Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Chemours Company (NYSE:CC) released its first quarter 2025 earnings presentation on May 6, showing mixed financial results as the specialty chemicals manufacturer navigates challenging market conditions. The company’s stock fell 5.95% to $11.38 in after-hours trading following the announcement, reflecting investor concerns about ongoing financial pressures despite strategic growth initiatives.

The presentation revealed a 65% reduction in quarterly dividend to $0.0875 per share, a significant move aimed at strengthening the company’s balance sheet amid high debt levels. This comes as Chemours continues to emphasize its "Pathway to Thrive" strategy while targeting growth opportunities in emerging markets like data center liquid cooling.

Quarterly Performance Highlights

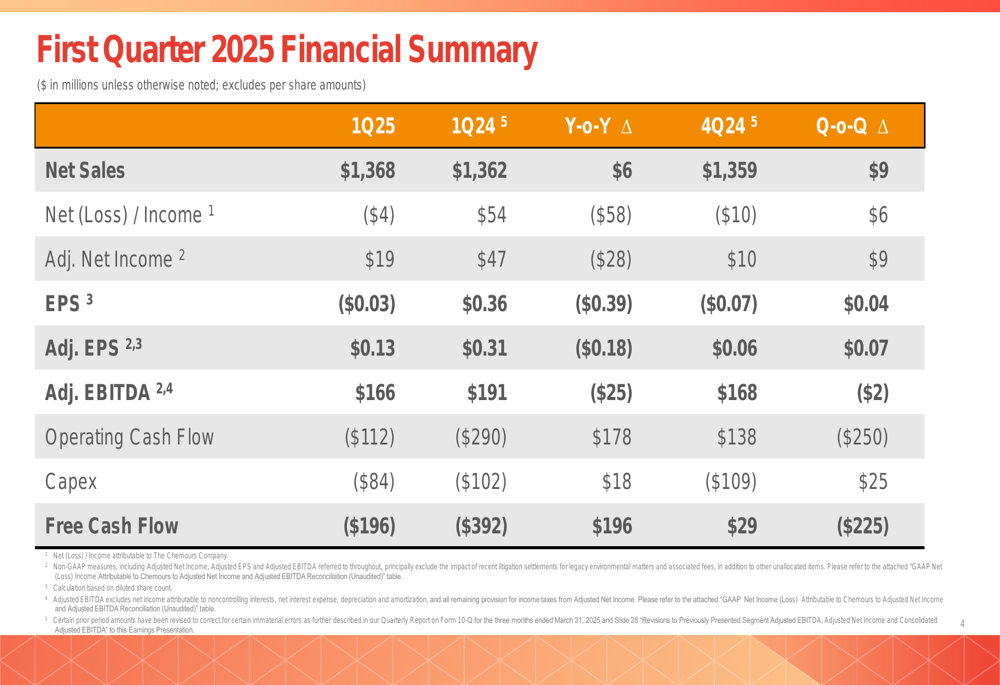

Chemours reported Q1 2025 net sales of $1.37 billion, essentially flat compared to $1.36 billion in Q1 2024. However, the company posted a net loss of $4 million (-$0.03 per share) compared to net income of $54 million ($0.36 per share) in the same period last year. Adjusted earnings per share came in at $0.13, down from $0.31 in Q1 2024.

As shown in the following comprehensive financial summary:

Adjusted EBITDA declined to $166 million from $191 million in Q1 2024, representing a 13% year-over-year decrease. The company’s cash position deteriorated with negative operating cash flow of $112 million and negative free cash flow of $196 million for the quarter.

