JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

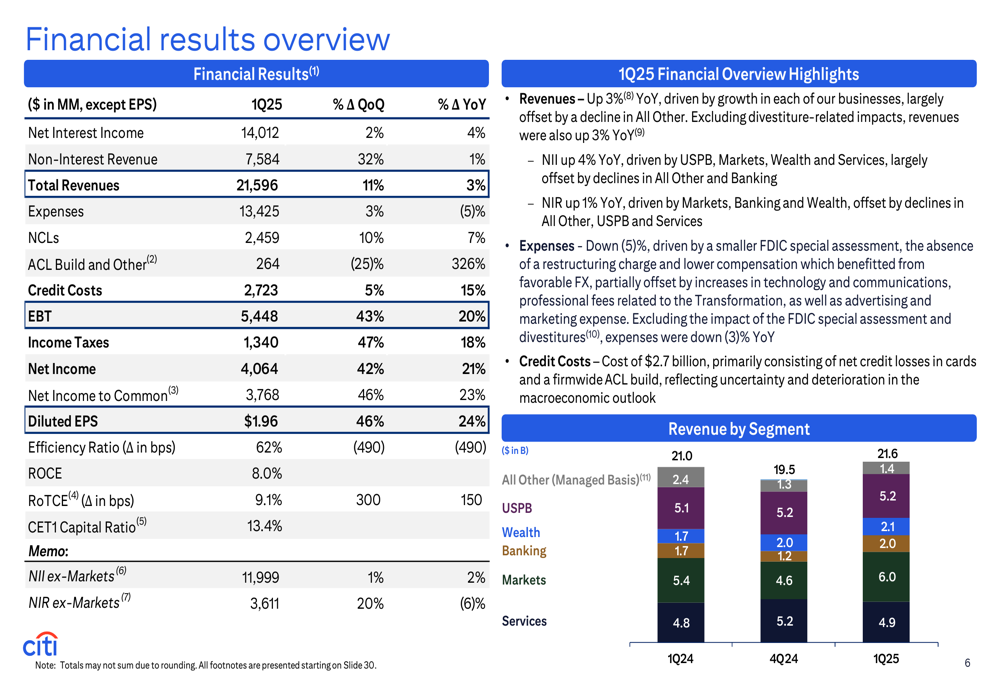

Citigroup Inc. (NYSE:C) released its first quarter 2025 earnings presentation on April 15, 2025, revealing better-than-expected results that drove its stock price up 4.03% to $65.77. The banking giant reported earnings per share (EPS) of $1.96, exceeding analysts’ forecast of $1.86, while revenue reached $21.6 billion, surpassing the expected $21.3 billion.

The strong performance comes amid Citigroup’s ongoing transformation efforts and strategic focus on its five interconnected businesses, which have collectively delivered positive operating leverage for the fourth consecutive quarter. The bank’s disciplined approach to expense management and capital return to shareholders appears to be resonating with investors, as the stock trades significantly higher than its 52-week low of $53.51, though still below its 52-week high of $84.74.

