These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Chicago Atlantic Real Estate Finance (NASDAQ:REFI), a commercial mortgage REIT focused on lending to state-licensed cannabis operators, presented its Q1 2025 financial results on May 7, showing mixed performance amid ongoing challenges in the U.S. cannabis sector. The company’s stock traded up 1.71% in after-hours trading following the presentation, suggesting investors found some positives in the results despite certain metrics falling short of year-ago figures.

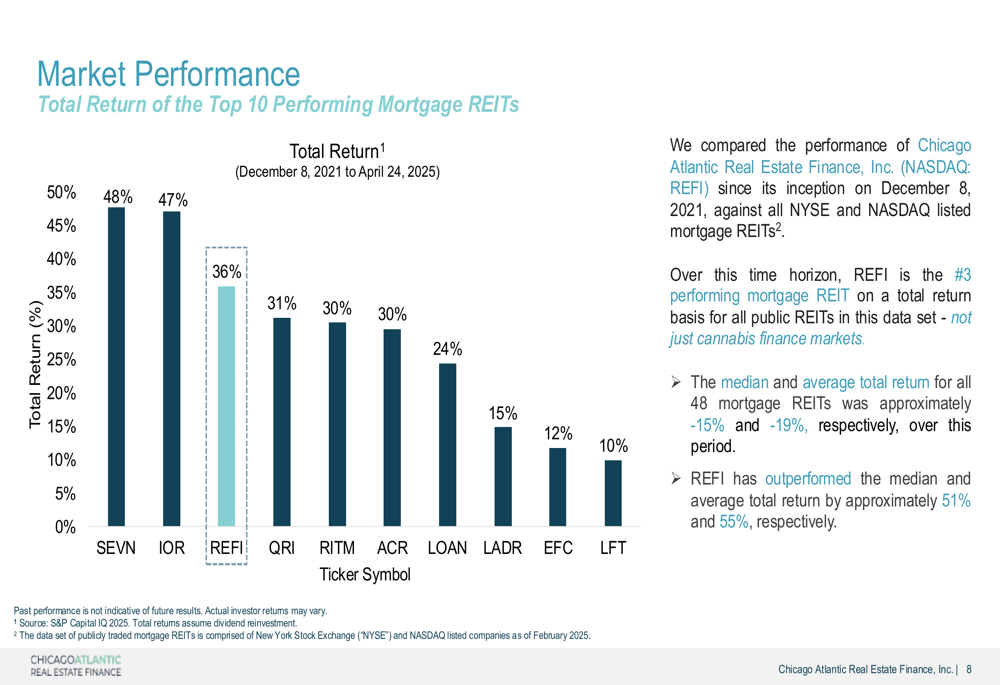

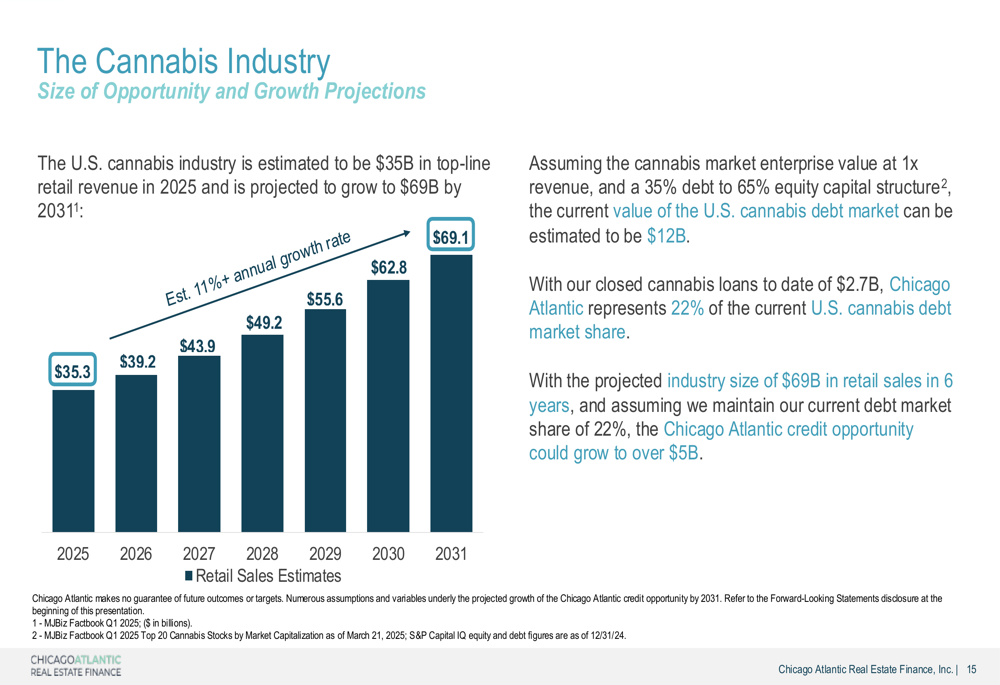

REFI has positioned itself as a leading cannabis lender with approximately 22% of the current U.S. cannabis debt market share, operating in an industry projected to grow from $35 billion in 2025 to $69 billion by 2031. The company’s presentation highlighted its outperformance compared to other mortgage REITs since its December 2021 IPO, with a total return of 36% versus the median of 30% among top-performing peers.

