Stock market today: S&P 500 falls as government shutdown, trade jitters persist

Introduction & Market Context

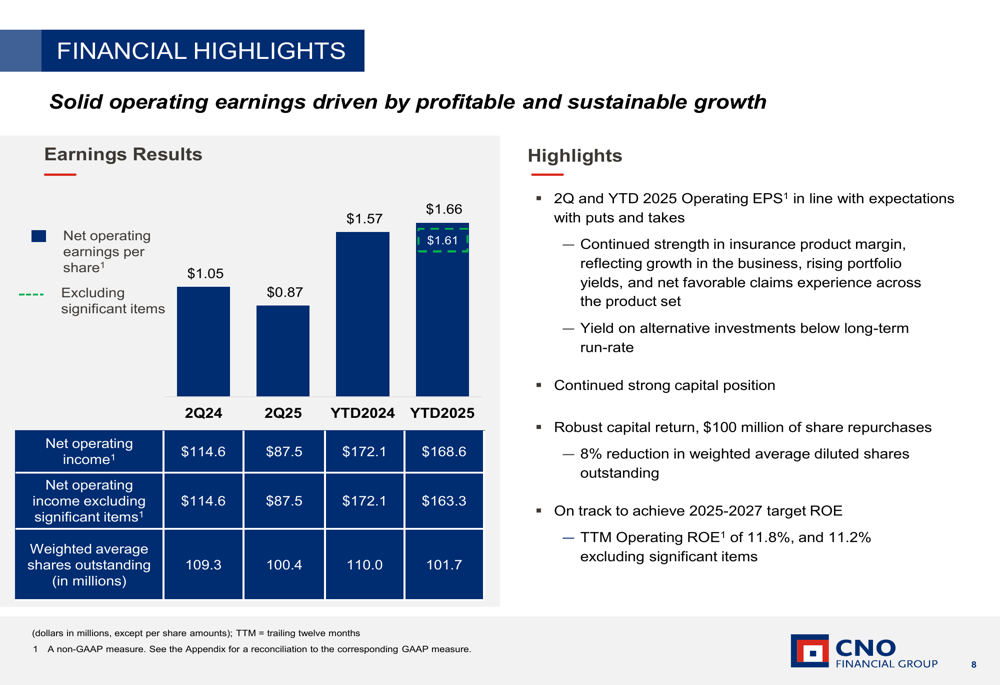

CNO Financial Group (NYSE:CNO) presented its second quarter 2025 results on July 28, highlighting consistent growth across key metrics while maintaining a solid capital position. The company reported operating earnings per share of $0.87 and an operating return on equity of 11.2% excluding significant items, demonstrating progress toward its long-term ROE targets.

Despite the positive operational results, CNO’s stock showed mixed market reaction, rising 1.84% to $39.40 during the regular trading session on October 14, but declining 1.52% to $38.80 in premarket trading the following day, suggesting some investor caution despite the company’s growth narrative.

