AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Cicor Technologies Ltd (SWX:SIX:CICN) released its half-year 2025 results on July 23, showcasing record sales driven by an aggressive acquisition strategy, though with some pressure on margins due to integration costs. The Swiss electronics manufacturing services (EMS) provider reported that its transformation into a pan-European leader is progressing, with particular strength in the aerospace and defense sector. Despite the positive narrative, Cicor’s stock fell 5.42% to CHF 174.50 following the presentation.

Financial Performance Highlights

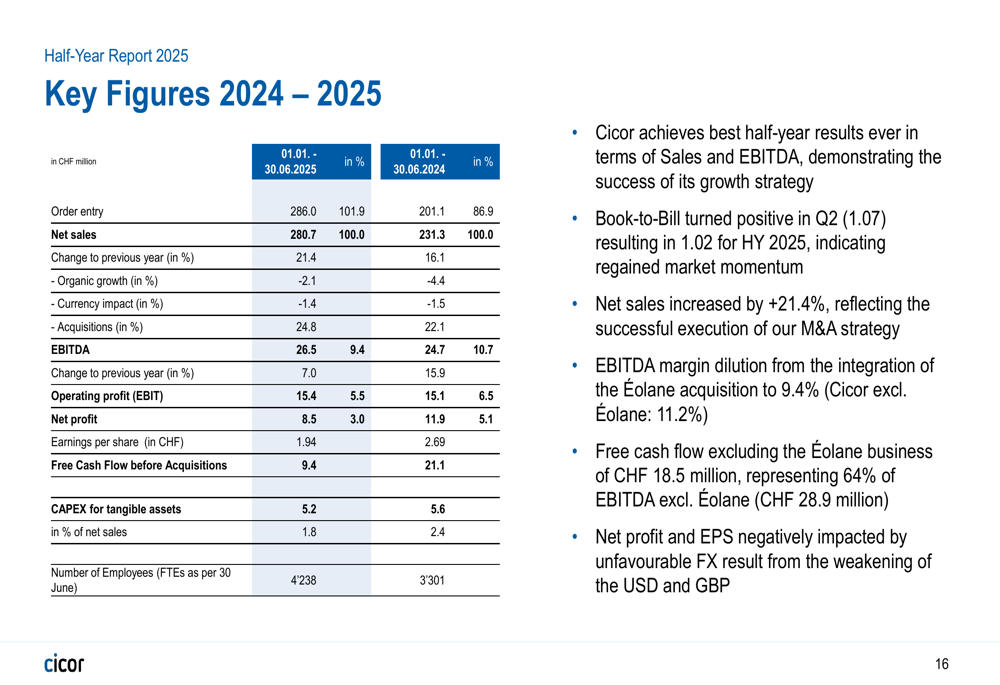

Cicor achieved its highest half-year sales and EBITDA figures in company history, with net sales increasing 21.4% year-over-year to CHF 280.7 million, primarily driven by acquisitions. However, organic growth remained slightly negative at -2.1% for the half-year, though the company highlighted a return to positive organic growth of 0.3% in Q2.

As shown in the following key financial comparison:

EBITDA rose to CHF 26.5 million from CHF 24.7 million in the prior year, but the EBITDA margin contracted to 9.4% from 10.7%. The company emphasized that excluding the effects of the Éolane France integration, the underlying EBITDA margin would have improved to 11.2%, representing a 50 basis point increase year-over-year.

