Piper plays down significance of Tesla Autopilot case in Florida

Introduction & Market Context

Cipher Pharmaceuticals (OTC:CPHRF) Inc. (TSX:CPH | OTCQX:CPHRF) presented its May 2025 investor update highlighting the company’s transformation into what it describes as "a profitable, high-growth specialty pharma company." The presentation, delivered shortly after the company’s Q1 2025 earnings release, showcases Cipher’s strategic focus on North American operations and its recent Natroba acquisition, which has significantly impacted the company’s revenue profile while presenting new challenges to bottom-line performance.

The specialty pharmaceutical company reported Q1 2025 earnings that fell short of analyst expectations, with EPS of $0.10 missing the forecasted $0.14, despite a substantial 105% year-over-year revenue increase. Cipher’s stock has shown resilience, trading at $12.35 as of July 23, 2025, within its 52-week range of $8.55 to $19.69.

Quarterly Performance Highlights

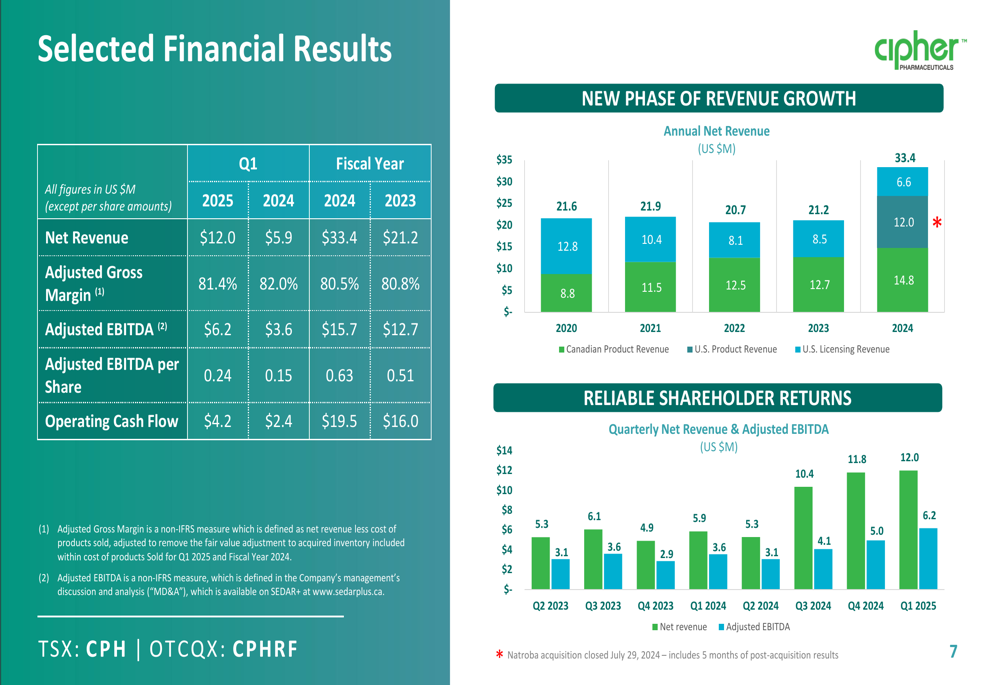

Cipher’s Q1 2025 results demonstrated significant top-line growth, with net revenue reaching $12.0 million, representing a 105% increase from the same period in 2024. The company achieved an adjusted gross margin of 81.4% and adjusted EBITDA of $6.2 million ($0.24 per share). Operating cash flow for the quarter was $4.2 million.

As shown in the following chart of quarterly financial performance:

Despite the impressive revenue growth, the company’s actual EPS of $0.10 fell short of analyst expectations of $0.14, representing a 28.6% miss. Net income dropped to $2.6 million from $4.9 million in Q1 2024, reflecting a decrease in EPS from $0.20 to $0.10 year-over-year.