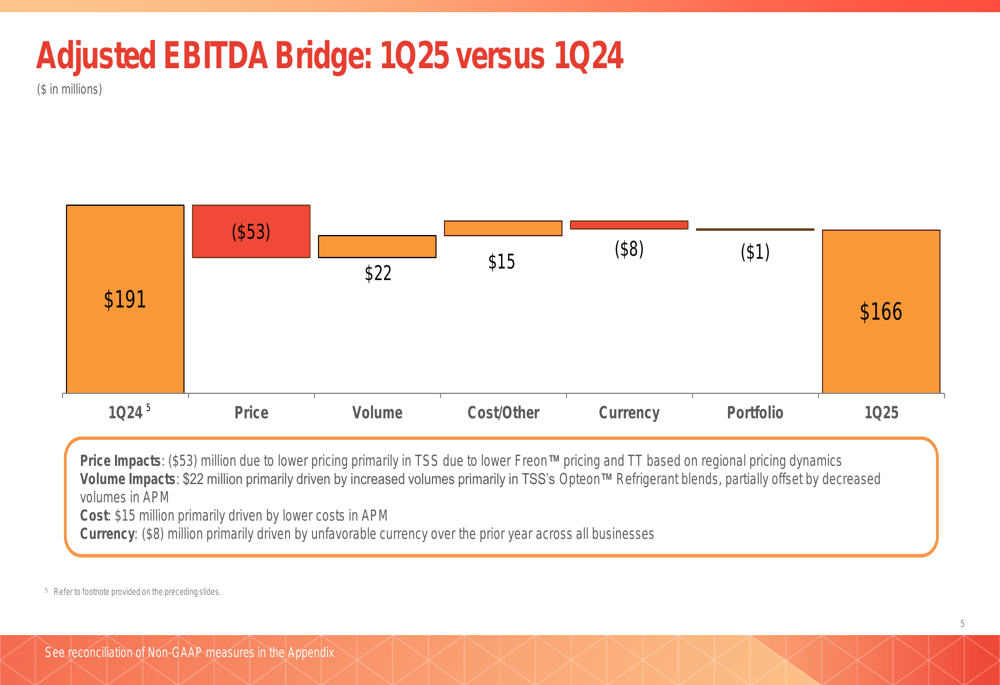

The following bridge analysis illustrates the key factors affecting the company’s EBITDA performance:

Price decreases had a significant negative impact of $53 million, primarily in the Thermal & Specialized Solutions (TSS) segment. This was partially offset by positive volume impacts of $22 million, driven by increased demand for Opteon™ Refrigerant blends, and cost improvements of $15 million. Currency effects created an $8 million headwind across all businesses.

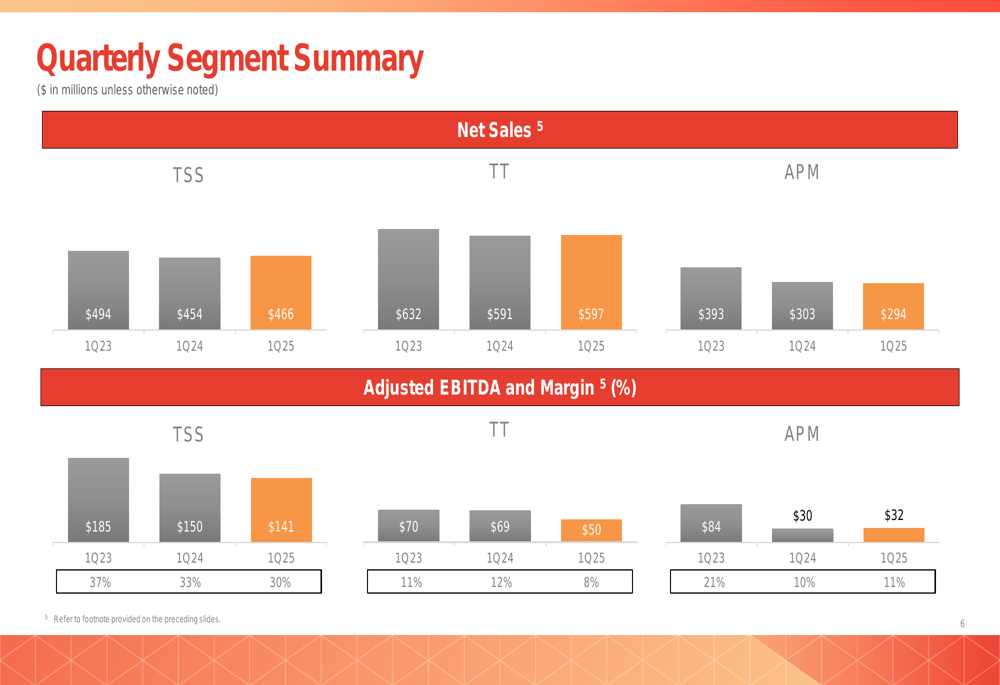

Segment performance varied considerably as shown in this quarterly comparison:

The TSS segment saw its adjusted EBITDA margin decline from 33% in Q1 2024 to 30% in Q1 2025, despite 40% year-over-year growth in Opteon™ Refrigerants sales. Titanium Technologies (TT) experienced a more significant margin compression, with adjusted EBITDA margin falling from 12% to 8%. The Advanced Performance Materials (APM) segment showed slight improvement, with margins increasing from 10% to 11%.

Financial Health & Challenges

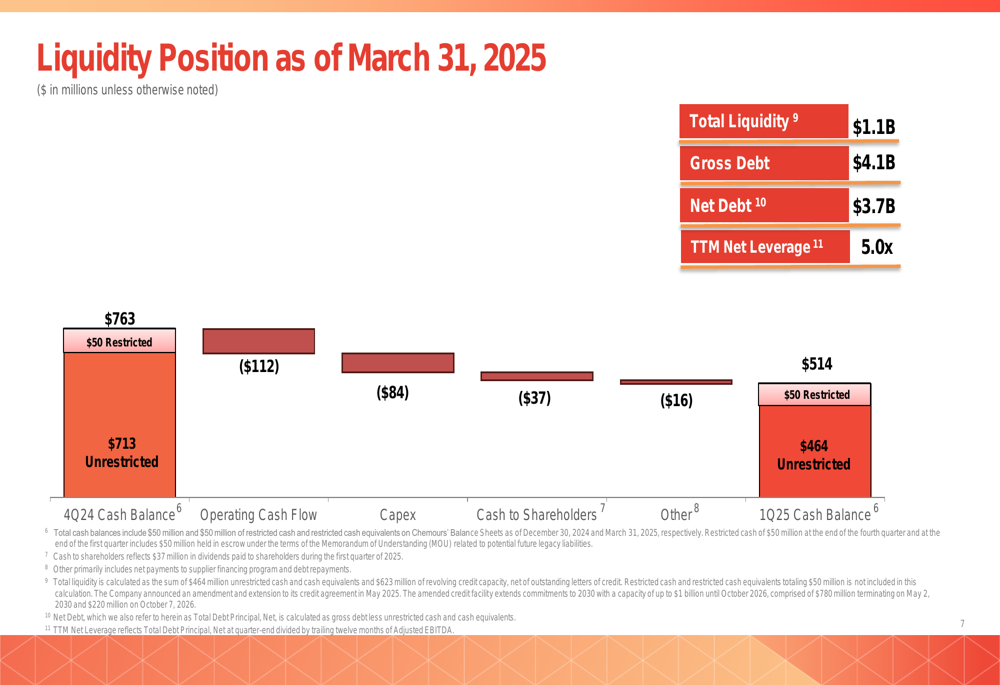

Chemours’ liquidity position and debt levels present ongoing challenges for the company:

As of March 31, 2025, Chemours reported total liquidity of $1.1 billion, with gross debt of $4.1 billion and net debt of $3.7 billion. The company’s trailing twelve-month net leverage ratio stands at 5.0x, indicating a significant debt burden that likely contributed to the decision to reduce the dividend.

The cash balance declined from $763 million at the end of Q4 2024 to $514 million at the end of Q1 2025, with $50 million restricted in both periods. This decline was driven by negative operating cash flow, capital expenditures, and shareholder returns.

The dividend reduction represents a strategic pivot to prioritize balance sheet improvement over shareholder returns in the near term. Management indicated this move would "enable balance sheet flexibility going forward," suggesting a focus on debt reduction and financial stability.