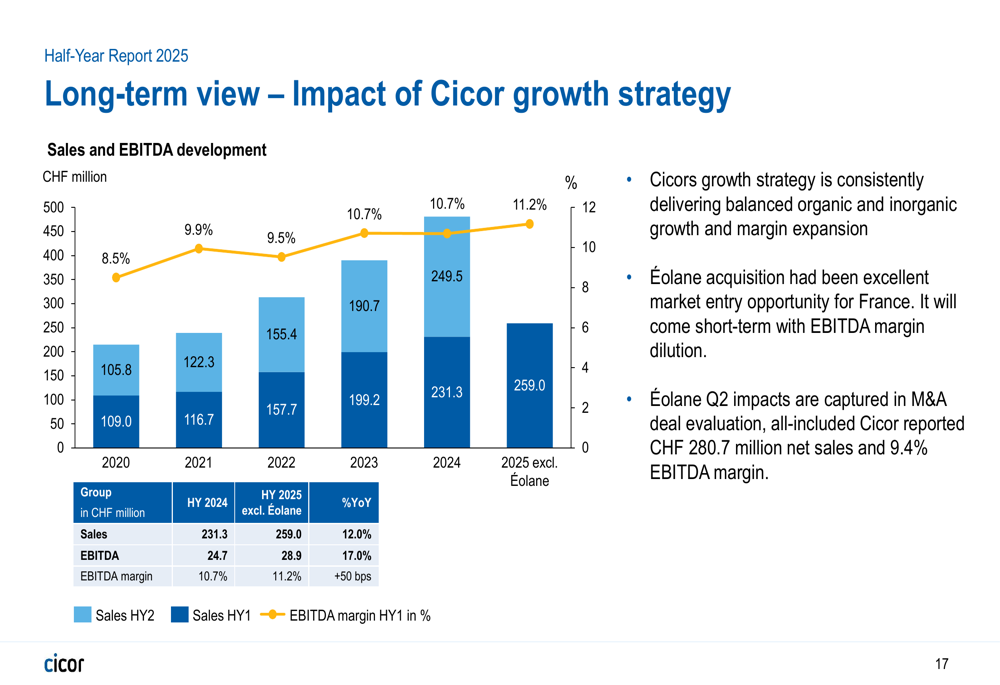

Net profit declined 28.7% to CHF 8.5 million, with earnings per share falling to CHF 1.94 from CHF 2.69. This decline was primarily attributed to unfavorable foreign exchange results and integration costs related to acquisitions. The following chart illustrates the company’s long-term performance trajectory:

The book-to-bill ratio improved to 1.02 from 0.87 in the prior year period, suggesting stronger future revenue potential. Free cash flow before acquisitions was CHF 9.4 million, or CHF 18.5 million when adjusting for the Éolane France integration effects.

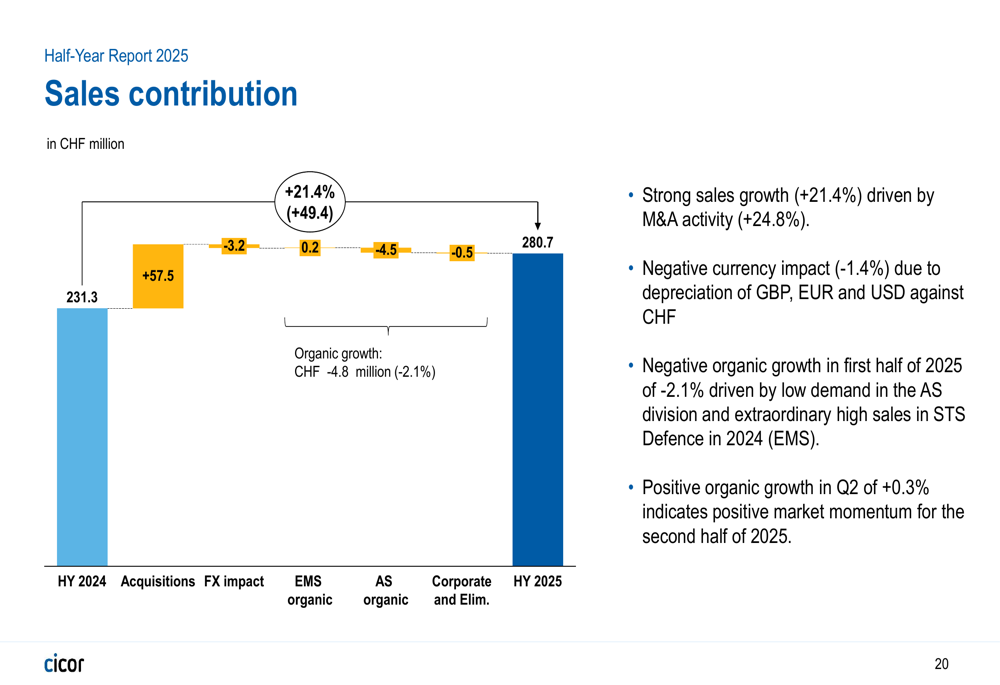

The following chart breaks down the various factors contributing to Cicor’s sales growth:

Acquisition Strategy

Cicor completed three significant acquisitions during the first half of 2025, investing a total of CHF 23.1 million in purchase considerations. These included Profectus Solutions in Germany (adding 90 employees), Éolane France operations in France and Morocco (adding 890 employees), and Mercury International in Switzerland (adding 34 employees).

The Éolane France acquisition was particularly significant, requiring a total cash investment of CHF 15.3 million and establishing Cicor’s presence in France (the second largest market for aerospace and defense applications in Europe) and Morocco. The company noted that while the integration temporarily pressured margins, it expects to progressively improve profitability to Cicor’s standard levels.

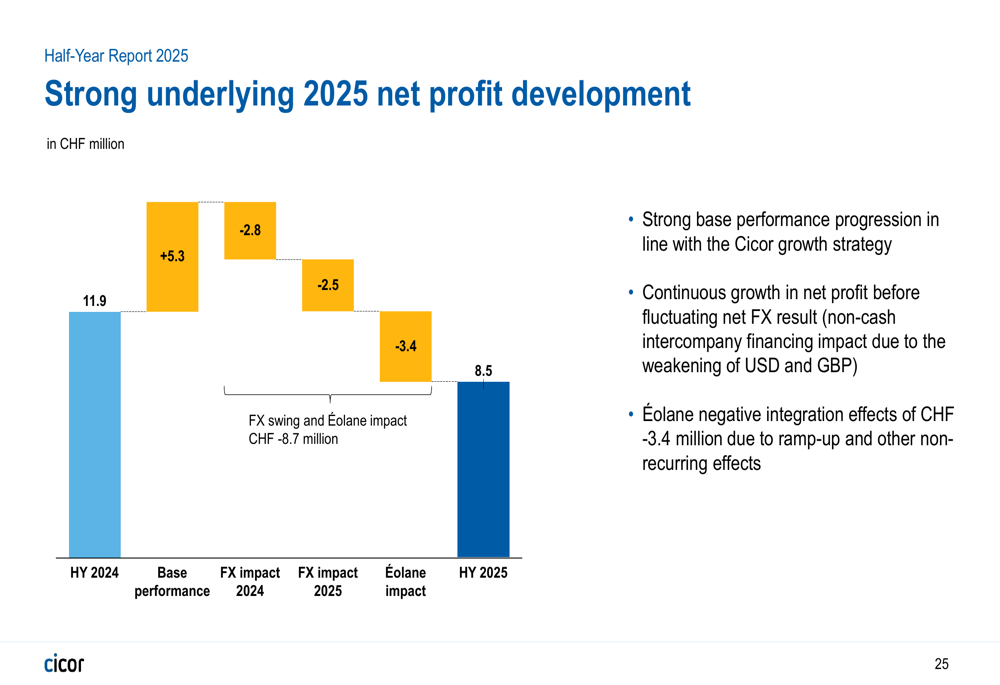

This waterfall chart illustrates how various factors, including the Éolane integration, affected net profit development:

The company has also signed an agreement to acquire MADES in Málaga, Spain, with closing expected in the second half of 2025 subject to regulatory approvals. This acquisition would further strengthen Cicor’s position in the aerospace and defense sector.