Quarterly Performance Highlights

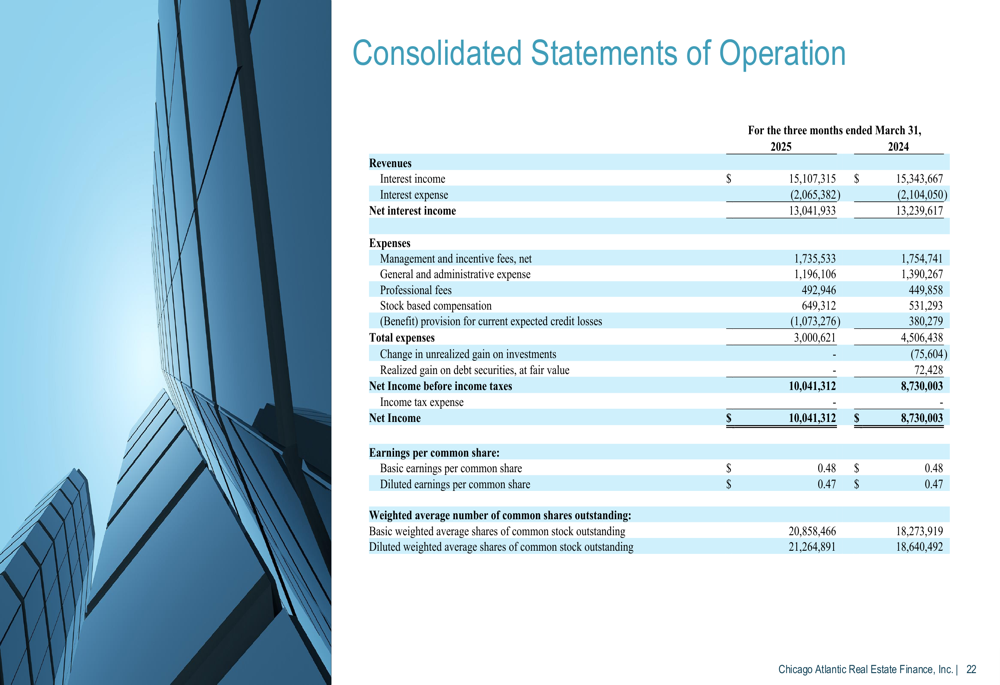

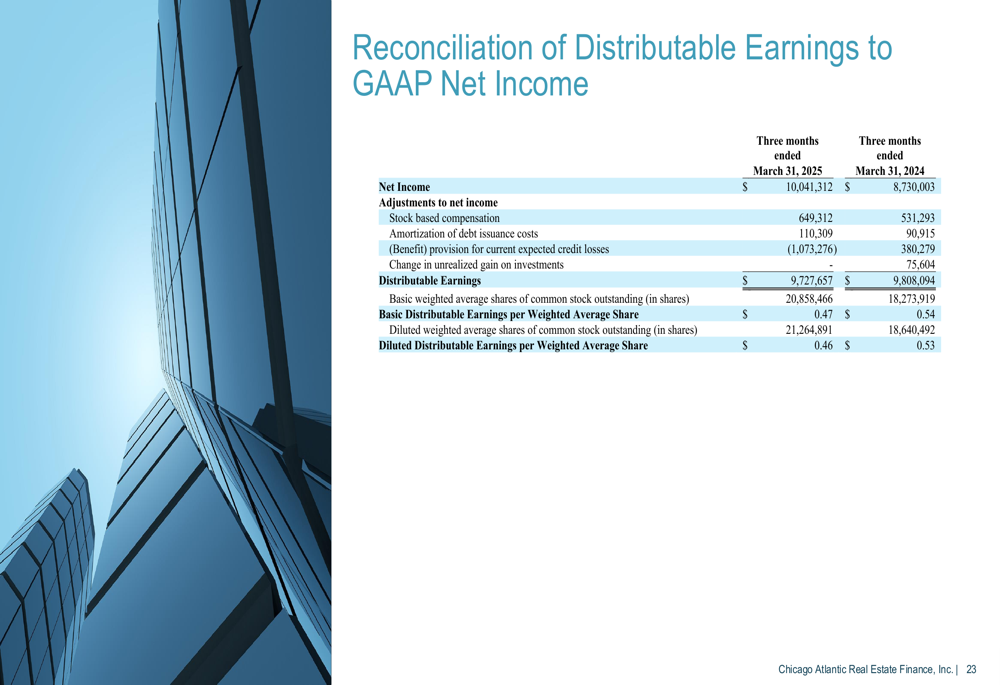

For Q1 2025, Chicago Atlantic reported net income of $10.04 million, representing a 15% increase from $8.73 million in Q1 2024. However, distributable earnings slightly decreased to $9.73 million from $9.81 million in the prior-year period. More notably, basic distributable earnings per share declined to $0.47 from $0.54 year-over-year, a 13% decrease that follows the company’s Q4 2024 earnings miss.

Interest income for the quarter came in at $15.11 million, slightly below the $15.34 million reported in Q1 2024. Net interest income also saw a modest decline to $13.04 million from $13.24 million in the comparable period.

The company’s balance sheet showed total assets of $414.67 million as of March 31, 2025, down from $435.15 million at the end of 2024. This reduction was partially driven by a decrease in the revolving loan from $55 million to $38 million, indicating reduced leverage. Meanwhile, stockholders’ equity increased slightly to $310.78 million from $308.96 million.

