Jamaica’s outlook revised to stable by Fitch after hurricane

Introduction & Market Context

Empresas CMPC (SNSE:CMPC) released its second quarter 2025 earnings presentation on August 8, showing sequential improvement in key financial metrics despite year-over-year challenges. The Chilean forestry and paper products company, currently trading at 1,465 Chilean pesos (up 1.11% on the day), demonstrated resilience in a challenging global pulp market environment.

The company's Q2 results follow a first quarter that had already shown signs of recovery, with CMPC continuing to navigate pulp price pressures while implementing its 2030 strategic plan. The latest presentation reveals a company in transition, balancing operational improvements with significant capital investments.

Quarterly Performance Highlights

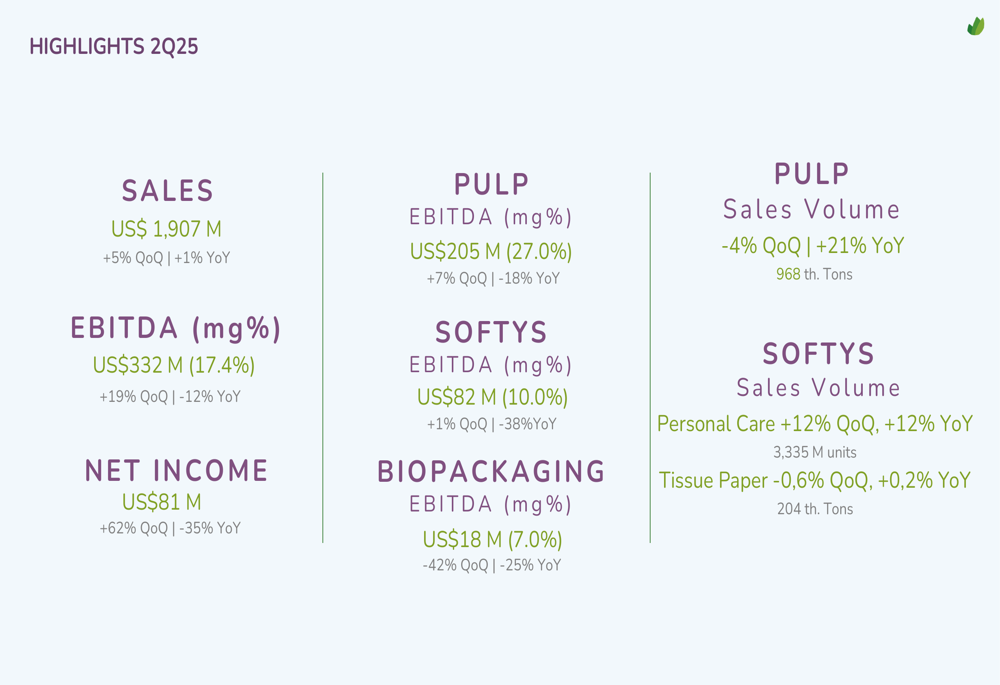

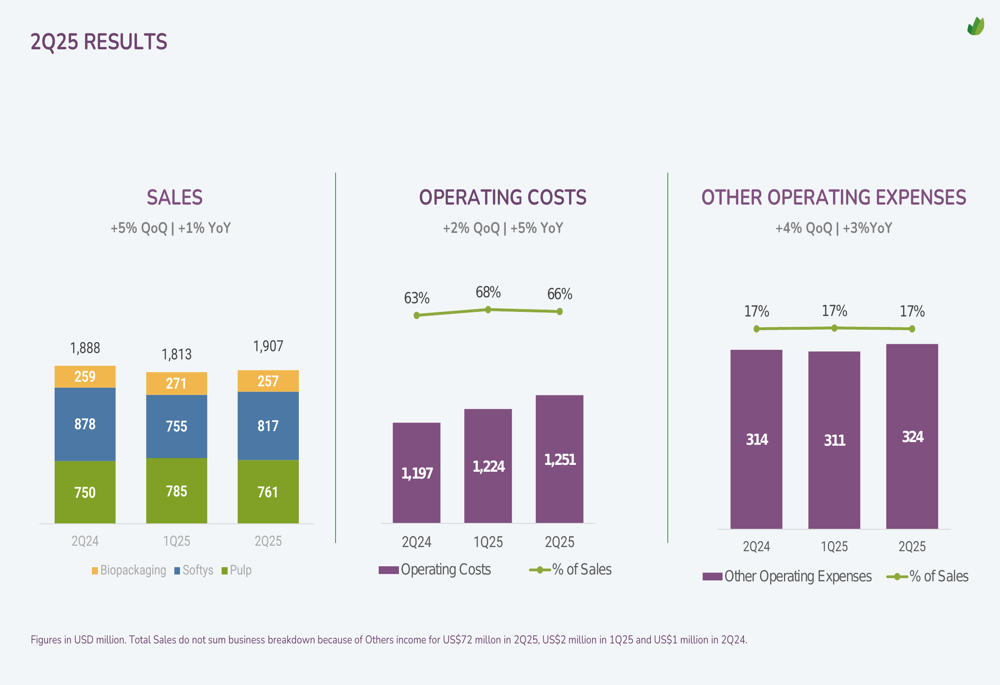

CMPC reported second quarter sales of US$1,907 million, representing a 5% increase from the previous quarter and a modest 1% gain year-over-year. More impressively, EBITDA jumped 19% quarter-over-quarter to US$332 million, though this figure remains 12% below the same period last year. The EBITDA margin stood at 17.4%.

Net income showed the strongest sequential improvement, surging 62% from Q1 to reach US$81 million, though still 35% below Q2 2024 levels. This continues the recovery trend seen in Q1, when the company reported US$50 million in net income.

As shown in the following chart of quarterly financial highlights:

The company's operating costs increased 2% quarter-over-quarter and 5% year-over-year to US$1,251 million, representing 66% of sales. This marks a slight improvement from the 68% ratio seen in Q1 2025, suggesting some success in cost management initiatives.

The breakdown of sales and costs across quarters illustrates both challenges and improvements:

Segment Analysis

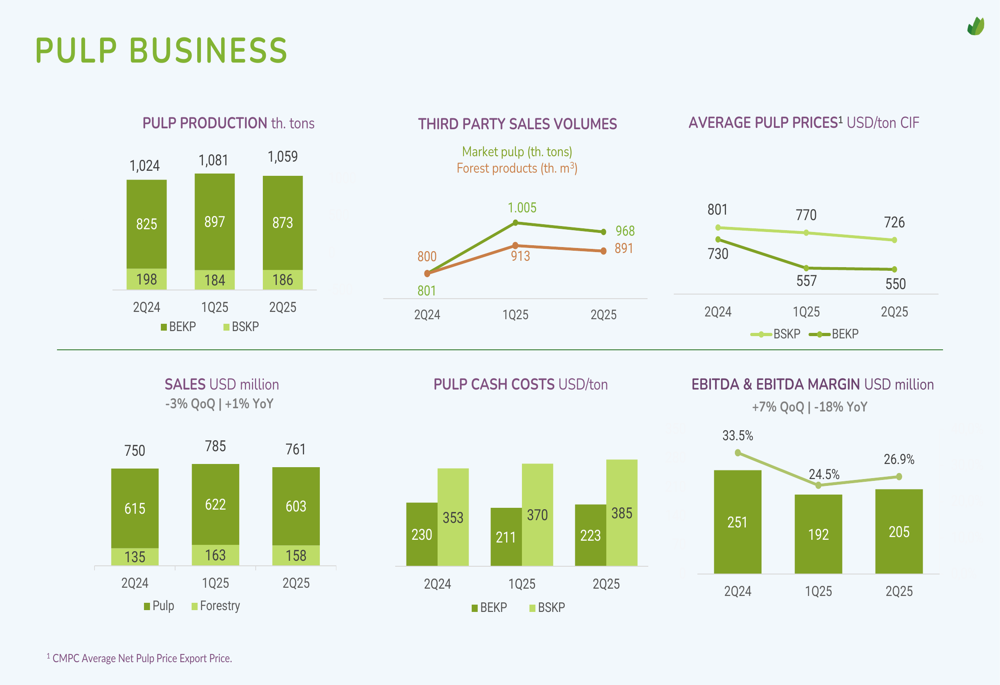

CMPC's pulp business remained the strongest performer, contributing 67% of total EBITDA in Q2 2025. The segment generated US$205 million in EBITDA (26.9% margin), up 7% from the previous quarter but down 18% year-over-year. Pulp production reached 1,059 thousand tons, slightly below the 1,081 thousand tons produced in Q1.

Notably, pulp prices continued to face pressure, with Bleached Softwood Kraft Pulp (BSKP) averaging US$550 per ton in Q2, down from US$557 in Q1 and significantly below the US$730 seen a year ago. Bleached Eucalyptus Kraft Pulp (BEKP) prices also declined to US$726 per ton from US$770 in Q1.

The detailed pulp segment performance shows the balance between volume and price dynamics:

The Softys business, which includes tissue and personal care products, delivered US$82 million in EBITDA (10.0% margin), a marginal 1% improvement from Q1 but 38% lower than Q2 2024. Personal care sales volumes showed robust growth of 12% both quarter-over-quarter and year-over-year, reaching 3,335 million units. Tissue paper volumes remained relatively stable at 204 thousand tons.

