Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

Canadian Imperial Bank of Commerce (TSE:CM) released its third quarter 2025 results on August 28, 2025, reporting strong performance across all business segments. The bank’s shares rose 3.61% in premarket trading to $78, building on momentum from its previous quarter’s outperformance. CIBC’s continued execution of its client-focused strategy has delivered another quarter of double-digit growth in key financial metrics.

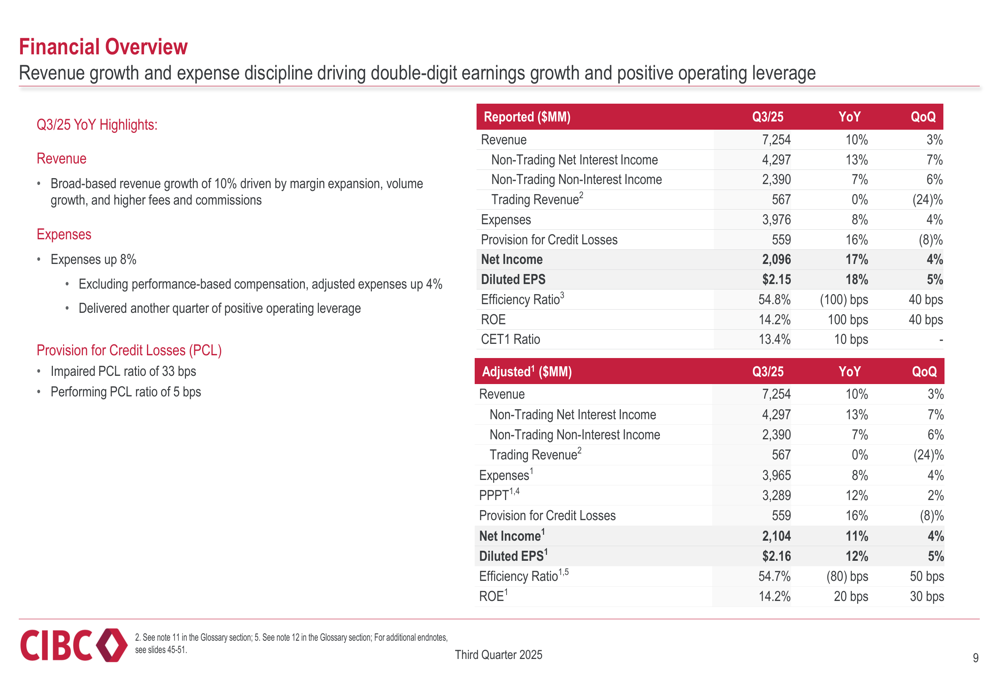

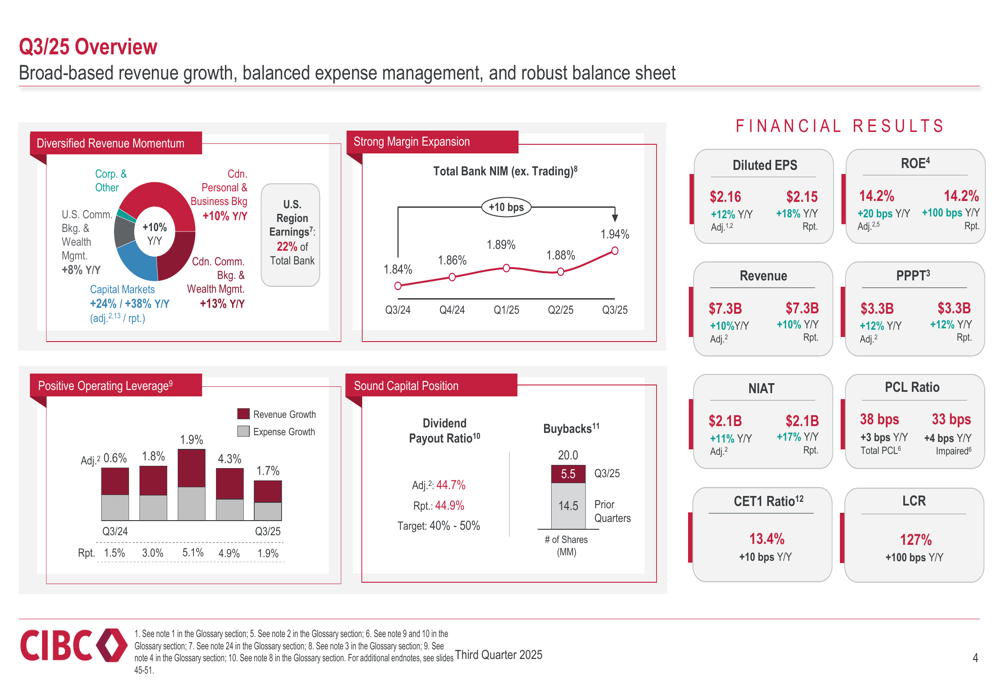

The bank reported diluted earnings per share (EPS) of $2.15, representing an 18% increase year-over-year, while adjusted EPS rose 12% to $2.16. This continues the positive trend seen in Q2 2025, when CIBC beat market expectations with EPS of $2.05.

Quarterly Performance Highlights