Strategic Initiatives

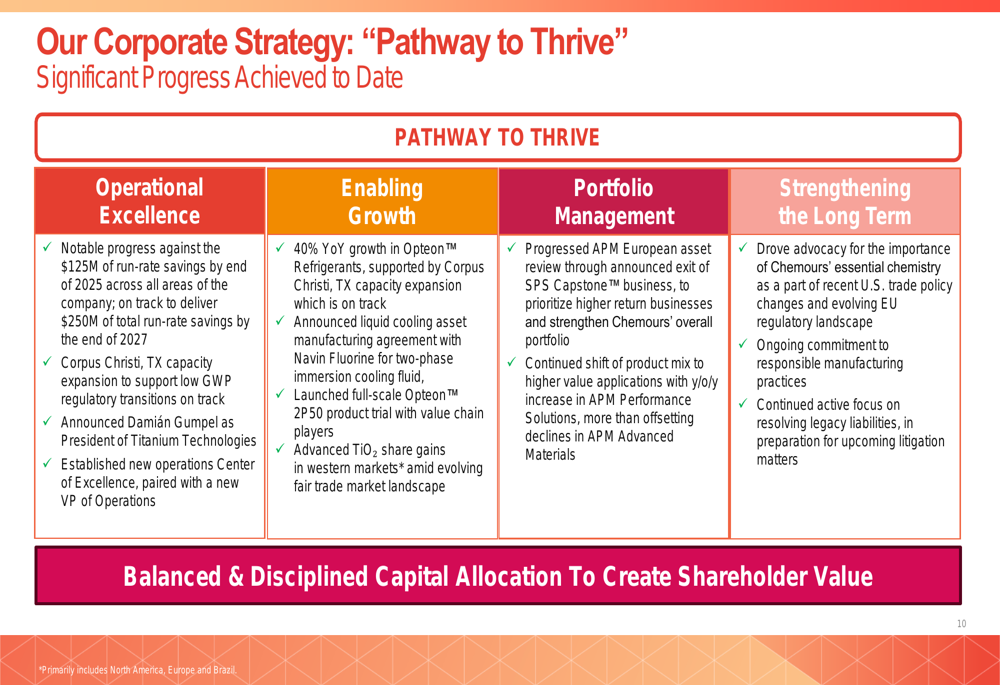

Despite current financial challenges, Chemours continues to emphasize its "Pathway to Thrive" strategy, which focuses on operational excellence, growth enablement, portfolio management, and long-term strengthening:

The company reported progress against its target of $125 million in run-rate savings by the end of 2025, part of a broader goal to achieve more than $250 million in cost reductions from 2024 to 2027. Other strategic initiatives include capacity expansion at the Corpus Christi, Texas facility and a new manufacturing agreement with Navin Fluorine for two-phase immersion cooling products.

