European stocks retreat on tech valuation concerns; U.K. economic woes

Introduction & Market Context

Empresas CMPC (SNSE:CMPC) presented its first-quarter 2025 results on May 9, showing a significant recovery in net income from the previous quarter despite continued year-over-year declines across most metrics. The Chilean forestry and paper products company reported mixed performance across its business segments, with its stock trading at 1,438 Chilean pesos, up 0.4% on the day of the presentation.

The company’s results come amid challenging global market conditions for the paper and forestry products industry, with CMPC working to balance operational efficiency with strategic growth initiatives. The presentation highlighted both achievements and ongoing challenges as the company navigates volatile commodity prices and varying demand across its product portfolio.

Quarterly Performance Highlights

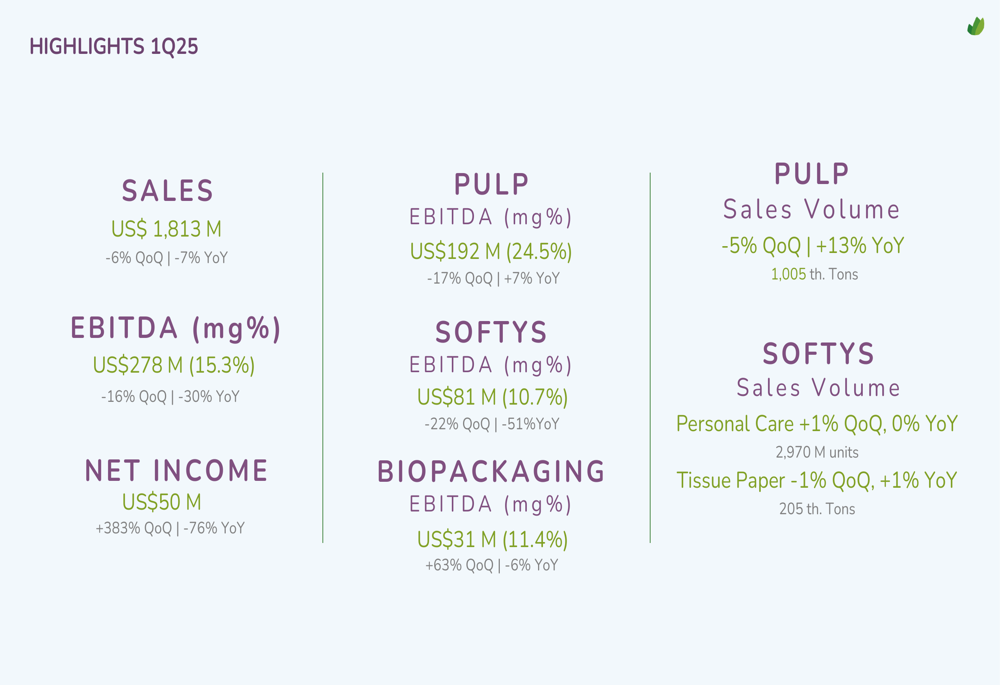

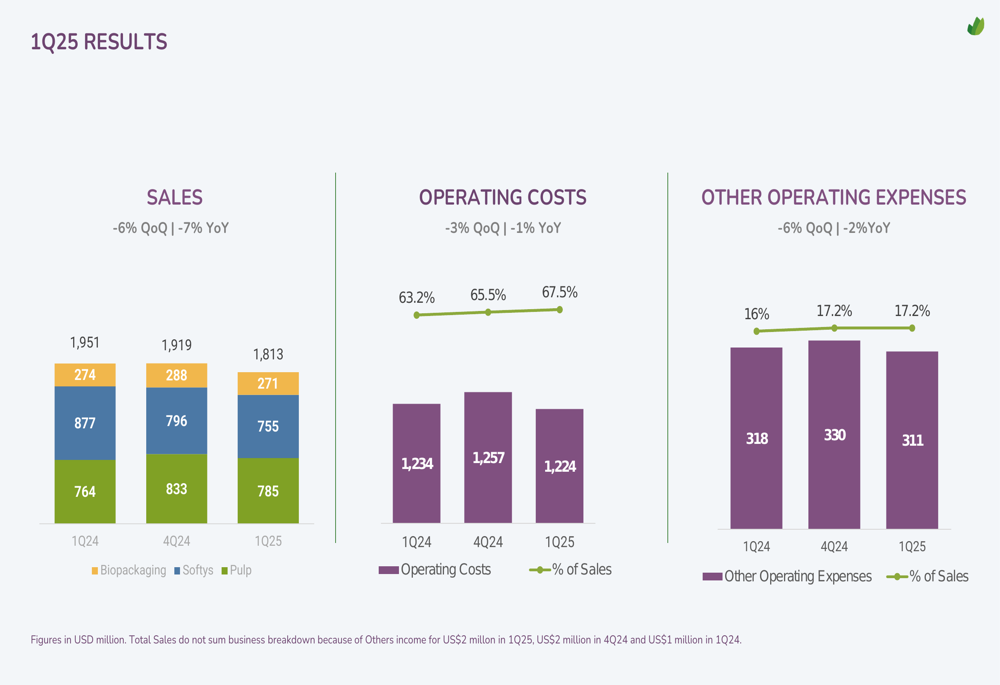

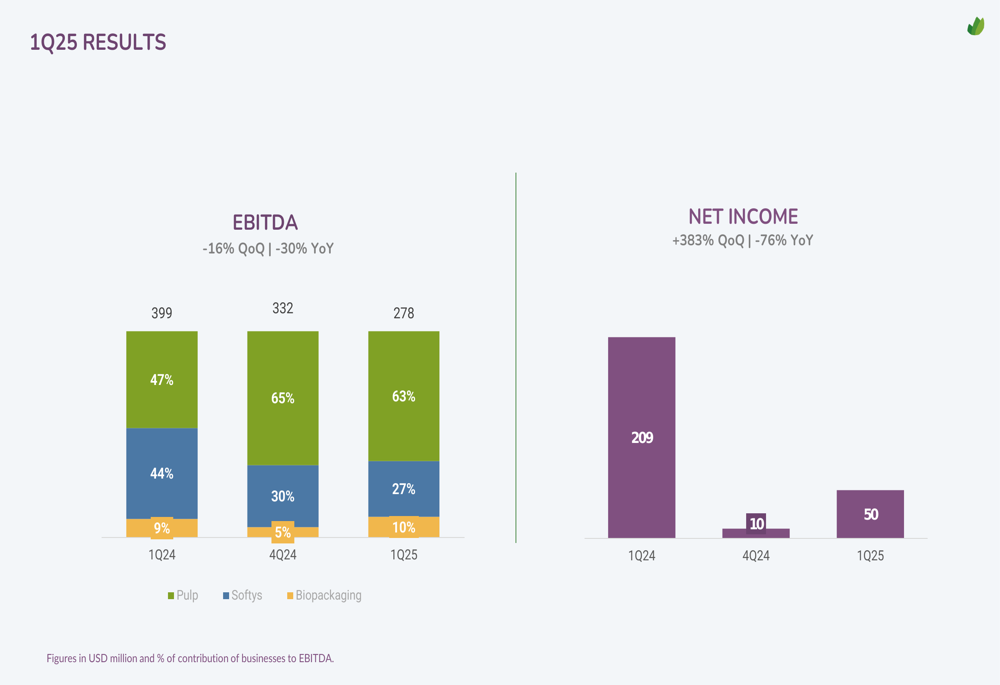

CMPC reported first-quarter 2025 sales of $1,813 million, representing a 6% decrease quarter-over-quarter and a 7% decline year-over-year. EBITDA came in at $278 million with a 15.3% margin, down 16% from the previous quarter and 30% compared to the same period last year. Despite these declines, net income showed a remarkable recovery, reaching $50 million – a 383% increase from Q4 2024, though still 76% below Q1 2024 levels.

As shown in the following chart of key financial metrics:

The company’s operating costs totaled $1,224 million in Q1 2025, representing 67.5% of sales – an increase from 65.5% in Q4 2024 and 63.2% in Q1 2024. This trend indicates growing pressure on margins, as illustrated in the following breakdown:

EBITDA contributions varied significantly across business segments, with Pulp accounting for 63% of total EBITDA, Softys contributing 27%, and Biopackaging representing 10%. This distribution reflects the continued strength of the Pulp segment despite market challenges.