CIBC delivered robust financial results for Q3 2025, with revenue reaching $7.3 billion, up 10% compared to the same period last year. Net income rose 17% year-over-year to $2.1 billion, while return on equity remained strong at 14.2%. The bank maintained positive operating leverage at 1.9% (1.7% on an adjusted basis), reflecting effective expense management alongside revenue growth.

As shown in the following comprehensive snapshot of Q3 results:

The bank’s efficiency ratio improved by 100 basis points to 54.8% (54.7% adjusted), demonstrating CIBC’s ability to generate more revenue while controlling costs. Pre-provision, pre-tax earnings (PPPT) grew by 12% year-over-year to $3.3 billion, providing a solid foundation for profitability.

All business segments contributed to the strong performance:

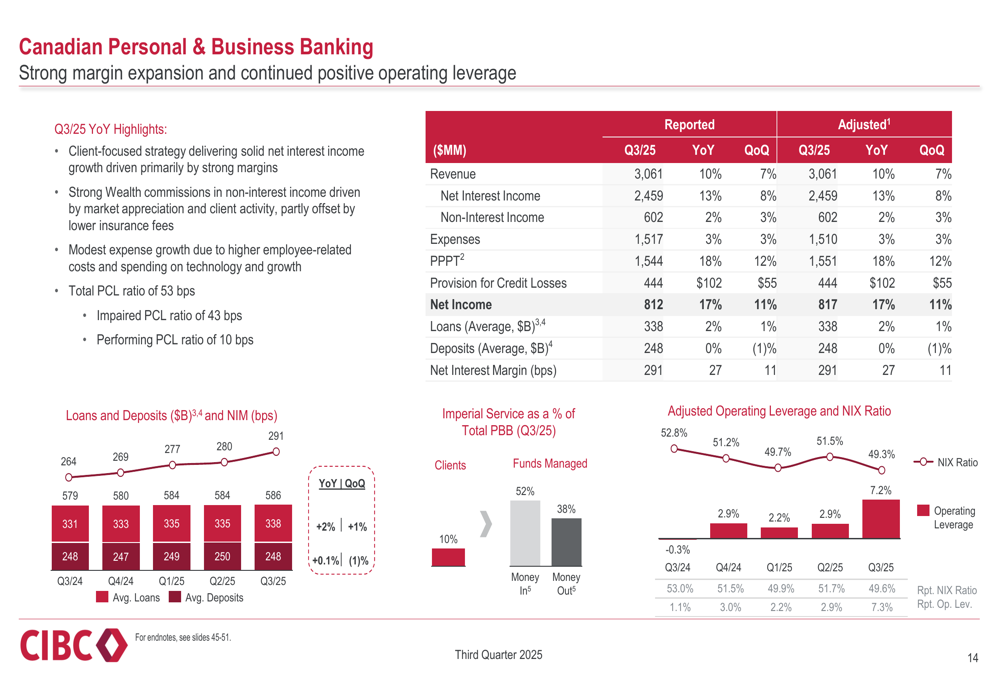

Canadian Personal & Business Banking reported net income of $812 million, up 17% year-over-year, driven by strong margin expansion and continued positive operating leverage. Net interest income in this segment grew by 13% compared to Q3 2024.

