Hedge funds are buying these two big tech stocks while selling two rivals

Introduction & Market Context

Cirrus Logic (NASDAQ:CRUS) released its investor relations presentation on November 4, 2025, showcasing solid financial performance for the second quarter of fiscal year 2026 alongside strategic initiatives aimed at expanding its product portfolio and addressable markets. The Austin, Texas-based semiconductor company reported revenue growth both sequentially and year-over-year, despite its significant reliance on a single customer.

The presentation comes as Cirrus Logic's stock experienced downward pressure, falling 1.22% in regular trading to $129.64 and an additional 2.34% in aftermarket trading, despite the company beating earnings expectations with an EPS of $2.83 against a forecast of $2.07.

Quarterly Performance Highlights

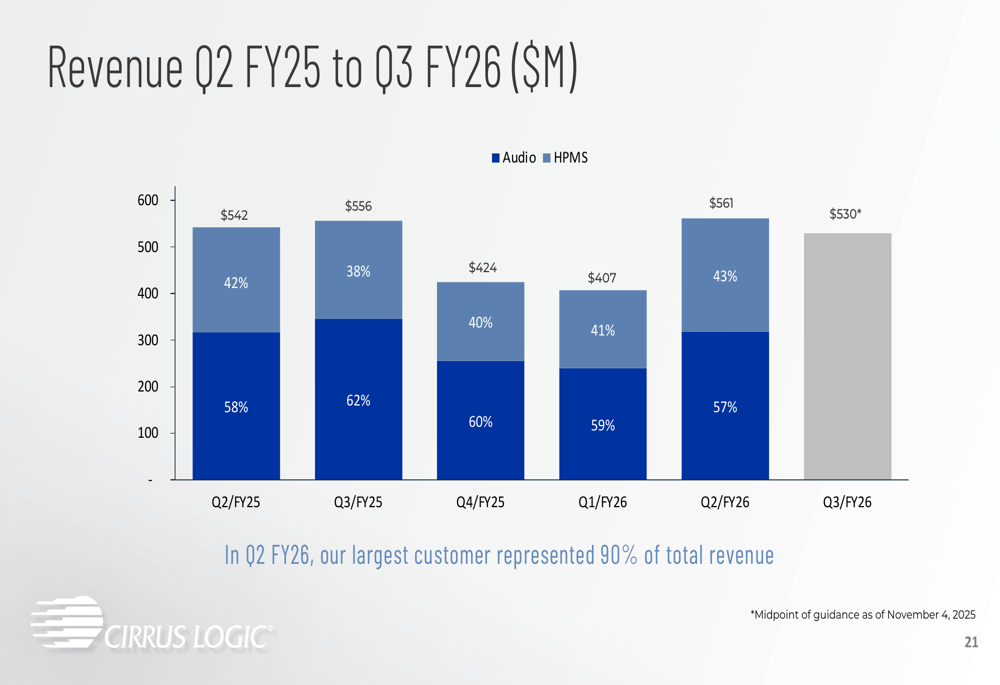

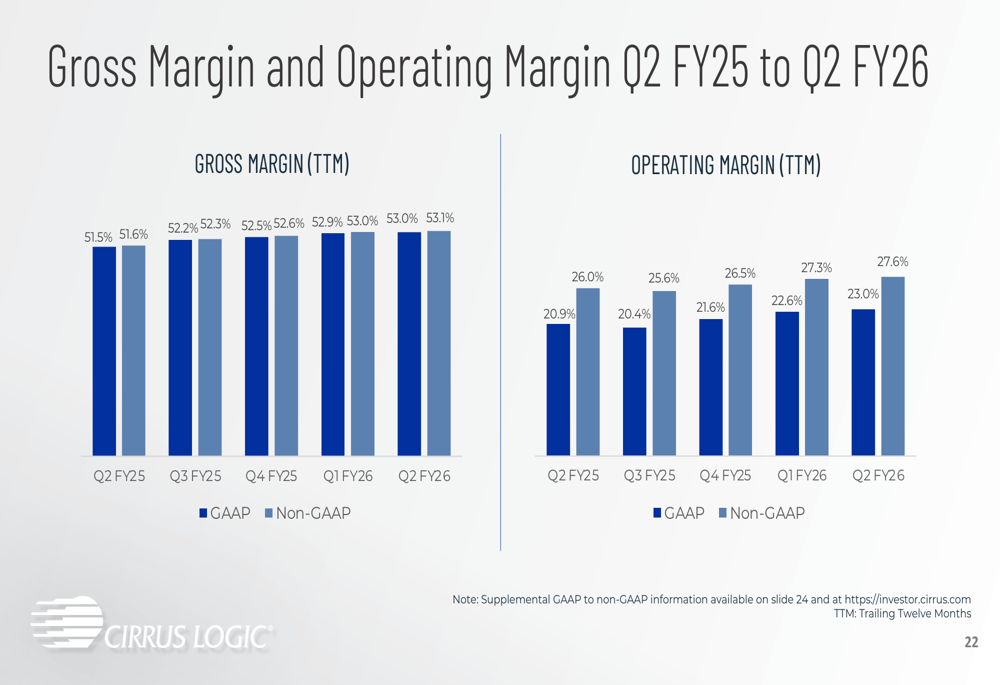

