BitMine increases ethereum holdings to $6.6 billion, adds 373,000 tokens

Introduction & Market Context

Chord Energy (NASDAQ:CHRD) presented its Q1 2025 corporate slides on May 7, 2025, positioning itself as a disciplined, oil-focused Williston Basin operator delivering strong returns despite trading at a discount to peers. The company’s stock closed at $90.28 on May 6, 2025, with after-hours trading showing a 2.09% increase to $92.50, still well below its 52-week high of $188.02.

Following strong Q4 2024 results that exceeded analyst expectations with EPS of $3.49 versus the forecasted $2.96, Chord continues to emphasize its attractive valuation relative to its asset base and cash flow generation capabilities.

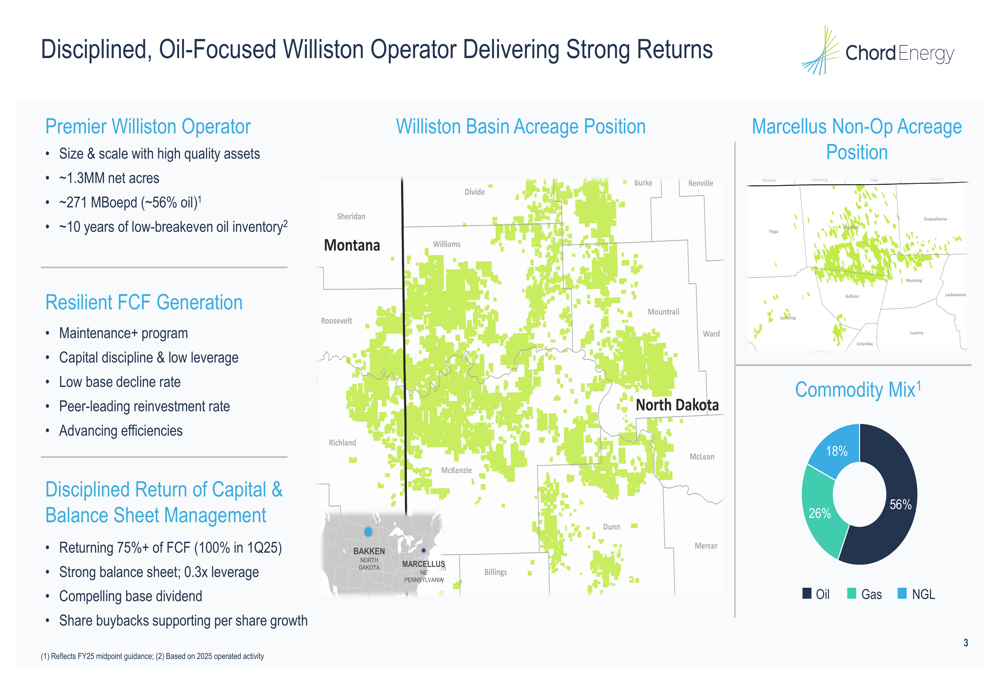

As shown in the following overview slide, Chord Energy maintains a significant position in the Williston Basin with approximately 1.3 million net acres, production of around 271 MBoepd (56% oil), and an estimated 10 years of low-breakeven oil inventory:

Operational Strategy & Efficiency Improvements

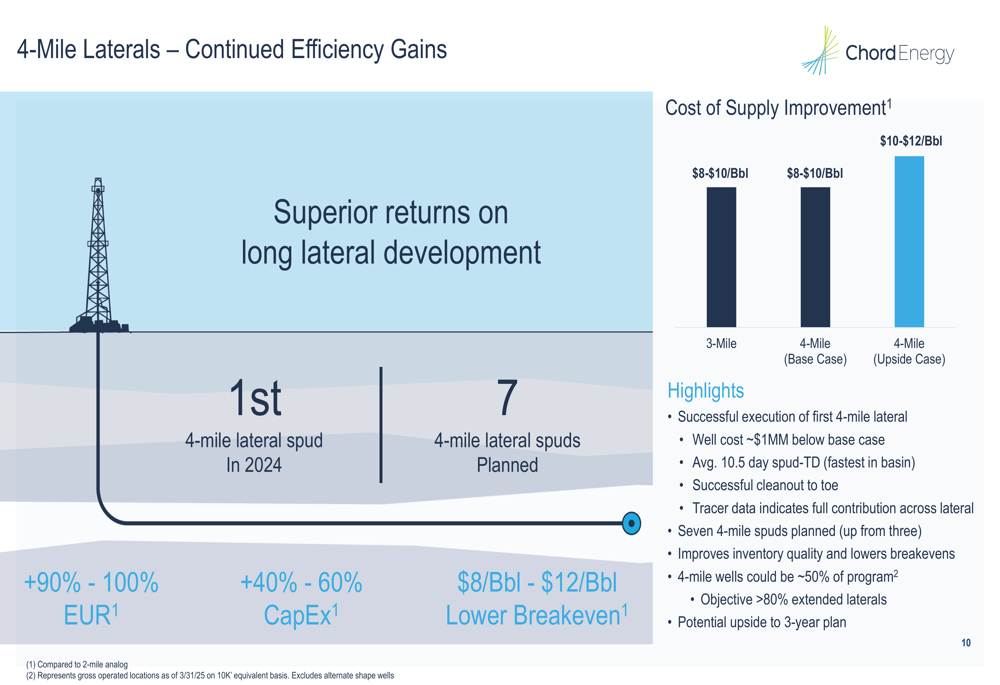

Chord Energy’s operational strategy centers on extending lateral lengths to improve capital efficiency and returns. The company has successfully executed its first 4-mile lateral well at approximately $1 million below base case projections, with seven 4-mile spuds planned for the year (increased from an initial three).

According to the presentation, these longer laterals significantly improve economics by increasing EUR (Estimated Ultimate Recovery) by 90-100% while only increasing capital expenditures by 40-60%, resulting in lower breakeven costs of $8-12 per barrel.

The following slide illustrates the economic benefits of the company’s 4-mile lateral development strategy:

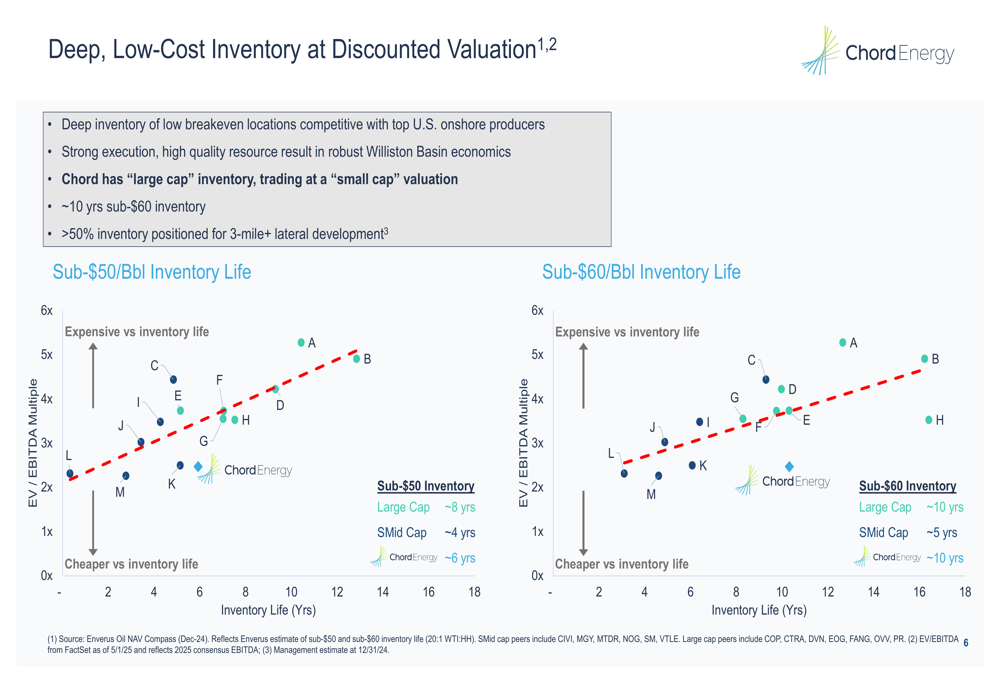

This operational efficiency is part of Chord’s broader strategy to maintain a competitive inventory of drilling locations. The company claims to have approximately 10 years of sub-$60 breakeven inventory, with more than 50% positioned for 3-mile or longer lateral development.

The scatter plot below shows Chord’s inventory position relative to peers, suggesting it has "large cap" inventory quality while trading at a "small cap" valuation:

Financial Position & Capital Allocation

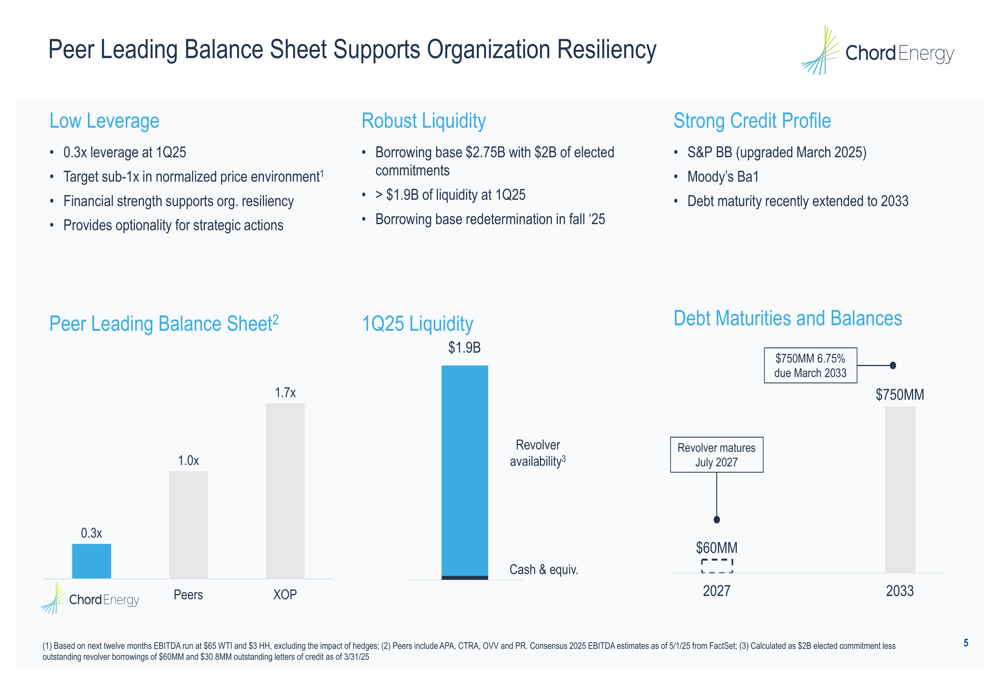

Chord Energy maintains a strong balance sheet with a leverage ratio of 0.3x as of Q1 2025, significantly below the peer average of 1.0x. This financial strength provides flexibility for strategic actions and supports the company’s shareholder return initiatives.

The company reported robust liquidity of approximately $1.9 billion at the end of Q1 2025, with a borrowing base of $2.75 billion and $2 billion of elected commitments. Chord’s debt maturity was recently extended to 2033, and its credit rating was upgraded by S&P to BB in March 2025.

As illustrated in the following chart, Chord’s leverage ratio compares favorably to both its direct peers and the broader energy index:

This financial discipline extends to Chord’s capital allocation strategy, with a reinvestment rate of 41% from 2022-2024, which the company claims is lower than most peers. The company’s low base oil decline rate of 35% supports durable free cash flow generation even in challenging price environments.

Shareholder Returns & Valuation

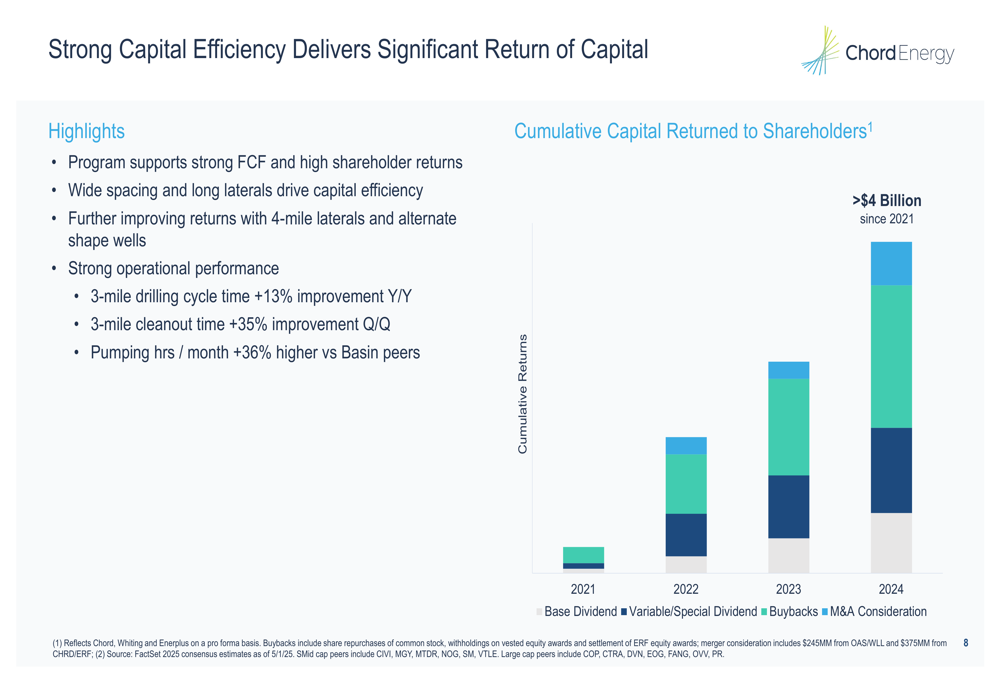

Chord Energy has returned over $4 billion to shareholders since 2021 through a combination of base dividends, variable dividends, and share repurchases. The company increased its base dividend to $5.20 per share annually in February 2025, representing approximately a 6% yield.

