Evercore picks Astera and MACOM as top AI connectivity stocks

Introduction & Market Context

Chimera Investment Corporation (NYSE:CIM) revealed its Q2 2025 financial performance and strategic initiatives in its latest investor presentation. The hybrid mortgage REIT reported modest financial results while highlighting a significant acquisition and continued expansion of its third-party asset management business against a challenging housing market backdrop.

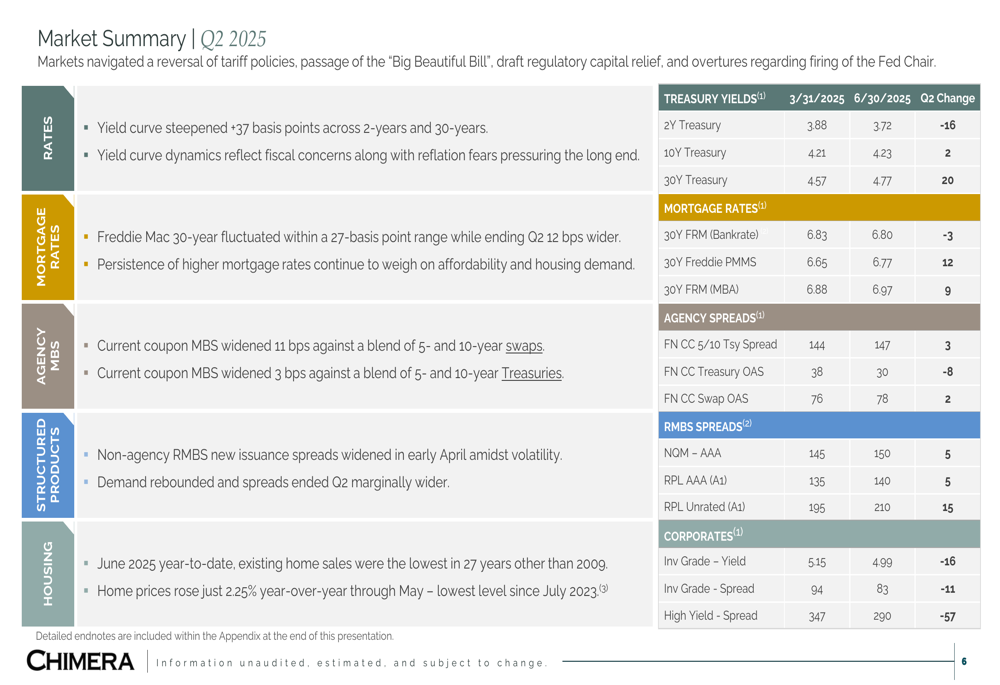

The company’s presentation emphasized that the current market environment features a steepening yield curve reflecting fiscal concerns and higher mortgage rates impacting housing affordability. Notably, existing home sales through June 2025 were at their lowest level in 27 years (except for 2009), while home prices rose just 2.25% year-over-year through May.

As shown in the following market summary chart detailing key rate and spread movements:

Quarterly Performance Highlights

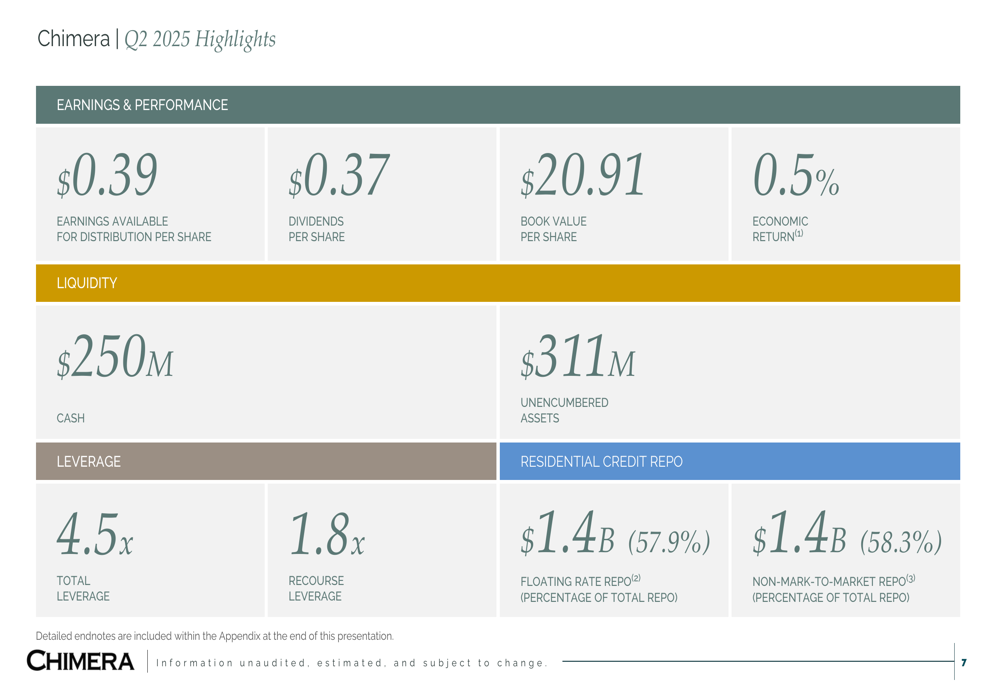

Chimera reported Earnings Available for Distribution per share of $0.39 for Q2 2025, slightly below the $0.41 reported in Q1 2025. The company declared dividends of $0.37 per share and maintained a book value per share of $20.91, generating a modest economic return of 0.5%.

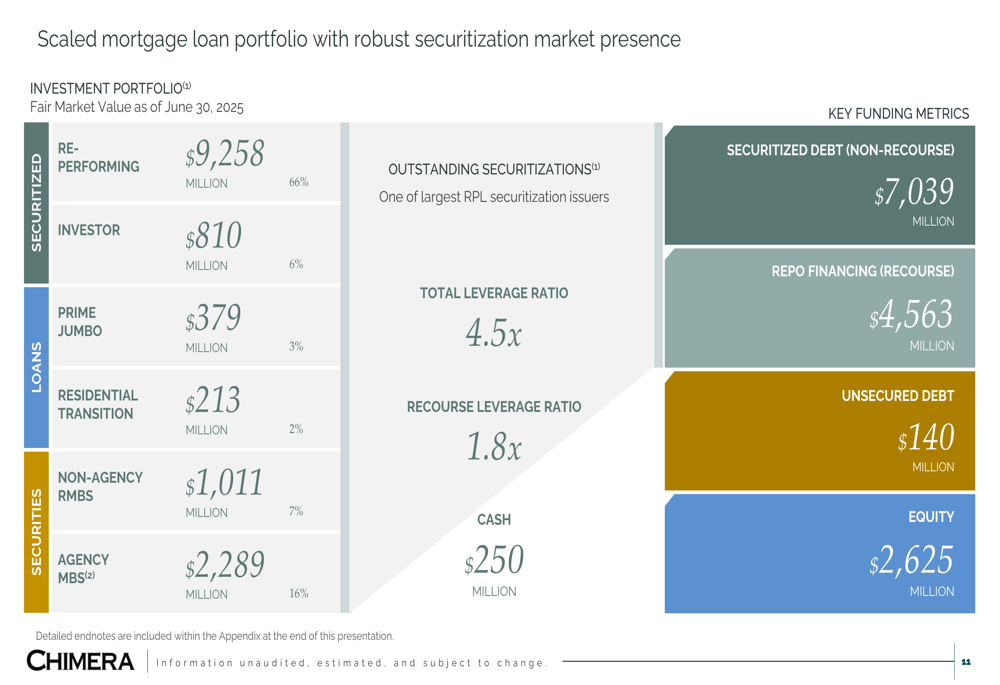

The company’s financial position includes $250 million in cash and $311 million in unencumbered assets. Chimera’s leverage metrics show total leverage of 4.5x (up from 3.9x in Q1) and recourse leverage of 1.8x, indicating a more aggressive capital deployment strategy compared to the previous quarter.

The following slide highlights Chimera’s key financial metrics for the quarter:

During the quarter, Chimera purchased $1.9 billion in notional Agency pass-throughs, with an additional $402 million settled in Q3. The company also managed its interest rate risk with $2.0 billion in swap notional against its Agency RMBS portfolio, while $1.5 billion of swap notional matured during the quarter.