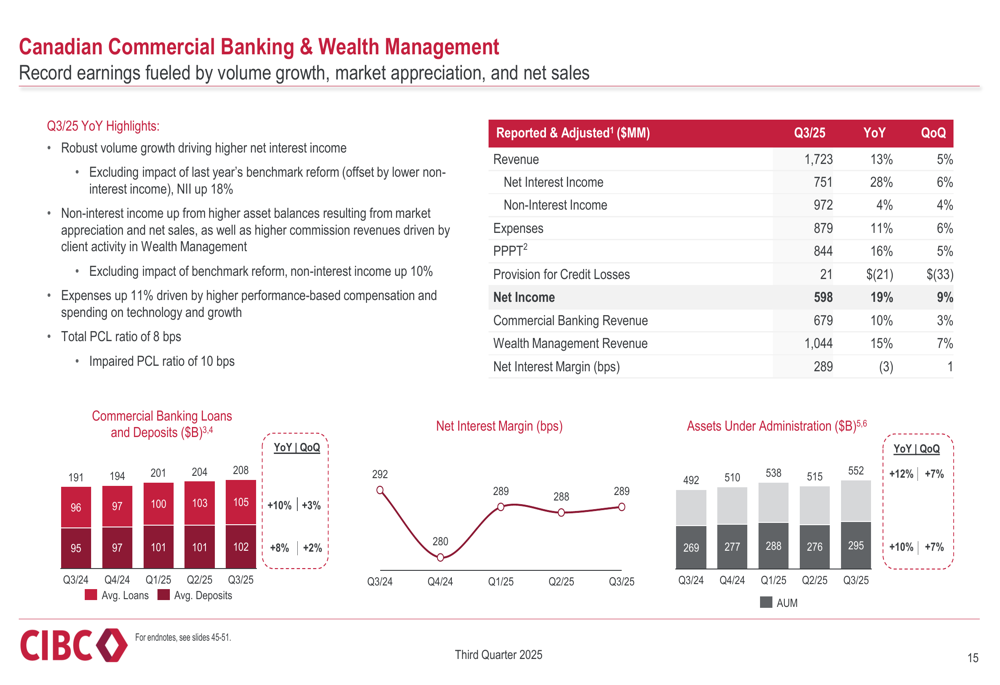

Canadian Commercial Banking & Wealth Management achieved record earnings with net income of $598 million, a 19% increase year-over-year, fueled by volume growth, market appreciation, and net sales.

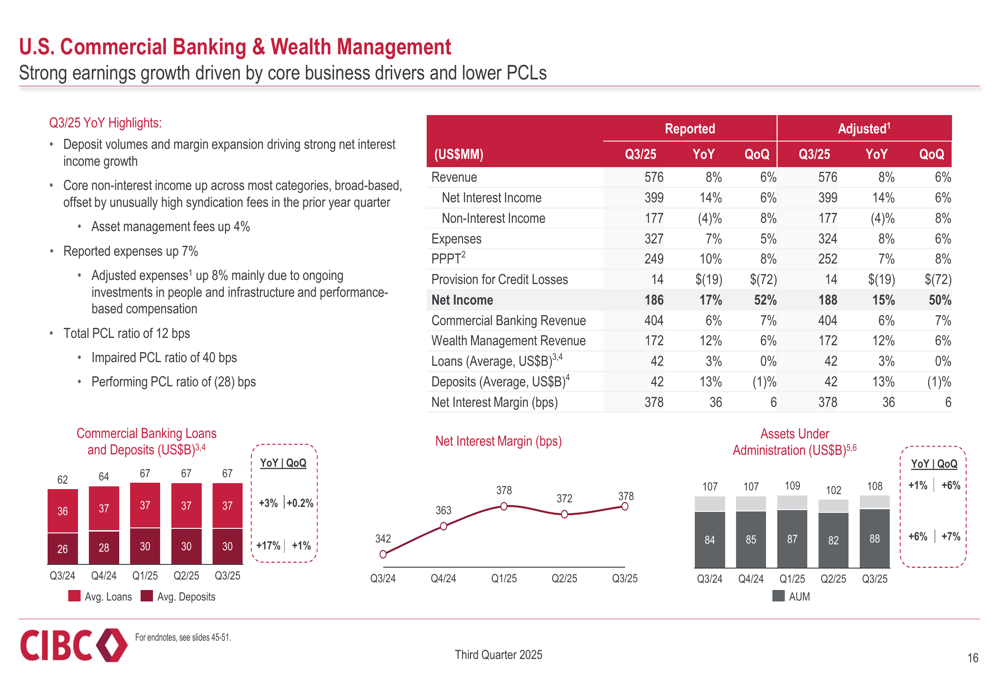

U.S. Commercial Banking & Wealth Management delivered net income of $186 million, up 17% year-over-year, driven by core business growth and lower provisions for credit losses.