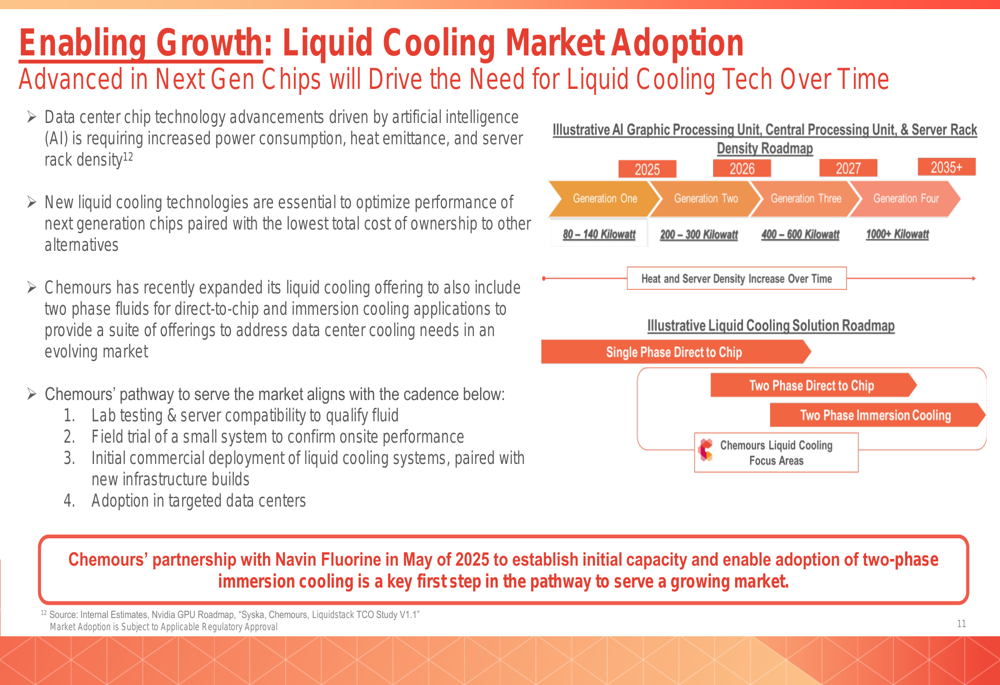

A key growth opportunity highlighted in the presentation is the expanding market for data center liquid cooling solutions, particularly for artificial intelligence applications:

Chemours is positioning itself to capitalize on the increasing power density requirements of AI processors, which are expected to grow from 80-140 kilowatts in 2025 to over 1,000 kilowatts beyond 2035. The company’s liquid cooling solutions include both single-phase direct-to-chip and two-phase technologies using its Opteon fluids.

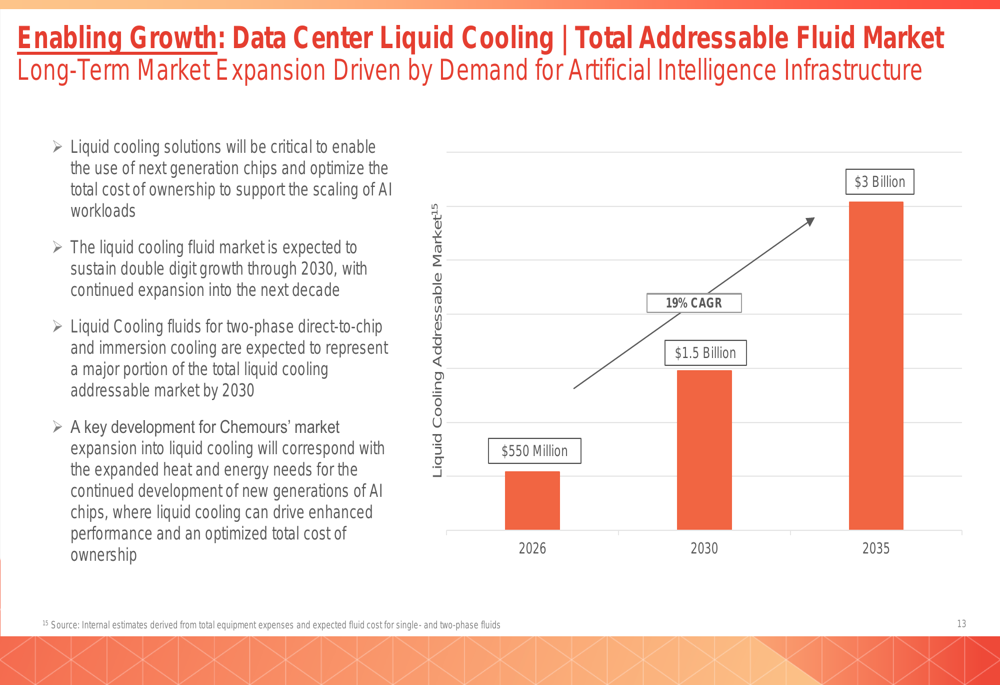

The total addressable market for these cooling solutions is projected to grow substantially in the coming years:

According to company estimates, the liquid cooling addressable market is expected to reach $550 million by 2026, growing to $1.5 billion by 2030 (representing a 19% CAGR) and $3 billion by 2035. This presents a significant growth opportunity for Chemours’ specialized fluids business.