Strategic Initiatives

The most significant strategic development announced was Chimera’s definitive agreement to acquire HomeXpress Mortgage Corp, with the transaction expected to close in Q4 2025. This acquisition represents a major step in Chimera’s evolution as a hybrid mortgage REIT.

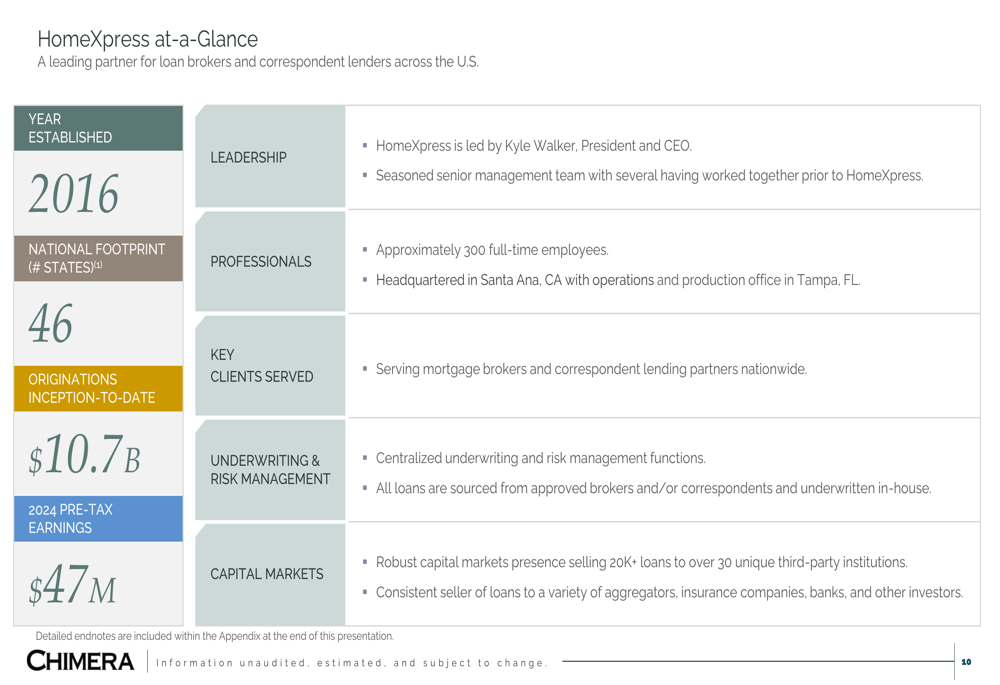

HomeXpress is a leading nationwide lending platform that has originated more than $10.7 billion of loans since its establishment in 2016. The company operates in 46 states, employs approximately 300 full-time staff, and reported $47 million in pre-tax earnings for 2024.

