S&P 500 climbs to record high as in-line inflation data point to Fed rate cut

Introduction & Market Context

Clover Health Investments Corp (NASDAQ:CLOV) presented its second quarter 2025 earnings results on August 5, 2025, highlighting strong membership growth and sustained profitability despite industry-wide elevated medical costs. The company’s stock closed at $2.88, down 1.04% in regular trading, but gained 0.69% in aftermarket trading following the earnings presentation.

The Medicare Advantage insurer continues to emphasize its technology-first approach to healthcare delivery, maintaining profitability while significantly expanding its membership base. This performance comes amid a challenging environment for Medicare Advantage insurers, with many competitors scaling back benefits due to rising medical costs.

Quarterly Performance Highlights

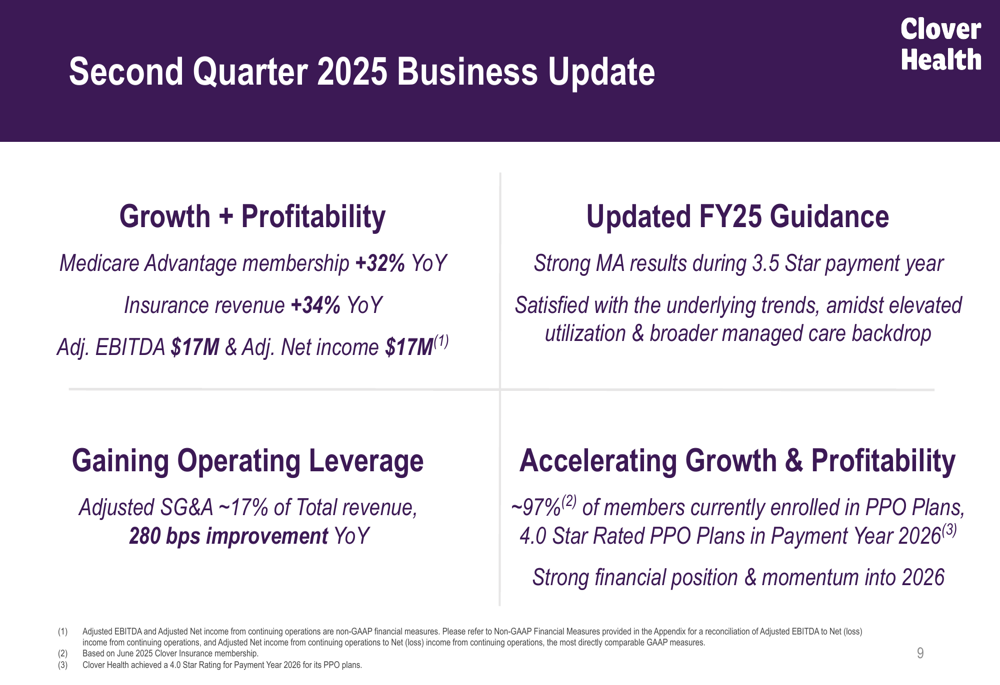

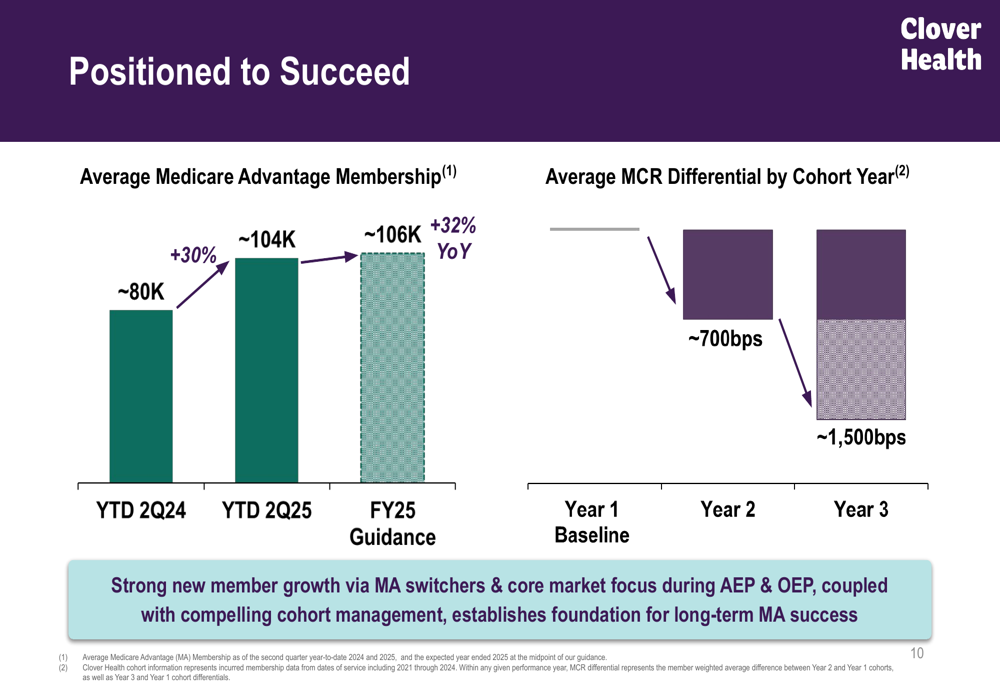

