Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

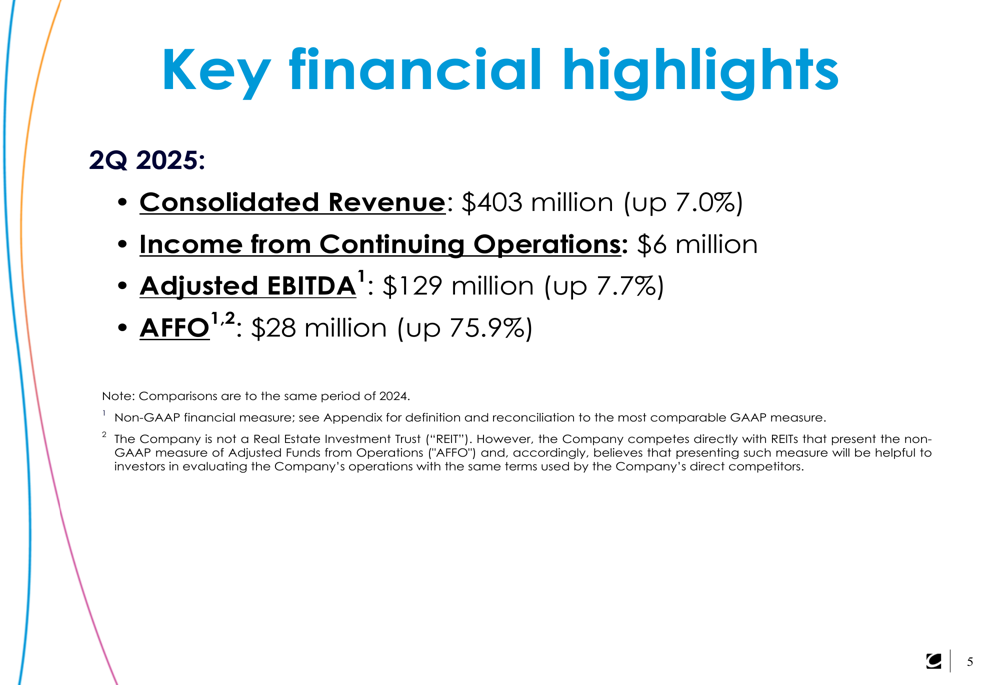

Clear Channel Outdoor Holdings (NYSE:CCO) reported strong second-quarter results on August 5, 2025, with consolidated revenue increasing 7.0% year-over-year to $403 million. The out-of-home advertising company’s shares have risen 7.84% to $1.10 following the presentation, continuing their recovery from the 52-week low of $0.811.

Quarterly Performance Highlights

Clear Channel delivered significant improvements across key financial metrics in Q2 2025. Adjusted EBITDA rose 7.7% to $129 million, while Adjusted Funds From Operations (AFFO) surged 75.9% to $28 million compared to the same period in 2024.

The company reported income from continuing operations of $6 million, a substantial improvement from the $25.4 million loss in the prior-year period. This turnaround reflects the company’s successful execution of strategic initiatives and growing advertising demand.

