Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Commercial Metals Company (NYSE:CMC) presented its Q3 FY 2025 supplemental slides on June 23, 2025, highlighting sequential improvement across its business segments following a challenging second quarter. The company's stock was trading at $48.68 at the time of the presentation, with a slight premarket decline of 2.49% to $47.47.

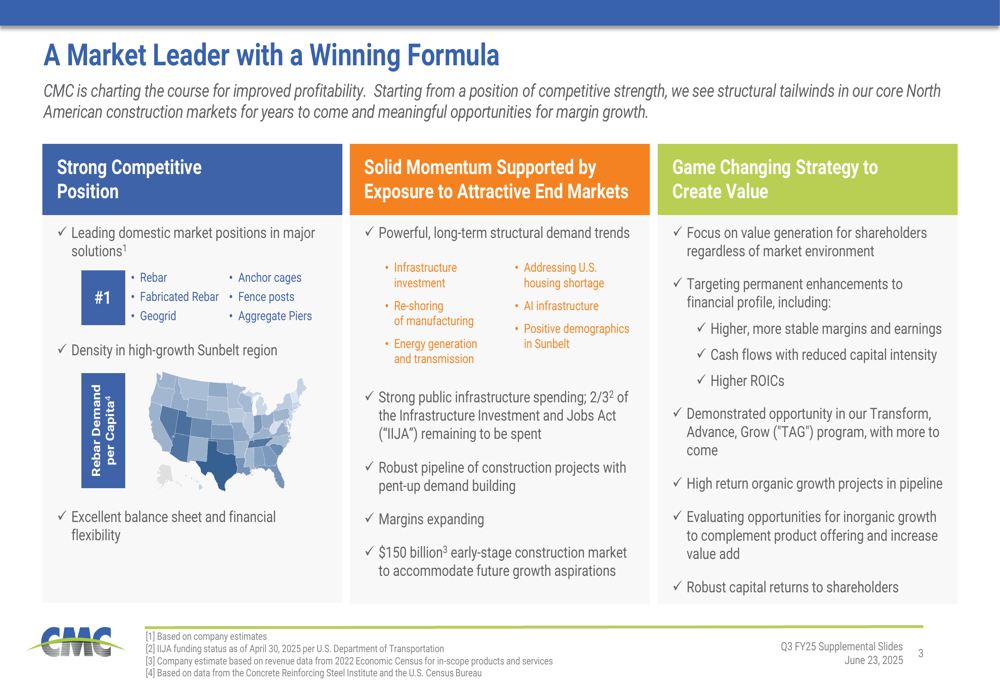

CMC positioned itself as a market leader with strong competitive advantages, particularly in the high-growth Sunbelt region where construction activity remains robust. The company emphasized its exposure to attractive end markets including infrastructure investment, manufacturing re-shoring, housing development, and AI infrastructure.

As shown in the following slide detailing CMC's market leadership and strategic positioning:

Quarterly Performance Highlights

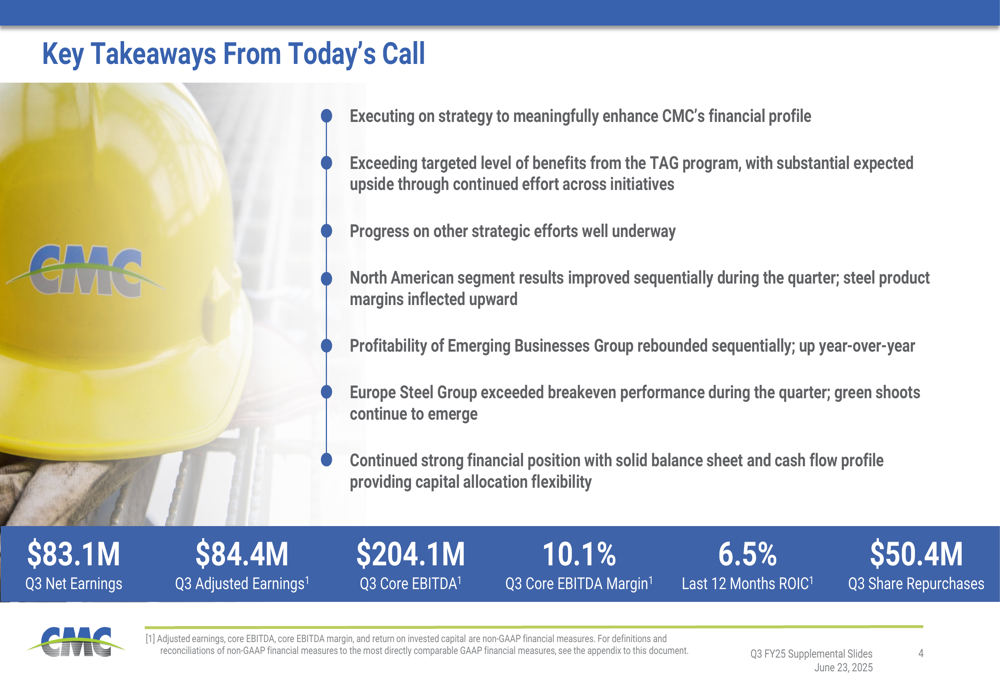

CMC reported Q3 net earnings of $83.1 million, adjusted earnings of $84.4 million, and core EBITDA of $204.1 million, representing a core EBITDA margin of 10.1%. The company achieved a last 12 months return on invested capital (ROIC) of 6.5% and completed $50.4 million in share repurchases during the quarter.

These results mark a significant improvement from the previous quarter when the company reported net earnings of $25.5 million and an EPS of $0.22 per diluted share, missing analyst expectations. The sequential improvement aligns with management's previous guidance that anticipated a financial rebound in Q3.

The following slide summarizes the key takeaways from the quarterly presentation:

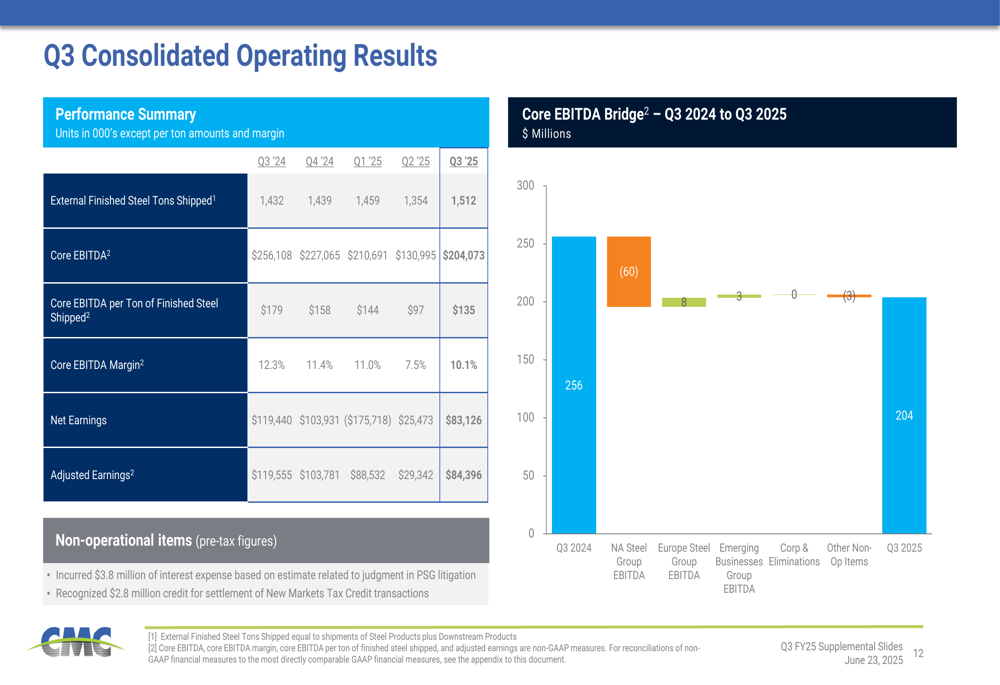

CMC's consolidated operating results show the company's performance trajectory over the past five quarters, with Q3 FY2025 showing improvement from the challenging Q2 period:

Strategic Initiatives

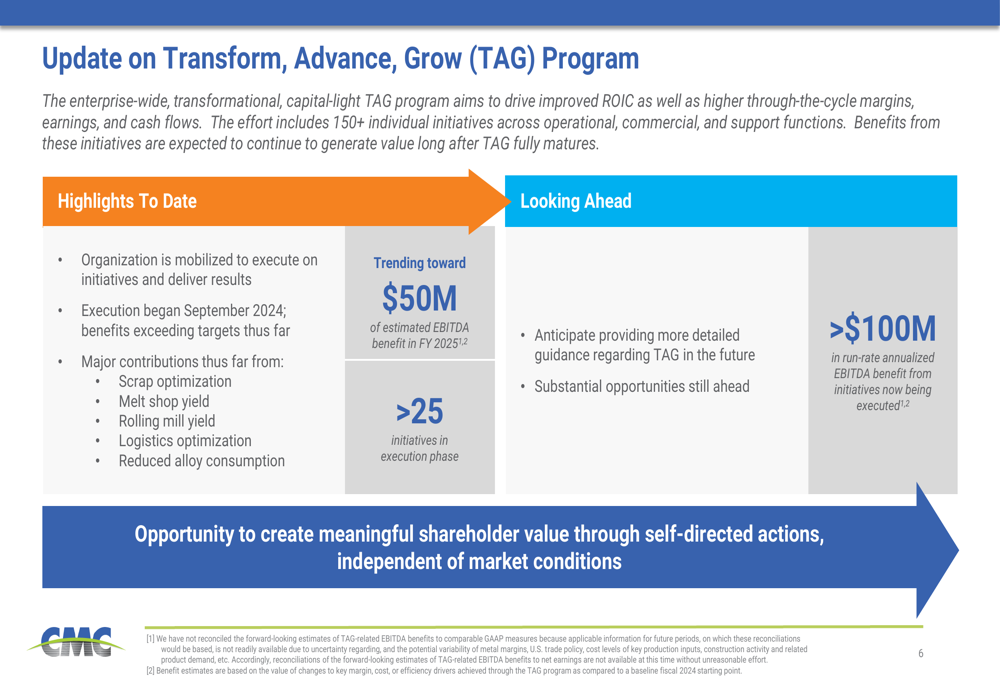

A centerpiece of CMC's strategy is its Transform, Advance, Grow (TAG) program, which aims to drive improved ROIC and higher through-the-cycle margins. The program is exceeding targets and trending toward $50 million of estimated EBITDA benefit in FY 2025, with a longer-term target of over $100 million in run-rate annualized EBITDA benefit.

The TAG program has already delivered significant results through initiatives focused on scrap optimization, melt shop yield, rolling mill yield, logistics optimization, and reduced alloy consumption. Management emphasized that this program creates "meaningful shareholder value through self-directed actions, independent of market conditions."

The following slide details the progress and expected benefits of the TAG program:

CMC is also pursuing a disciplined capital allocation strategy focused on growth and providing competitive cash distributions. The company reported capital expenditures of $293.9 million through the first nine months of FY 2025 and has $254.9 million remaining under its current share repurchase authorization.

Segment Performance Analysis

CMC's North America Steel Group showed sequential improvement during Q3, with steel product margins inflecting upward. However, year-over-year comparisons show some pressure, with adjusted EBITDA declining from $246,304 in Q3 FY2024 to $185,984 in Q3 FY2025, and adjusted EBITDA margin decreasing from 14.7% to 11.9%.