Quarterly Performance Highlights

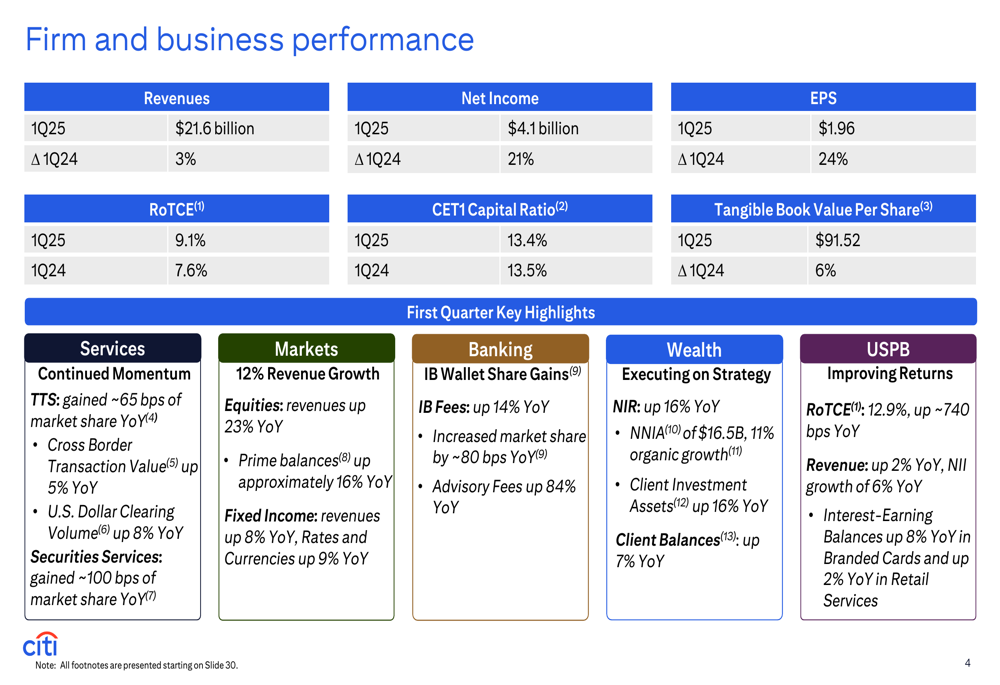

Citigroup’s Q1 2025 results demonstrated broad-based strength across its business segments, with notable improvements in profitability metrics. Net income rose 21% year-over-year to $4.1 billion, while the Return on Tangible Common Equity (RoTCE) improved to 9.1%, up approximately 150 basis points from the previous year.

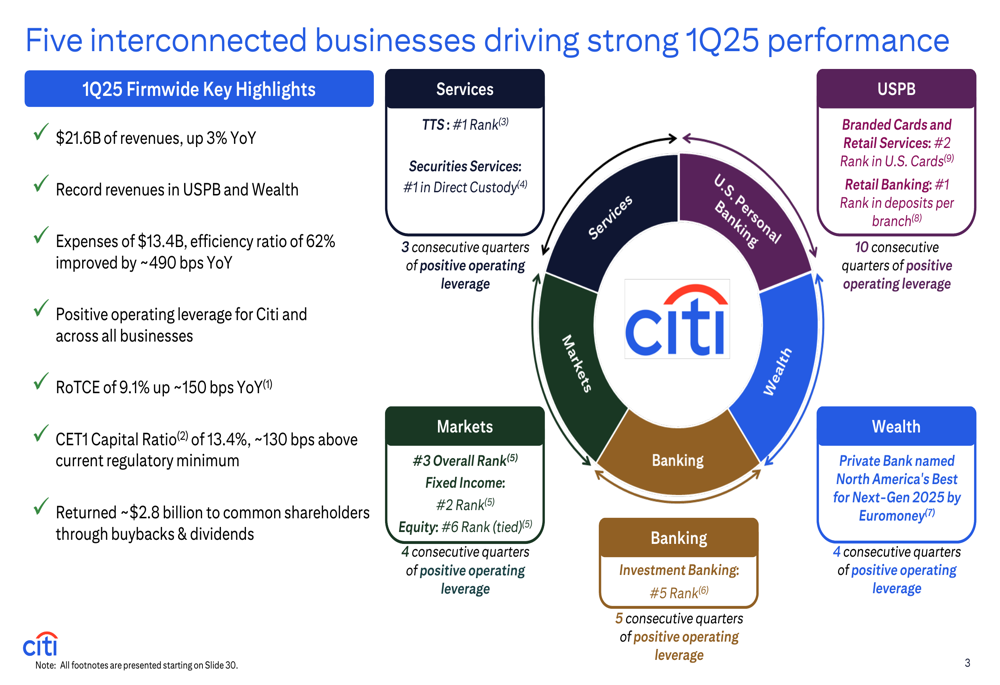

As shown in the following overview of the firm’s interconnected businesses and their performance:

The bank’s efficiency ratio improved significantly to 62%, representing an enhancement of approximately 490 basis points year-over-year. This improvement reflects the company’s disciplined expense management, with total expenses declining 5% compared to the same period last year.

