Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Clean Harbors Inc . (NYSE:CLH) presented its second-quarter 2025 results on July 30, showing a mixed performance with flat overall revenue but improved profitability. The environmental services provider reported that while its core Environmental Services segment delivered solid growth, this was offset by a significant decline in its Safety-Kleen Sustainability Solutions business.

The market appeared cautious about the results, with Clean Harbors stock trading down 3.48% in premarket to $230.00, despite the company’s emphasis on margin improvements and strong cash flow generation.

Quarterly Performance Highlights

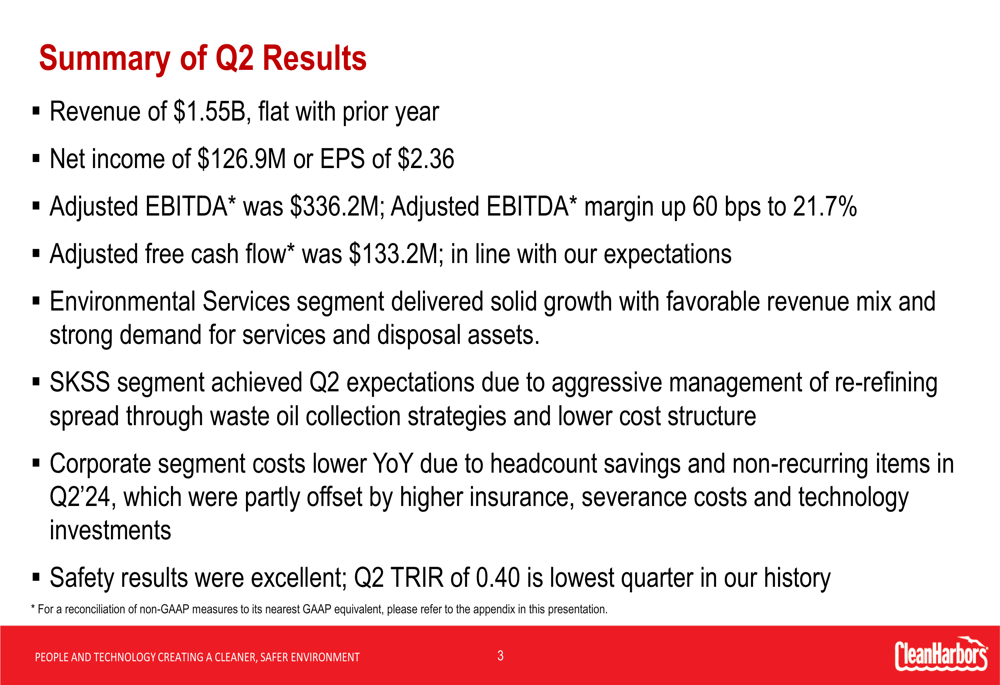

Clean Harbors reported Q2 2025 revenue of $1.55 billion, essentially flat compared to the same period last year. However, the company improved its profitability metrics, with adjusted EBITDA increasing to $336.2 million, up from $327.8 million in Q2 2024. The adjusted EBITDA margin expanded by 60 basis points to 21.7%.

As shown in the company’s summary of quarterly results:

Net income came in at $126.9 million, translating to earnings per share of $2.36, down from $133.3 million or $2.46 per share in the prior-year period. The company highlighted that its adjusted free cash flow reached $133.2 million, a significant improvement from $84.2 million in Q2 2024.

Clean Harbors also emphasized its safety performance, achieving a Total (EPA:TTEF) Recordable Incident Rate (TRIR) of 0.40, which it claimed was the lowest quarterly rate in company history.