Quarterly Performance Highlights

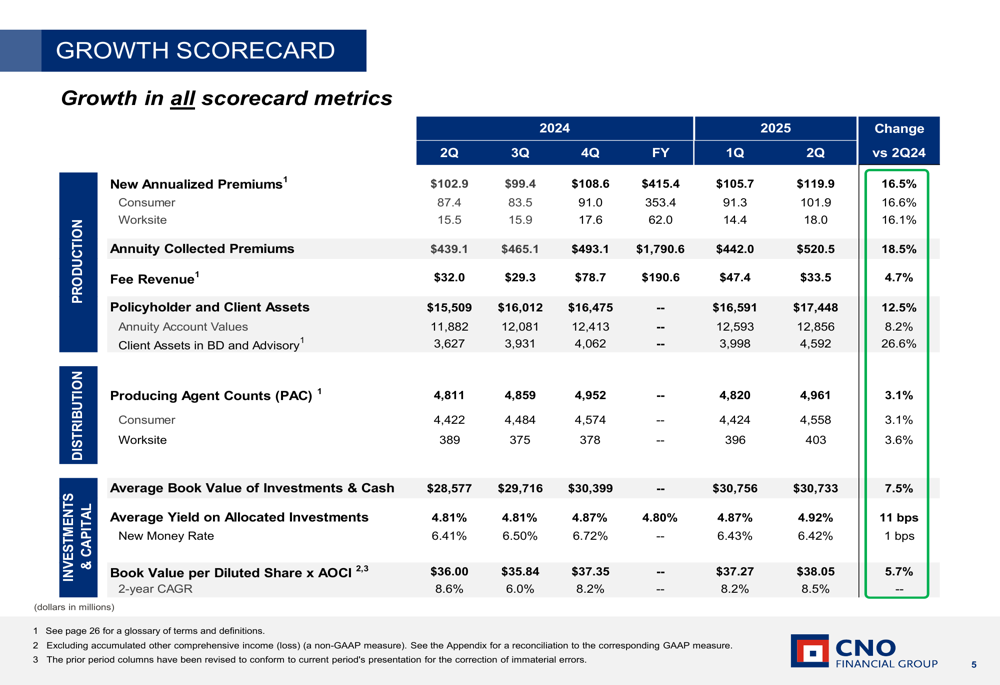

CNO reported its 12th consecutive quarter of strong sales momentum, with total new annualized premiums up 16.5% year-over-year to $119.9 million. Annuity collected premiums increased 18.5% to $520.5 million, while fee revenue grew 4.7% to $33.5 million.

As shown in the following growth scorecard, policyholder and client assets increased 12.5% to $17.4 billion, with particularly strong growth in client assets in brokerage and advisory, which surged 26.6% to $4.59 billion:

The company’s producing agent count grew for the 10th consecutive quarter, rising 3.1% to 4,961 agents. This growth in distribution capacity helped drive the consistent sales performance across product lines.

Detailed Financial Analysis

CNO’s operating earnings per share of $0.87 for Q2 2025 was in line with management expectations, though down from $1.05 in Q2 2024. The company attributed this to various offsetting factors, including strong insurance product margins balanced by alternative investment income below long-term run-rate expectations.

The following chart illustrates the company’s net operating earnings per share performance:

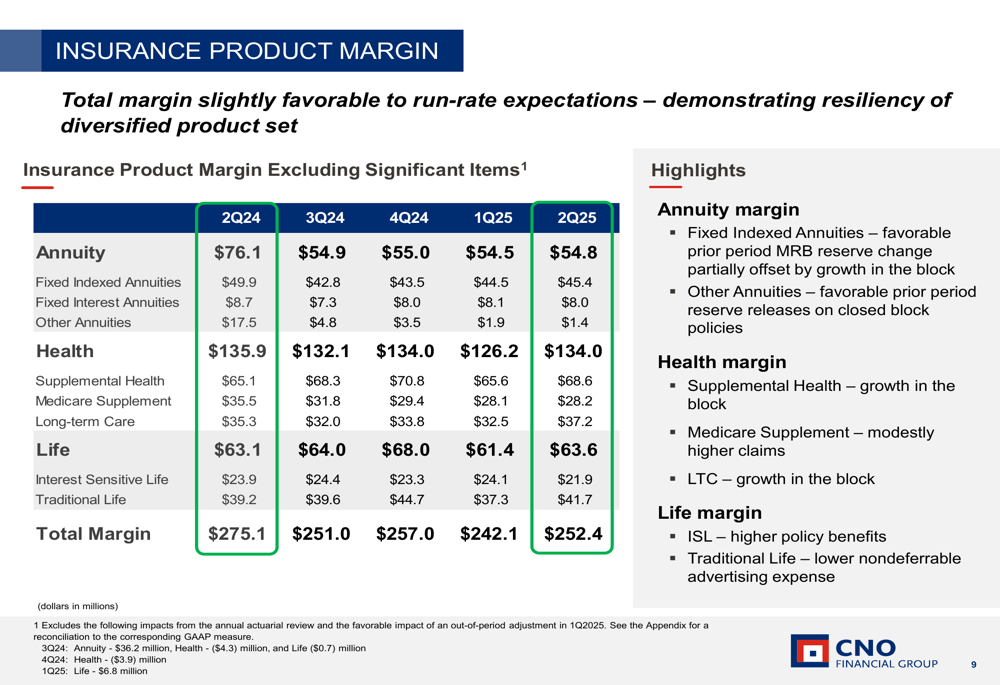

Insurance product margins demonstrated the resilience of CNO’s diversified product portfolio, with total margin at $252.4 million compared to $275.1 million in the prior-year period. Supplemental health showed particularly strong performance with margins increasing from $65.1 million to $68.6 million year-over-year.