Capital Markets showed the most dramatic improvement, with net income surging 87% year-over-year to $540 million, powered by strong growth in both Global Markets and Corporate & Investment Banking activities.

Detailed Financial Analysis

CIBC’s revenue growth was primarily driven by net interest income, which increased by 13% year-over-year (excluding trading). This growth was supported by margin expansion across all major business segments.

The following chart illustrates the bank’s net interest income and margin trends:

Total bank net interest margin (excluding trading) rose by 10 basis points year-over-year to 1.94%. Canadian Personal & Commercial banking NIM increased by 18 basis points to 2.81%, while U.S. Commercial & Wealth NIM saw a significant expansion of 36 basis points to 3.78%.

Non-interest income grew by 4% overall, or 7% excluding trading, with market-related fees (excluding trading) up 19%. However, transactional revenues declined by 6%, primarily due to lower credit fees.

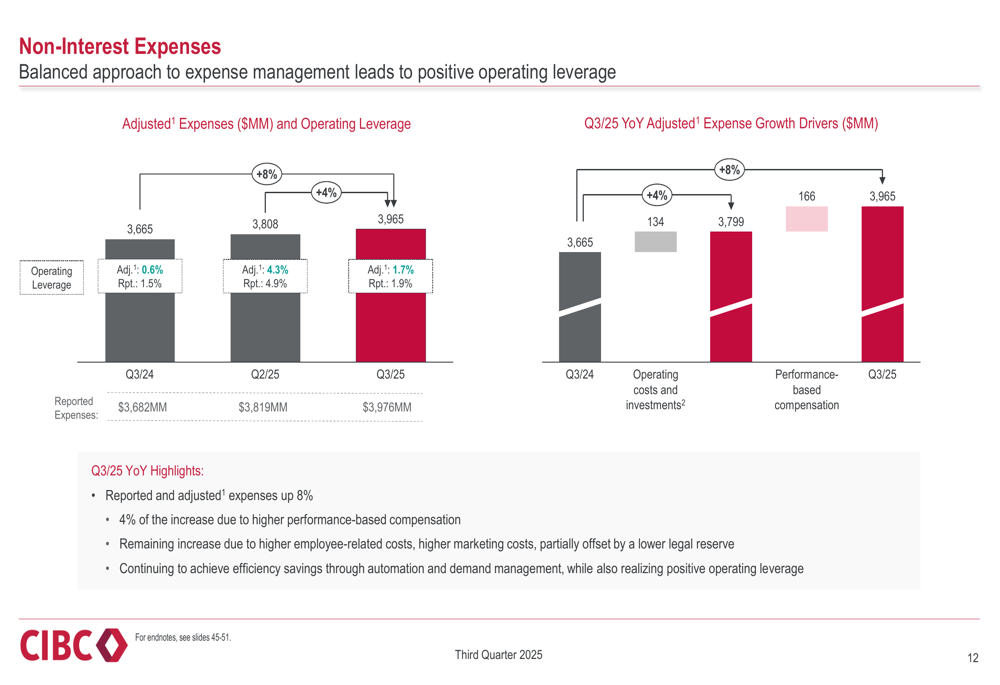

On the expense side, both reported and adjusted expenses increased by 8%, with 4% of this growth attributed to higher performance-based compensation. The remaining increase came from higher employee-related costs and marketing expenses. Despite these increases, CIBC maintained positive operating leverage, demonstrating effective cost management.