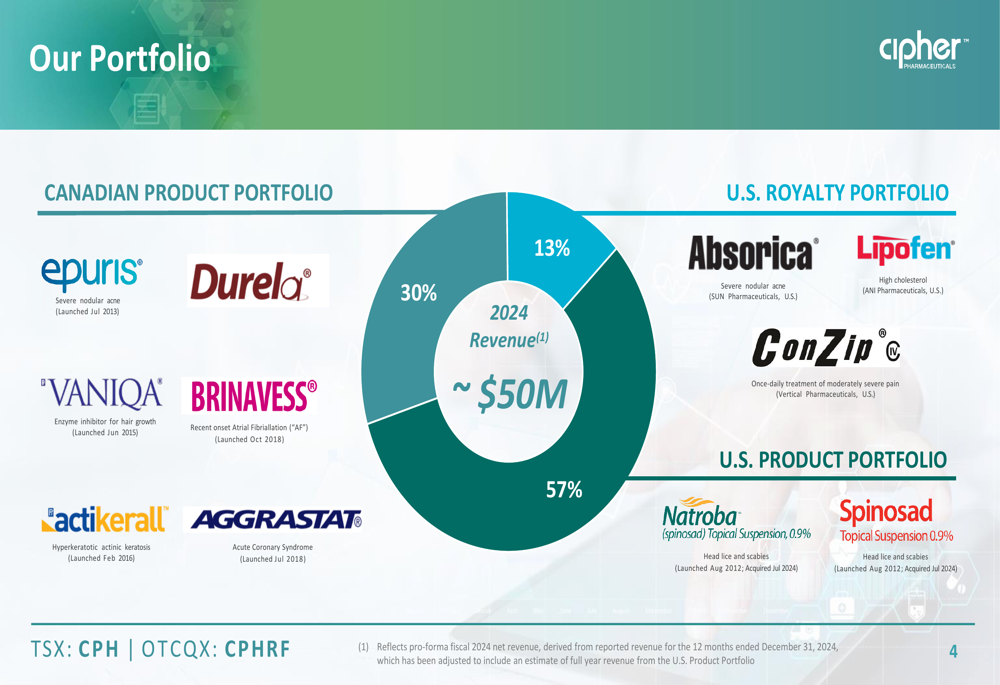

The company’s product portfolio has evolved significantly, with revenue now distributed across Canadian products (30%), US royalty products (13%), and US products (57%), the latter category substantially boosted by the Natroba acquisition.

The following slide illustrates this revenue breakdown:

Strategic Initiatives

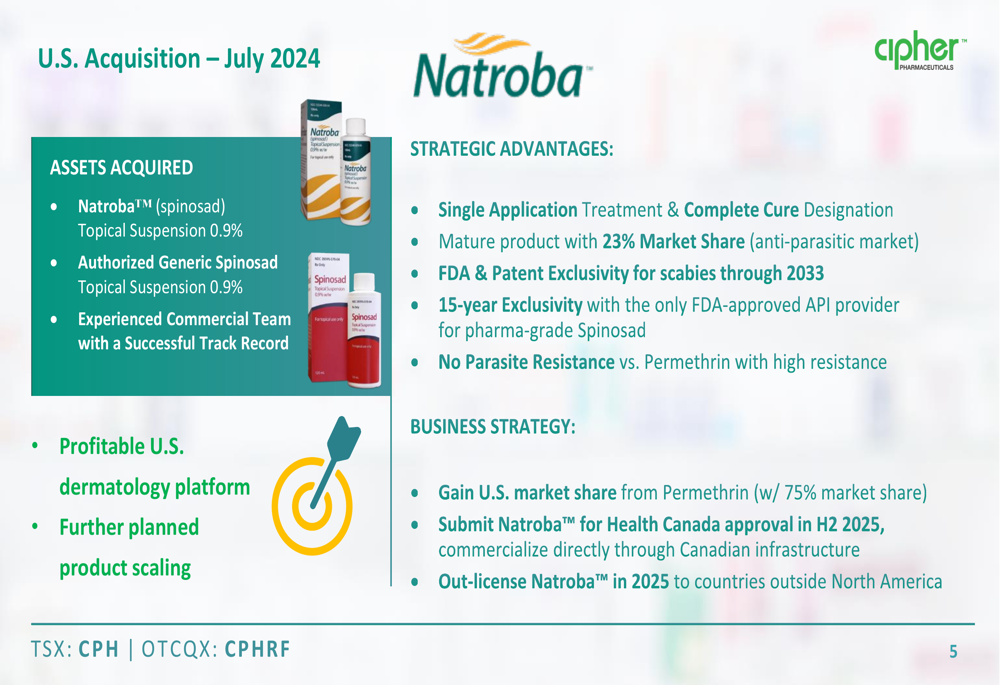

The centerpiece of Cipher’s growth strategy has been the Natroba acquisition, completed in July 2024. This transaction has transformed the company’s revenue profile, with US products now representing the majority of revenue.

Natroba (spinosad) Topical Suspension 0.9% is positioned as a differentiated treatment in the anti-parasitic market with several competitive advantages, including single application treatment, complete cure designation from the FDA, patent exclusivity for scabies through 2033, and no parasite resistance compared to the market-leading permethrin-based treatments.

The following slide details the strategic rationale behind the Natroba acquisition:

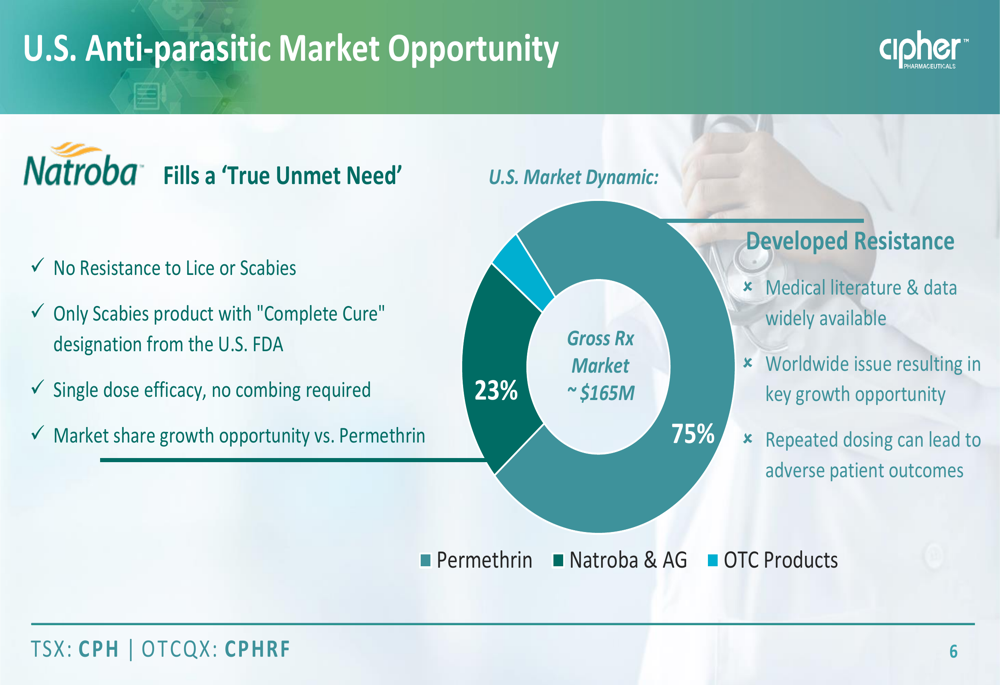

Cipher’s management sees significant growth potential for Natroba in the $165 million US anti-parasitic market, where it currently holds 23% market share compared to permethrin’s dominant 75%. The company plans to gain market share from permethrin-based products, which face increasing parasite resistance issues.

The market opportunity is illustrated in this slide:

During the earnings call, CEO Craig Mao emphasized the company’s strategic focus on the US market, stating, "Our first priority is The U.S. where we’ve got the existing infrastructure." The company also reported that Natroba has been positioned as a preferred Medicaid product in Illinois, with plans to expand this status to other states.