Segment Analysis

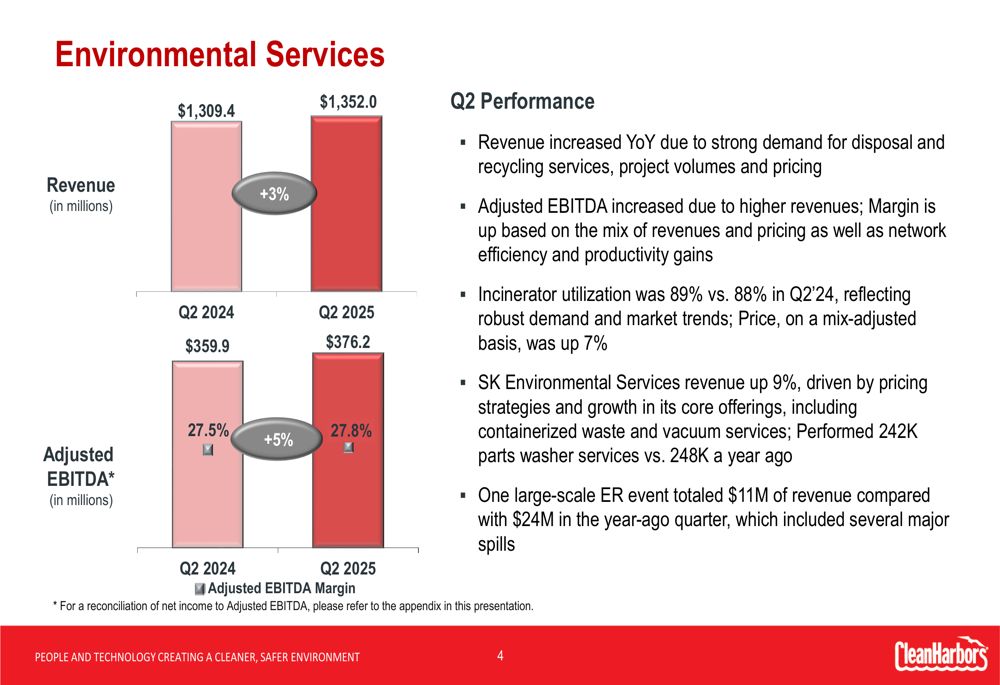

The Environmental Services segment, which represents the bulk of Clean Harbors’ business, delivered 3% revenue growth to $1.35 billion. The segment’s adjusted EBITDA increased 5% to $376.2 million, with margins improving to 27.8% from 27.5% in the prior year. The company attributed this growth to strong demand for disposal and recycling services, higher project volumes, and effective pricing strategies.

The segment’s performance is illustrated in the following chart:

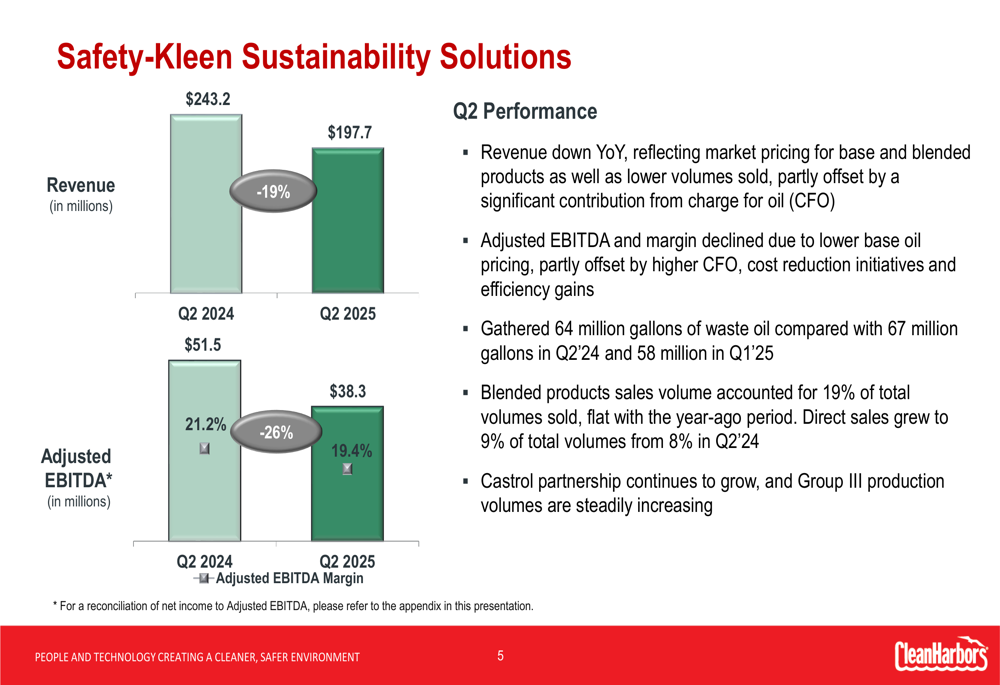

In contrast, the Safety-Kleen Sustainability Solutions segment experienced significant challenges, with revenue declining 19% to $197.7 million and adjusted EBITDA falling 26% to $38.3 million. The segment’s margin contracted from 21.2% to 19.4%. The company cited lower base oil pricing and reduced volumes as key factors behind the decline, though noted this was partially offset by higher charge-for-oil (CFO) revenue and cost reduction initiatives.

The following chart illustrates the Safety-Kleen segment’s performance:

Financial Position and Cash Flow

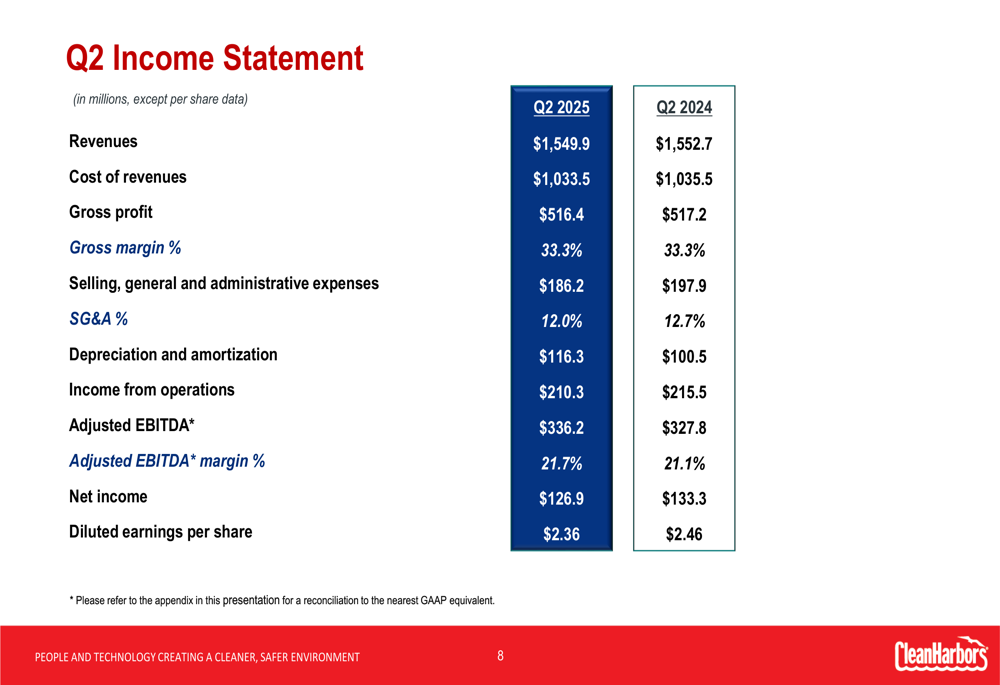

Clean Harbors’ Q2 income statement revealed that while gross profit remained stable at $516.4 million (33.3% margin), the company reduced its selling, general and administrative expenses to $186.2 million or 12.0% of revenue, down from $197.9 million or 12.7% in Q2 2024. However, depreciation and amortization expenses increased to $116.3 million from $100.5 million in the prior-year period.

