Behind US stock gains, gold’s climb reflects growing market uncertainty: Macquarie

Introduction & Market Context

Clover Health Investments Corp (NASDAQ:CLOV) presented its first quarter 2025 earnings results on May 6, 2025, showcasing strong growth in both membership and financial metrics. The technology-focused Medicare Advantage insurer continues its transformation from a focus on profitability that began in 2022 to a growth phase starting in 2025.

In after-hours trading following the presentation, Clover Health stock rose 1.49% to $3.40, building on its closing price of $3.35. This positive reaction follows a period of significant stock volatility, with shares having traded between $0.70 and $4.87 over the past 52 weeks.

Quarterly Performance Highlights

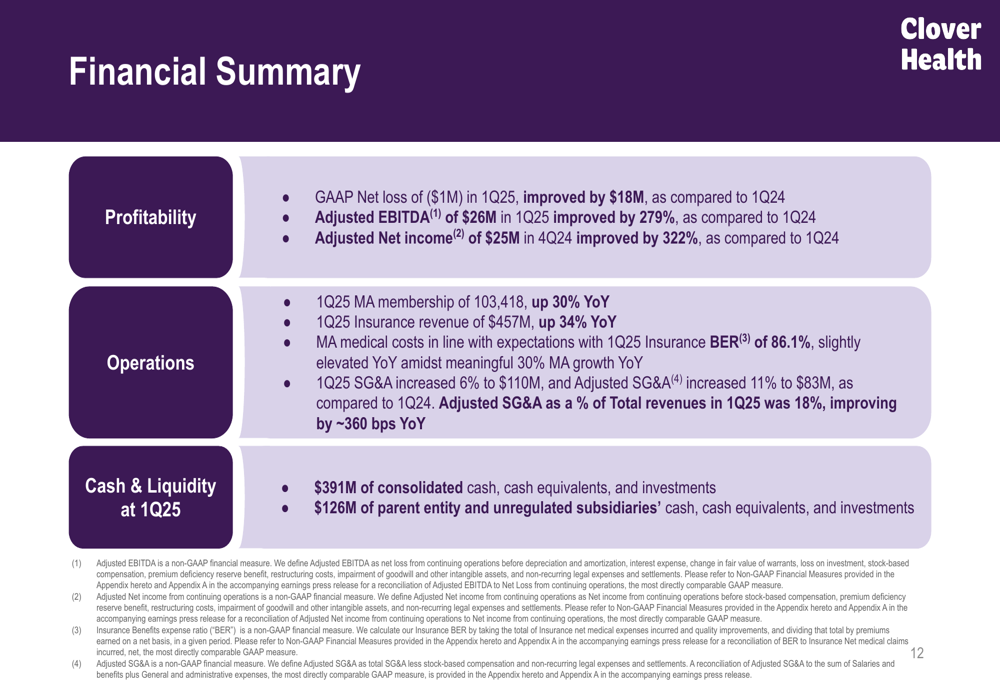

Clover Health reported substantial year-over-year improvements across key metrics for Q1 2025. Medicare Advantage membership grew 30% year-over-year to 103,418 members, driving a 34% increase in insurance revenue to $457 million.

As shown in the following financial summary chart, the company dramatically improved its profitability metrics while managing its strong growth:

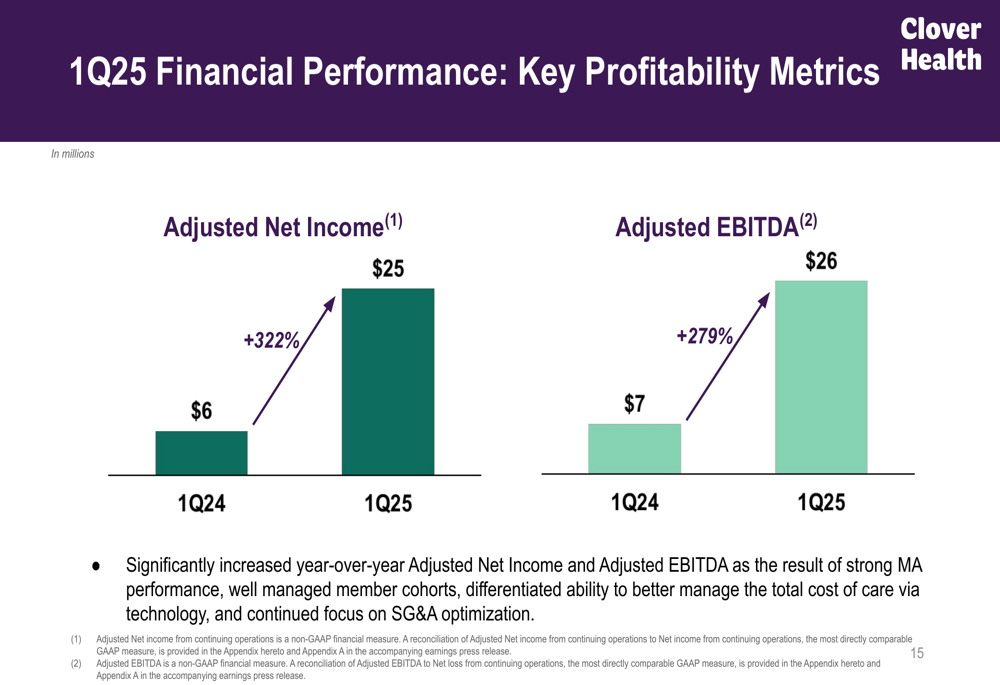

The company reported a GAAP net loss of just $1 million in Q1 2025, an $18 million improvement compared to Q1 2024. More impressively, adjusted EBITDA reached $26 million, representing a 279% increase year-over-year, while adjusted net income grew 322% to $25 million.

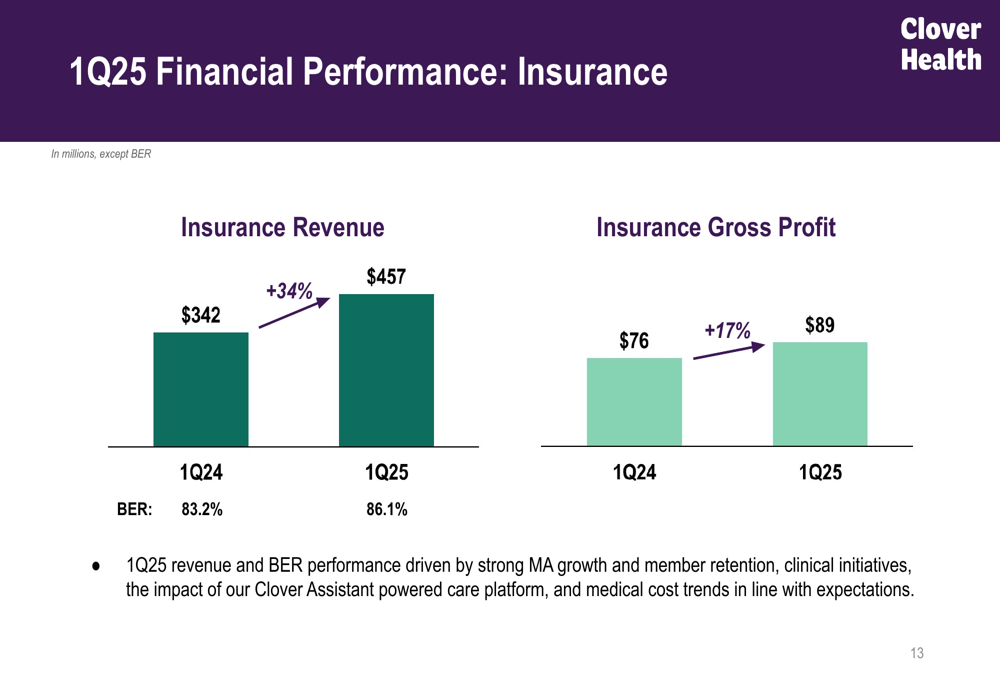

The insurance segment, which represents Clover’s core business, showed particularly strong performance in the quarter:

While insurance revenue grew 34% to $457 million, insurance gross profit increased 17% to $89 million. The Benefits Expense Ratio (BER) increased slightly to 86.1% from 83.2% in the prior year period, which the company attributed to the significant membership growth and associated costs of onboarding new members.