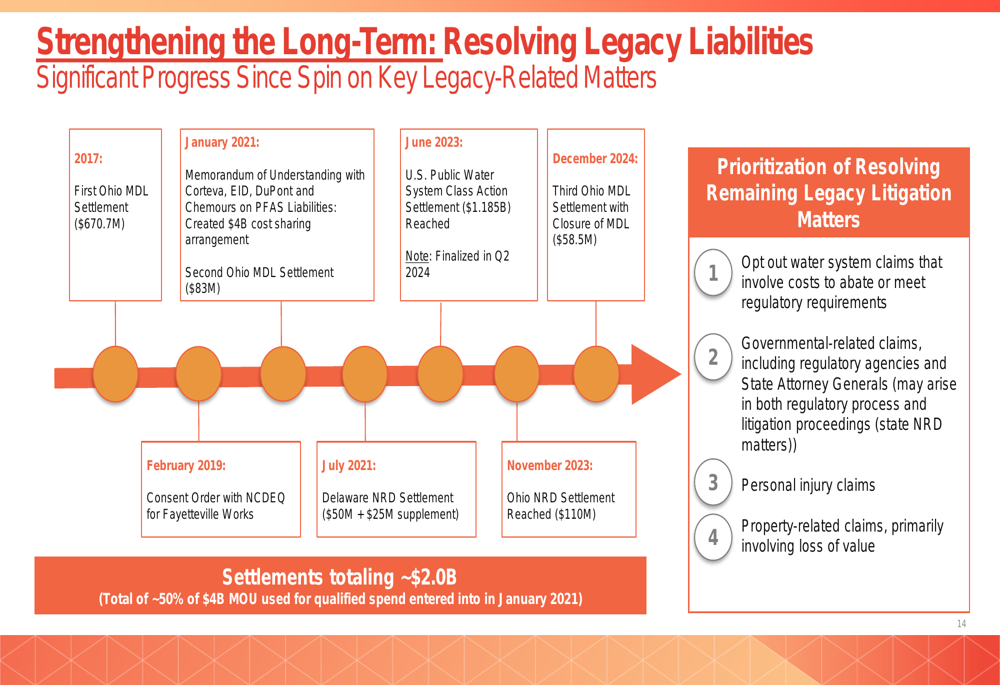

The company also highlighted progress in resolving legacy PFAS liabilities:

Since 2017, Chemours has reached settlements totaling approximately $2.0 billion related to PFAS contamination. The company noted that approximately 50% of the $4 billion memorandum of understanding established in January 2021 has been used for qualified spend.