Portfolio Composition and Risk Management

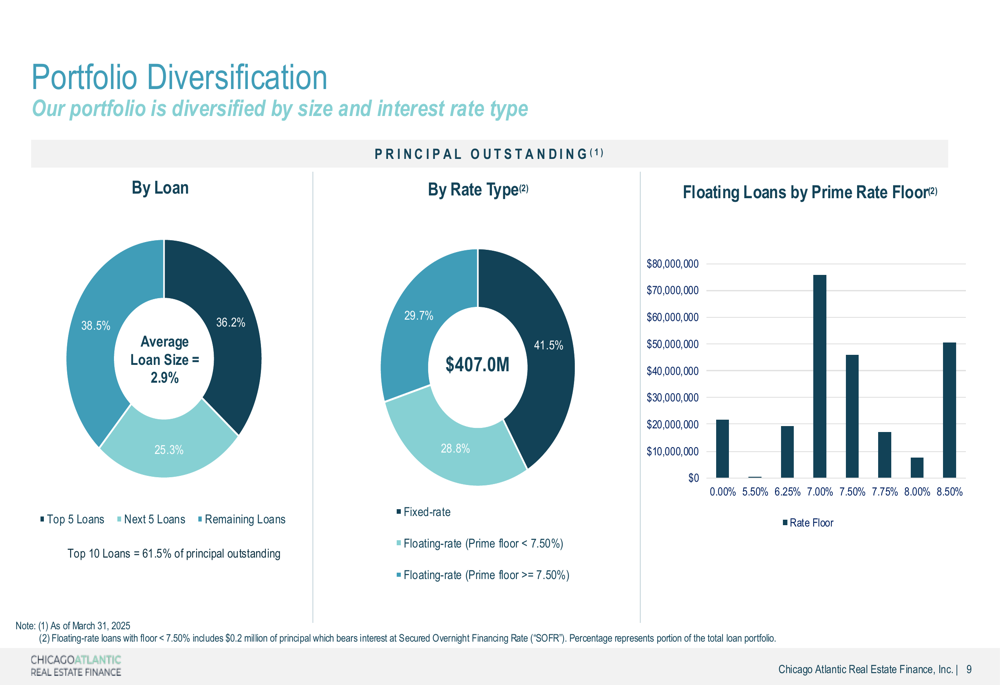

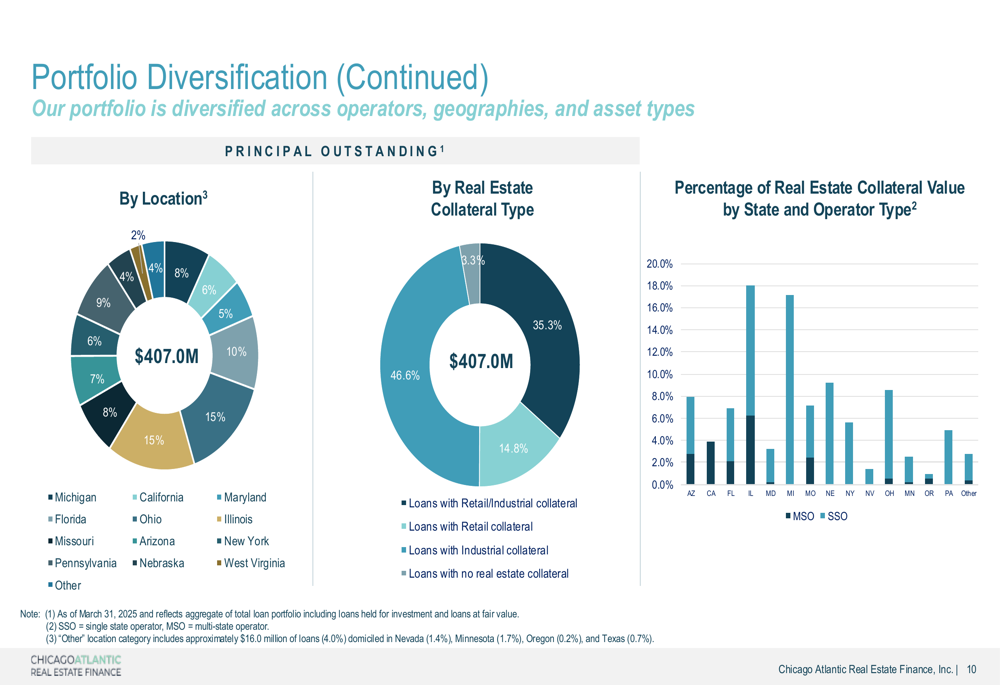

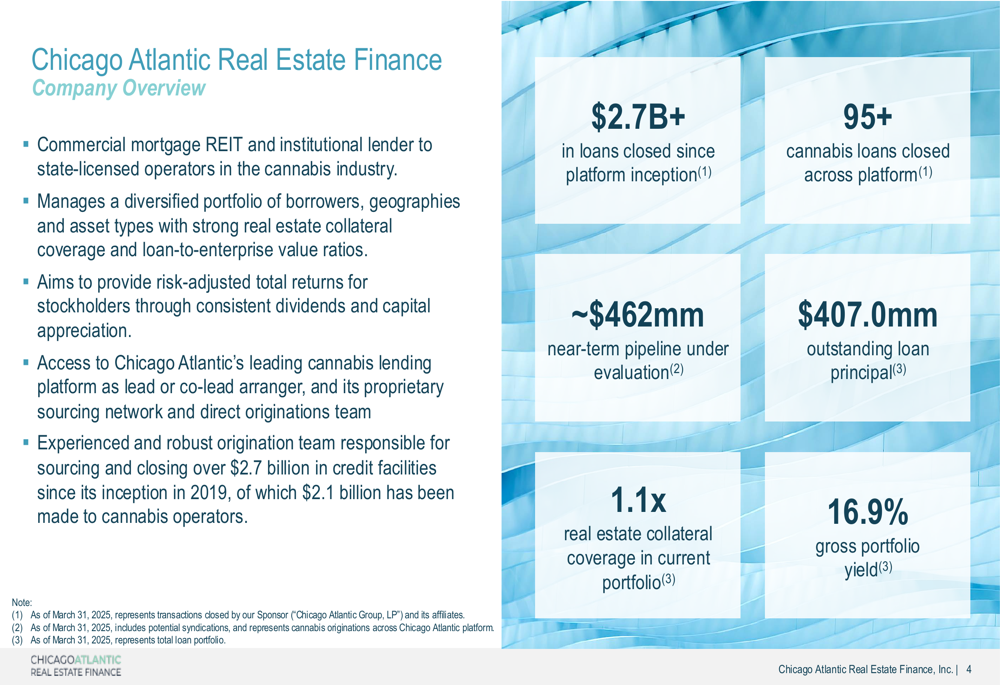

As of March 31, 2025, Chicago Atlantic’s portfolio consisted of $407 million in outstanding loan principal with a gross portfolio yield of 16.9%. The company maintains a diversified approach, though with some concentration among top borrowers - the top 10 loans represent 61.5% of principal outstanding, with the top 5 accounting for 36.2%.

The portfolio shows balanced diversification across rate types, with 29.7% in fixed-rate loans, 28.8% in floating-rate loans with Prime floor below 7.50%, and 41.5% in floating-rate loans with Prime floor at or above 7.50%. This structure provides some protection against interest rate fluctuations.

Geographically, the portfolio is spread across multiple states, with the largest concentrations in California and Michigan (15% each), followed by Maryland (10%) and Nebraska (9%). This diversification helps mitigate regional regulatory risks in the cannabis sector.

