBITDA reveals the underlying financial performance:

Capital expenditures for the quarter were $9 million, down 69% year-over-year, reflecting the company’s more disciplined approach to investments while maintaining its content development capabilities.

Forward-Looking Statements

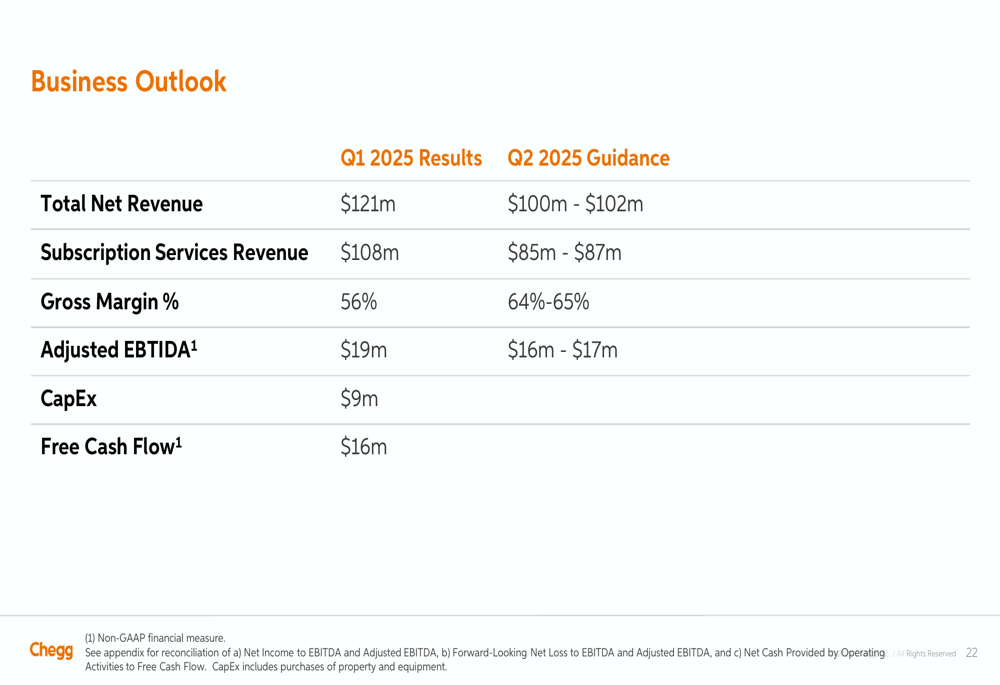

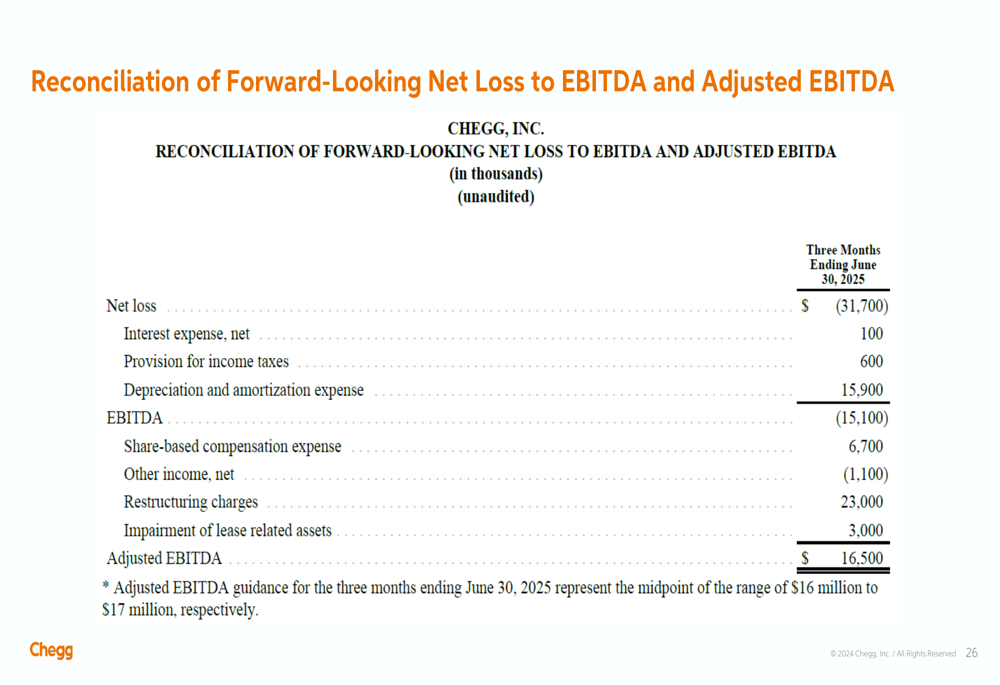

For Q2 2025, Chegg provided guidance of $100-102 million in total revenue and $16-17 million in adjusted EBITDA, indicating continued year-over-year declines but sequential stabilization:

The company is implementing significant cost-saving measures, which are expected to generate $45-55 million in savings during 2025 and $100-110 million in 2026. These initiatives aim to align costs with the company’s business outlook while maintaining investment in strategic growth areas.

The forward-looking adjusted EBITDA guidance is further detailed in this reconciliation:

Chegg’s management also noted "significant progress" on its strategic alternatives process, suggesting the company may be exploring various options including potential partnerships, asset sales, or other corporate transactions to enhance shareholder value.

While Chegg faces substantial challenges in reversing its subscriber decline, the company’s better-than-expected Q1 performance, positive cash flow, and strategic initiatives provide some optimism for potential stabilization. However, investors will likely remain cautious until more concrete evidence of a sustainable turnaround emerges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.