Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Chimera Investment Corporation (NYSE:CIM) released its Q1 2025 investor presentation on May 8, highlighting a significant turnaround from the previous quarter’s performance. The mortgage real estate investment trust (REIT) reported a 7.4% increase in book value per share and a return to profitability after posting a loss in Q4 2024. The company’s stock was trading at $12.45 in pre-market, up 3.66% ahead of the presentation.

The Q1 results come as a welcome change for investors following the company’s challenging Q4 2024, when CIM reported a GAAP net loss of $168.3 million and saw its stock drop by 8.18% despite beating revenue and EPS forecasts.

Quarterly Performance Highlights

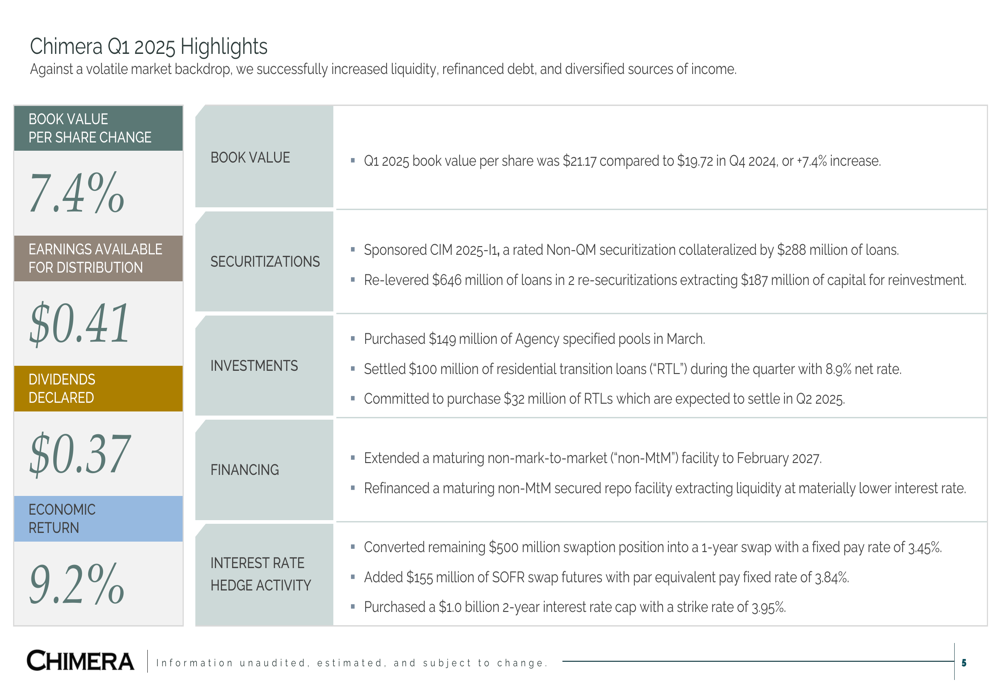

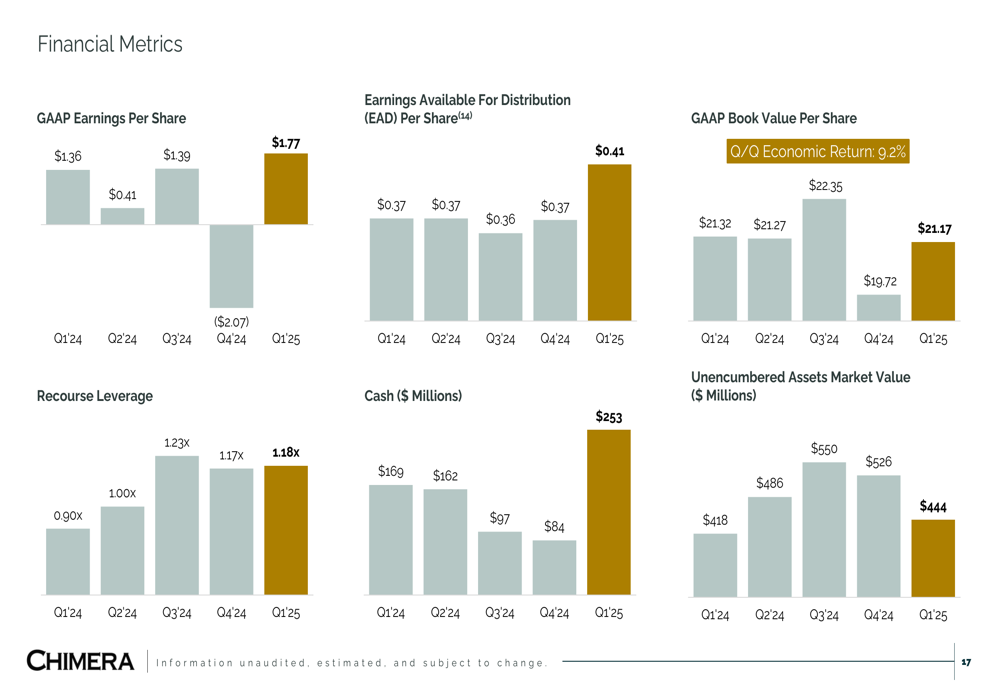

Chimera’s Q1 2025 results showed marked improvement across several key metrics. Book value per share increased to $21.17, representing a 7.4% rise from the previous quarter. The company reported GAAP net income available to common stockholders of $145.9 million, a dramatic improvement from the $168.3 million loss reported in Q4 2024.

As shown in the following highlights from the presentation:

The company completed two securitizations during the quarter and re-leveraged $646 million of loans, freeing up $187 million to be reinvested. Chimera also strategically positioned itself against interest rate volatility by converting its remaining $500 million swaption position into a 1-year swap with a fixed pay rate of 3.45% and adding $155 million of SOFR swap futures with a par equivalent pay fixed rate of 3.84%.

Earnings Available for Distribution (EAD), a non-GAAP measure that the company uses to determine dividend payments, increased to $33.5 million in Q1 2025 from $30.4 million in Q4 2024. The company maintained a strong liquidity position with $253 million in cash.

Portfolio Composition and Strategy

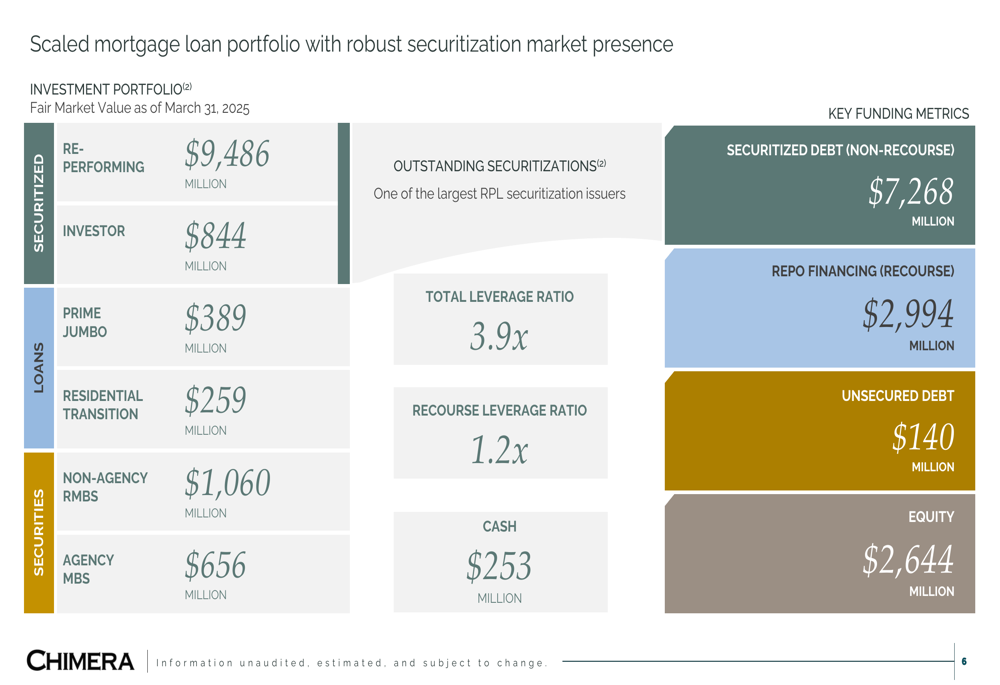

Chimera’s investment portfolio remains diversified across various mortgage-related assets. As of March 31, 2025, the company’s portfolio included $9.5 billion in re-performing loans, $844 million in investor loans, $389 million in prime jumbo loans, $259 million in residential transition loans, $1.1 billion in non-agency RMBS, and $656 million in agency MBS.

The following chart illustrates the composition of Chimera’s scaled mortgage loan portfolio:

The company maintained a total leverage ratio of 3.9x and a recourse leverage ratio of 1.2x, unchanged from the previous quarter. Funding sources included $7.3 billion in non-recourse securitized debt, $3.0 billion in recourse repo financing, and $140 million in unsecured debt, supported by $2.6 billion in equity.

