Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Coface (EPA:COFA) reported its first quarter 2025 results on May 5, revealing a 9.2% decline in net income amid rising global economic policy uncertainty. The trade credit insurer’s shares closed at €18.24 on the day of the presentation, up 1.75%, suggesting investors were largely anticipating these results.

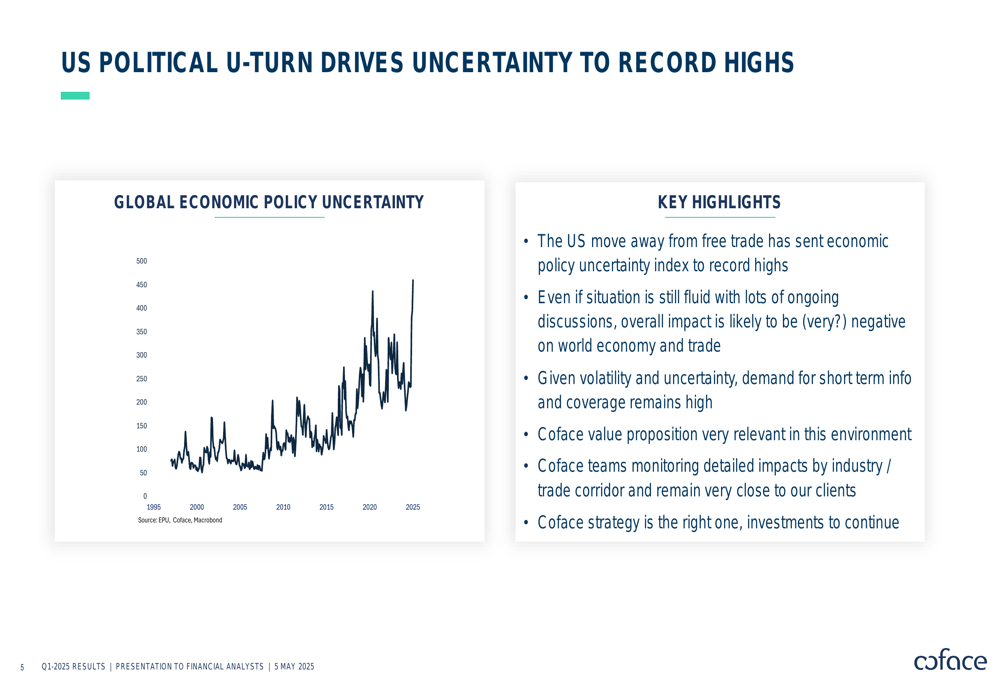

The company highlighted that the US move away from free trade has sent economic policy uncertainty to record highs, creating a challenging but opportunity-rich environment for Coface’s risk management services.