The detailed income statement comparison is shown below:

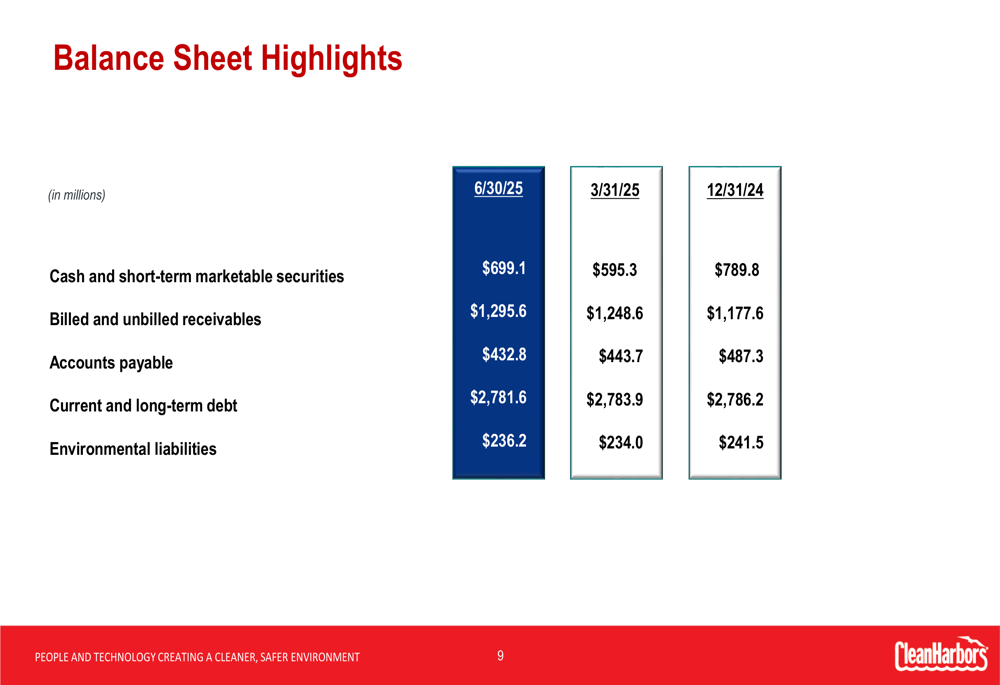

The company’s balance sheet showed a strengthened cash position, with cash and short-term marketable securities increasing to $699.1 million as of June 30, 2025, up from $595.3 million at the end of Q1 2025. Total debt remained relatively stable at $2.78 billion.