Citigroup’s business segments each contributed to the overall strong performance:

- Services: Revenues up 3% with Treasury and Trade Solutions (TTS) showing continued momentum

- Markets: Revenues up 12%, with fixed income up 8% and equities up 23%

- Banking: Revenues up 12%, with M&A revenue nearly doubling

- Wealth: Revenues up 24% with growth across all three businesses

- U.S. Personal Banking (USPB): Revenues up 2%, driven by branded cards and retail banking

The detailed breakdown of the firm’s performance metrics illustrates the strength across business lines:

Strategic Initiatives

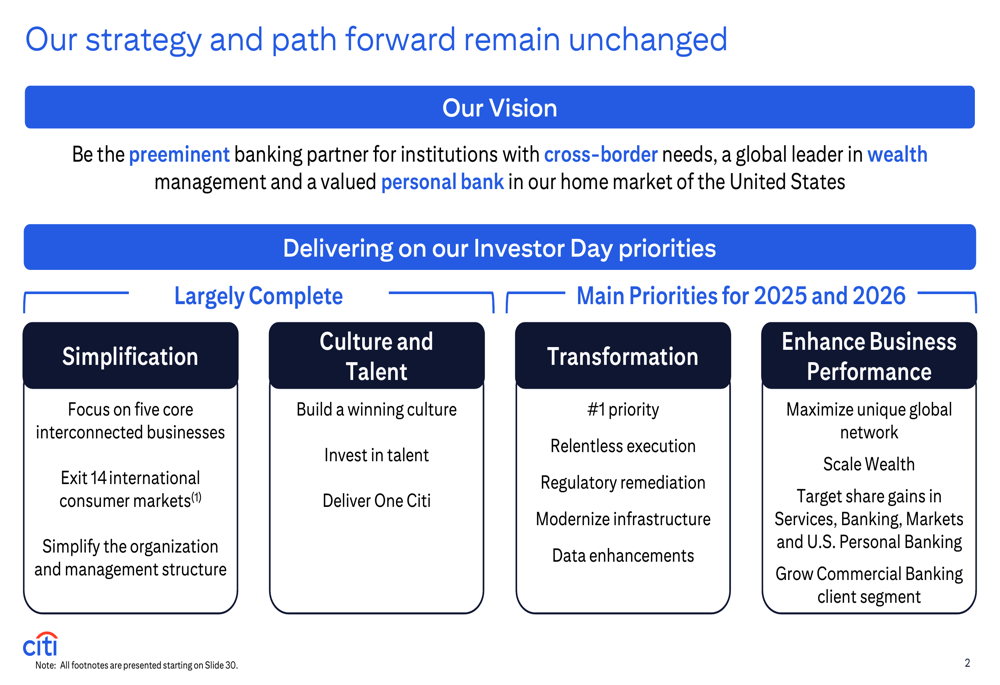

Citigroup continues to execute on its strategic vision to become "the preeminent banking partner for institutions with cross-border needs, a global leader in wealth management, and a valued personal bank in the US." The presentation highlighted the bank’s progress on its key strategic priorities:

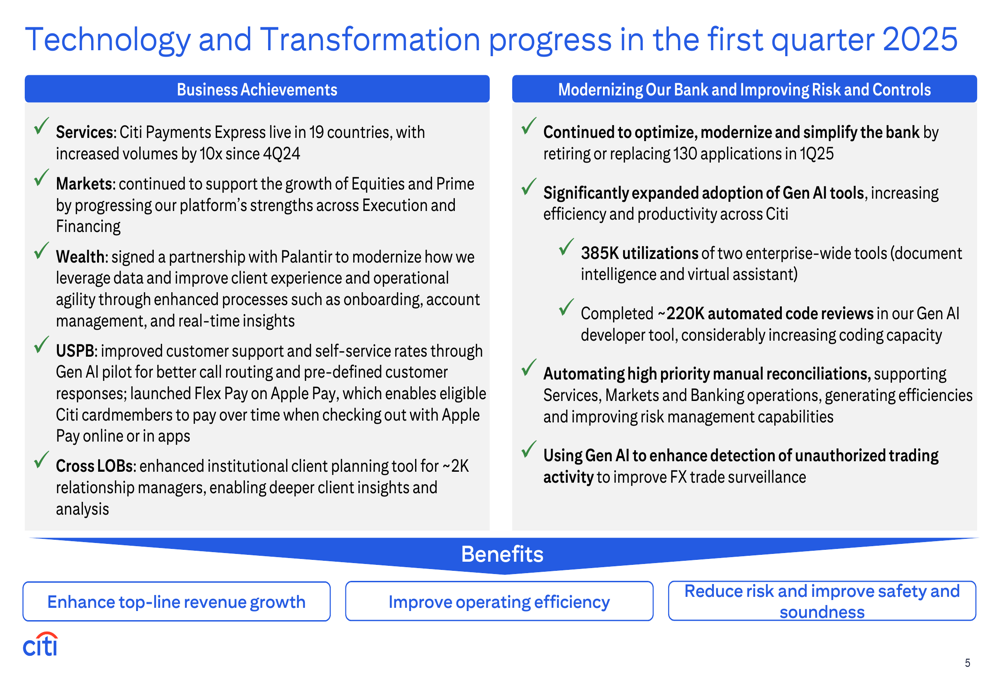

Technology transformation remains a top priority for Citigroup, with significant investments in modernizing infrastructure, enhancing data capabilities, and implementing AI solutions. The bank reported several technology achievements in Q1 2025, including the expansion of Citi Payments Express to 19 countries and the launch of AI-powered customer support tools.

As demonstrated in the technology and transformation progress slide:

During the earnings call, CEO Jane Fraser emphasized Citigroup’s position as "a port during the storm" for clients navigating global economic uncertainty. Fraser highlighted the bank’s deep knowledge and breadth of capabilities from decades of local market presence as key differentiators when serving clients, particularly those reconfiguring supply chains or addressing hedging and funding approaches.