Cirrus Logic reported Q2 FY26 revenue of $561.0 million, representing a 4% increase from the $542 million recorded in the same quarter last year. The company maintained a healthy gross margin of 52.5% while achieving combined R&D and SG&A expenses of $149.6 million.

As shown in the following revenue breakdown:

The company's product mix continues to evolve, with high-performance mixed-signal (HPMS) products growing to represent 43% of total revenue in Q2 FY26, up from 42% in Q2 FY25. This shift reflects Cirrus Logic's strategic push to diversify beyond its traditional audio business.

Notably, Cirrus Logic's financial performance shows consistent margin improvement over the trailing twelve months, with non-GAAP gross margin increasing from 51.6% in Q2 FY25 to 53.1% in Q2 FY26, and non-GAAP operating margin expanding from 26.0% to 27.6% over the same period.

Strategic Initiatives

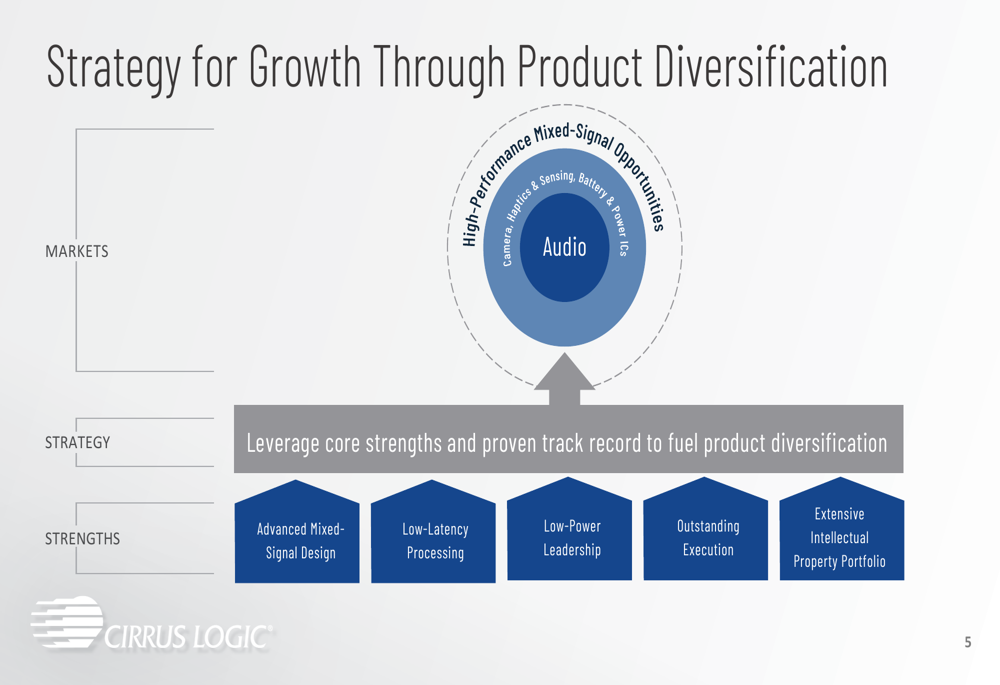

The company's presentation emphasized its three-pronged growth strategy: maintaining leadership in smartphone audio, increasing HPMS content in smartphones, and leveraging its core technologies to expand into additional applications and markets.