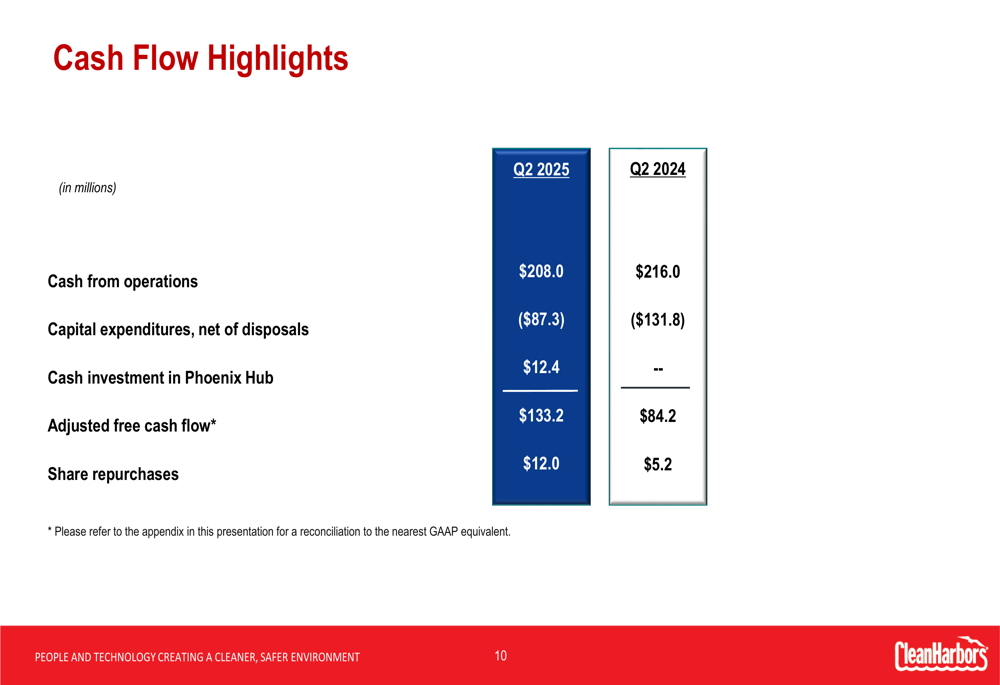

Cash flow highlights revealed that capital expenditures decreased significantly to $87.3 million from $131.8 million in Q2 2024. The company also increased its share repurchases to $12.0 million from $5.2 million in the prior-year period.

Guidance and Outlook

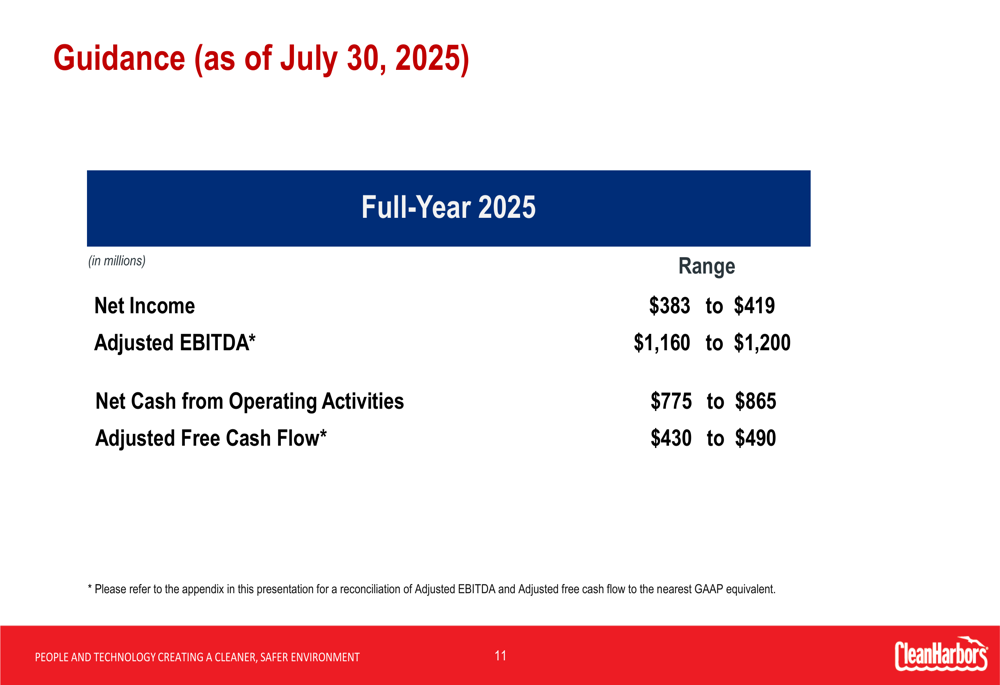

Looking ahead, Clean Harbors maintained its full-year 2025 guidance, projecting net income between $383 million and $419 million, and adjusted EBITDA between $1.16 billion and $1.2 billion. The company expects net cash from operating activities to range from $775 million to $865 million, with adjusted free cash flow between $430 million and $490 million.

The company’s full-year guidance is summarized in the following table:

Clean Harbors emphasized its disciplined capital allocation strategy, focusing on organic growth investments, share repurchases, strategic acquisitions, and debt management. The company indicated it would continue to evaluate acquisition opportunities while executing its authorized share buyback plan.

Despite the positive framing of results and maintained guidance, the premarket stock decline suggests investors may be concerned about the significant challenges in the Safety-Kleen segment and the company’s ability to drive overall revenue growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.