Clover Health reported Medicare Advantage membership of 106,323 in Q2 2025, representing a 32% year-over-year increase. This membership growth drove a 34% increase in insurance revenue to $470 million compared to $350 million in Q2 2024.

The company achieved an Adjusted EBITDA of $17 million and Adjusted Net Income of $17 million for the quarter. Year-to-date, Clover has maintained steady profitability with Adjusted EBITDA of $43 million and Adjusted Net Income of $42 million, on par with the same period last year despite significant growth investments.

As shown in the following chart detailing the company’s quarterly performance:

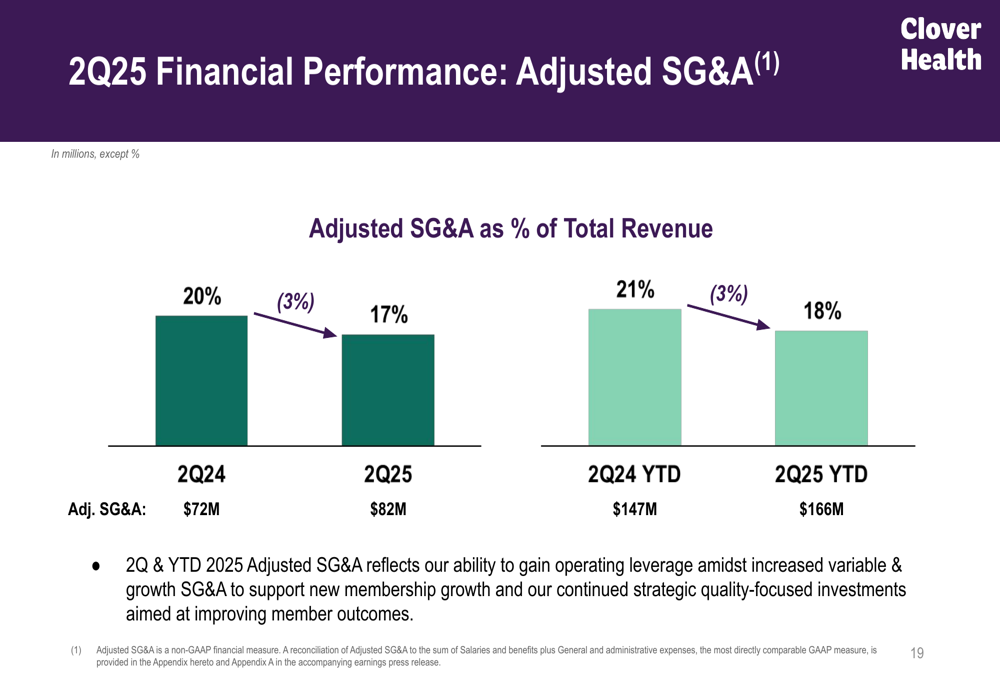

Clover’s Insurance Benefits Expense Ratio (BER) was 88.4% for Q2 2025, reflecting elevated utilization trends that have affected the broader Medicare Advantage industry. Despite these headwinds, the company improved its operational efficiency, with Adjusted SG&A as a percentage of total revenue decreasing to 17% in Q2 2025, an improvement of approximately 280 basis points year-over-year.