Cirrus Logic's diversification strategy is illustrated in this strategic overview:

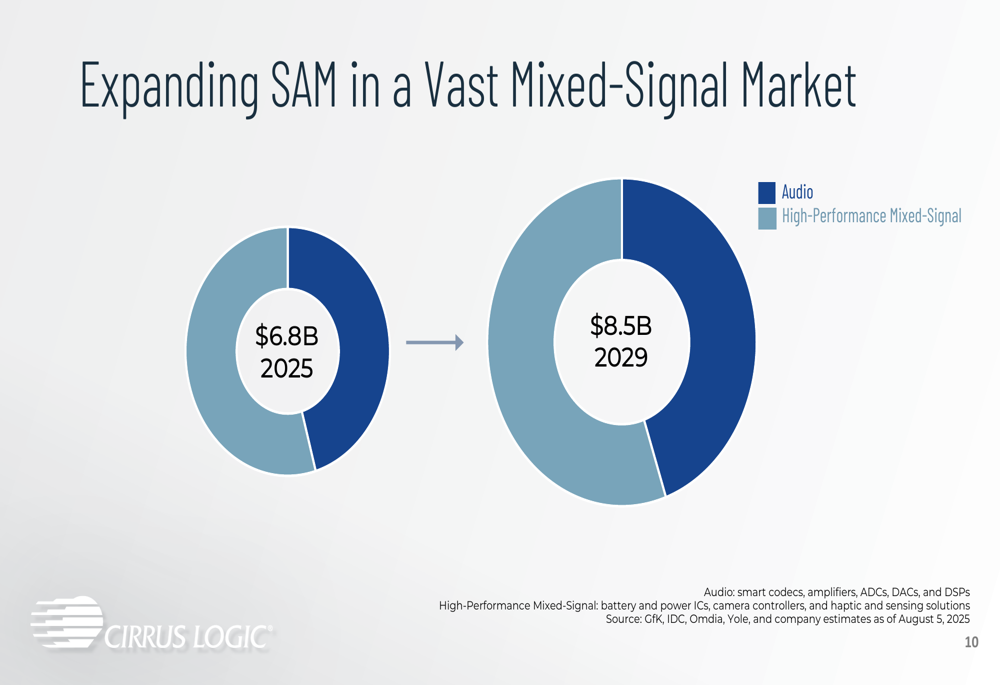

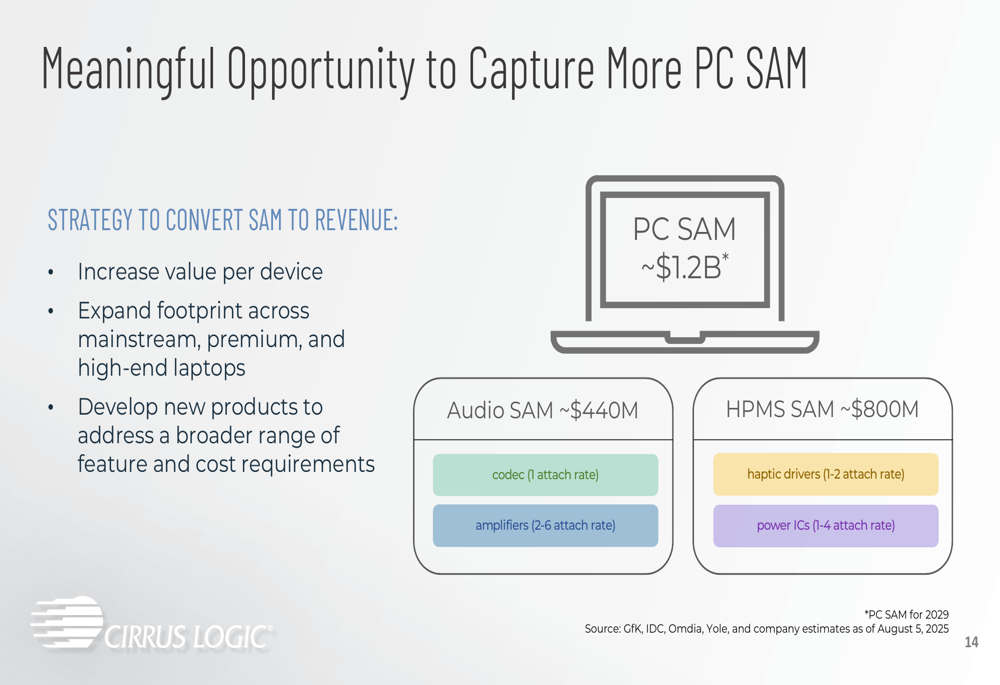

A key focus for future growth is expanding the company's serviceable addressable market (SAM), which is projected to grow from $6.8 billion in 2025 to $8.5 billion by 2029. This expansion is driven by both audio products (smart codecs, amplifiers) and high-performance mixed-signal solutions (battery and power ICs, camera controllers, haptic and sensing solutions).

The PC market represents a particularly significant growth opportunity, with Cirrus Logic targeting a SAM of approximately $1.2 billion by 2029. The company's strategy involves increasing value per device, expanding its footprint across laptop segments, and developing new products to address varying feature and cost requirements.