Segment Analysis

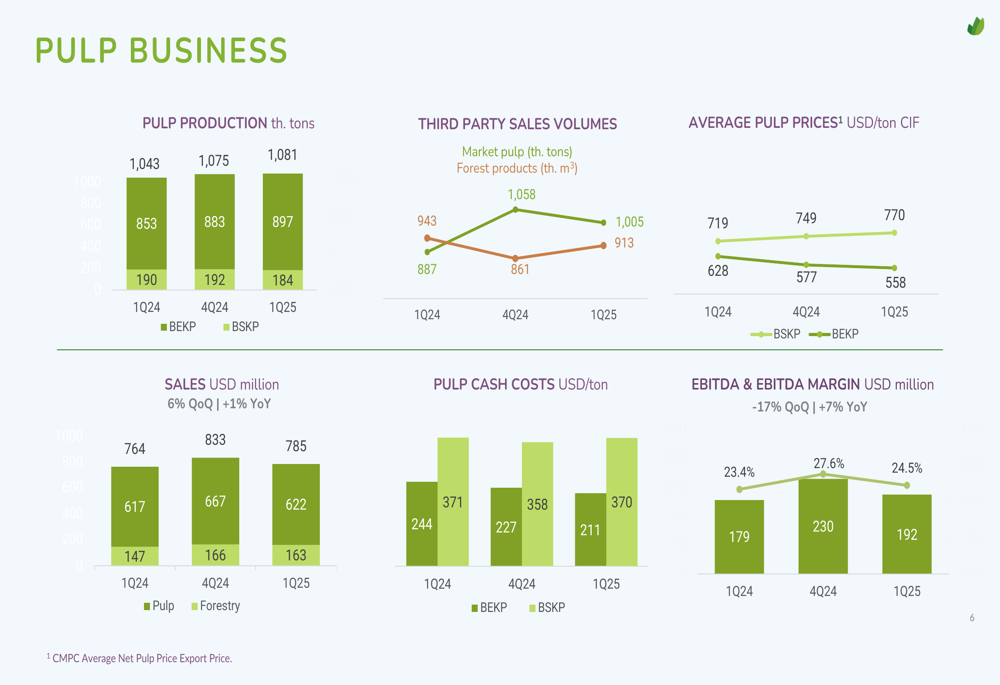

The Pulp segment remained CMPC’s strongest performer, generating $192 million in EBITDA with a 24.5% margin. While this represents a 17% decrease quarter-over-quarter, it shows a 7% improvement year-over-year. Pulp production reached 1,081 thousand tons, with sales volumes of 861 thousand tons, down 5% from the previous quarter but up 13% year-over-year.

The segment benefited from improved production efficiency and lower cash costs for BEKP (Bleached Eucalyptus Kraft Pulp), which decreased to $211 per ton from $227 in Q4 2024. However, average BEKP prices also declined to $558 per ton from $577 in the previous quarter, partially offsetting cost improvements.

As illustrated in the comprehensive pulp business metrics:

The Softys segment, which includes tissue and personal care products, continued to face significant challenges. EBITDA fell to $81 million with a 10.7% margin, representing a 22% decrease from Q4 2024 and a concerning 51% drop year-over-year. Sales volumes remained relatively stable with personal care products at 2,970 million units (+1% QoQ) and tissue paper at 205 thousand tons (-1% QoQ).

The following chart shows the declining performance trend in the Softys segment:

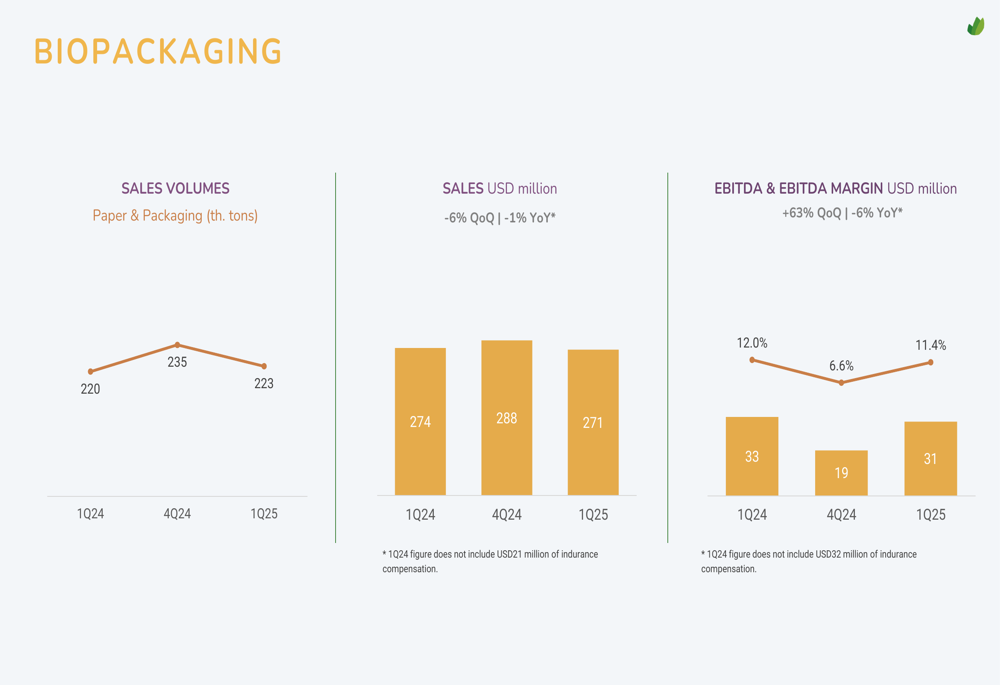

In contrast, the Biopackaging segment showed signs of recovery, with EBITDA increasing 63% quarter-over-quarter to $31 million, though still down 6% year-over-year. The segment’s EBITDA margin improved to 11.4% from 6.6% in Q4 2024, demonstrating operational improvements despite relatively flat sales volumes of 223 thousand tons.