The following chart details the Softys segment performance:

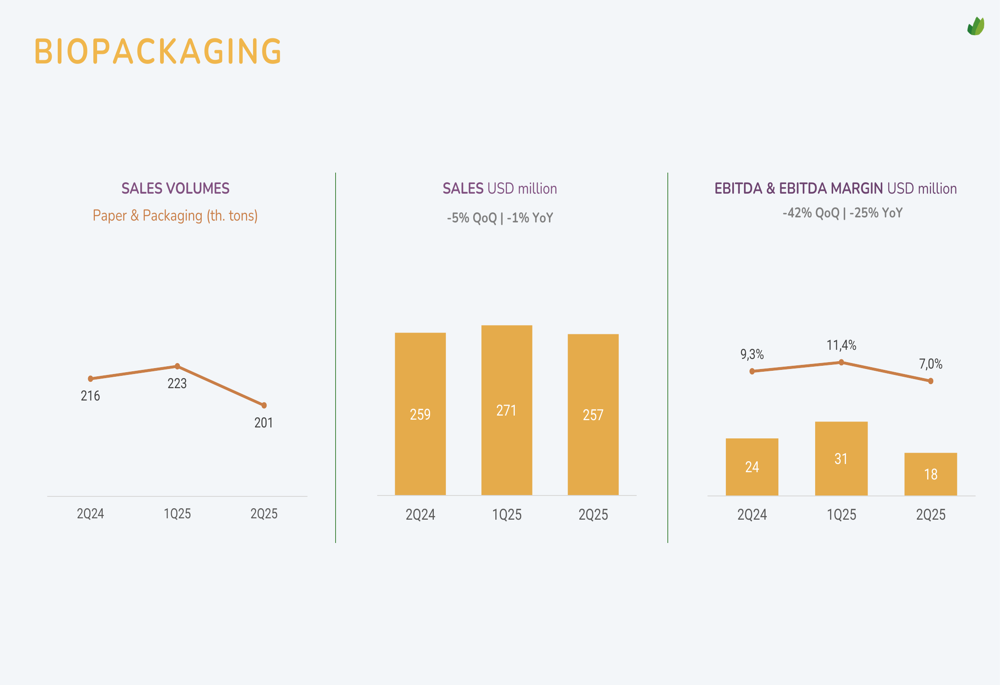

The Biopackaging segment experienced the most significant challenges, with EBITDA falling 42% quarter-over-quarter and 25% year-over-year to US$18 million, representing a 7.0% margin. Sales volumes declined to 201 thousand tons from 223 thousand tons in Q1.

Capital Expenditure and Debt Position

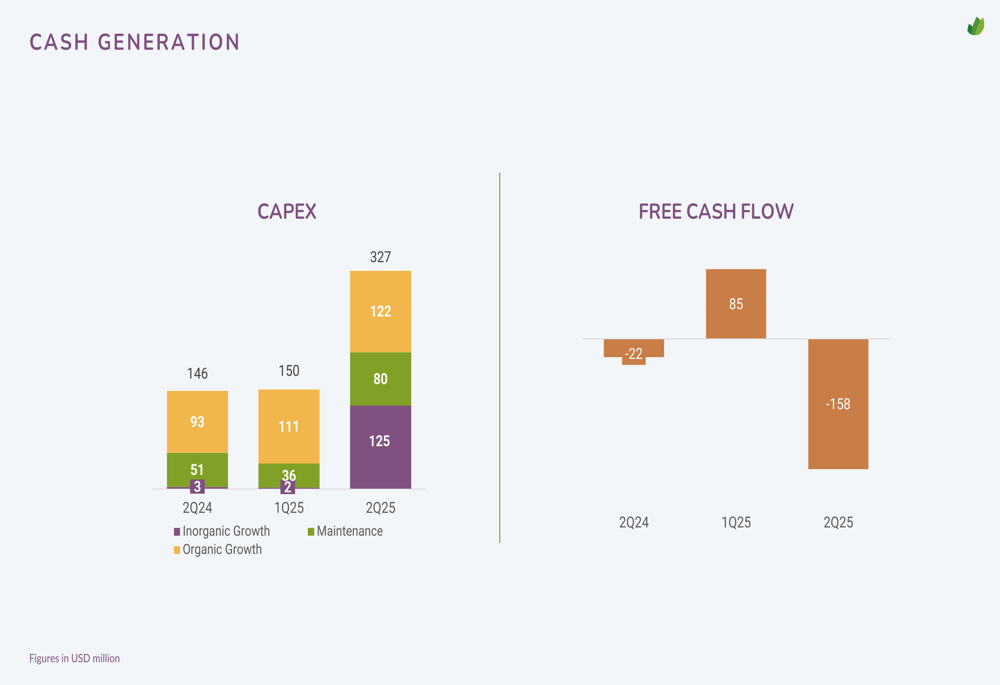

One of the most notable aspects of CMPC's Q2 results was the substantial increase in capital expenditures, which more than doubled to US$327 million from US$150 million in Q1. This significant investment was distributed across inorganic growth (US$125 million), organic growth (US$80 million), and maintenance (US$122 million).