Forward-Looking Statements

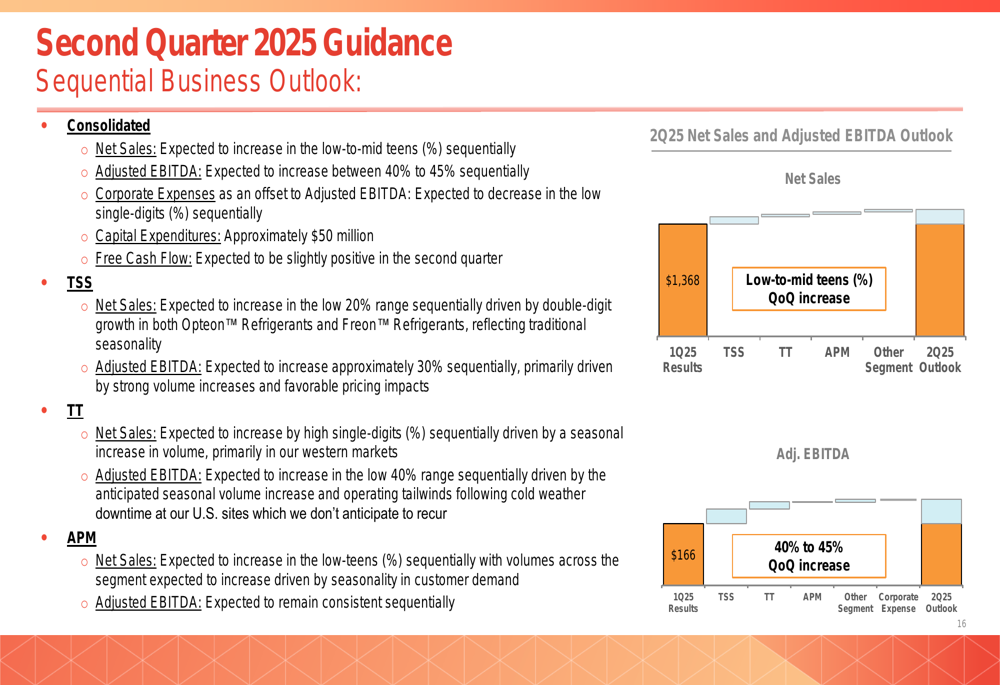

Looking ahead to Q2 2025, Chemours provided the following guidance:

The company expects sequential improvement across all segments, with consolidated net sales projected to increase in the low-to-mid teens percentage range and adjusted EBITDA anticipated to grow 40-45% compared to Q1 2025. The TSS segment is expected to lead this improvement with net sales growth in the low 20% range and adjusted EBITDA growth of approximately 30%.

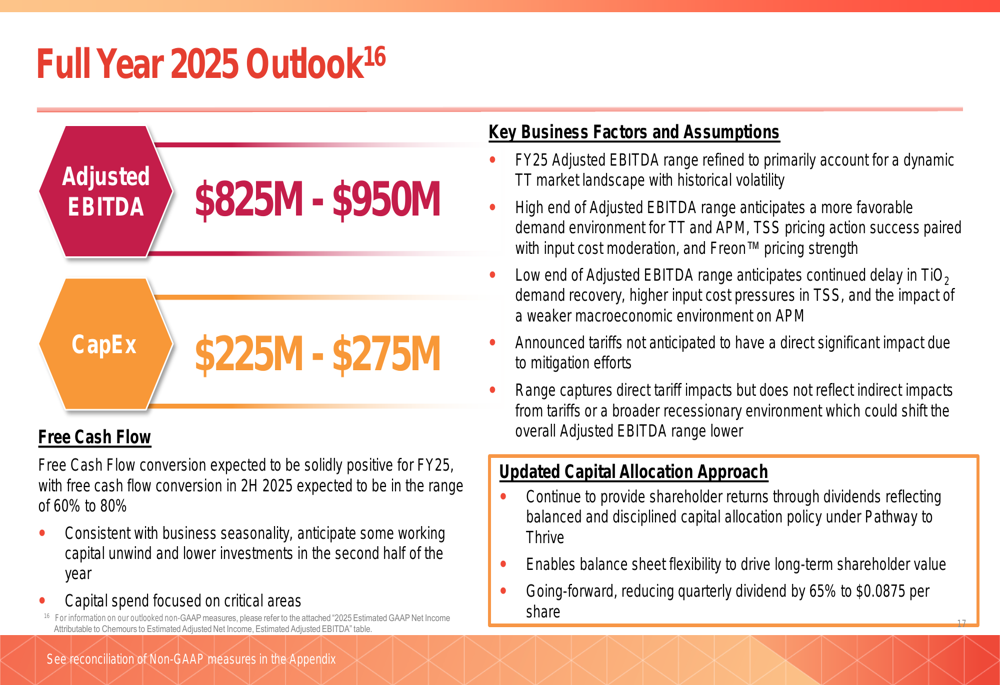

For the full year 2025, Chemours provided this outlook:

The company refined its adjusted EBITDA guidance to a range of $825-$950 million, primarily accounting for what it described as a "dynamic TT market landscape with historical volatility." Capital expenditures are projected at $225-$275 million, and free cash flow is expected to be "solidly positive" for the full year, despite the negative result in Q1.

The guidance suggests Chemours anticipates significant improvement in the coming quarters, though the reduction in dividend indicates management is taking a more conservative approach to capital allocation amid ongoing market uncertainties and high debt levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.