Detailed Financial Analysis

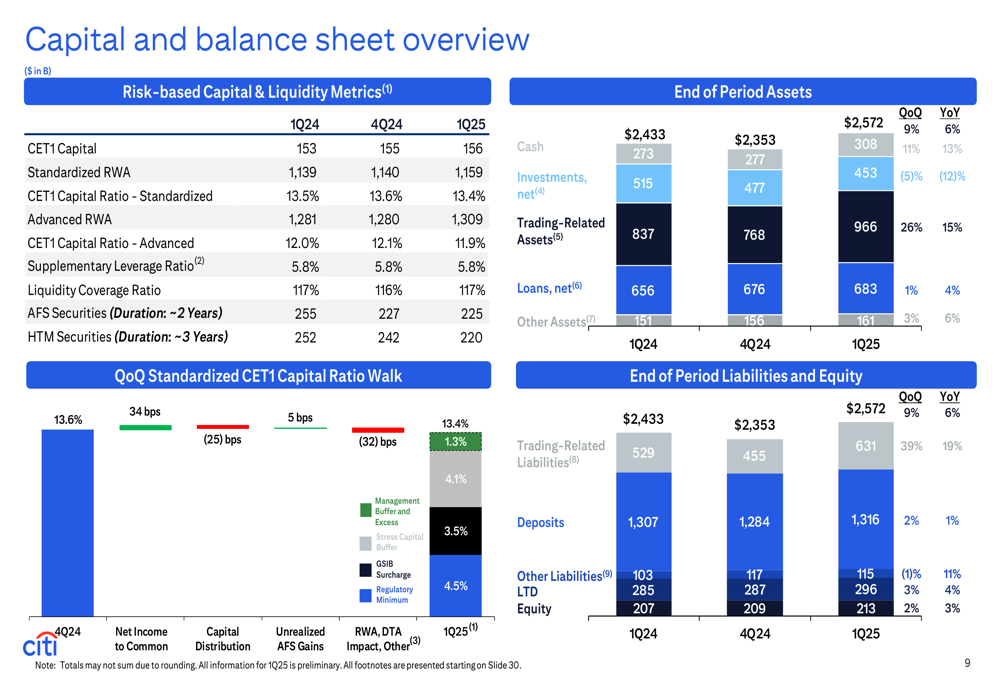

Citigroup’s financial results show improvements across key metrics, with the bank maintaining a strong capital and liquidity position. The CET1 Capital Ratio stood at 13.4%, approximately 130 basis points above the current regulatory minimum.

The following financial overview provides a comprehensive look at the bank’s performance:

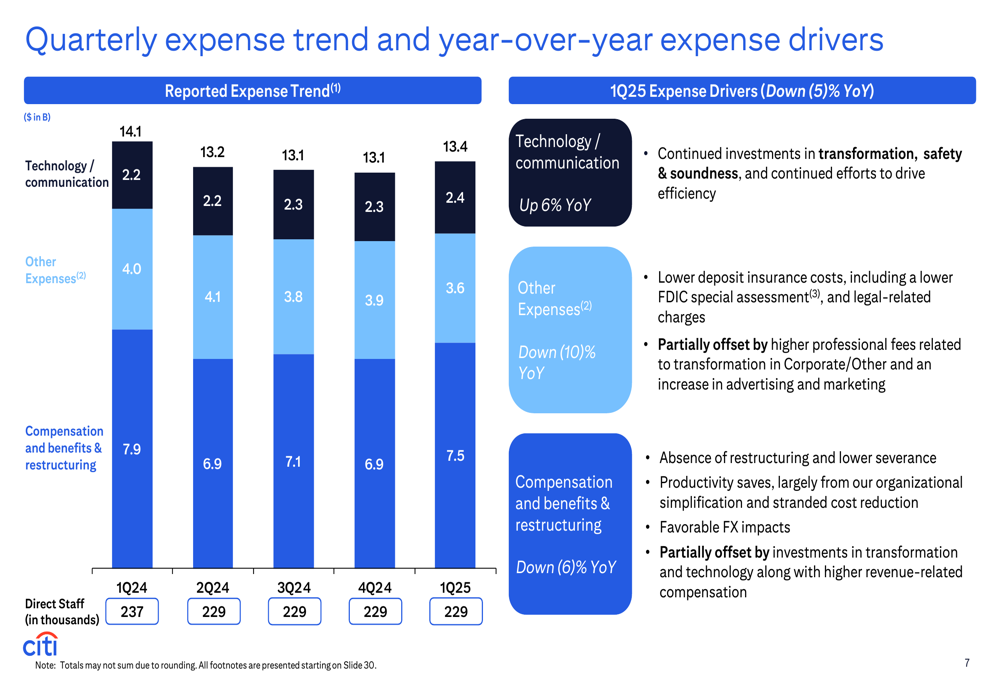

Expense management has been a key focus area, with the bank reducing expenses by 5% year-over-year. The expense reduction was driven by lower deposit insurance costs, the absence of restructuring charges, and lower compensation costs, partially offset by continued investments in transformation and technology.

The quarterly expense trend illustrates this disciplined approach:

Citigroup’s capital position remains strong, with the bank returning approximately $2.8 billion to shareholders during the quarter, including $1.75 billion in share repurchases as part of its $20 billion buyback program. The tangible book value per share increased 6% year-over-year to $91.52.