Financial Position and Cash Flow

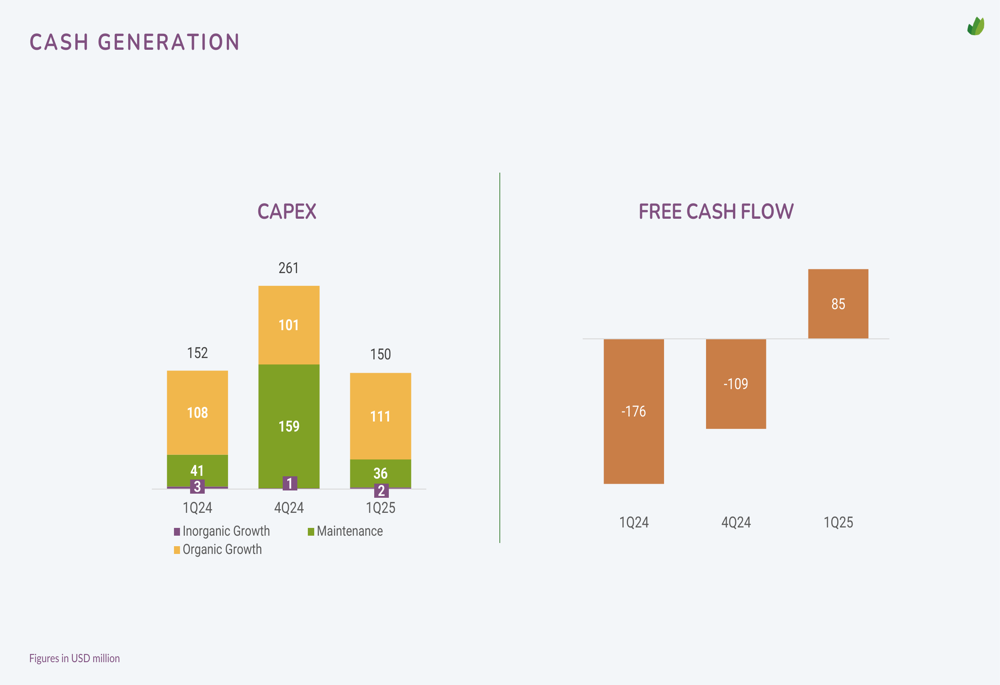

CMPC’s financial position showed notable improvement in cash generation, with free cash flow turning positive at $85 million in Q1 2025, compared to negative $109 million in Q4 2024 and negative $176 million in Q1 2024. This positive development came despite continued capital expenditures of $150 million, primarily directed toward organic growth initiatives ($111 million).

The following chart illustrates this significant improvement in cash flow:

The company’s debt profile remains a concern, with total debt of $5,509 million and net debt of $4,843 million as of Q1 2025. The net debt to EBITDA ratio increased to 3.41x from 3.15x in the previous quarter, reflecting the impact of lower EBITDA on leverage metrics. CMPC maintains an average debt term of 5.50 years with an average interest rate of 4.74%.

Strategic Initiatives and Outlook

During the quarter, CMPC highlighted several strategic developments that position the company for future growth. The company was ranked among the top 1% of sustainable companies in the S&P Global Sustainability Yearbook for the second consecutive year, reinforcing its environmental credentials.

In line with its growth strategy, Softys acquired Falcon Distribuição in Brazil, including a production plant for diapers, strengthening its position in the personal care market. Meanwhile, CMPC divested its non-core asset TENSA (Transmisora de Energía Nacimiento S.A.), a transmission operator in Portugal, to Transemel S.A., focusing resources on core business areas.

The company’s 106th Annual General Meeting resulted in the appointment of Bernardo Larraín Matte as the new Chairman, while maintaining its dividend policy at 30% of distributable net income.

Looking ahead, CMPC faces continued challenges in the Softys segment, which will require strategic attention to reverse declining margins. The Pulp segment appears relatively stable despite price pressures, while Biopackaging shows promising signs of recovery. The company’s improved free cash flow generation provides greater financial flexibility, though high debt levels remain a consideration for future investment decisions.

The positive net income trend compared to Q4 2024 suggests operational improvements are beginning to take effect, but year-over-year comparisons indicate CMPC still has significant ground to recover to return to previous performance levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.