The breakdown of insurance product margins by segment provides insight into the performance of different product lines:

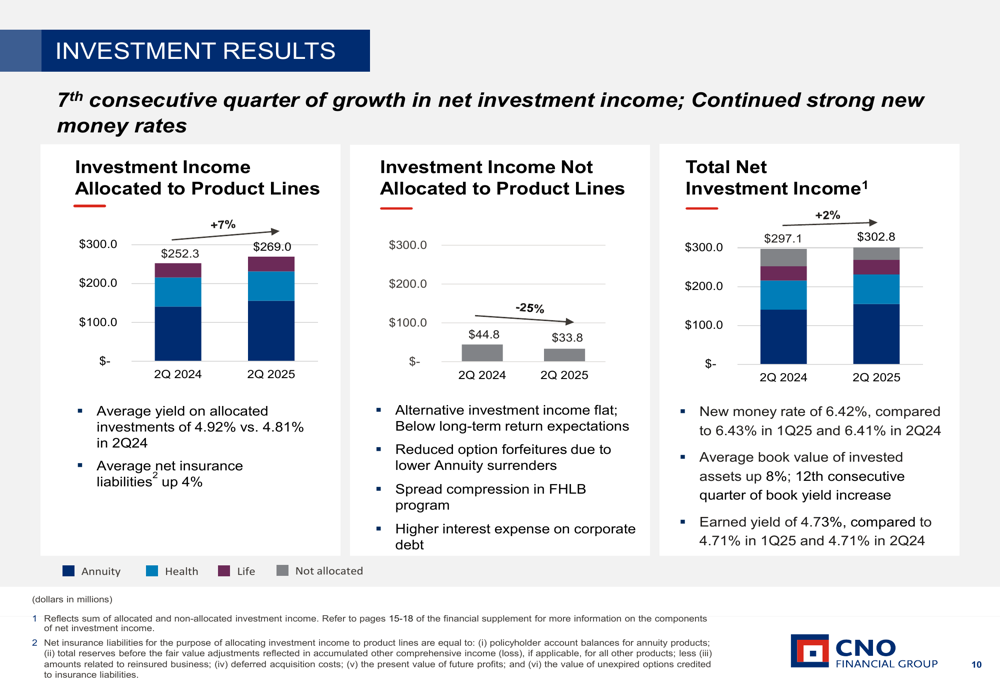

Investment performance remained solid with net investment income increasing 2% year-over-year to $302.8 million. The company maintained a strong new money rate of 6.42%, consistent with the 6.41% rate in Q2 2024, marking the 10th consecutive quarter with rates above 6%.

The following chart shows the components of net investment income:

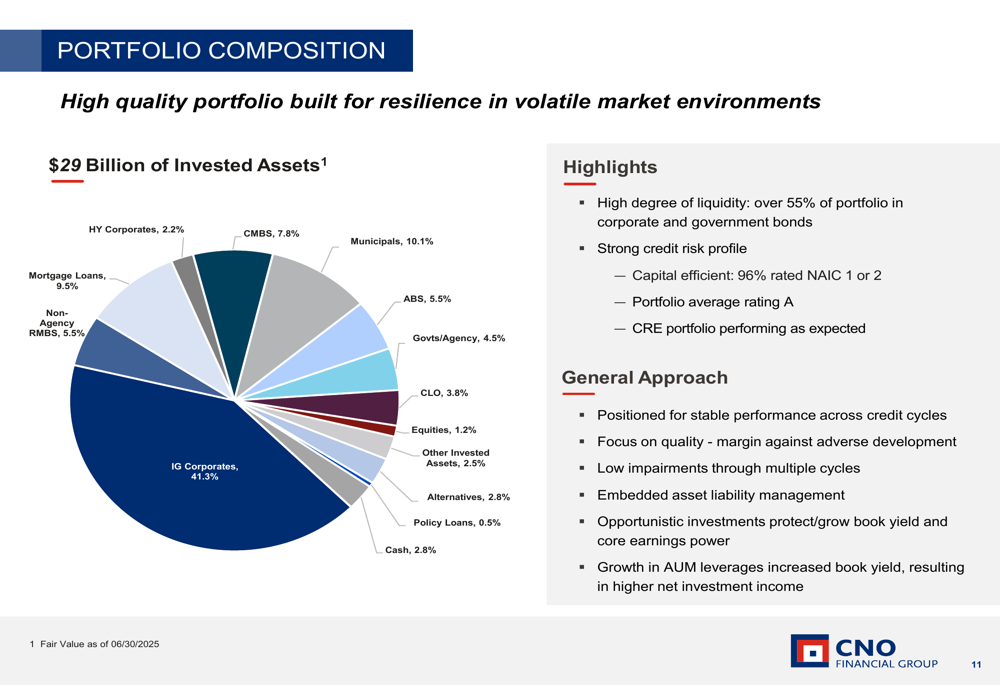

CNO’s investment portfolio remains high-quality and diversified, with 41.3% in investment-grade corporates and significant allocations to municipals (10.1%), mortgage loans (9.5%), and commercial mortgage-backed securities (7.8%):

Strategic Initiatives

The company’s digital transformation efforts continue to yield results, with web and digital channels generating 30% of total direct-to-consumer sales, up 39% year-over-year. Additionally, CNO achieved an 89% instant decision rate on eligible Simplified Issue Life business, up 12% from the prior year.

The Consumer Division reported its 11th consecutive quarter of sustained growth, with nearly all products showing double-digit increases. Life NAP grew 20%, driven by record direct-to-consumer NAP (up 29%), while health NAP increased 13%.

Similarly, the Worksite Division recorded its 13th consecutive quarter of NAP growth, with life NAP up 54% and hospital indemnity NAP up 22%. Geographic expansion contributed 25% of NAP growth for the division in Q2 2025.

The company’s broker-dealer and registered investment advisor business showed particularly strong momentum, with client assets up 27% year-over-year to $4.59 billion and registered agent counts up 6% to 759.