During the earnings call, CEO John Forsyth highlighted the company's progress in the PC market, stating, "We are making excellent progress here, especially in the PC market." This aligns with the presentation's emphasis on broadening content beyond smartphones into PCs, tablets, wearables, gaming, and AR/VR applications.

Financial Outlook

For Q3 FY26, Cirrus Logic provided revenue guidance of $500 million to $560 million with an expected gross margin between 51% and 53%. Combined R&D and SG&A expenses are projected to be between $151 million and $157 million.

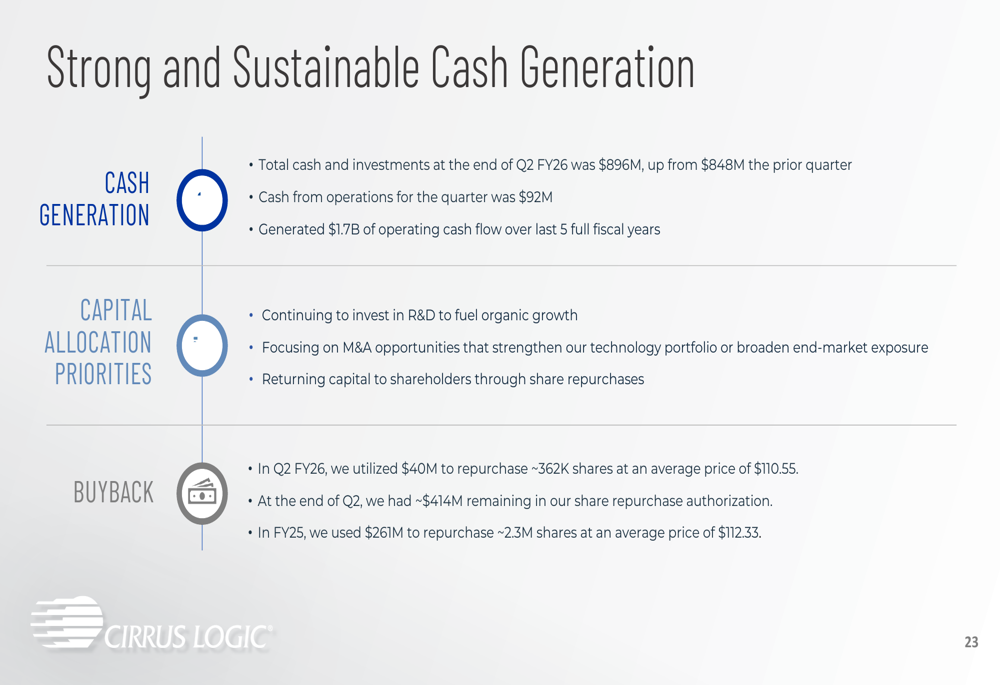

The company's cash position remains strong, with total cash and investments reaching $896 million at the end of Q2 FY26, up from $848 million in the previous quarter. Cash from operations for the quarter was $92 million, contributing to the $1.7 billion in operating cash flow generated over the last five fiscal years.

Cirrus Logic continues to return capital to shareholders through its share repurchase program. In Q2 FY26, the company utilized $40 million to repurchase approximately 362,000 shares at an average price of $110.55, with $414 million remaining in its repurchase authorization at quarter's end.

Challenges and Risks

Despite strong financial performance, Cirrus Logic faces significant customer concentration risk, with its largest customer representing 90% of total revenue in Q2 FY26. While not explicitly named in the presentation, this customer is widely understood to be Apple.

The company's guidance for Q3 FY26 suggests potential sequential revenue decline from Q2's $561 million to a midpoint of $530 million, which could explain some of the negative market reaction despite the earnings beat.

Additionally, Cirrus Logic operates in highly competitive markets where technological innovation moves rapidly. The company's continued success depends on its ability to execute its diversification strategy and maintain technological leadership in both audio and high-performance mixed-signal products.

Market Reaction

Despite exceeding analyst expectations with an EPS of $2.83 (36.71% above the forecast) and revenue 3.8% higher than anticipated, Cirrus Logic's stock declined following the earnings release. This disconnect between financial performance and stock movement may reflect broader market trends or investor concerns about the company's high customer concentration and potential sequential revenue decline in the coming quarter.

The stock closed at $128.17 in aftermarket trading on November 4, 2025, down from the previous close of $131.24, suggesting investors may be focusing on forward guidance rather than current results.

In conclusion, Cirrus Logic's Q2 FY26 presentation portrays a company with solid financial performance and a clear strategic vision for diversification and growth. However, challenges remain in reducing customer concentration and maintaining growth momentum in an increasingly competitive semiconductor landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.