The following slide illustrates this operational improvement:

Technology and Clinical Outcomes

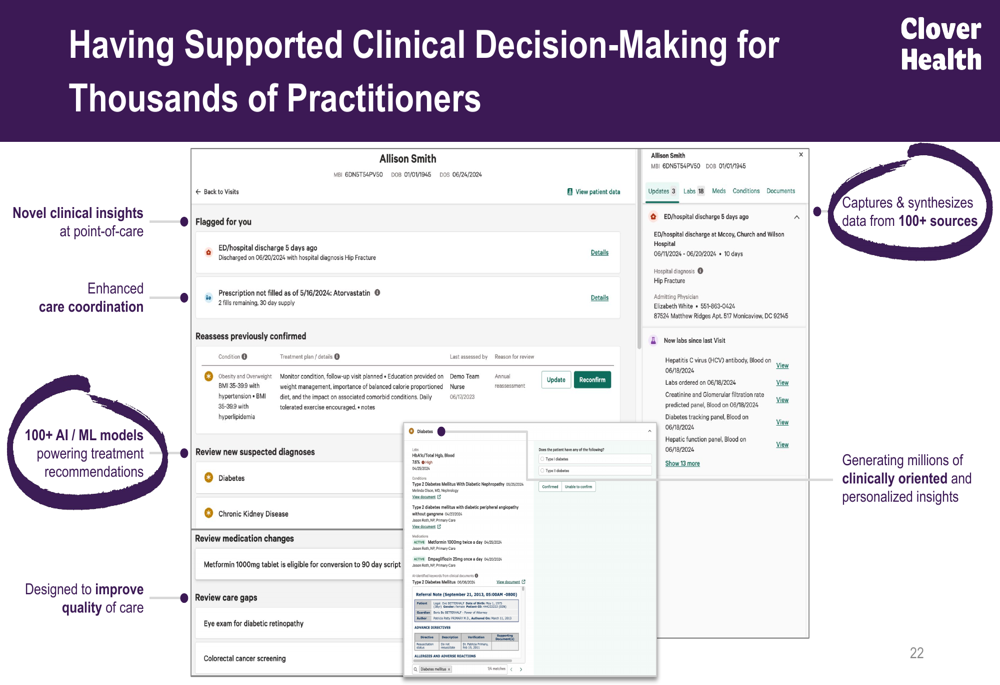

Clover Health continues to differentiate itself through its AI-powered Clover Assistant platform, which provides clinical decision support to physicians. The company presented several clinical outcome improvements across various chronic conditions, attributing these results to its technology-driven approach.

The Clover Assistant interface, shown below, integrates data from over 100 sources and utilizes more than 100 AI/ML models to generate personalized clinical insights:

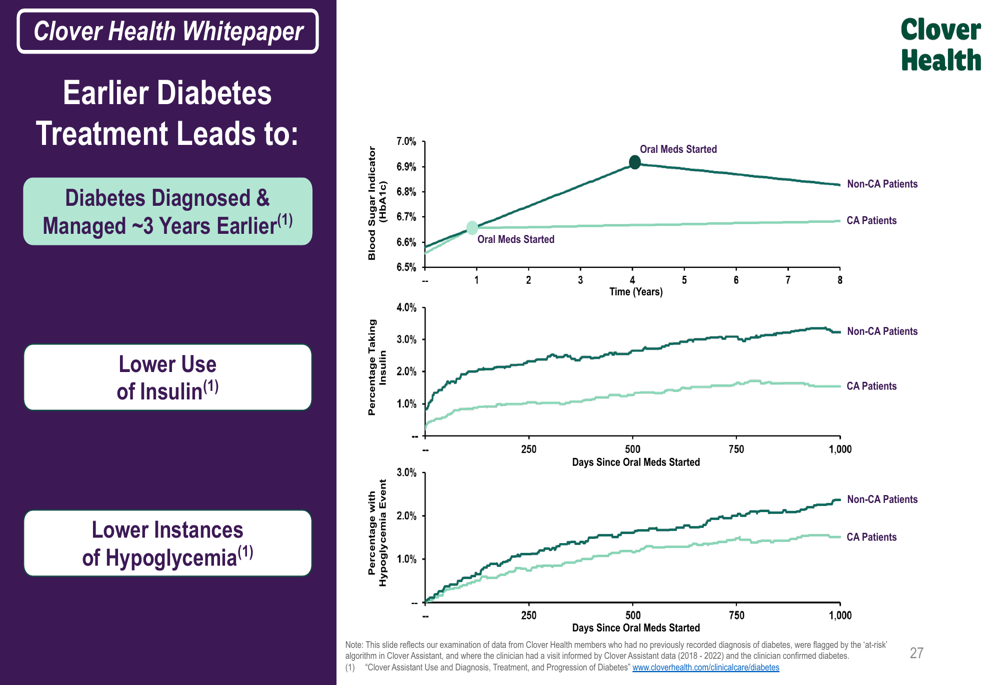

The company highlighted significant improvements in clinical outcomes for patients with chronic conditions. For diabetes patients, Clover’s approach led to earlier diagnosis and treatment, approximately 36 months sooner than traditional approaches, with lower insulin use and fewer hypoglycemic events:

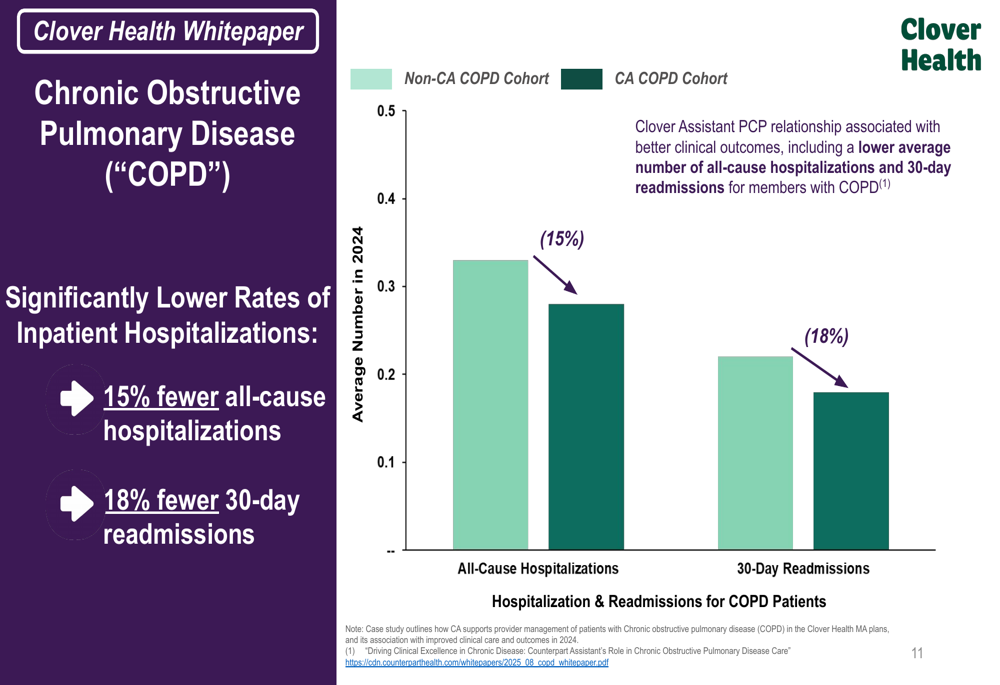

Similarly, for patients with Chronic Obstructive Pulmonary Disease (COPD), the company reported 15% fewer all-cause hospitalizations and 18% fewer 30-day readmissions:

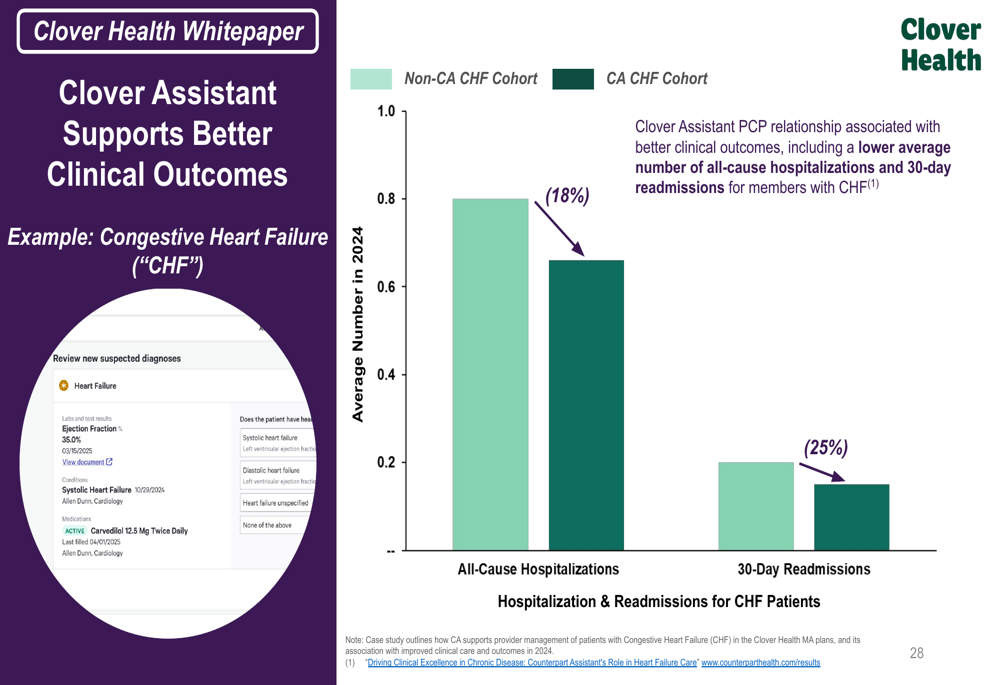

For Congestive Heart Failure (CHF) patients, the data showed even more significant improvements:

Forward-Looking Statements

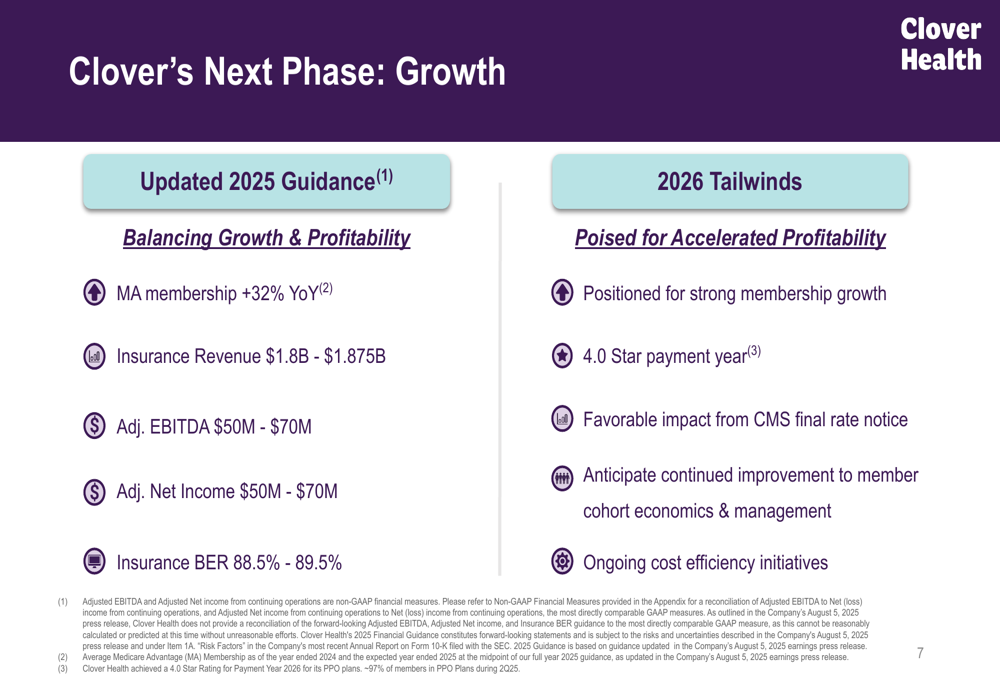

Clover Health updated its full-year 2025 guidance, projecting insurance revenue between $1.8 billion and $1.875 billion, with Adjusted EBITDA and Adjusted Net Income both in the range of $50 million to $70 million. The company expects average Medicare Advantage membership between 104,000 and 108,000, representing approximately 32% year-over-year growth.

The updated guidance and outlook for 2026 are detailed in the following slide:

A key positive development for 2026 is Clover’s achievement of a 4.0 Star rating for its PPO plans, up from 3.5 Stars in 2025. This improvement is expected to boost reimbursement rates and enhance the company’s competitive position in the Medicare Advantage market. The company also highlighted favorable impacts from the CMS final rate notice and ongoing cost efficiency initiatives as tailwinds for 2026.

Competitive Industry Position

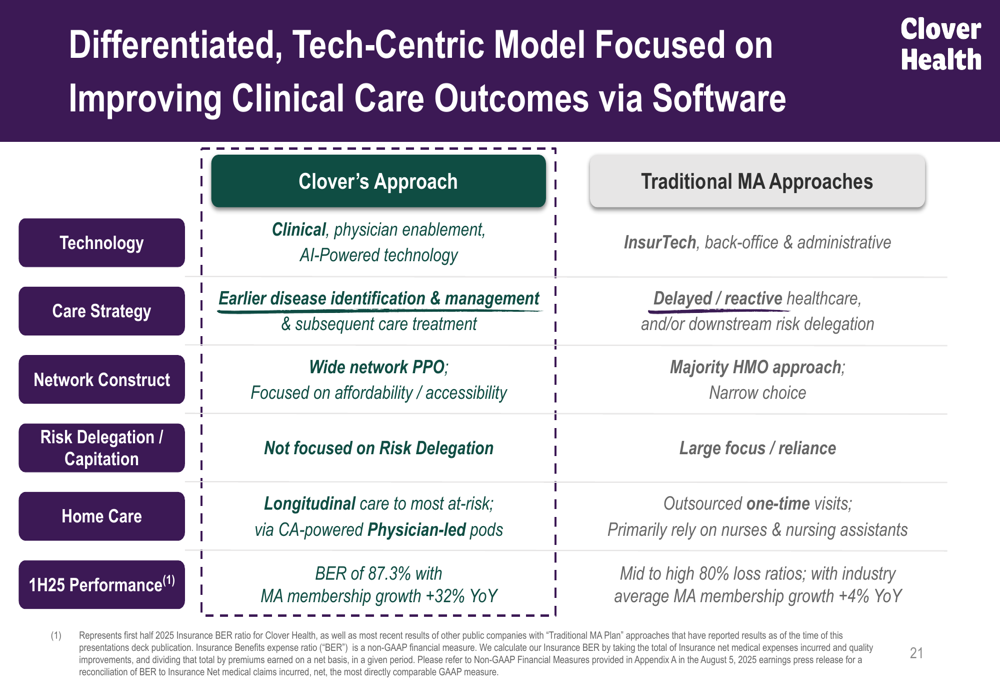

Clover Health emphasized its differentiated approach in the Medicare Advantage market, with 97% of its membership enrolled in PPO plans, contrasting with the industry’s predominant HMO model. The company positions itself as offering greater choice through wider networks while leveraging its technology platform to manage costs.