Financial Analysis

Clover Health demonstrated improving operational efficiency alongside its growth. Adjusted SG&A as a percentage of total revenue decreased to 18% in Q1 2025, an improvement of approximately 360 basis points year-over-year. This reflects the company’s ability to leverage its fixed costs across a growing membership base.

The following chart illustrates the significant improvement in key profitability metrics:

The company maintained a strong cash position, reporting $391 million in consolidated cash, cash equivalents, and investments at the end of Q1 2025. Of this amount, $126 million was held at the parent entity and unregulated subsidiaries.

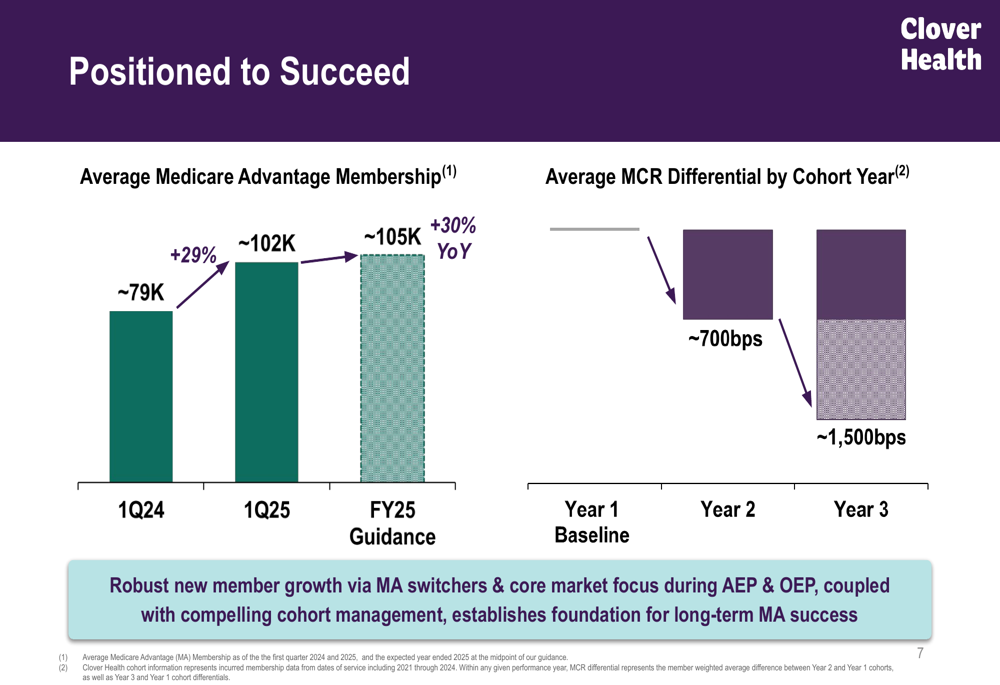

Clover’s financial strategy appears to be working, with cohort economics showing significant improvement over time. According to the company’s data, member cohorts show a 700 basis point improvement in MCR ( Medical (TASE:BLWV) Cost Ratio) by year two and a 1,500 basis point improvement by year three:

Technology and Clinical Outcomes

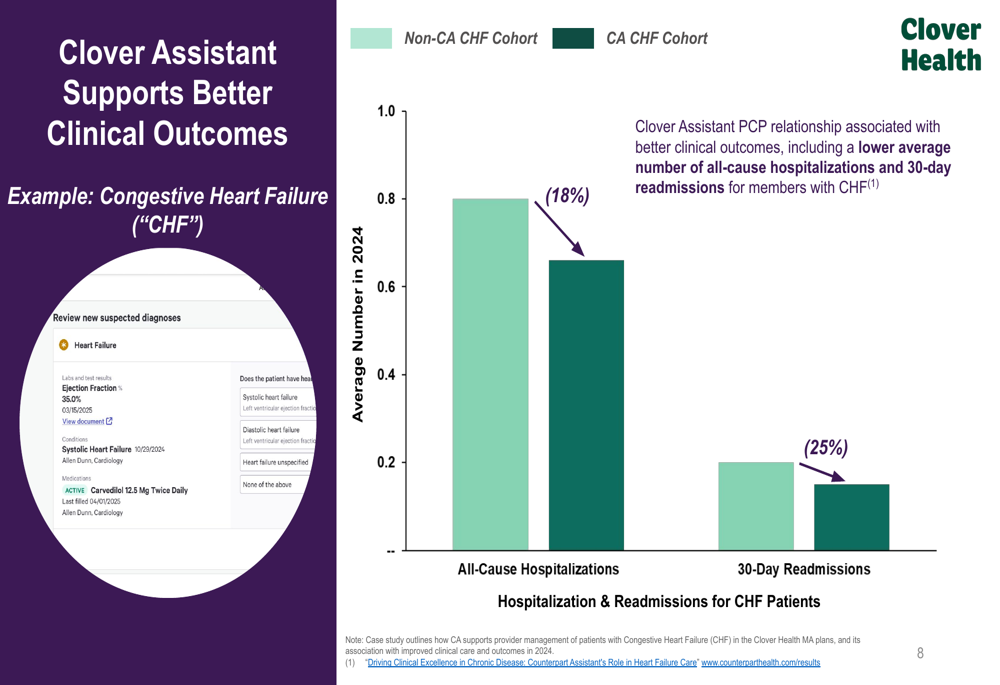

A central theme of Clover’s presentation was the clinical effectiveness of its Clover Assistant technology platform. The company presented data showing that its technology-driven approach leads to better health outcomes and cost management.

For example, the following chart demonstrates how Clover Assistant is associated with reduced hospitalizations and readmissions for patients with congestive heart failure:

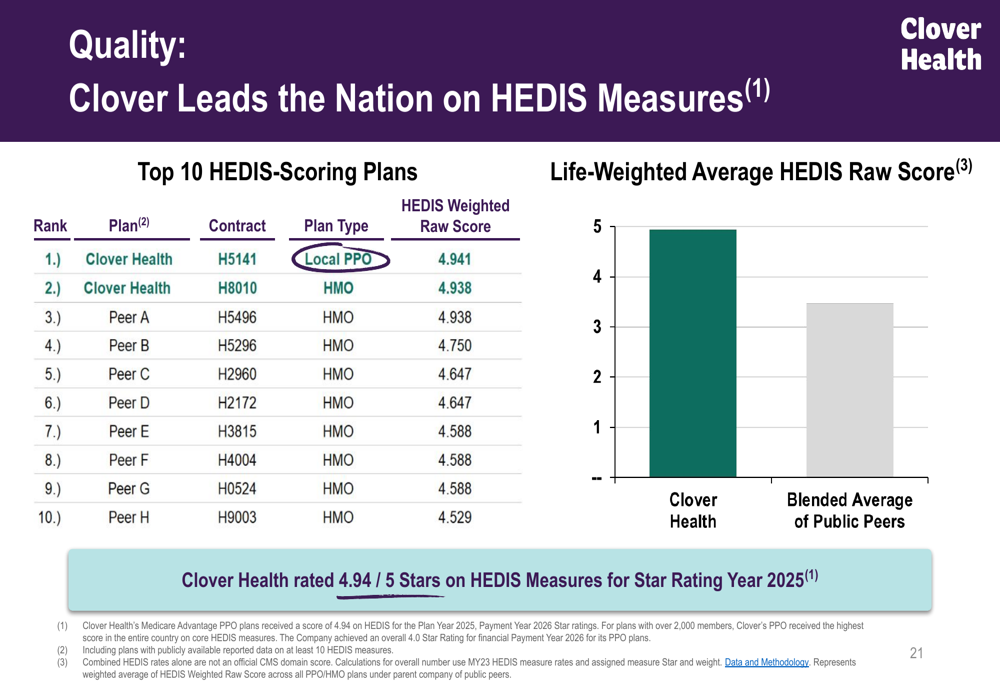

The company also highlighted its leadership in healthcare quality metrics, achieving what it claims is the highest HEDIS (Healthcare Effectiveness Data and Information Set) score in the entire country:

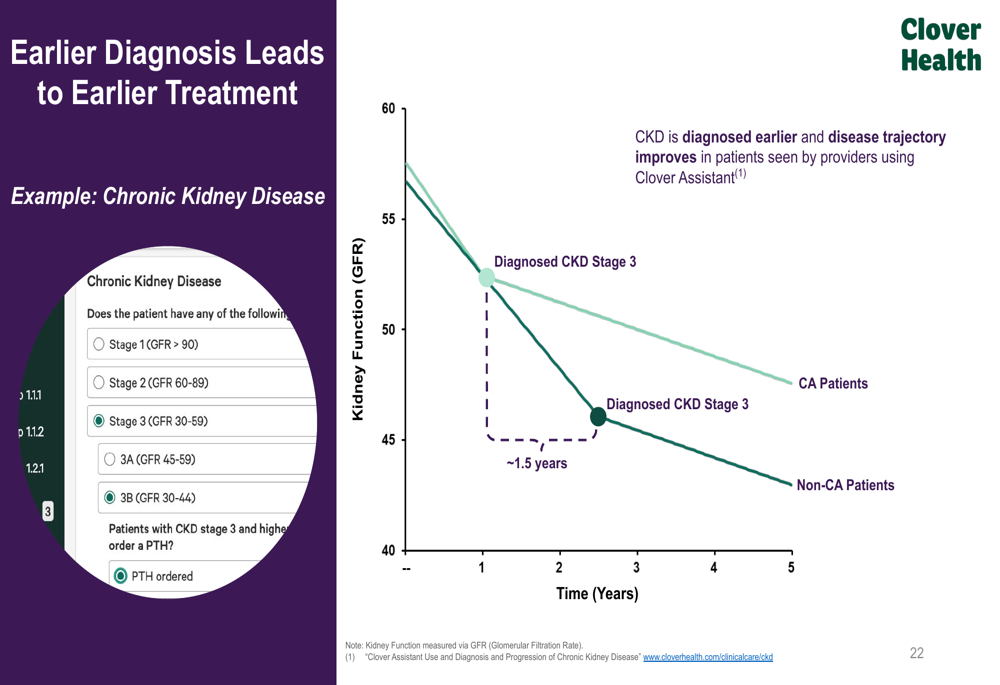

Clover’s technology platform appears to be driving earlier diagnosis and treatment of chronic conditions. The company presented data showing earlier diagnosis of chronic kidney disease and diabetes, leading to better management of these conditions:

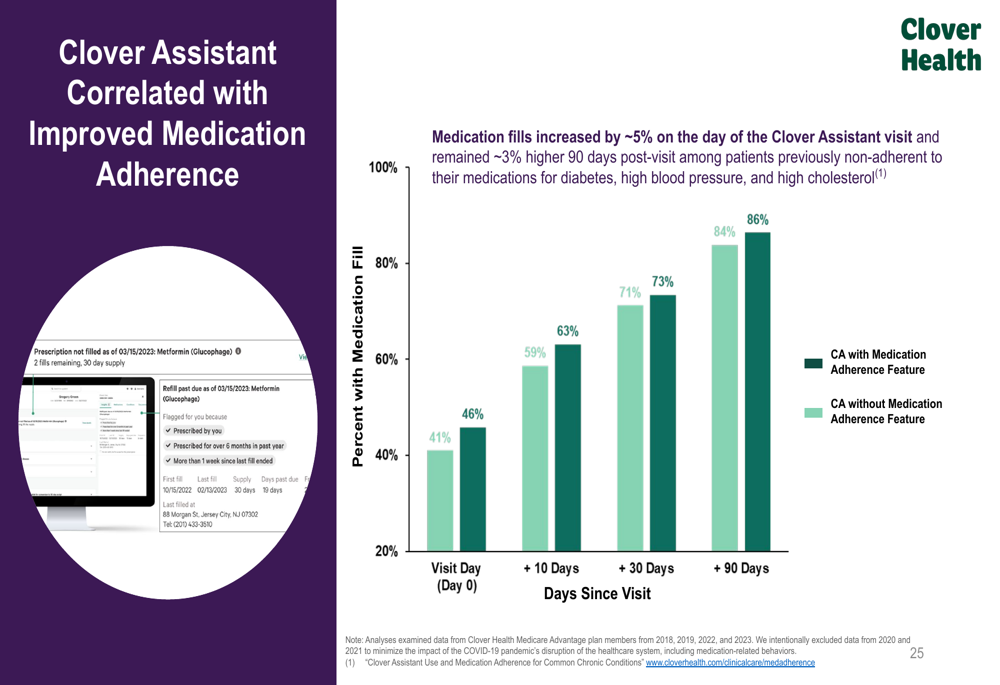

Additionally, the company showed evidence that its technology improves medication adherence, a critical factor in managing chronic conditions:

Forward Guidance and Outlook

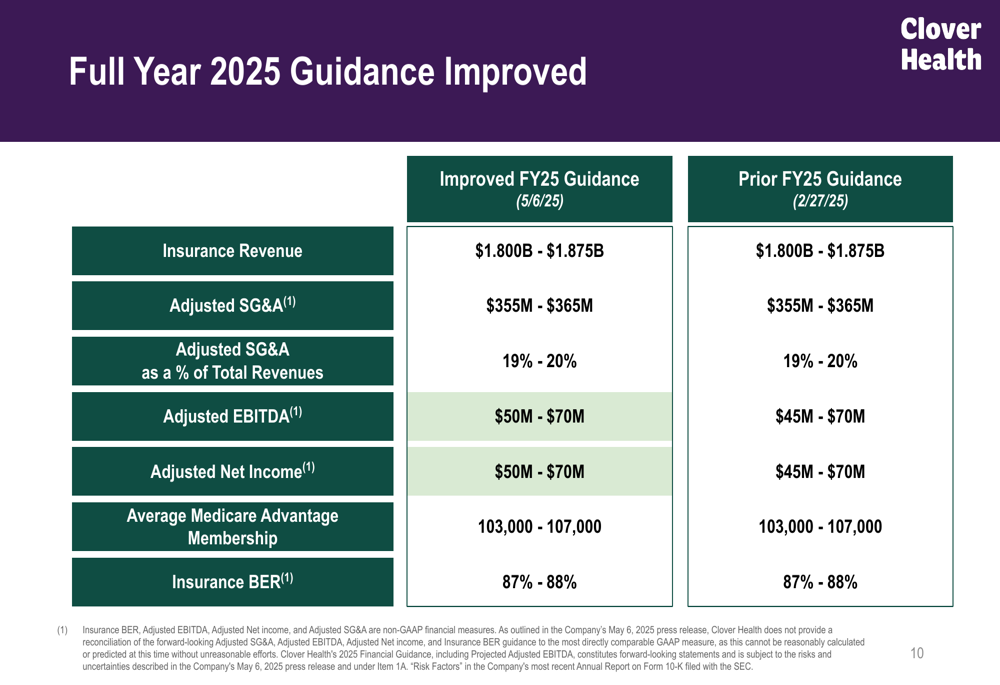

Clover Health raised the lower end of its full-year 2025 guidance for adjusted EBITDA and adjusted net income, while maintaining its revenue and membership projections. The updated guidance reflects increased confidence in the company’s ability to balance growth and profitability.

As shown in the following guidance table, the company now expects:

For full-year 2025, Clover Health projects insurance revenue between $1.8 billion and $1.875 billion, with adjusted EBITDA and adjusted net income both in the range of $50 million to $70 million. The company expects to maintain its Medicare Advantage membership growth of approximately 30% year-over-year.

Looking further ahead, Clover highlighted several tailwinds for 2026, including its 4.0 Star rating for payment year 2026, which should result in higher reimbursement rates, continued improvement in member cohort economics, and ongoing cost efficiency initiatives.

The company’s long-term strategy continues to focus on its technology-driven approach to healthcare, with an emphasis on earlier diagnosis and treatment of chronic conditions, which it believes will lead to better health outcomes and lower costs over time.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.