TSX futures inch lower after index closes at new all-time high

Introduction & Market Context

Clearwater Analytics Holdings Inc (NYSE:CWAN) presented its Q1 2025 investor presentation on April 30, showcasing strong financial performance and detailing its recent strategic acquisitions. The company, which provides a cloud-native investment accounting and analytics platform, reported results that exceeded analyst expectations while outlining its vision to build a comprehensive front-to-back investment management solution.

The presentation comes as Clearwater has completed three significant acquisitions: Enfusion, Beacon, and Blackstone (NYSE:BX)’s Bistro. These moves represent a strategic expansion of Clearwater’s capabilities from its traditional strength in middle and back-office functions into front-office operations, positioning the company to offer a more comprehensive solution to investment managers.

Quarterly Performance Highlights

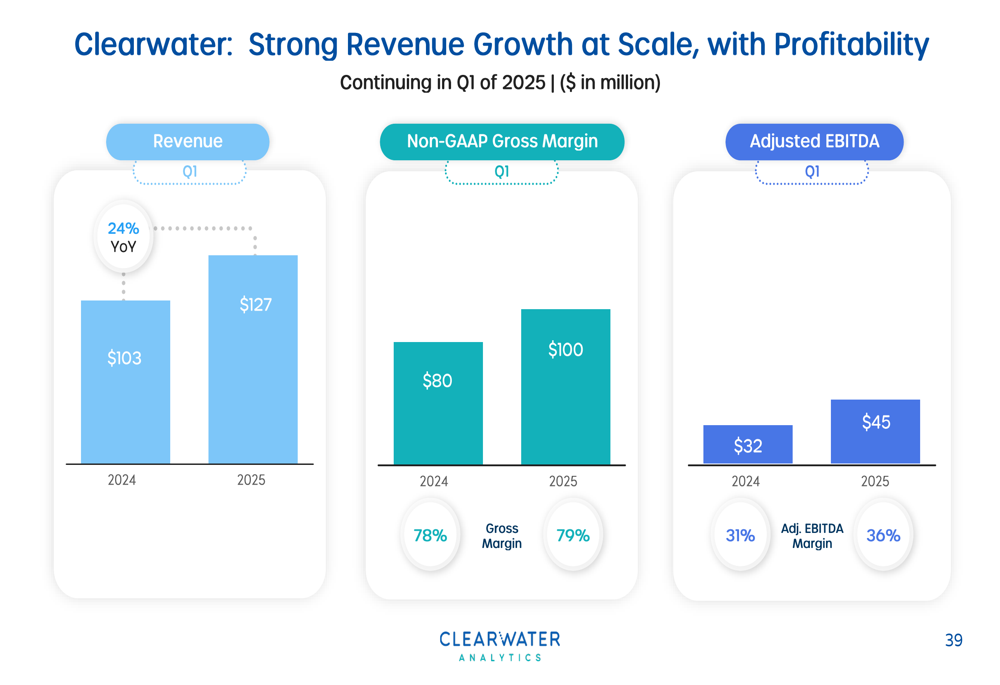

Clearwater reported impressive Q1 2025 results, with revenue reaching $126.9 million, representing a 24% year-over-year increase. The company achieved an adjusted EBITDA of $45.1 million, reflecting a 36% margin, up from 31% in the same period last year.

As shown in the following chart detailing Clearwater’s strong revenue growth and profitability:

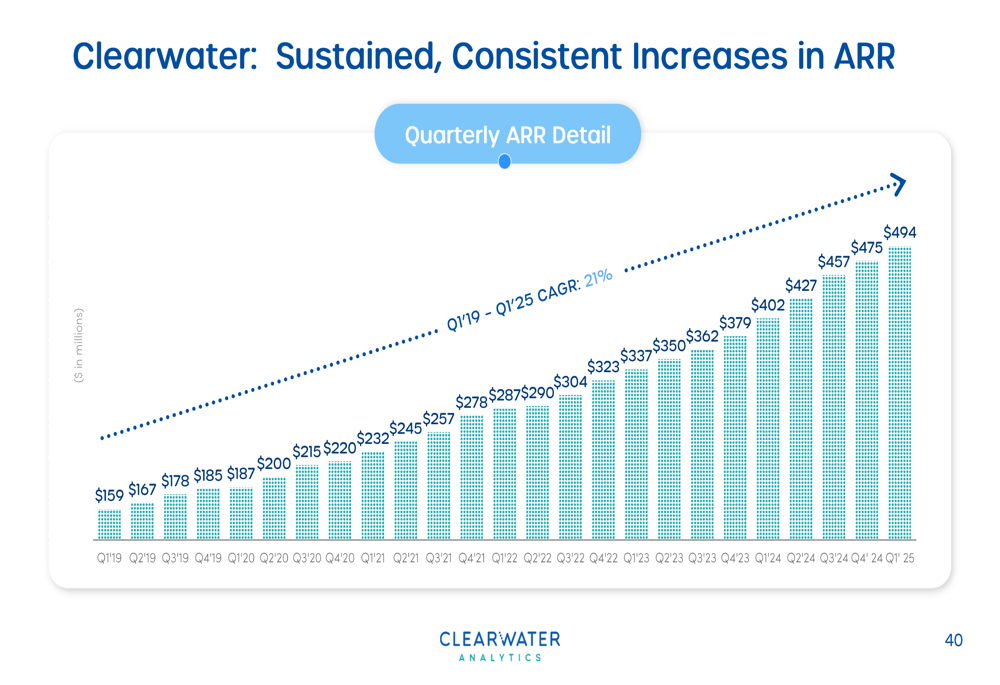

The company’s Annual Recurring Revenue (ARR) has shown consistent growth, reaching $494 million in Q1 2025, representing a 23% CAGR since 2016. This growth trajectory is illustrated in the quarterly ARR detail:

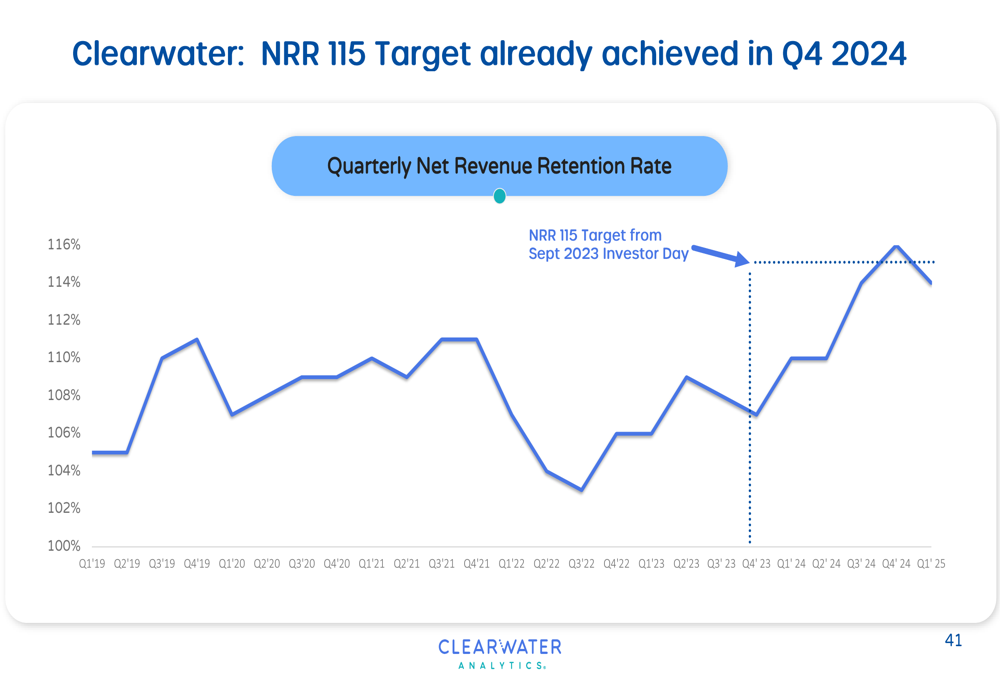

Clearwater has maintained exceptionally high client retention rates, with a gross revenue retention rate of 98% or higher for 24 of the past 25 quarters. The company also reported a net revenue retention rate of 114%, exceeding its target of 115% ahead of schedule, as shown in the following chart:

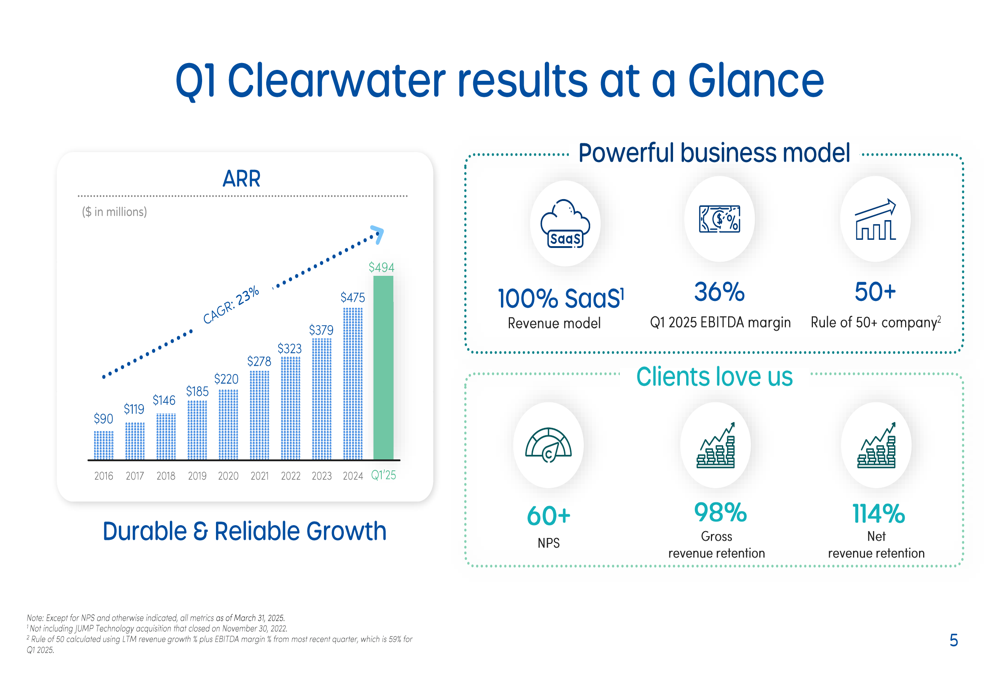

The Q1 results snapshot highlights Clearwater’s powerful business model, combining 100% SaaS revenue, strong EBITDA margins, and high client satisfaction metrics:

Strategic Initiatives

The centerpiece of Clearwater’s strategy is its recent acquisition spree, designed to transform the company from a middle/back-office specialist into a comprehensive front-to-back platform. The three acquisitions include:

1. Enfusion: Closed on April 21, 2025, this $760 million cash plus 28 million shares acquisition brings a market-leading front-office platform for hedge funds and asset managers, with approximately 900 clients and $206 million in ARR.

2. Beacon: Closed on April 30, 2025, this $336 million cash plus 7.5 million shares acquisition adds cross-asset trading and risk management capabilities, with approximately 40 clients including Blackstone, PIMCO, and Global Atlantic Financial Group.

3. Blackstone’s Bistro: Completed on March 31, 2025, this $10 million cash plus 3.8 million shares asset purchase brings private credit assets data visualization capabilities.