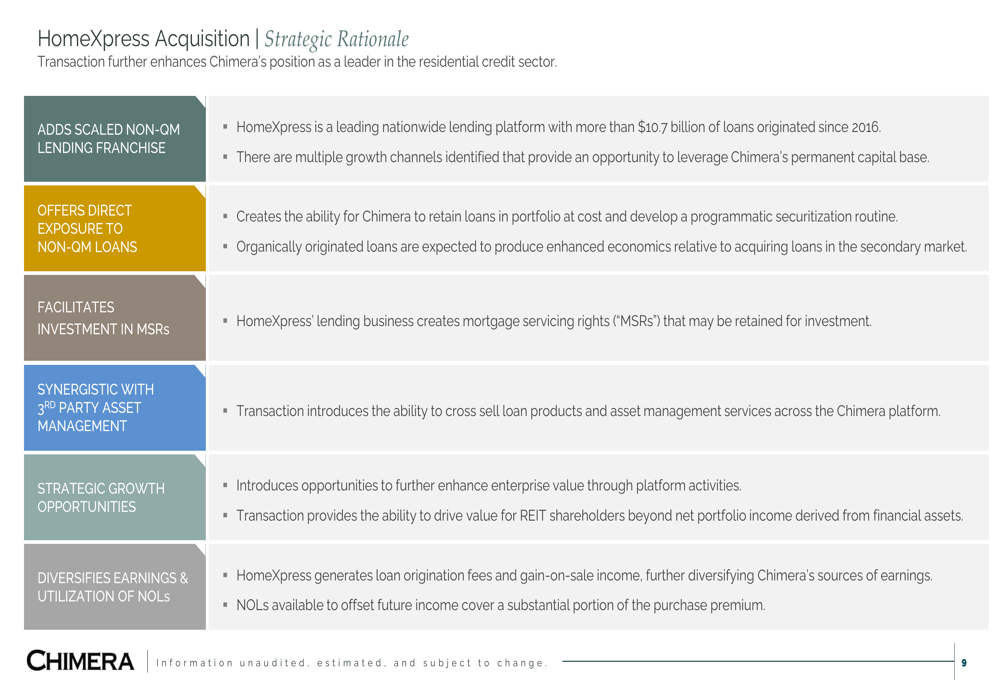

The strategic rationale behind the acquisition is illustrated in the following slide:

Chimera’s management highlighted that the acquisition will add a scaled non-QM lending franchise, provide direct exposure to non-QM loans, facilitate investment in mortgage servicing rights (MSRs), create synergies with the company’s third-party asset management business, and diversify earnings.

The following slide provides additional details about HomeXpress:

Detailed Financial Analysis

Chimera’s investment portfolio remains heavily weighted toward residential mortgage assets, with a significant focus on re-performing loans. As of June 30, 2025, the company’s scaled mortgage loan portfolio showed re-performing loans at $9,258 million (66%), investor loans at $810 million (6%), and non-Agency RMBS at $1,011 million (7%).

The company’s funding structure includes $7,039 million in securitized debt (non-recourse) and $4,563 million in repo financing (recourse), supporting $2,625 million in equity.

The following slide illustrates the composition of Chimera’s mortgage loan portfolio:

The company’s investment summary shows a total investment portfolio with $18,006,091 (in thousands) in principal value and $13,960,597 in fair value across various asset classes including Non-Agency RMBS, Agency RMBS, Agency CMBS, and Loans Held for Investment.

Chimera’s residential credit portfolio consists primarily of re-performing loans (87%), with a total current unpaid principal balance of $10.9 billion across 95,686 loans. The weighted average interest rate on this portfolio is 5.95%, with a weighted average loan age of 191 months.