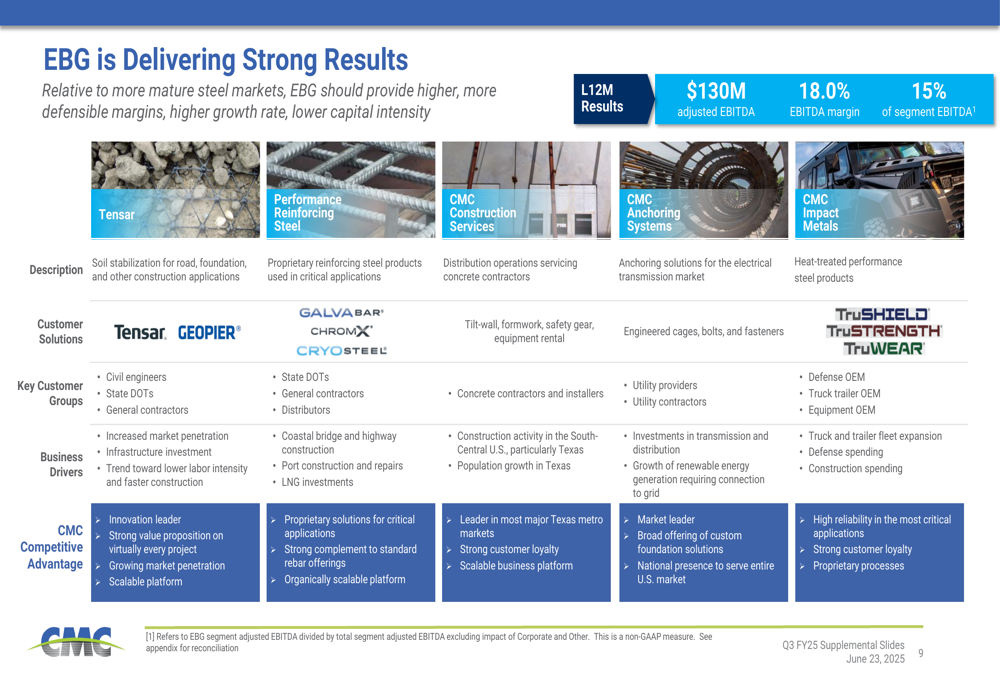

The Emerging Businesses Group (EBG) delivered particularly strong results, with adjusted EBITDA of $40,912 in Q3 FY2025, up 7.0% from $38,220 in Q3 FY2024. The EBG segment has achieved last 12 months adjusted EBITDA of $130 million with an impressive EBITDA margin of 18.0%, representing 15% of segment EBITDA.

As illustrated in the following slide, EBG offers higher margins, higher growth rates, and lower capital intensity compared to CMC's traditional steel business:

The Europe Steel Group exceeded breakeven performance during the quarter, posting adjusted EBITDA of $3,593 compared to a loss of $4,192 in the same period last year. Management pointed to "green shoots" in the European market, citing increasing EU funds, major projects entering the market, and expectations for accelerated economic growth in Poland.