Market Positioning

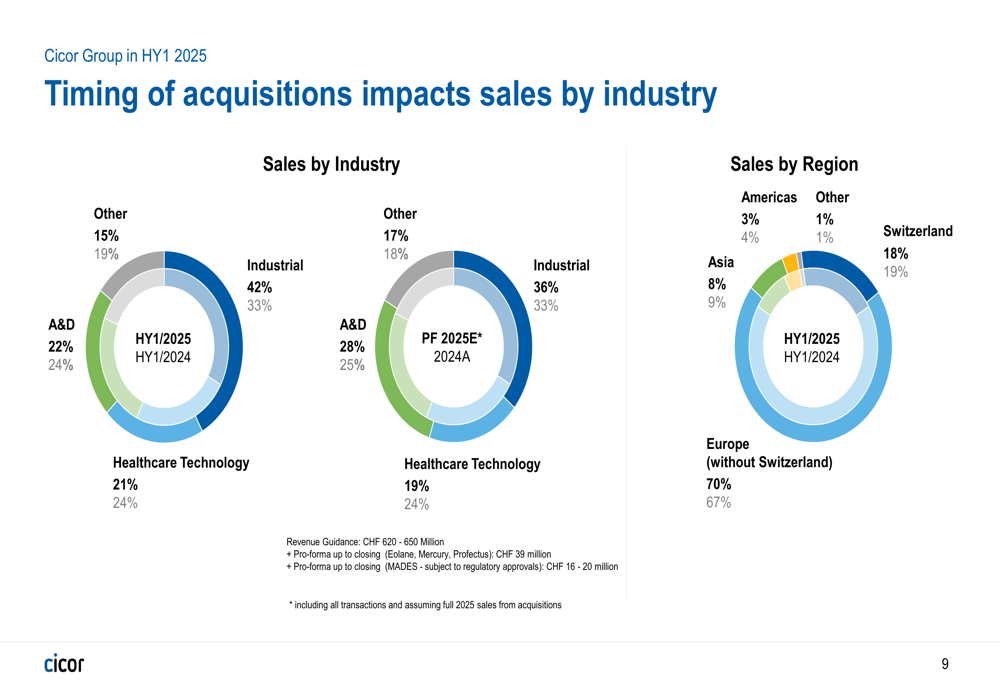

Cicor is strategically focusing on three key markets: Industrial (37% of pro-forma FY 2025 sales), Aerospace & Defense (28%), and Healthcare Technology (19%). The company highlighted its expanding position in the aerospace and defense sector, claiming to be the only EMS company with a pan-European presence in this market.

The following chart shows the distribution of sales by industry and region:

Geographically, Europe (excluding Switzerland) accounts for 70% of sales, followed by Switzerland at 18%, Asia at 8%, and the Americas at 3%. The company’s global footprint now spans 13 countries across Europe and Asia, with recent expansion into Morocco providing an attractive nearshoring location for European customers.