Detailed Financial Analysis

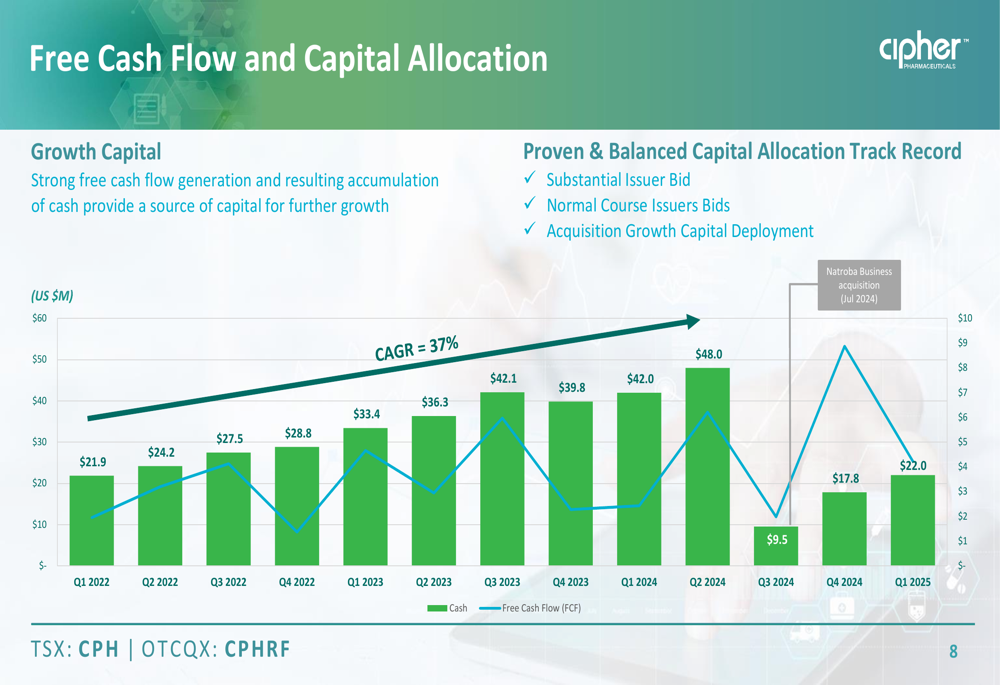

Cipher’s financial position shows a company in transition, with strong revenue growth accompanied by significant investments in future expansion. The company has demonstrated prudent capital management, reducing its debt from $40 million to $25 million while maintaining substantial liquidity for future acquisitions.

Free cash flow has shown impressive growth with a 37% CAGR, as illustrated in the following chart:

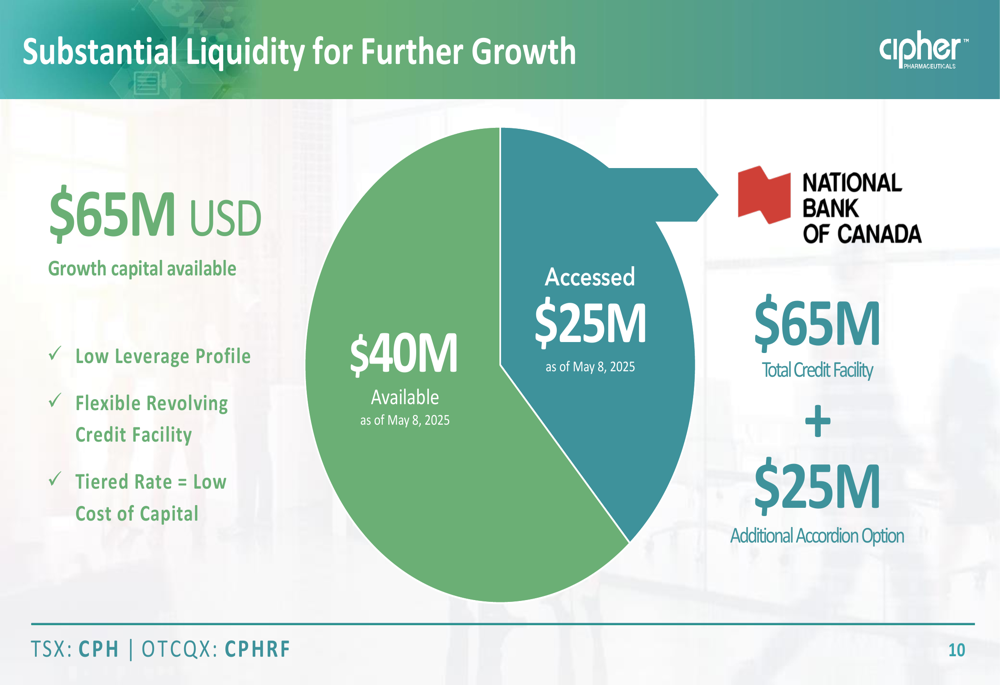

The company maintains access to a $65 million total credit facility, with $40 million available as of May 8, 2025. This financial flexibility positions Cipher to pursue additional acquisitions while maintaining a leverage ratio below 1.5x earnings.

The company’s liquidity position is detailed in this slide:

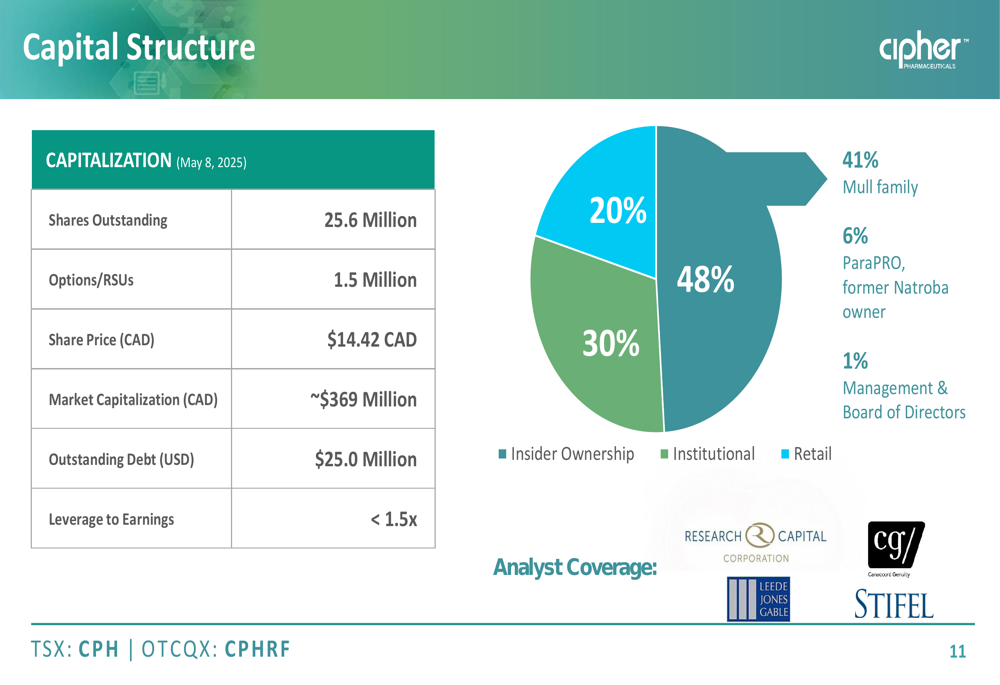

Cipher’s capital structure includes 25.6 million shares outstanding, with a market capitalization of approximately $369 million CAD. Ownership is concentrated, with the Mull family controlling 41%, ParaPRO (former Natroba owner) holding 6%, and management and board members owning 1%.

Forward-Looking Statements

Cipher has outlined six growth levers for future expansion, including maximizing market share for lead products, out-licensing existing products internationally, in-licensing complementary dermatology products, cross-pollinating products between Canada and the US, pursuing add-on acquisitions, and considering opportunistic acquisitions of non-complementary portfolios with strategic value.