Financial Strength and Capital Allocation

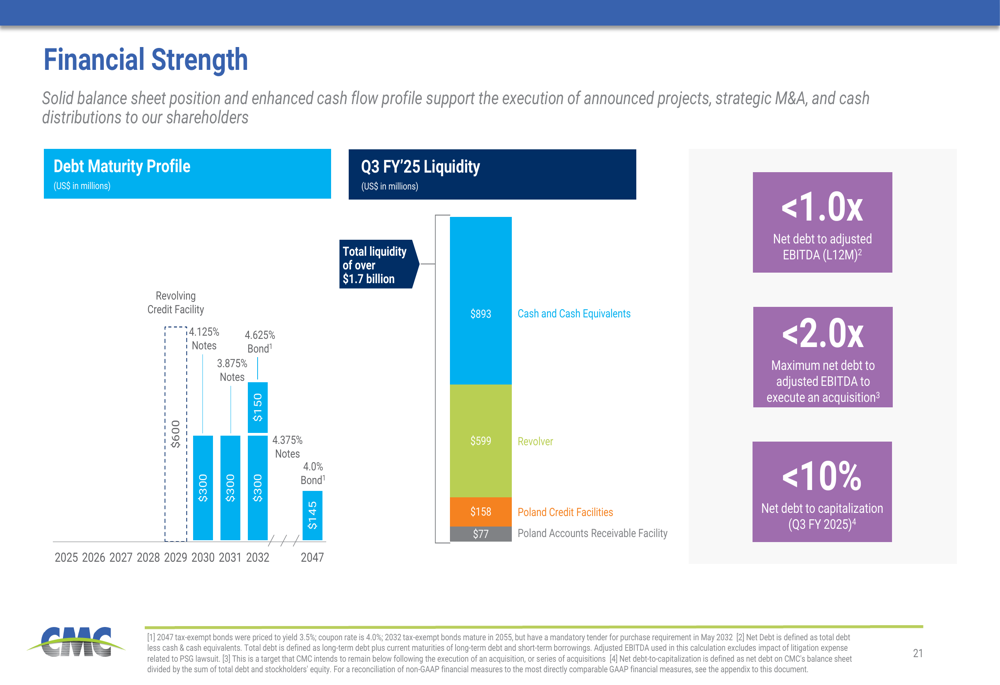

CMC emphasized its strong financial position, with a solid balance sheet and enhanced cash flow profile. The company reported Q3 FY2025 liquidity of $1.7 billion, comprising cash and cash equivalents of $893 million and various credit facilities.

Key financial metrics highlight CMC's conservative financial approach, with net debt to adjusted EBITDA (last 12 months) below 1.0x and net debt to capitalization (Q3 FY2025) below 10%. The company maintains a maximum net debt to adjusted EBITDA target of less than 2.0x for potential acquisitions.

The following slide details CMC's financial strength and liquidity position:

For inorganic growth, CMC has established a framework targeting businesses with EBITDA margins above 20% that are less volatile than current CMC levels, with solid underlying organic growth rates. The company is looking at transaction amounts sized between $500-$750 million, focusing on adding capabilities that complement its existing portfolio and extend its growth runway in the $150 billion early-stage construction market.

Sustainability Leadership

CMC positioned itself as a clear sustainability leader in the circular steel economy, highlighting its environmental performance compared to industry averages. The company's Scopes 1&2 greenhouse gas emissions intensity is 0.42 tCO2e per MT of steel, significantly lower than the global average of 1.8 and the U.S. average of 1.0.

Similarly, CMC's Scopes 1-3 GHG emissions intensity, energy intensity, and water withdrawal intensity all compare favorably to global industry averages, reinforcing the company's environmental leadership position.

The following slide illustrates CMC's sustainability metrics compared to industry benchmarks:

Forward-Looking Statements

Looking ahead to Q4 FY2025, CMC anticipates that consolidated financial results will improve from the third quarter level, with adjusted EBITDA for the Europe Steel Group expected to increase sequentially.

The company highlighted several positive market factors supporting its outlook, including resilient demand for long steel products in North America, with finished steel shipments increasing 1.6% year-over-year. The Dodge Momentum Index remains near all-time highs, indicating a robust project pipeline, and rebar consumption is expected to be supported by strong public sector construction spending.

CMC also noted the impact of tariffs on its business, which have restricted import levels, with imports representing approximately 11% of the rebar market and 12% of the merchant market. While tariffs have created some uncertainty related to project costs and delayed some projects not under contract, they are also intended to boost U.S. manufacturing and should lead to increased investment in industrial capacity.

Overall, CMC's Q3 FY2025 presentation portrays a company executing effectively on its strategic initiatives and benefiting from favorable market conditions, particularly in North America. The sequential improvement across segments and the success of the TAG program provide a foundation for continued performance improvement in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.