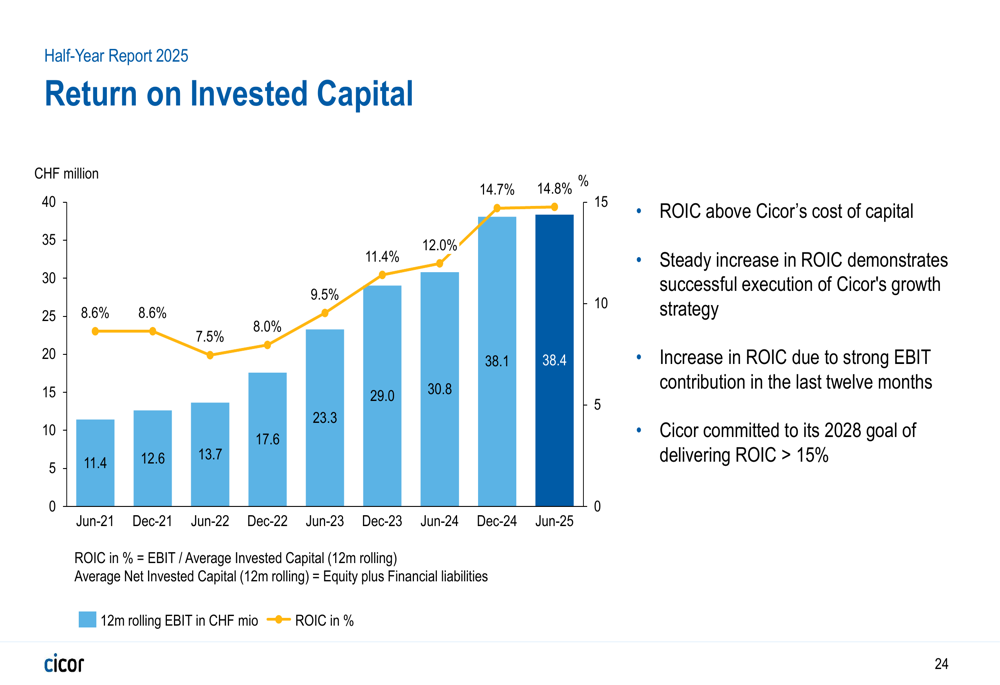

Cicor’s strategic focus on higher-margin sectors appears to be yielding results in terms of return on invested capital (ROIC), which has steadily improved to 14.8% as of June 2025:

Forward-Looking Statements

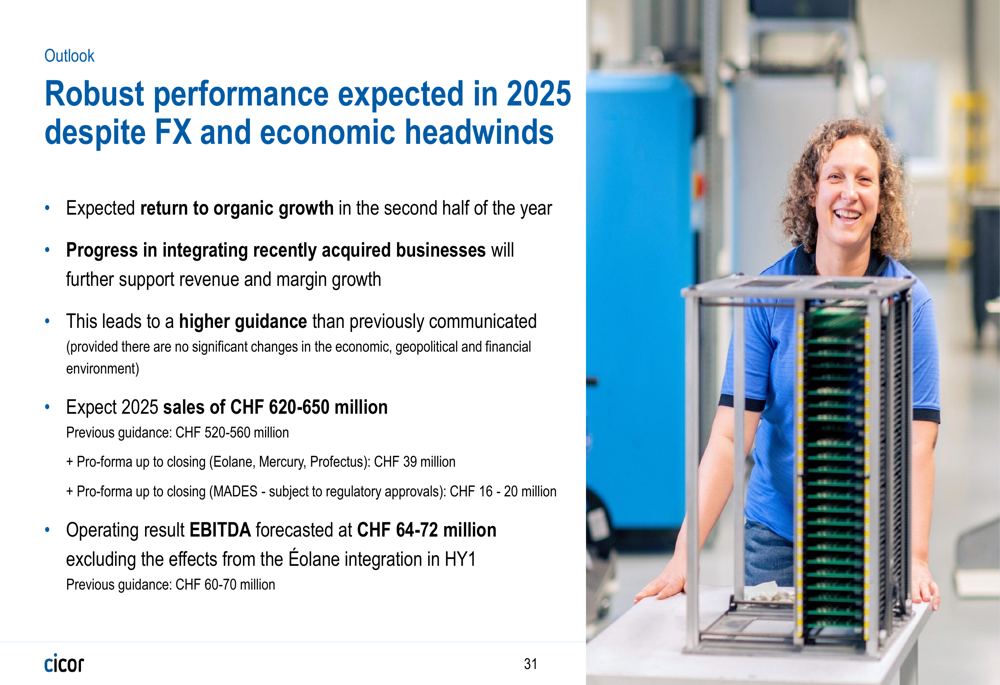

Cicor raised its full-year guidance based on expected order and sales growth and progress in integrating newly acquired businesses. The company now forecasts 2025 sales of CHF 620-650 million and EBITDA of CHF 64-72 million (excluding the effects from the Éolane integration in the first half).

Management expressed confidence in returning to organic growth for the full year and continuing to make progress in integrating recently acquired businesses. The company remains committed to its 2028 vision of becoming "the leading pan-European electronics design and manufacturing partner for healthcare technology, aerospace & defense and industrial" sectors.

Cicor’s financial leverage remains manageable with a net debt to EBITDA ratio of 1.16x, providing room for potential further acquisitions. The company’s market capitalization has more than tripled year-over-year to CHF 712 million, reflecting investor confidence in its growth strategy despite the short-term integration challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.