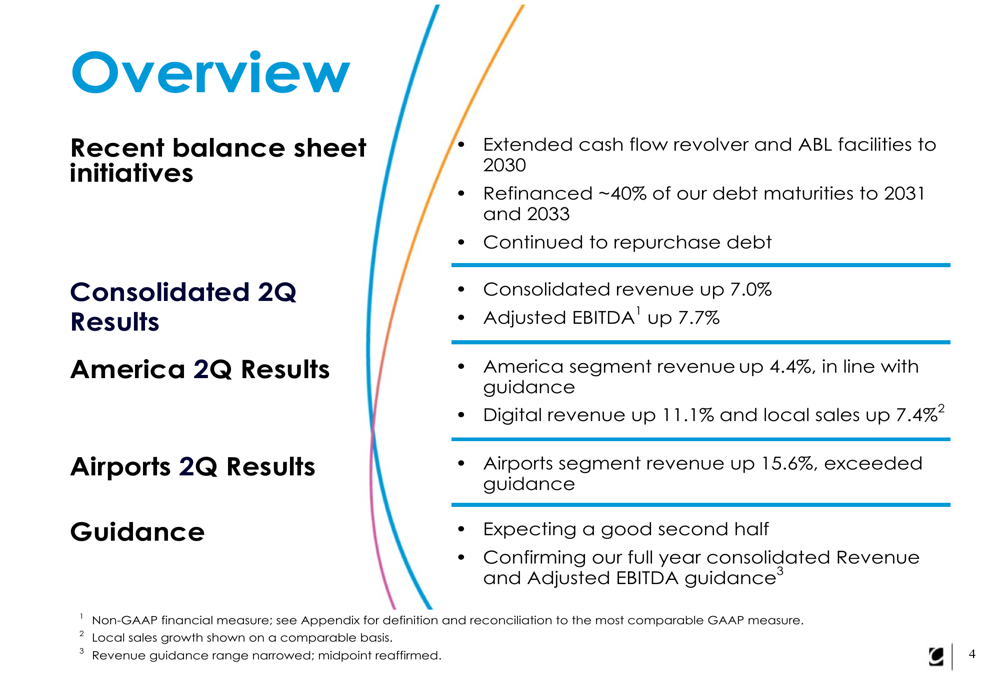

As shown in the following overview of Q2 2025 results:

The performance represents a significant acceleration from Q1 2025, when the company reported just 2.2% revenue growth and a 12.5% decline in Adjusted EBITDA year-over-year.

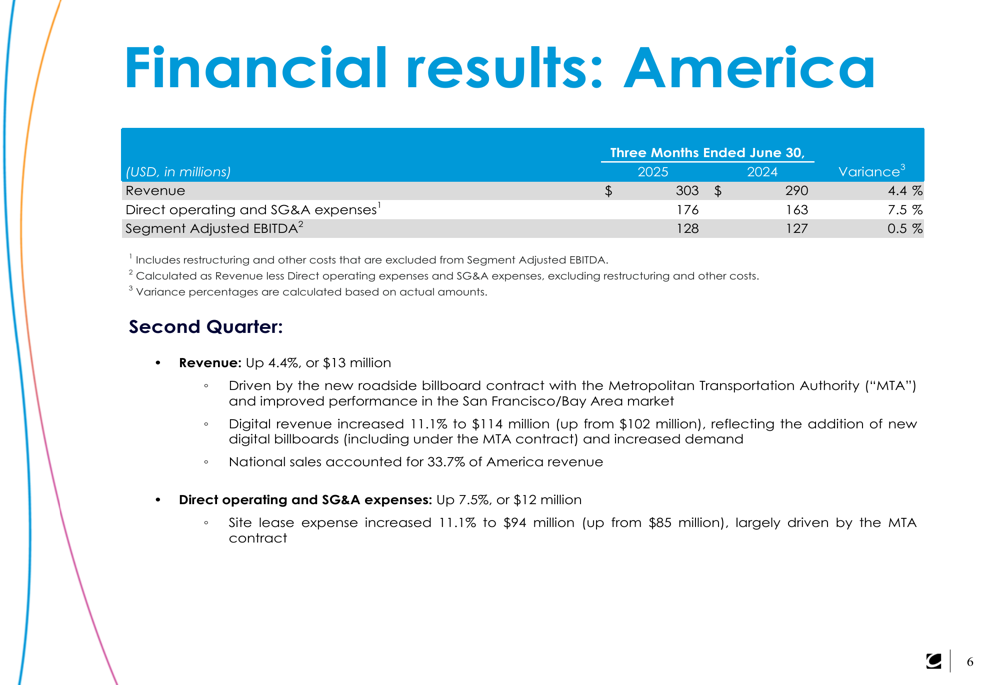

Breaking down segment performance, the America segment saw revenue increase by 4.4% to $303 million, driven by a new roadside billboard contract with the Metropolitan Transportation Authority (MTA) and improved performance in the San Francisco/Bay Area market. Segment Adjusted EBITDA increased marginally by 0.5% to $128 million.