Forward-Looking Statements

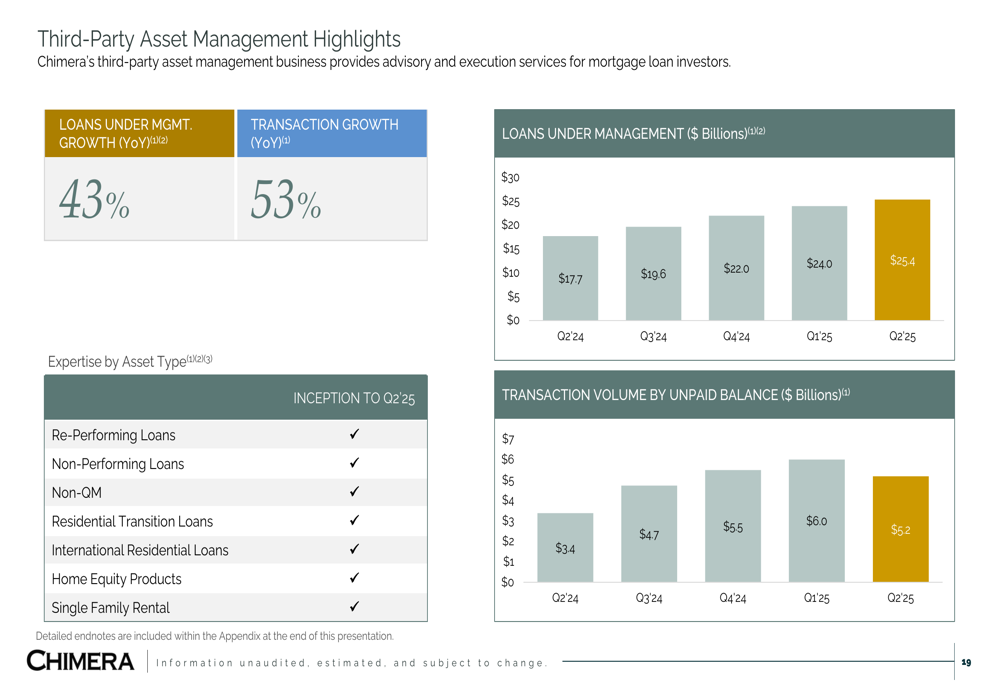

A notable bright spot in Chimera’s presentation was the strong performance of its third-party asset management business, which showed 43% year-over-year growth in loans under management, reaching $25.4 billion. Transaction (JO:NTUJ) growth was even more impressive at 53% year-over-year.

The following chart illustrates this growth trajectory:

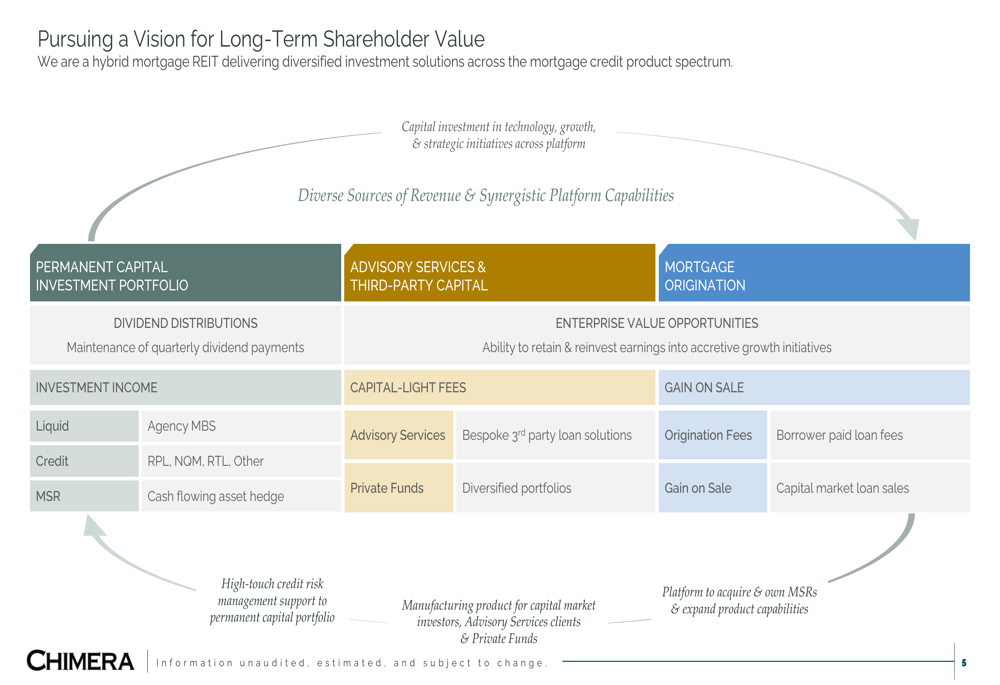

Chimera’s vision for long-term shareholder value creation emphasizes the interconnectedness of its permanent capital investment portfolio, advisory services & third-party capital, and mortgage origination capabilities. The company is focusing on diverse revenue sources including investment income, capital-light fees from advisory services, and gain-on-sale income.

As shown in the following strategic vision diagram:

The HomeXpress acquisition aligns with this vision by strengthening Chimera’s mortgage origination capabilities and creating additional synergies with its third-party asset management business.

Looking ahead, Chimera appears positioned to navigate the challenging housing market environment through its diversified approach. While the current economic return remains modest at 0.5%, the strategic initiatives underway, particularly the HomeXpress acquisition and the growing third-party asset management business, provide potential catalysts for future growth.

Chimera’s stock closed at $13.57 on August 5, 2025, down 0.73% for the day, and continues to trade well below its 52-week high of $16.89, suggesting potential upside if the company’s strategic initiatives deliver the anticipated benefits.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.