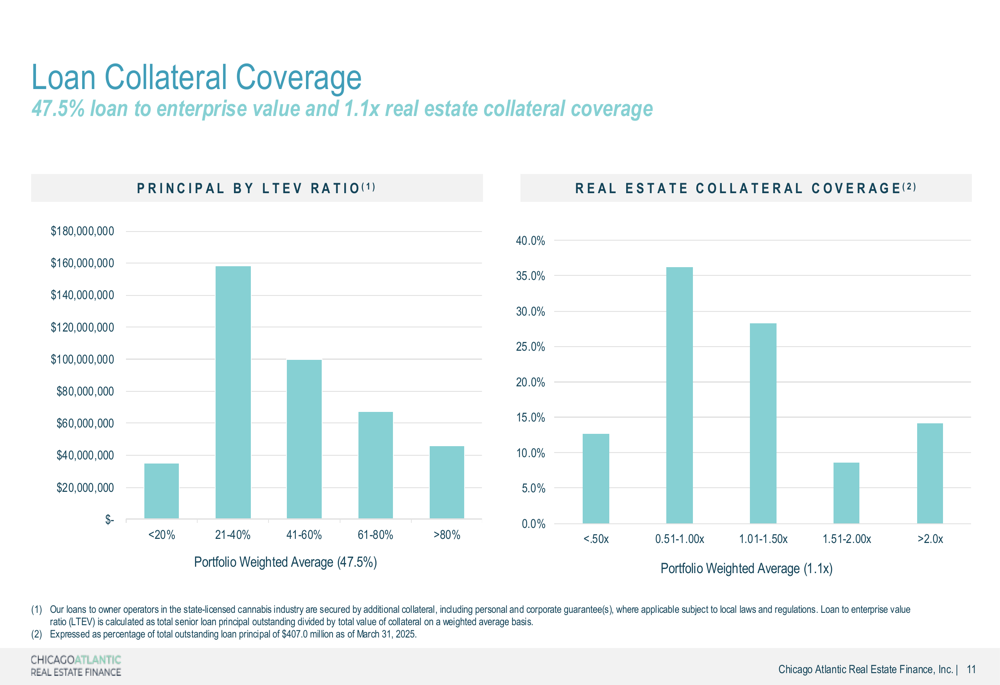

The company emphasizes strong collateral coverage, with a portfolio weighted average of 1.1x real estate collateral coverage. Approximately 96.7% of loans have some form of real estate collateral, with 46.6% backed by both retail and industrial properties. The weighted average loan-to-enterprise-value ratio stands at 47.5%, reflecting the company’s conservative underwriting approach.

Cannabis Industry Outlook

Chicago Atlantic’s presentation highlighted significant growth projections for the U.S. cannabis industry, estimating the market at $35.3 billion in 2025 and forecasting growth to $69.1 billion by 2031. The company noted that maintaining its current 22% debt market share could potentially grow its credit opportunity to over $5 billion as the industry expands.

The presentation emphasized several factors creating lending opportunities, including the lack of traditional financing for cannabis businesses, high barriers to entry in limited license states, and low correlations to traditional markets. As of early 2025, 24 states plus the District of Columbia have legalized both recreational and medical cannabis use, with an additional 17 states permitting medical use only.

Strategic Positioning and Competitive Advantages

Chicago Atlantic positions itself as having several competitive advantages in the cannabis lending space. The company’s presentation highlighted shorter loan durations, lower loan-to-value ratios, and greater diversification compared to competitors. Additionally, the company emphasized its ability to lead deals, upsize existing loans, and maintain close relationships with management teams of borrowers.

The company’s target loan profile focuses on real estate financing, capital expenditure, and growth/acquisition capital, with loan sizes ranging from $10-50 million and terms of 2-3 years. Loans typically feature strong collateral packages including mortgages, stock pledges, and all-asset liens, with loan-to-value ratios below 60% and senior debt to EBITDA ratios less than 2.0x.

Forward-Looking Statements

Looking ahead, Chicago Atlantic remains cautiously optimistic about growth opportunities in the cannabis lending space, while acknowledging industry challenges. The company’s comprehensive investment process emphasizes capital preservation, predictable exit strategies, and strong current income, with regular monitoring of borrowers and quarterly valuations.

The presentation did not provide specific guidance for upcoming quarters, but the historical pattern of distributable earnings and dividends suggests the company aims to maintain its dividend policy. However, investors should note the recent trend of declining distributable earnings per share, which could potentially impact future dividend sustainability if the trend continues.

Given the company’s strong market position, diversified portfolio, and the projected growth of the cannabis industry, Chicago Atlantic appears positioned to navigate the challenging regulatory and competitive landscape, though near-term performance may continue to show volatility as the industry matures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.