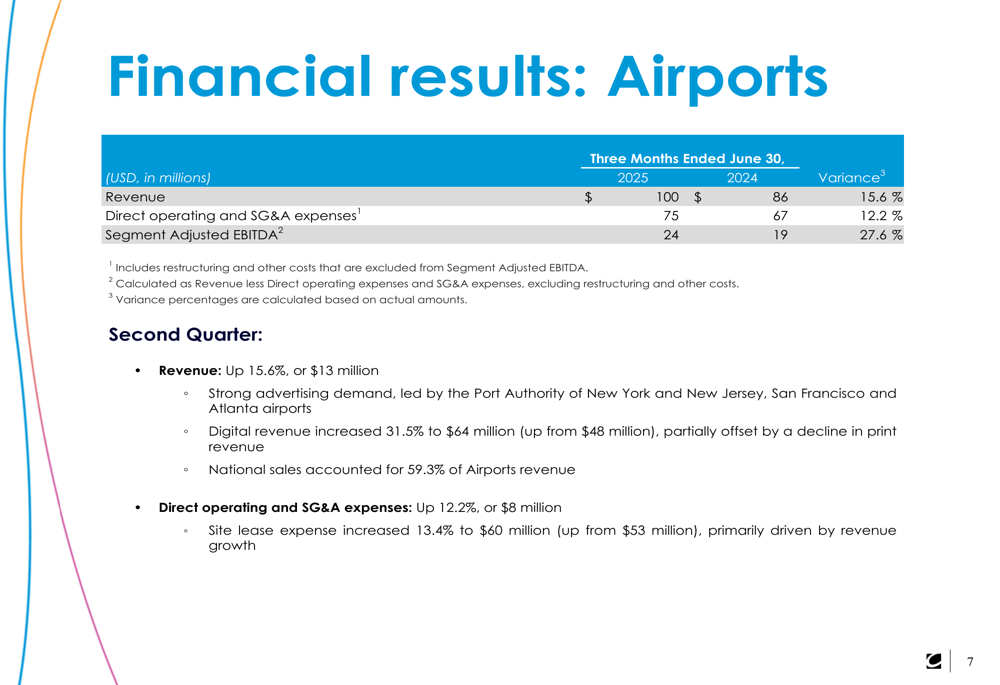

The Airports segment delivered exceptional results with revenue jumping 15.6% to $100 million and Adjusted EBITDA surging 27.6% to $24 million. This growth was fueled by strong advertising demand, particularly at the Port Authority of New York and New Jersey, San Francisco, and Atlanta airports.

The following table details the key financial metrics for Q2 2025:

Digital Transformation Driving Growth

Digital revenue continues to be a primary growth driver for Clear Channel, with the America segment reporting an 11.1% increase in digital revenue to $114 million. The Airports segment saw even more dramatic digital growth, with revenue surging 31.5% to $64 million.

The segment breakdown reveals the company’s successful digital transformation strategy:

The Airports segment’s impressive performance demonstrates the effectiveness of the company’s digital-first approach in high-traffic locations:

Capital expenditures for the quarter totaled $13 million, down from $16 million in the same period last year. The reduction was primarily due to lower digital spend and reduced contractual spending on shelters in the America segment.

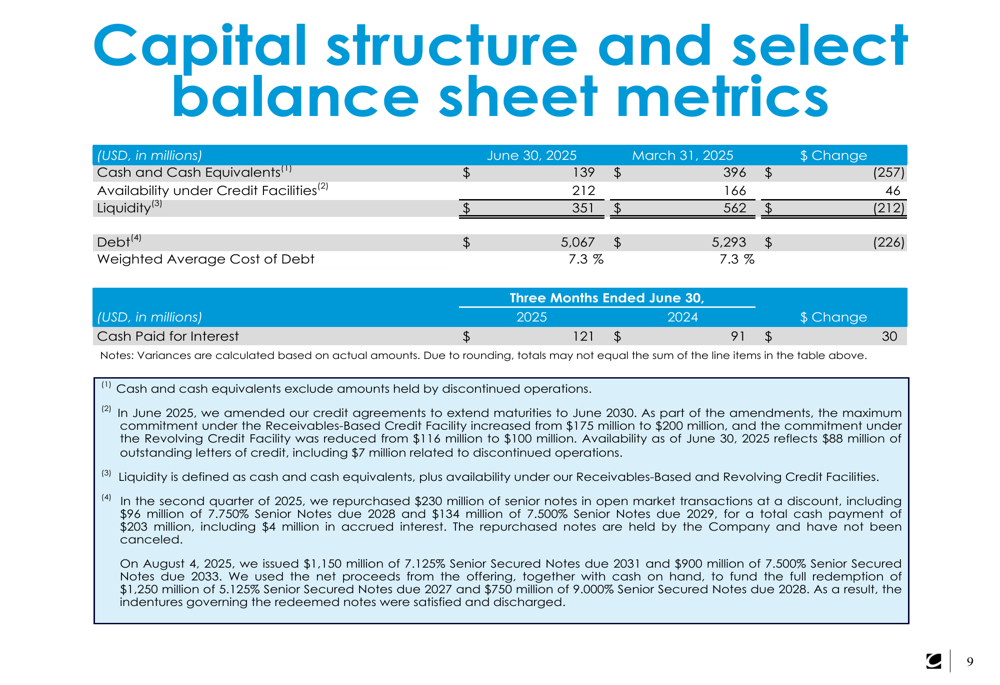

Balance Sheet and Capital Management

Clear Channel has made significant progress in strengthening its balance sheet and managing its debt profile. During the quarter, the company extended its cash flow revolver and ABL facilities to 2030 and refinanced approximately 40% of its debt maturities to 2031 and 2033.