Quarterly Performance Highlights

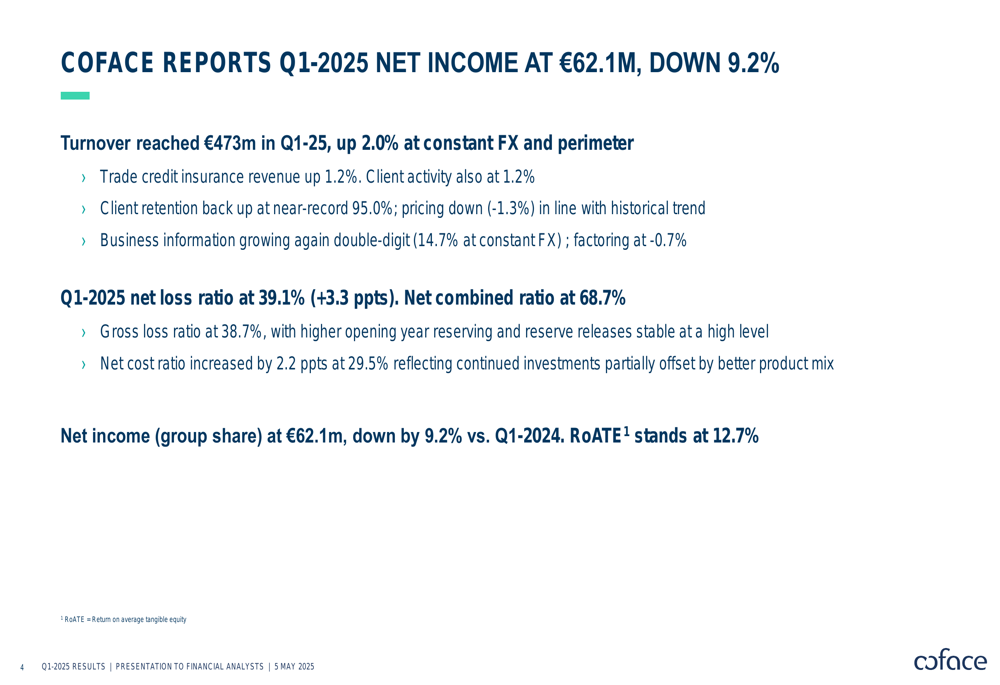

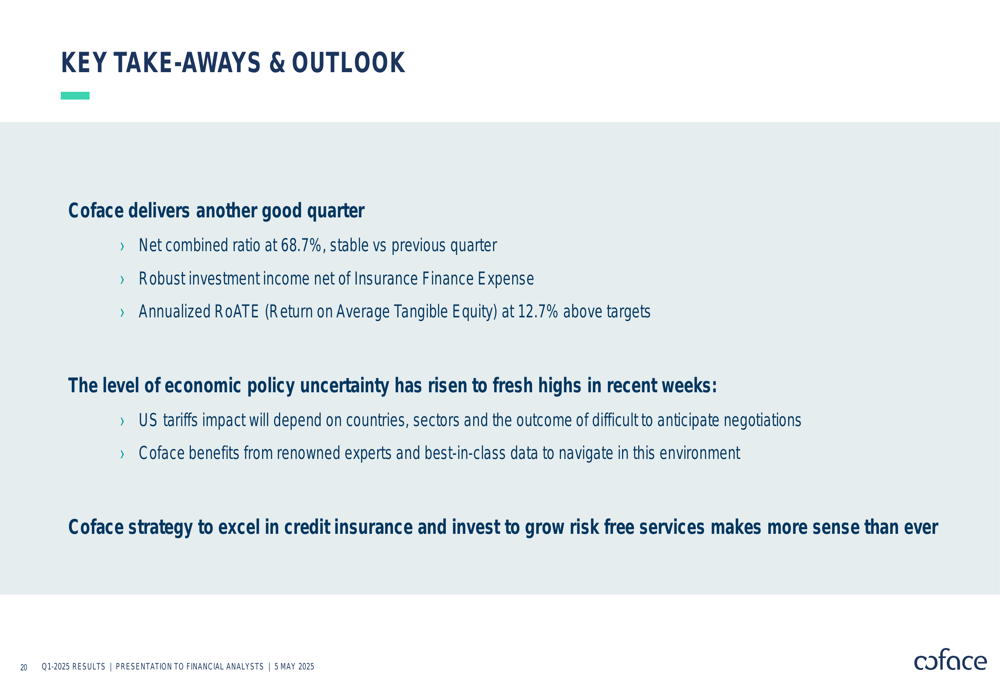

Coface reported Q1 2025 net income of €62.1 million, down 9.2% compared to the same period last year, with a Return on Average Tangible Equity (RoATE) of 12.7%. Total (EPA:TTEF) revenue reached €473 million, representing a 2.0% increase at constant FX and perimeter.

As shown in the following key financial results summary, the company maintained strong client retention while experiencing normalization in its loss ratio:

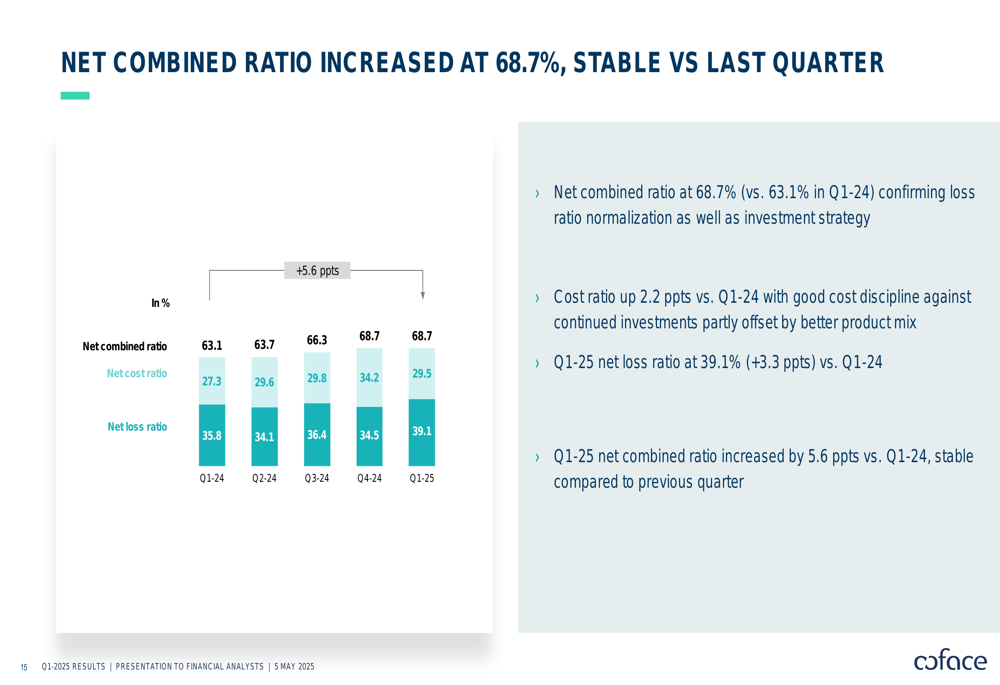

Trade credit insurance revenue grew by 1.2%, matching client activity growth. Client retention rebounded to a near-record 95.0%, while pricing declined by 1.3%, in line with historical trends. The company’s net loss ratio increased to 39.1% (up 3.3 percentage points year-over-year), resulting in a net combined ratio of 68.7%.

Coface emphasized that the current economic environment, characterized by high uncertainty, creates strong demand for its core services. The following chart illustrates the dramatic rise in global economic policy uncertainty:

Detailed Financial Analysis

Revenue Growth Drivers

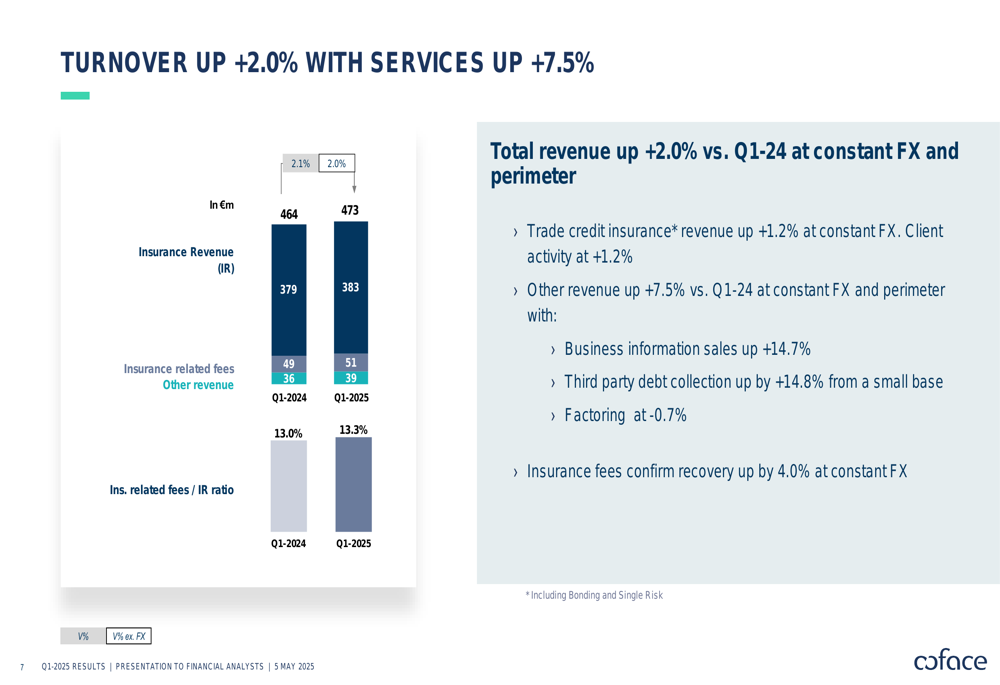

Coface’s turnover growth was primarily driven by services, which increased by 7.5% compared to Q1 2024. Business information sales showed particularly strong performance, growing by 14.7%, while third-party debt collection increased by 14.8%, albeit from a smaller base. Insurance-related fees also recovered, growing by 4.0% at constant FX.