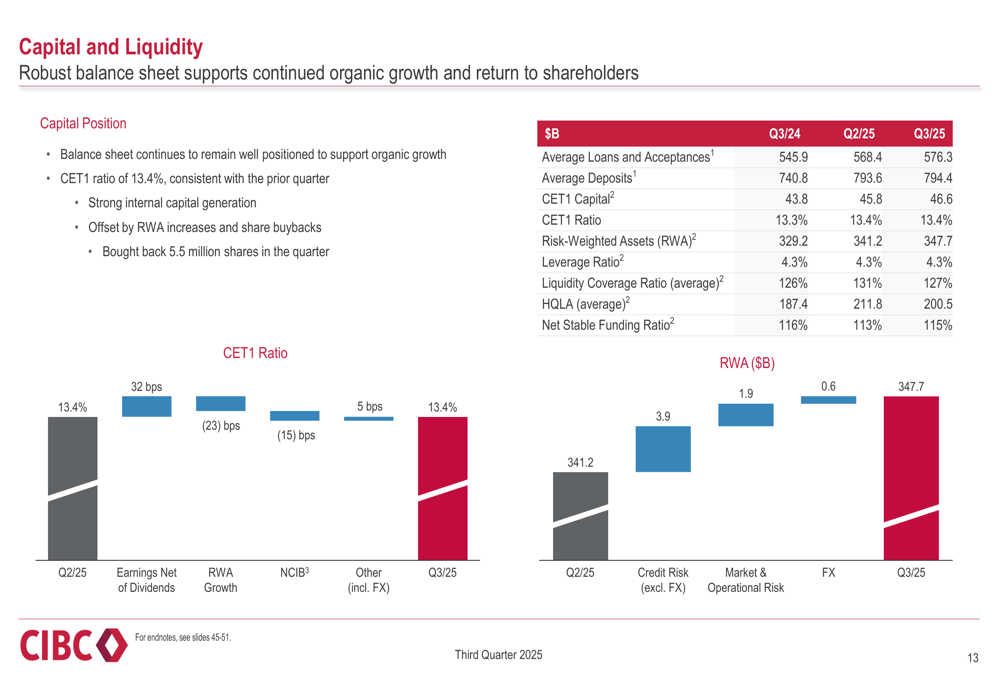

The bank’s balance sheet remains robust, with a CET1 ratio of 13.4%, well above the regulatory requirement of 11.5%. This strong capital position supports organic growth and shareholder returns.

The following slide provides an overview of CIBC’s capital and liquidity position:

Credit quality remains solid, with a total provision for credit losses (PCL) ratio of 38 basis points and an impaired PCL ratio of 33 basis points. The bank’s allowance coverage increased year-over-year from 0.74% to 0.78%, reflecting prudent risk management amid macroeconomic uncertainty.

Strategic Initiatives

CIBC continues to execute its client-focused strategy, with emphasis on growing its mass affluent and private wealth franchise, expanding digital capabilities, and delivering connectivity across business lines.

The following slide outlines key elements of CIBC’s strategy:

Digital transformation remains a priority, with digital registration surpassing 10 million clients and achieving a record-high digital registration rate of 81%. The bank’s AI initiative, CIBC AI (CAI), was recognized as the Best Gen-AI Initiative by The Digital Banker for innovative use of generative AI to enhance employee experience.

Digital adoption and engagement continue to grow, as illustrated in the following trends:

The bank’s lending portfolio maintains a strong risk profile and is well-diversified between consumer (61%) and business & government (39%) segments:

Cross-line-of-business referrals within U.S. Commercial Banking & Wealth Management have shown impressive growth of 25% annualized year-to-date, while U.S. region Capital Markets revenue has increased by 37% year-to-date, demonstrating the effectiveness of CIBC’s connectivity strategy.

Forward-Looking Statements

Looking ahead, CIBC is well-positioned to continue its strong performance, supported by a robust balance sheet and deep client relationships. The bank’s CEO succession transition is progressing well, with strong leadership driving effective execution across all business lines.

Management emphasized three key points for future growth:

1. Results demonstrate continued momentum and consistency amid ongoing global trade uncertainty

2. Relentless client focus and execution mindset with strong performance across all businesses

3. Well-positioned to execute on strategy to deliver relative outperformance through-the-cycle

CIBC’s strong Q3 2025 results build on the momentum seen in Q2, when the bank targeted a medium-term return on equity over 15%. With current ROE at 14.2%, the bank appears to be making steady progress toward this goal.

The bank’s balance sheet strength enables continued growth and capital return to shareholders, while its proactive risk management approach provides coverage for various potential economic outcomes in an uncertain macroeconomic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.