The following chart illustrates Chord’s cumulative capital returned to shareholders since 2021:

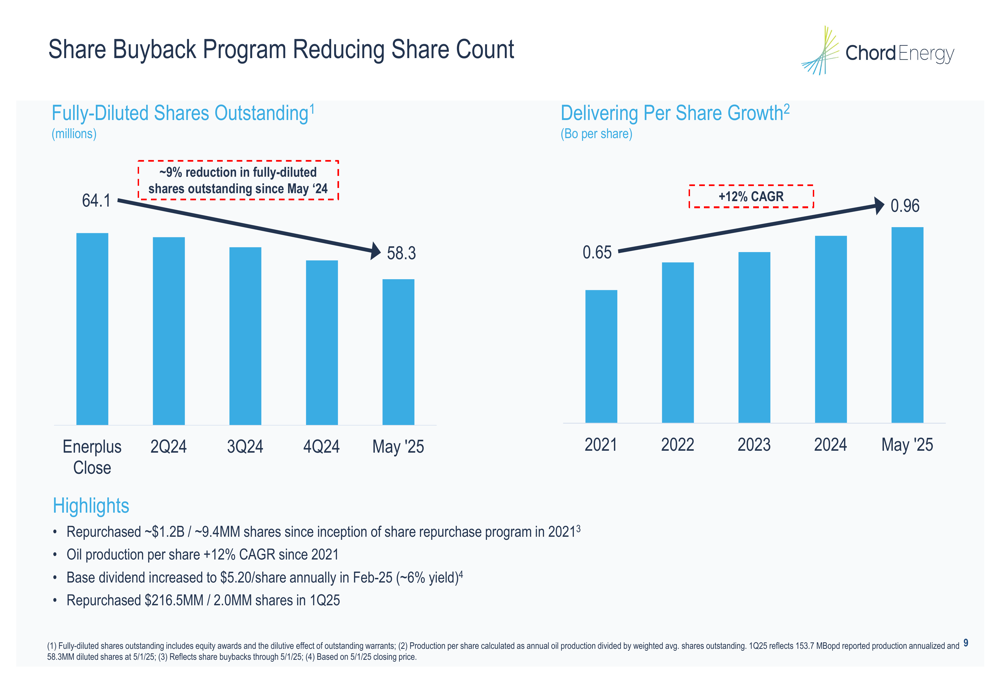

Share repurchases have been a significant component of Chord’s capital return strategy. Since May 2024, the company has reduced its fully-diluted share count by approximately 9%, from 64.1 million shares to 58.3 million shares. In Q1 2025 alone, Chord repurchased $216.5 million worth of shares (approximately 2.0 million shares).

This aggressive buyback program has contributed to per-share growth metrics, with oil production per share increasing at a 12% CAGR since 2021:

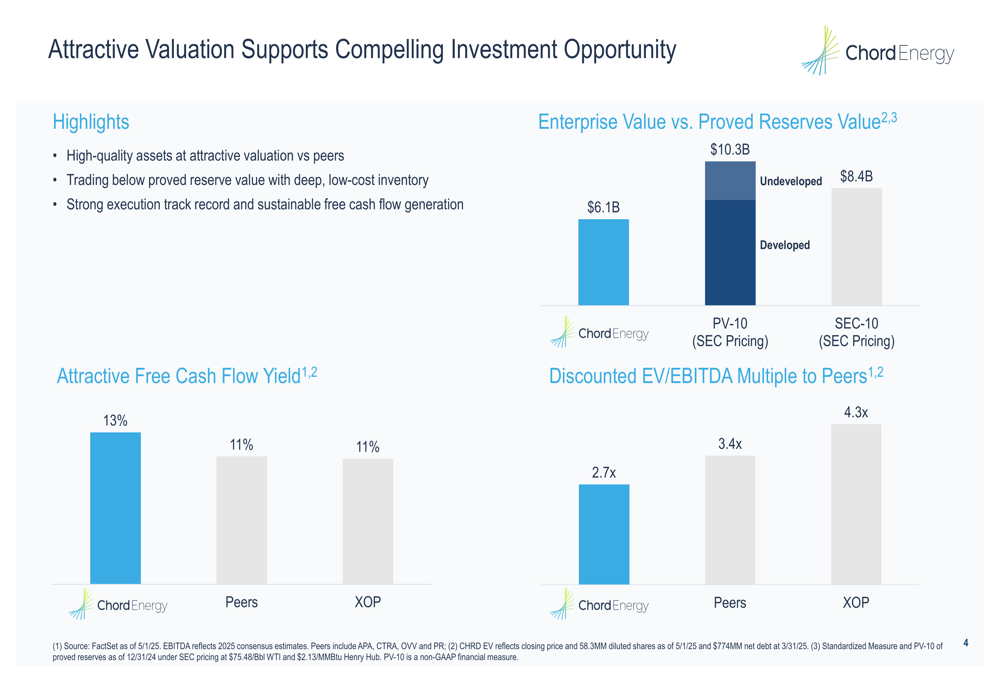

Chord argues that it represents a compelling investment opportunity based on several valuation metrics. The company’s enterprise value of $6.1 billion trades below its PV-10 value of $10.3 billion. Additionally, Chord claims a free cash flow yield of 13% compared to 11% for peers and an EV/EBITDA multiple of 2.7x versus 3.4x for peers.

The following slide highlights these valuation metrics:

Forward Outlook

Looking ahead, Chord Energy projects capital investment of $1.4 billion for 2025 with expected production between 152,000 and 153,000 barrels of oil per day, according to statements from the Q4 2024 earnings call. The company anticipates generating approximately $860 million in free cash flow with a reinvestment rate of around 60%.

Chord is also exploring potential monetization of its non-operated Marcellus assets, which could provide additional capital for shareholder returns or strategic investments.

The company’s three-year outlook focuses on continued operational efficiency improvements, with a goal of having 80% of inventory developed through long-lateral wells. Management has indicated that 4-mile wells could eventually comprise approximately 50% of the development program.

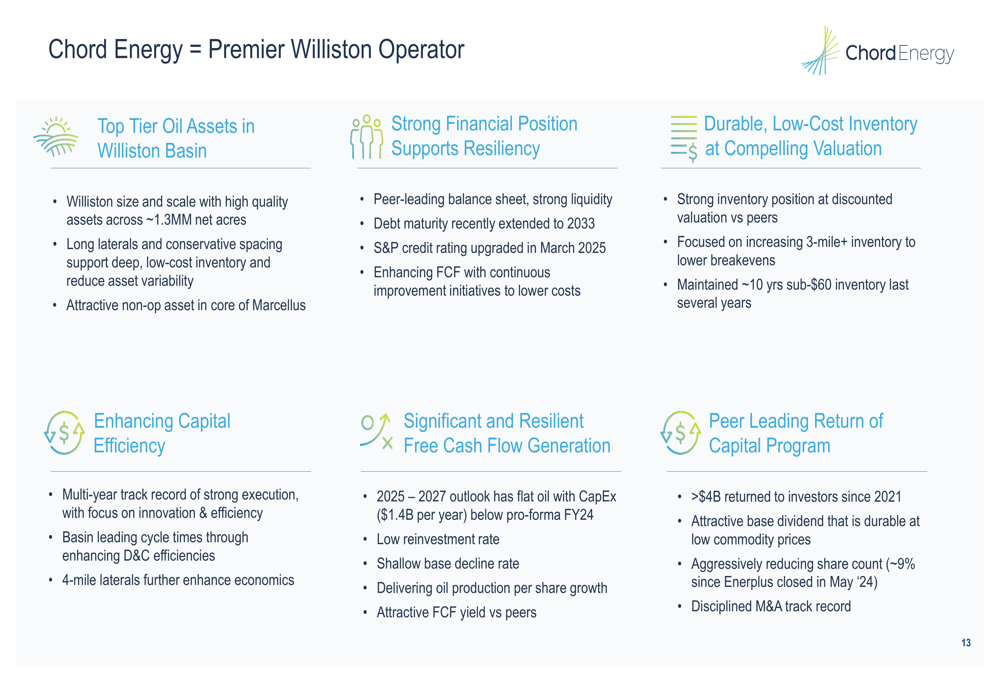

As summarized in the following slide, Chord positions itself as a premier Williston operator with strong financial positioning, durable inventory, and a commitment to shareholder returns:

While Chord Energy’s presentation paints an optimistic picture of its operational efficiency and shareholder return strategy, investors should note that the stock currently trades significantly below its 52-week high, suggesting the market may not fully share the company’s valuation assessment. However, with strong Q4 2024 results exceeding analyst expectations and a continued focus on capital discipline and shareholder returns, Chord appears positioned to potentially narrow this valuation gap.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.