The following slide illustrates how Clover’s approach differs from traditional Medicare Advantage insurers:

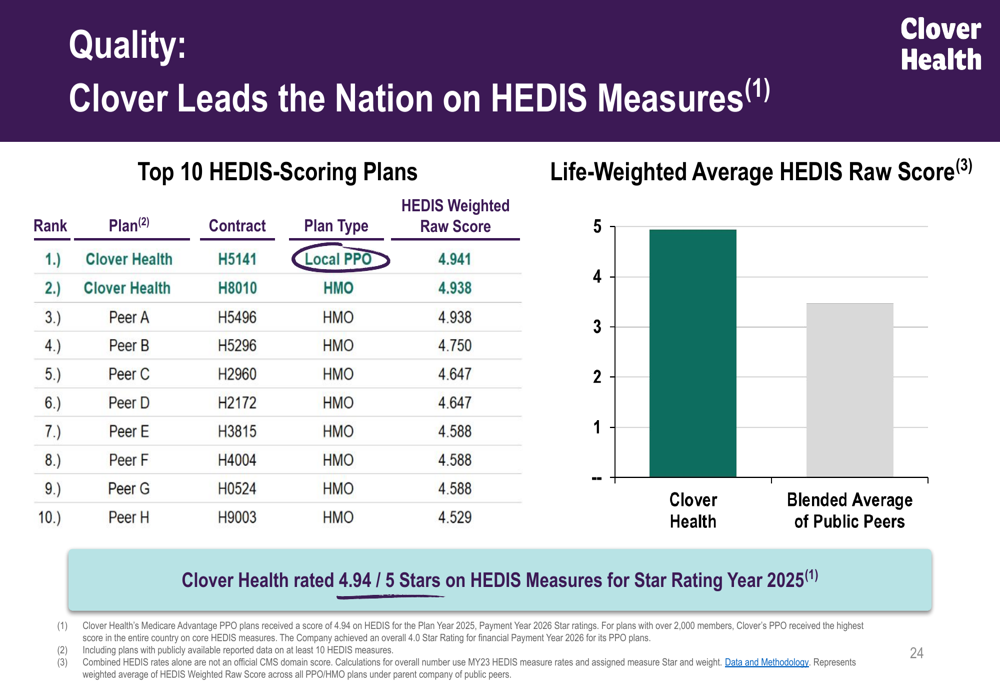

The company’s quality performance is another area of differentiation, with Clover achieving a 4.94 out of 5 Stars rating on HEDIS measures for Star Rating Year 2025:

Strategic Initiatives

Clover Health outlined its evolution through three phases: Innovation (2018), Profitability (2022), and Growth (2025 & Beyond). The company is now focused on the growth phase while maintaining the profitability achieved in recent years.

A key component of Clover’s strategy is its cohort management approach. The company presented data showing significant improvements in Medical (TASE:BLWV) Cost Ratio (MCR) as member cohorts mature, with approximately 700 basis points improvement in Year 2 and 1,500 basis points improvement in Year 3:

The company’s vision centers on empowering physicians with technology to identify, manage, and treat chronic diseases earlier. This approach aims to deliver better health outcomes while controlling costs through earlier intervention and more effective disease management.

Conclusion

Clover Health’s Q2 2025 results demonstrate the company’s ability to maintain profitability while significantly expanding its membership base in a challenging Medicare Advantage environment. The company’s technology-driven approach continues to show promising clinical outcomes, though elevated medical utilization remains a headwind.

Looking ahead, Clover is positioned for potential acceleration in both growth and profitability in 2026, benefiting from its improved Star rating and the maturing economics of its existing member cohorts. However, investors will be watching closely to see if the company can effectively manage medical costs while continuing its rapid expansion.

With $389 million in consolidated cash, cash equivalents, and investments, Clover appears well-capitalized to execute its growth strategy. The stock’s performance, currently trading well below its 52-week high of $4.87, suggests investors remain cautious about the company’s ability to navigate industry-wide challenges while delivering on its growth and profitability targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.