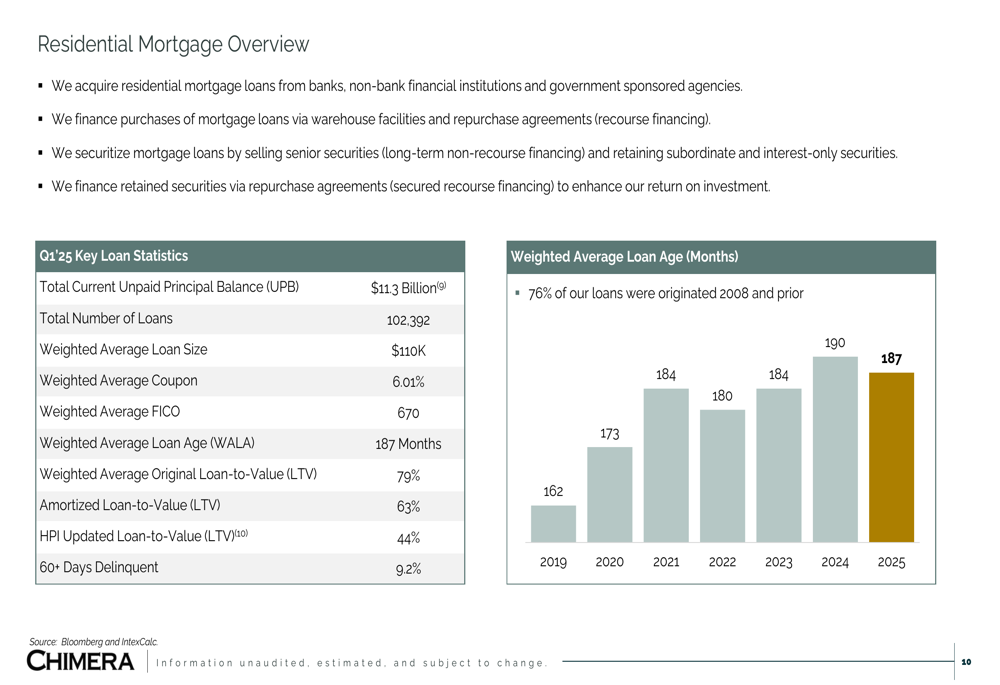

Chimera’s residential mortgage portfolio consists of 102,392 loans with a total unpaid principal balance of $11.3 billion. The weighted average loan age is 187 months, with 76% of loans originated in 2008 or earlier. The portfolio has benefited from housing price appreciation, with updated loan-to-value ratios improving from 66% in 2019 to 44% in 2025.

The following chart shows key metrics of the residential mortgage portfolio:

Third-Party Asset Management Growth

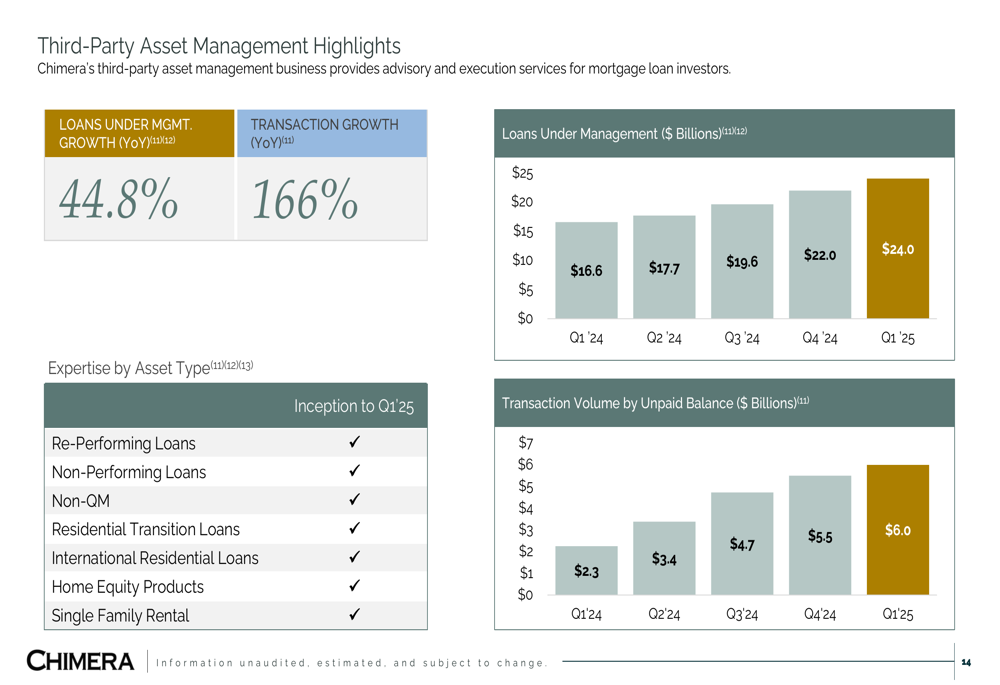

A standout area of growth for Chimera has been its third-party asset management business, which saw loans under management increase by 44.8% year-over-year to $24.0 billion. Transaction (JO:NTUJ) volume grew even more dramatically, up 166% compared to Q1 2024.