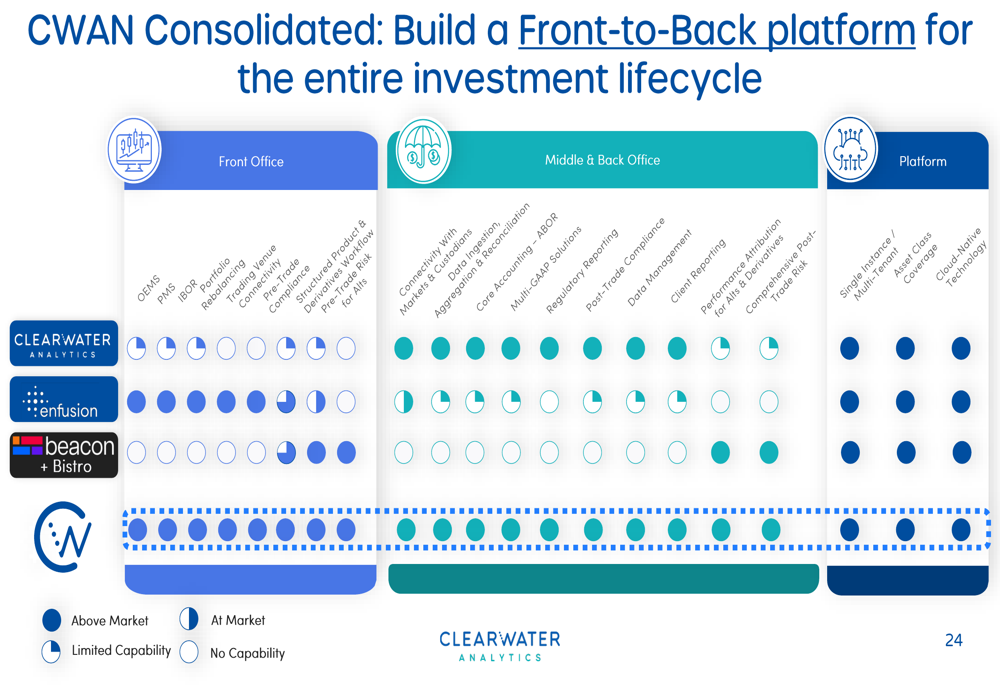

The following image illustrates how these acquisitions transform Clearwater’s platform capabilities across the front, middle, and back office:

Clearwater outlined a three-phase integration strategy, starting with maximizing each standalone business, then building cross-sell opportunities, and ultimately creating a comprehensive front-to-back platform. The company highlighted existing integrations with key clients like PIMCO, Global Atlantic, and Blackstone as early success stories.

The company’s vision for enhanced growth opportunities is outlined in the following framework:

Competitive Industry Position

The presentation positioned Clearwater as a disruptive force against legacy competitors like SS&C, State Street (NYSE:STT), SAP, BNY Mellon (NYSE:BK), SimCorp, and FIS. The company claims an approximately 80% competitive win rate and a Net Promoter Score above 60, indicating strong client satisfaction.

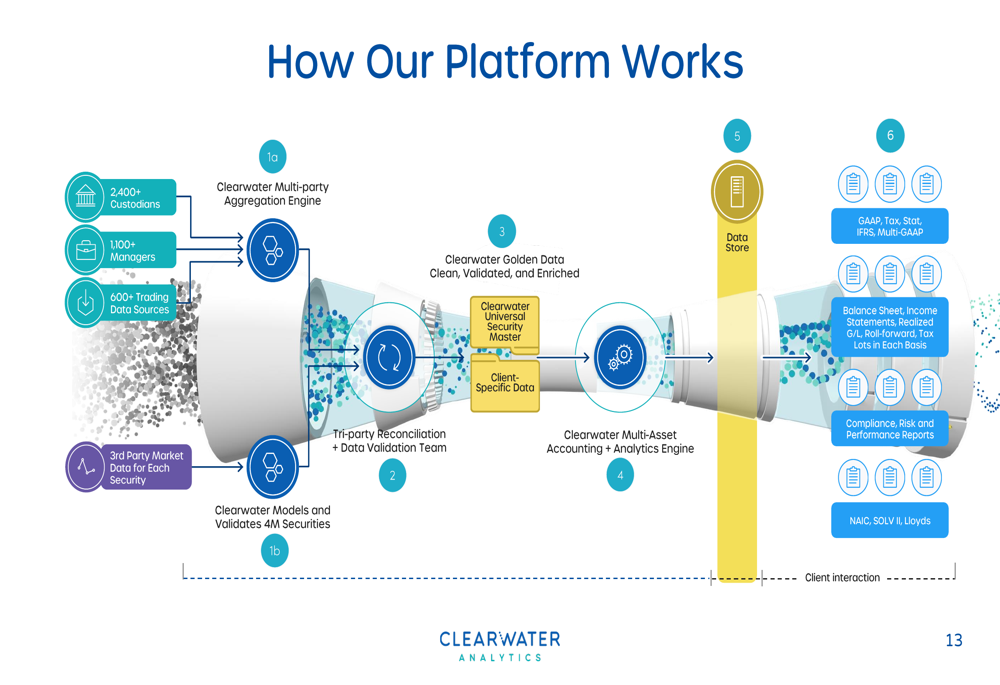

Clearwater’s platform works by aggregating data from multiple sources, validating and enriching it, and then providing multi-asset accounting and analytics capabilities:

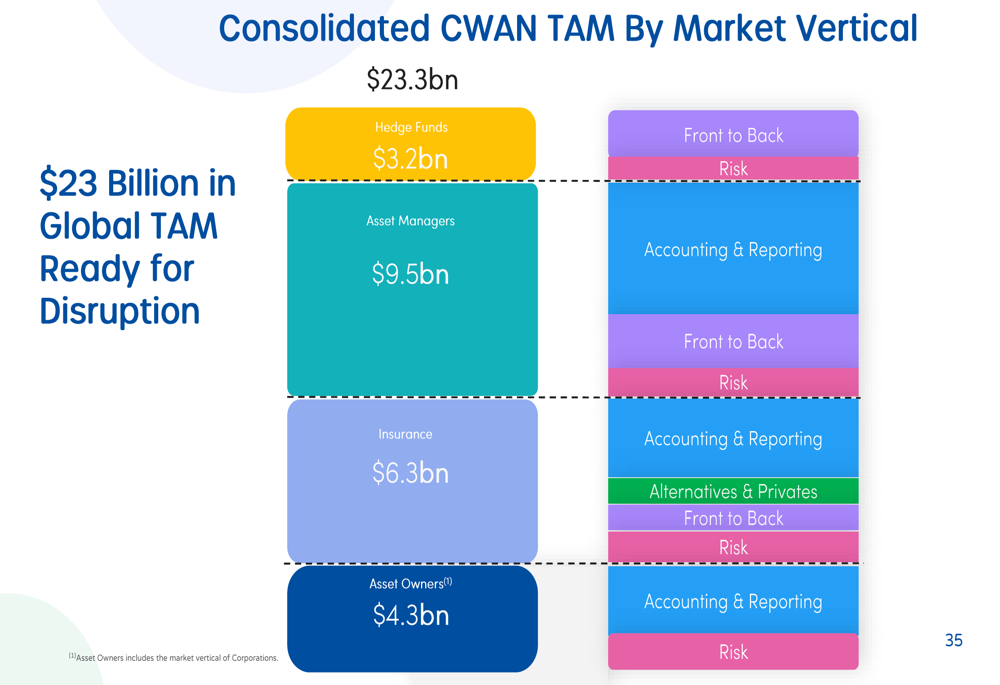

The acquisitions have significantly expanded Clearwater’s total addressable market (TAM) to $23.3 billion across multiple verticals:

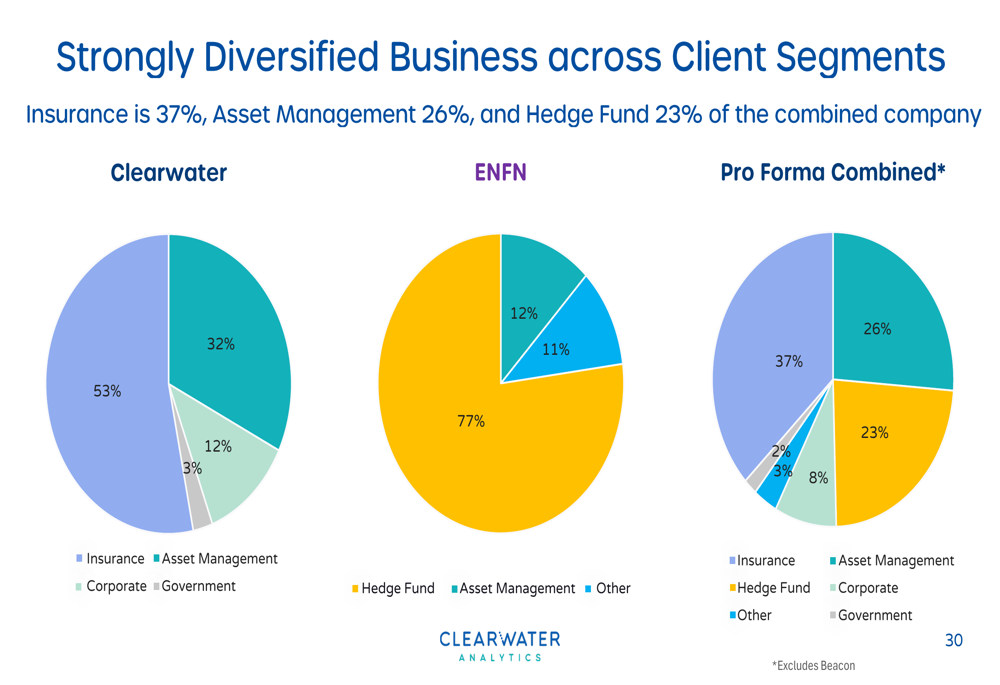

The combined company now has a more diversified client base across multiple segments, reducing concentration risk and opening new growth opportunities:

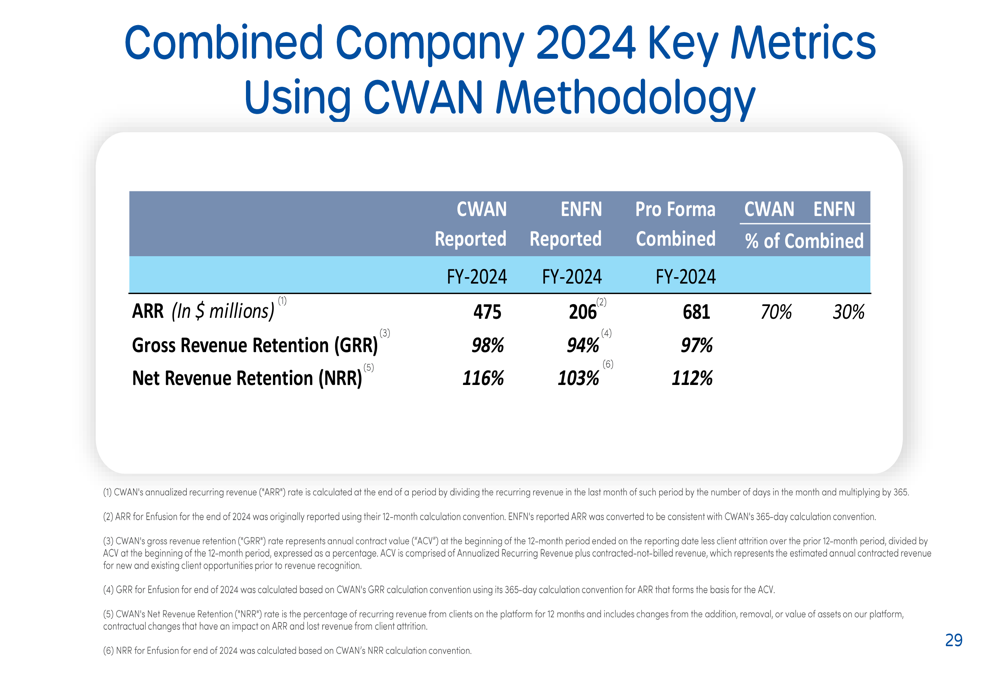

The combined metrics for Clearwater and its acquisitions show strong fundamentals, with a pro forma ARR of $681 million, 97% gross revenue retention, and 112% net revenue retention:

Forward-Looking Statements

Looking ahead, Clearwater provided guidance for 2025, projecting revenue between $720 million and $728 million, representing growth of 59% to 61%. The company also expects EBITDA to range from $230 million to $235 million.

CEO Sandeep Sahai emphasized the company’s strategic vision during the earnings call, stating, "We are working backwards from a future where fragmented investment systems will be as obsolete as paper ledgers." He also highlighted the potential impact of a unified security master, noting, "A single security master would completely change the game of how people think about investment management technology."

The company’s long-term goals remain unchanged: 20% revenue growth, 40% EBITDA margin, and 115% net revenue retention. With the recent acquisitions, Clearwater expects to achieve a "Rule of 50+" status (combined revenue growth and EBITDA margin exceeding 50%), with approximately 20% pro forma growth and 32% consolidated EBITDA margin in 2025.

Despite the positive outlook, investors should consider potential risks, including integration challenges with the recent acquisitions, macroeconomic pressures that could impact client investment strategies, and competitive pressures in the cloud-native investment platform market. The stock closed at $22.91 on May 1, 2025, up 0.75% for the day, but showing a 2.27% decline in after-hours trading.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.