The following chart breaks down the company’s revenue components:

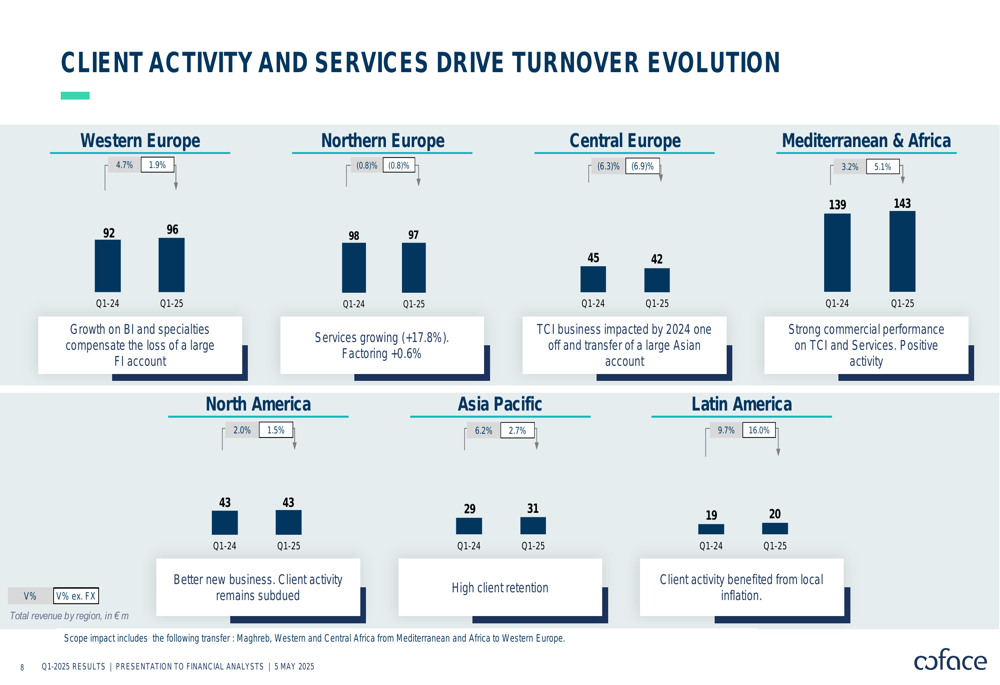

Regional performance varied significantly across Coface’s global operations. Latin America led growth with a 16.0% increase at constant FX, benefiting from local inflation. Asia Pacific and Mediterranean & Africa regions also showed solid growth, while Central Europe experienced a 6.9% decline, impacted by a 2024 one-off and the transfer of a large Asian account.

The regional breakdown illustrates these varying performance levels:

Risk and Loss Ratio Analysis

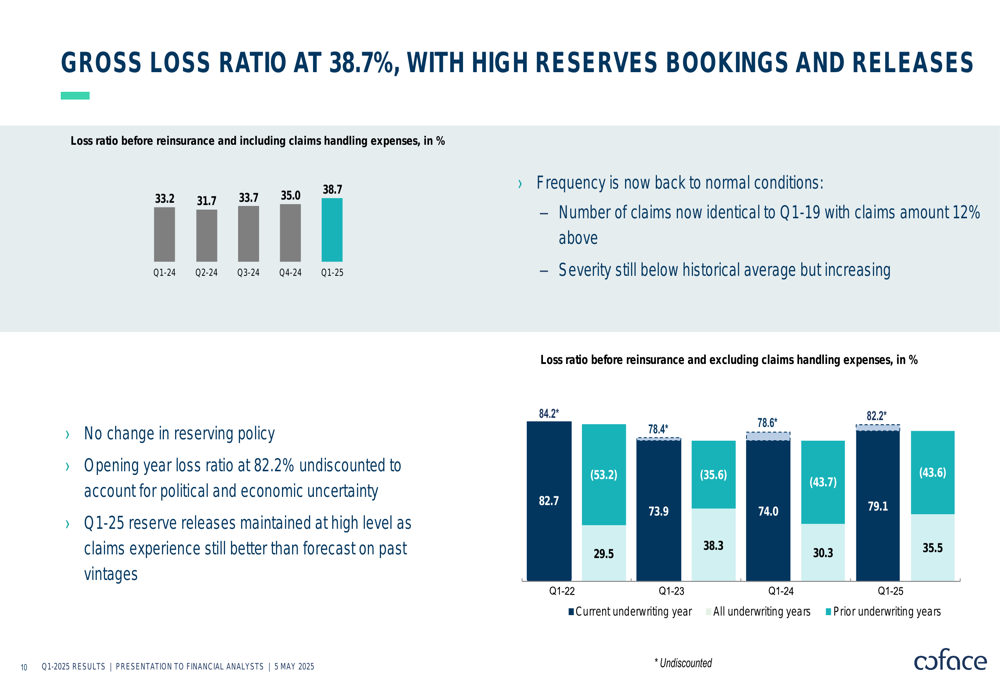

Coface’s gross loss ratio increased to 38.7% in Q1 2025 from 33.2% in Q1 2024, reflecting what the company described as a "normalization" of claims frequency. The company maintained its reserving policy, setting the opening year loss ratio at 82.2% undiscounted to account for political and economic uncertainty.

The following chart shows the evolution of the loss ratio components:

Loss ratios varied significantly by region, with Latin America experiencing a particularly high ratio of 107.0% in Q1 2025, while Western Europe maintained a healthier 25.3%. North America saw its loss ratio increase substantially to 49.6%, up from 33.3% in Q1 2024.

The combined ratio, a key measure of insurance profitability, increased to 68.7% in Q1 2025 from 63.1% in Q1 2024, driven by both higher loss ratios and increased costs. The cost ratio rose by 2.2 percentage points to 29.5%, reflecting continued investments and cost inflation, partially offset by improved product mix.

This trend is illustrated in the following combined ratio breakdown:

Investment Performance

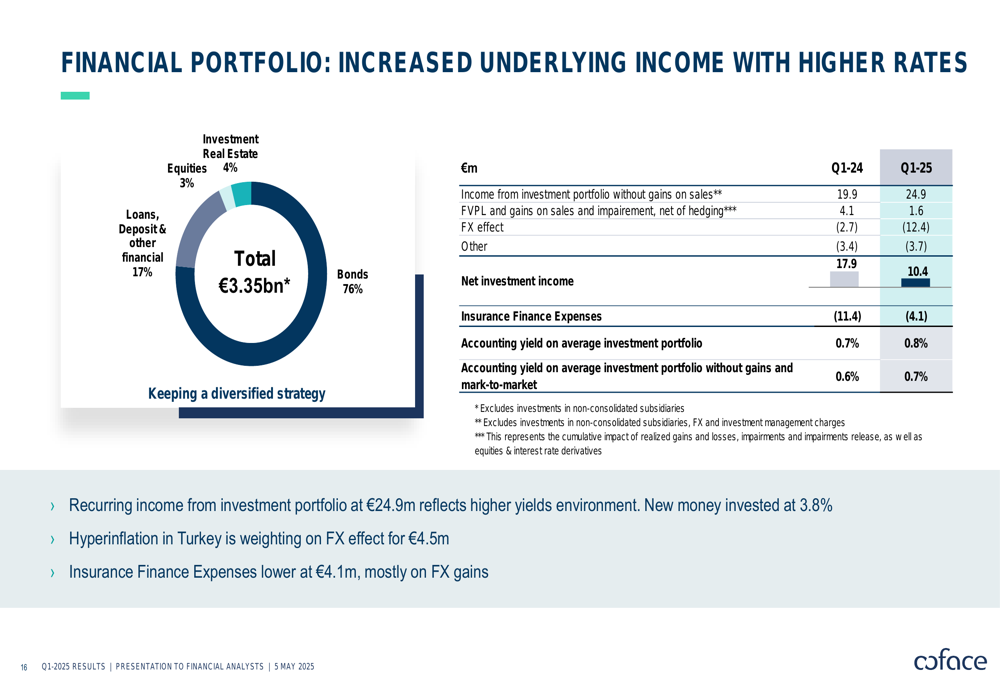

Coface’s investment portfolio generated recurring income of €24.9 million, benefiting from the higher yield environment with new money invested at 3.8%. However, hyperinflation in Turkey weighed on FX effects, resulting in a €4.5 million negative impact. The company’s total investment portfolio stood at €3.35 billion, with 76% allocated to bonds.

Strategic Initiatives

Coface continues to invest in growth while navigating the challenging economic environment. The company’s strategy focuses on excelling in its core credit insurance business while expanding risk-free services, particularly in business information and debt collection.

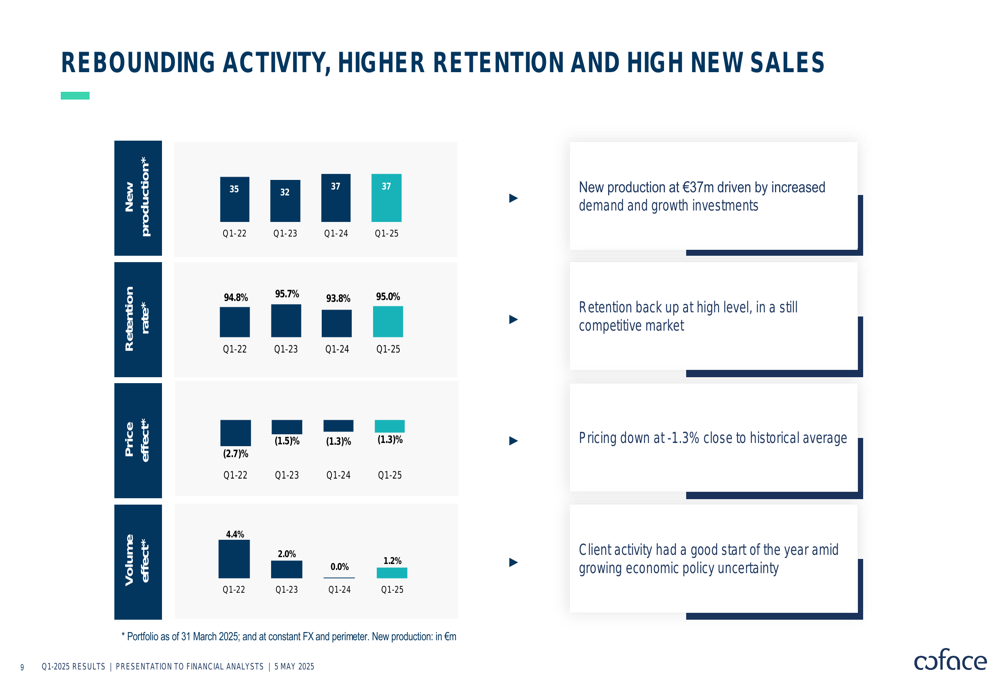

Client activity and retention metrics show positive momentum, with new production stable at €37 million and retention rebounding to 95.0%, indicating the company’s strong competitive position despite market challenges:

Forward-Looking Statements

Looking ahead, Coface management emphasized that the company is well-positioned to navigate the heightened economic uncertainty. The company benefits from "renowned experts and best-in-class data" to manage risks in this environment, according to the presentation.

Management reiterated that Coface’s strategy to excel in credit insurance while investing to grow risk-free services "makes more sense than ever" given current market conditions. The company’s RoATE of 12.7% remains above its targets despite recent pressures.

While acknowledging the normalization of loss ratios and increased economic uncertainty, Coface maintained a confident outlook, emphasizing its ability to adapt to changing market conditions and leverage its expertise in risk assessment. The impact of potential US tariffs remains a key area of focus, with outcomes depending on countries, sectors, and the results of ongoing negotiations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.