The following chart demonstrates this impressive growth trajectory:

This expansion of the asset management business represents a strategic diversification of revenue streams for Chimera, potentially providing more stable fee-based income to complement its investment portfolio returns. The company has developed expertise across multiple asset types, including re-performing loans, non-performing loans, non-QM loans, residential transition loans, international residential loans, home equity products, and single-family rental properties.

Financial Analysis

Chimera’s financial metrics show improvement across several key indicators. The company’s economic net interest income increased to $72.3 million in Q1 2025 from $69.2 million in Q4 2024, reflecting improved spreads between asset yields and funding costs.

The following chart illustrates key financial metrics over recent quarters:

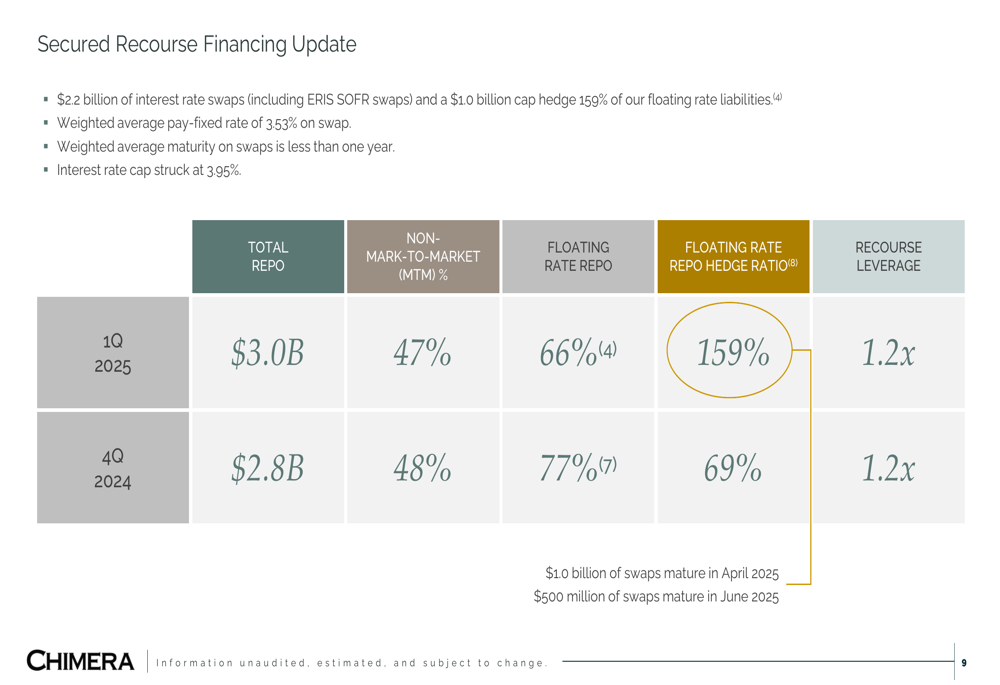

The company has also been active in managing its interest rate risk. As of Q1 2025, Chimera had $2.2 billion of interest rate swaps with a weighted average pay-fixed rate of 3.53% to hedge its floating rate liabilities. The floating rate repo hedge ratio increased significantly to 159% in Q1 2025 from 69% in Q4 2024.

The following table provides details on Chimera’s secured recourse financing:

Chimera also enhanced its liquidity through securitization, releasing $187 million of investable capital by exercising call rights on seven non-REMIC securitizations and re-securitizing the collateral in two new securitizations.

Forward-Looking Statements

Looking ahead, Chimera appears well-positioned to continue its recovery trajectory. The company’s strategy focuses on maintaining a diversified portfolio across the mortgage credit spectrum while growing its third-party asset management business.

The improved housing market fundamentals, with updated loan-to-value ratios now at 44%, provide a cushion against potential credit losses. However, the 60+ day delinquency rate of 9.2% remains a concern that investors should monitor.

Chimera’s securitization expertise remains a core strength, with the company having completed 108 deals and securitized $54 billion in residential mortgage assets since inception. This expertise allows the company to optimize its balance sheet and enhance liquidity, as demonstrated by the recent re-securitization activities.

With its improved financial position, diversified portfolio, and growing asset management business, Chimera appears to be executing a strategic pivot that could position it well for sustainable growth in the evolving mortgage market landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.