The increased capital spending contributed to a negative free cash flow of US$158 million for the quarter, a sharp reversal from the positive US$85 million generated in Q1 2025.

The following chart illustrates this significant shift in capital allocation:

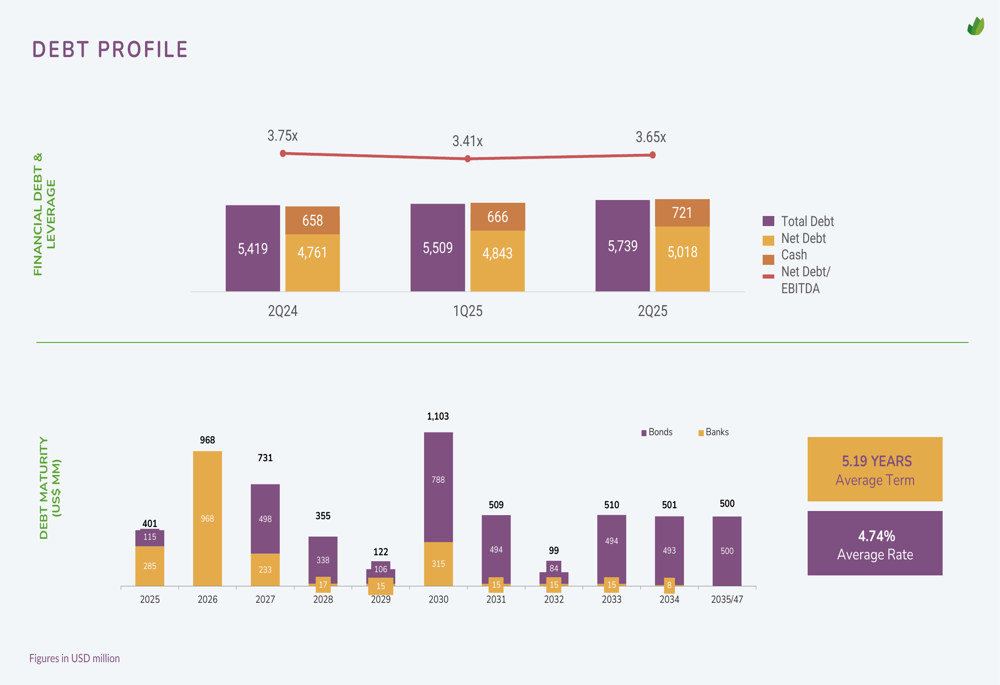

The company's debt profile shows total debt of US$5,739 million and net debt of US$5,018 million as of Q2 2025. The net debt to EBITDA ratio increased to 3.65x from 3.41x in the previous quarter, moving further from the company's previously stated goal of reducing leverage below 3x by year-end.

CMPC maintains an average debt term of 5.19 years with an average interest rate of 4.74%. The debt maturity schedule shows significant repayments due in 2025 (US$968 million) and 2026 (US$731 million), which may require refinancing given the current negative free cash flow.

Strategic Initiatives and Outlook

The presentation highlighted CMPC's progress on its 2030 Strategy, including the implementation of a new operational model featuring 10 vice presidencies. The company also conducted an Investor Site Visit at its Guaíba, Brazil facility during the quarter.

While the presentation did not provide specific forward guidance, the sequential improvements in financial metrics suggest a gradual recovery trajectory. However, the significant increase in capital expenditures indicates CMPC is prioritizing long-term strategic investments despite near-term cash flow impacts.

The company faces several challenges moving forward, including continued pressure on pulp prices, the need to improve margins in the Softys and Biopackaging segments, and managing its increasing leverage ratio. The substantial capital investments suggest confidence in future growth opportunities, but also raise questions about the timeline for returns on these investments.

For investors, CMPC's Q2 2025 results present a mixed picture - operational improvements and sequential earnings growth are positive signs, but increased spending and leverage may create near-term financial pressure as the company positions itself for its longer-term strategic vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.