Forward-Looking Statements

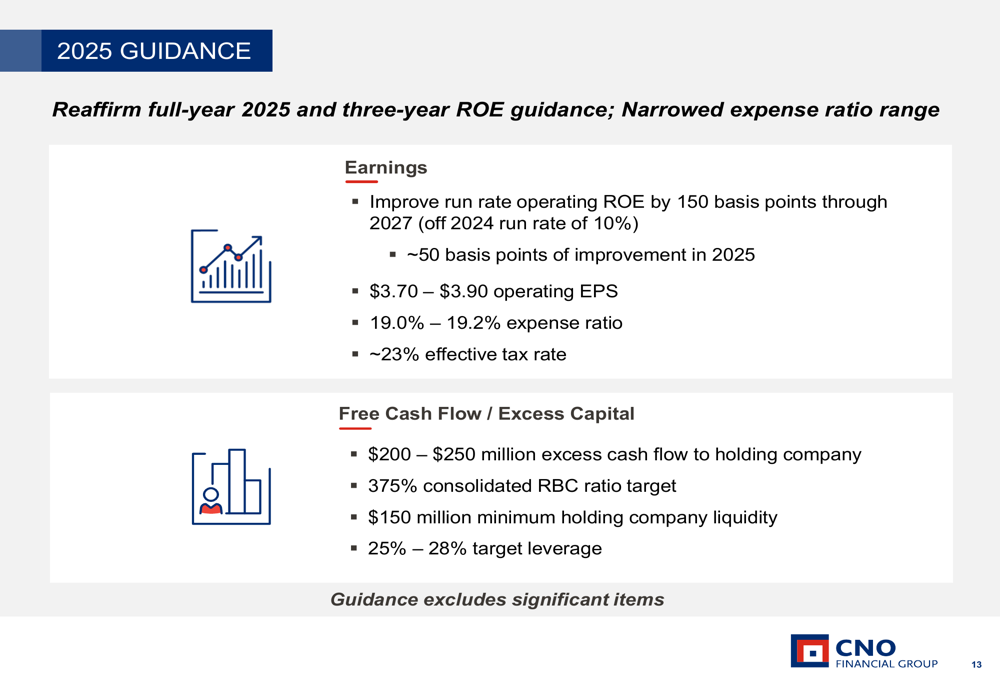

CNO reaffirmed its full-year 2025 guidance and three-year ROE targets while narrowing its expense ratio range. The company expects operating EPS of $3.70-$3.90 for 2025, with an expense ratio of 19.0%-19.2% and an effective tax rate of approximately 23%.

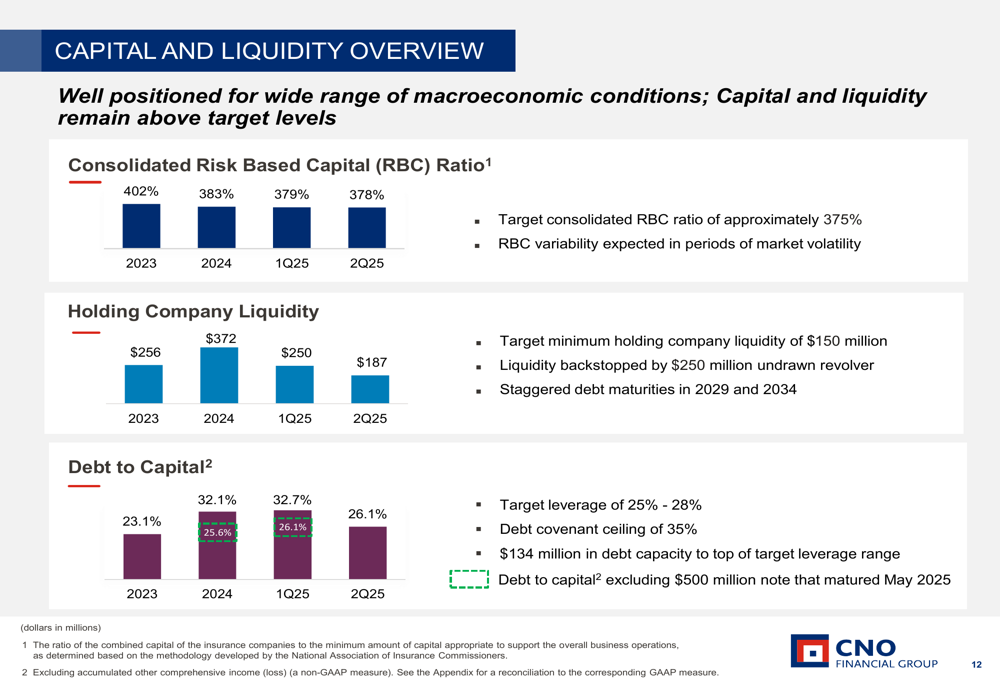

The capital and liquidity position remains strong, with the consolidated RBC ratio at 378% (versus a target of approximately 375%), holding company liquidity at $187 million (above the $150 million minimum target), and debt-to-capital ratio at 26.1% (within the 25%-28% target range):

Looking ahead, CNO aims to improve its run-rate operating ROE by 150 basis points through 2027 (from a 2024 run rate of 10%), with approximately 50 basis points of improvement expected in 2025:

The company plans to generate $200-$250 million in excess cash flow to the holding company in 2025, supporting continued capital returns to shareholders. In Q2 2025, CNO returned $117 million to shareholders, bringing the year-to-date total to $234 million.

Management highlighted several levers to drive operating ROE improvement, including accelerating brokerage and advisory growth, optimizing agent count and productivity, refining the capital structure, and maintaining expense discipline.

With its exclusive focus on the underserved middle-income market, significant demographic tailwinds, and integrated distribution model, CNO appears well-positioned to continue delivering growth while improving returns on equity, despite potential challenges from Medicare Supplement margin volatility and competitive pressures in the annuities market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.