The capital and balance sheet overview demonstrates the bank’s solid financial foundation:

Forward-Looking Statements

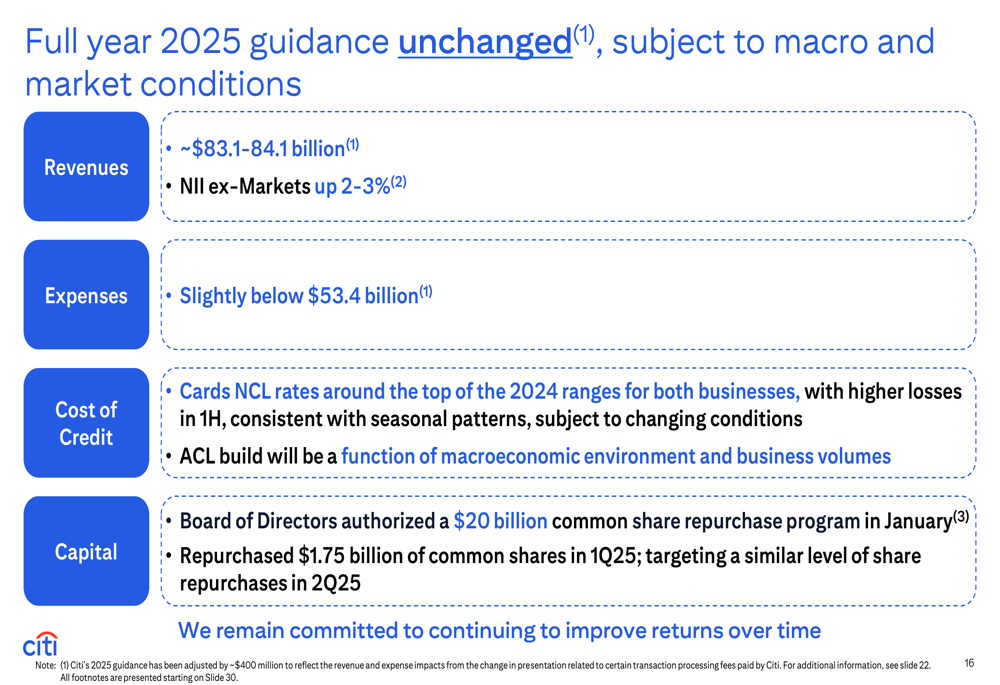

Citigroup maintained its full-year 2025 guidance, projecting revenues of approximately $83.1-84.1 billion and expenses slightly below $53.4 billion. The bank expects net interest income (excluding markets) to rise by 2-3% and anticipates credit card net charge-off rates around the top of the 2024 ranges.

The full year guidance summary provides a clear outlook for investors:

Looking beyond 2025, Citigroup remains committed to achieving a RoTCE of 10-11% by 2026. During the earnings call, CFO Mark Mason emphasized that while the drivers behind this target remain the same, the revenue mix might differ depending on how global economic conditions evolve.

Mason also highlighted the bank’s strong reserve position, with nearly $23 billion in total reserves and a reserve-to-funded loans ratio of 2.7%. The bank’s reserves incorporate an eight-quarter weighted average unemployment rate of 5.1%, reflecting a cautious approach to potential economic uncertainty.

Competitive Industry Position

Citigroup’s global footprint and diversified business model position it uniquely among its peers to navigate changing global trade patterns and economic uncertainty. During the earnings call, Fraser emphasized that the bank’s deep embeddedness with clients—many of whom have been with Citigroup for decades or even over a century—makes it less vulnerable to geopolitical dynamics.

The bank’s services business, in particular, benefits from being deeply integrated into clients’ day-to-day operations across markets. Fraser noted that while cross-border trade flows may change due to tariffs and trade tensions, Citigroup is well-positioned to facilitate these shifts and provide necessary hedging and financing activities.

In wealth management, Citigroup reported impressive net new investment assets of $16.5 billion in the quarter and over $56 billion in the last twelve months, representing approximately 11% organic growth. This performance underscores the bank’s growing competitive position in the global wealth management space.

As global economic uncertainty persists, Citigroup’s management expressed confidence in the bank’s diversified business strategy, which they believe will perform well across various macroeconomic scenarios. With capital strength, ample liquidity, and strong reserves, the bank appears well-positioned to navigate through challenging environments while continuing to execute on its transformation agenda and improve returns for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.