The company’s growth strategy is summarized in this slide:

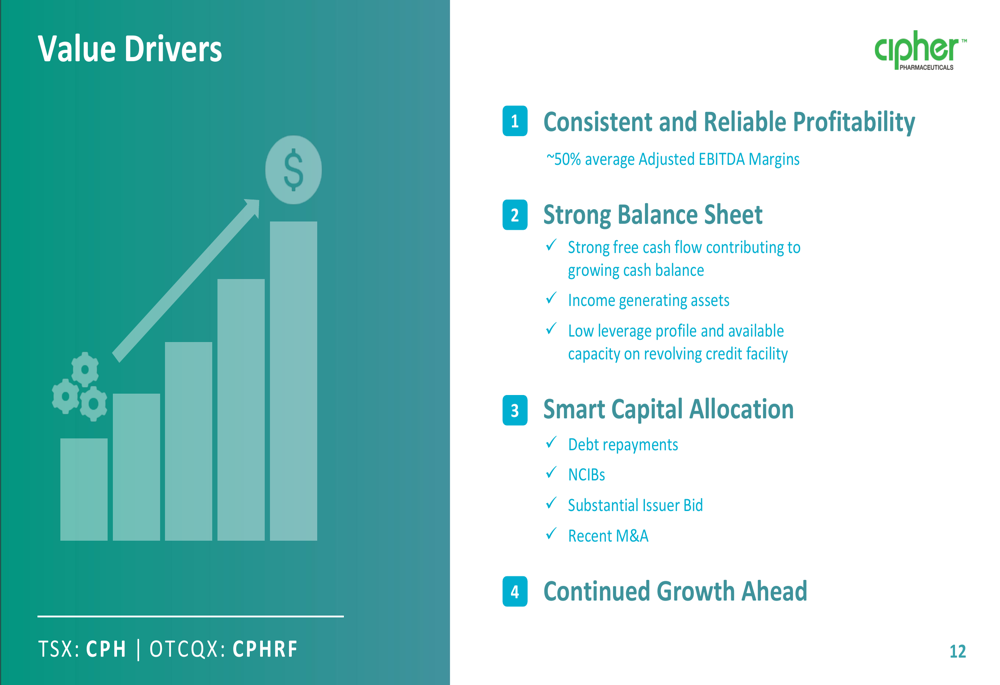

Management has identified several value drivers that underpin their optimistic outlook, including consistent profitability with approximately 50% average adjusted EBITDA margins, a strong balance sheet with growing free cash flow, and a track record of smart capital allocation.

Competitive Industry Position

Cipher positions itself as a specialty pharmaceutical company with a focused approach to the North American market. The company operates with direct product sales in Canada and a combination of product sales and royalties in the United States.

The company’s operational model is illustrated in this slide:

In the anti-parasitic market, Cipher’s Natroba product faces both challenges and opportunities. While permethrin-based treatments dominate with 75% market share, their effectiveness is increasingly compromised by parasite resistance. Natroba’s positioning as the only scabies product with "complete cure" designation from the FDA and its single-dose efficacy provide competitive advantages that Cipher believes will drive market share gains.

However, the company faces risks including market saturation, potential economic pressures affecting healthcare budgets, and regulatory challenges in expanding Medicaid preferred status beyond Illinois.

Conclusion

Cipher Pharmaceuticals’ May 2025 investor presentation portrays a company in transition, with the Natroba acquisition driving substantial revenue growth while creating short-term pressure on earnings. The company’s strategic focus on the North American specialty pharmaceutical market, particularly in dermatology, provides a clear direction for future growth.

While the Q1 2025 earnings miss raises questions about profitability in the near term, the company’s strong cash flow generation, reduced debt, and available liquidity position it well for both organic growth and potential acquisitions. Investors will be watching closely to see if Cipher can translate its impressive top-line growth into improved bottom-line performance in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.