As of June 30, 2025, the company reported:

- Cash and cash equivalents of $139 million (down from $396 million on March 31)

- Total debt of $5,067 million (reduced from $5,293 million on March 31)

- Weighted average cost of debt at 7.3%

- Liquidity of $351 million

The following table provides a detailed view of the company’s capital structure:

The company continues to execute its strategy of divesting international operations, having completed sales totaling $745 million. These include the Europe-North business for $625 million in March 2025 and operations in Mexico, Peru, and Chile for $20 million in February 2025. A pending sale of the Brazil business was announced in Q2 2025 and is expected to close later this year.

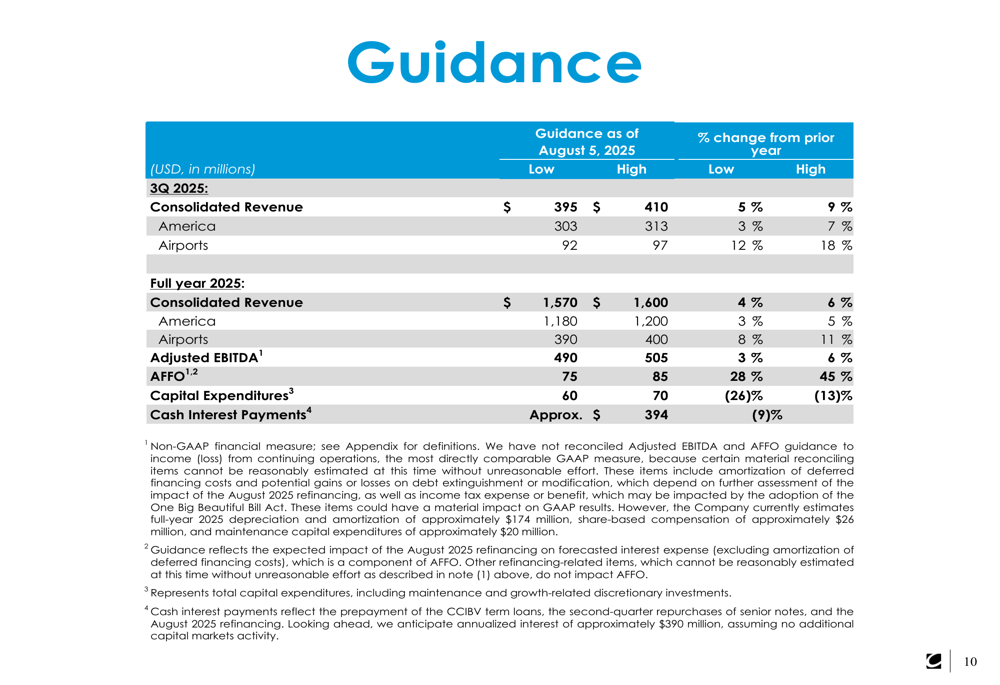

Forward Guidance and Outlook

Clear Channel reaffirmed its full-year 2025 guidance, projecting consolidated revenue of $1,570-1,600 million (4-6% year-over-year growth) and Adjusted EBITDA of $490-505 million (3-6% growth). The company expects AFFO to reach $75-85 million, representing substantial growth of 28-45% from 2024.

For the third quarter of 2025, Clear Channel anticipates consolidated revenue of $395-410 million, reflecting 5-9% growth compared to the prior year. The America segment is expected to grow 3-7%, while the Airports segment is projected to continue its strong performance with 12-18% growth.

The detailed guidance is presented in the following table:

The company’s outlook suggests continued momentum in the second half of 2025, with growth rates expected to remain solid across both segments. The projected improvement in AFFO indicates enhanced cash generation capabilities as the company benefits from its debt refinancing initiatives and operational improvements.

Strategic Initiatives and Social Responsibility

Beyond financial performance, Clear Channel highlighted its environmental and social initiatives, including campaigns to raise awareness for missing children in partnership with the Texas Center for the Missing, promoting heat relief resources through digital billboards, and supporting youth-driven road safety campaigns like Project Yellow Light.

These initiatives demonstrate the company’s commitment to leveraging its advertising platforms for social good while building positive brand equity in its markets.

The strong Q2 results and positive outlook reflect Clear Channel’s successful execution of its strategic priorities: growing digital revenue, optimizing its U.S. portfolio, and improving its balance sheet. With the stock up 7.84% following the presentation and trading well above its 52-week low, investors appear to be recognizing the company’s improved performance and prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.