Cigna earnings beat by $0.04, revenue topped estimates

Semiconductor equipment provider shows signs of recovery with improved gross margins and strong recurring revenue growth

Introduction & Market Context

Cohu Inc. (NASDAQ:COHU) presented its first quarter 2025 financial results on May 1, 2025, showing sequential improvement in key metrics while projecting a return to profitability in the second quarter. The semiconductor equipment manufacturer closed the trading day at $16.00, up 0.44%, as investors digested the latest financial performance and outlook.

The company continues to navigate a challenging semiconductor equipment market, with test cell utilization down 1 percentage point quarter-over-quarter to 72%, indicating ongoing capacity adjustments across the industry. However, Cohu’s strategic focus on recurring revenue and expansion into new markets is beginning to show results.

Quarterly Performance Highlights

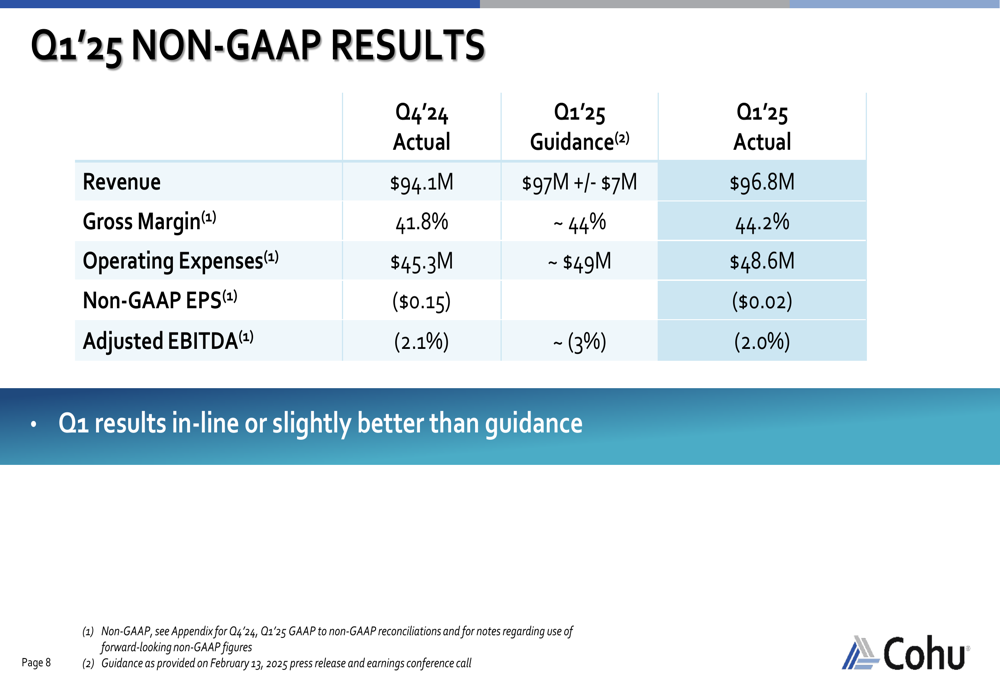

Cohu reported Q1 2025 revenue of $96.8 million, representing a 2.9% increase from $94.1 million in Q4 2024, though still below the $107.6 million recorded in Q1 2024. The company’s non-GAAP gross margin improved to 44.2%, up from 41.8% in the previous quarter but below the 46.0% achieved in the same period last year.

As shown in the following quarterly results comparison:

The company posted a non-GAAP loss per share of $0.02 in Q1 2025, a significant improvement from the $0.15 loss per share in Q4 2024. Adjusted EBITDA remained negative at -2.0%, showing a slight improvement from -2.1% in the previous quarter, but still below the positive 2.6% recorded in Q1 2024.

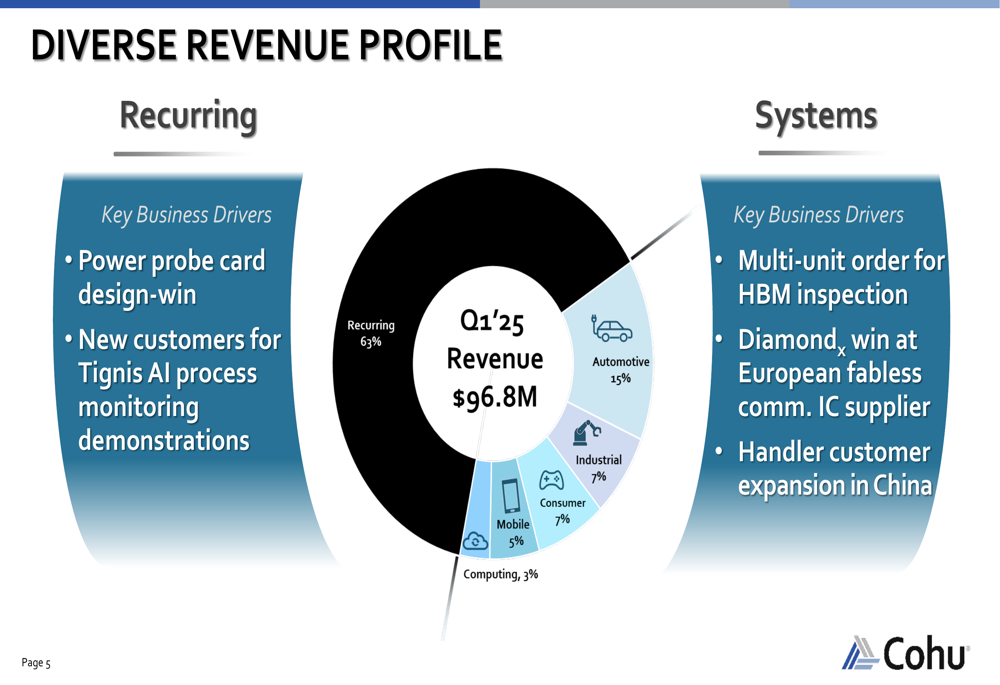

Cohu’s revenue profile has shifted toward a higher proportion of recurring revenue, which now accounts for 63% of total revenue, with systems revenue making up the remaining 37%. The systems revenue is diversified across multiple end markets, with automotive leading at 15% of total revenue.

The company’s diverse revenue profile and key business wins are illustrated in this breakdown:

Strategic Initiatives

Cohu highlighted several strategic wins during the quarter, including a multi-unit order for High Bandwidth (NASDAQ:BAND) Memory (HBM) inspection systems, a power probe card design win, and new customer acquisitions for its Tignis AI process monitoring solutions. The company also expanded its handler customer base in China and secured a Diamond win at a European fabless communications IC supplier.

The company is implementing cost reduction measures to lower operating expenses and return to profitability, including restructuring its underutilized Asian factories. These initiatives are part of Cohu’s strategy to "open the business aperture" through design wins and expansion into new markets.

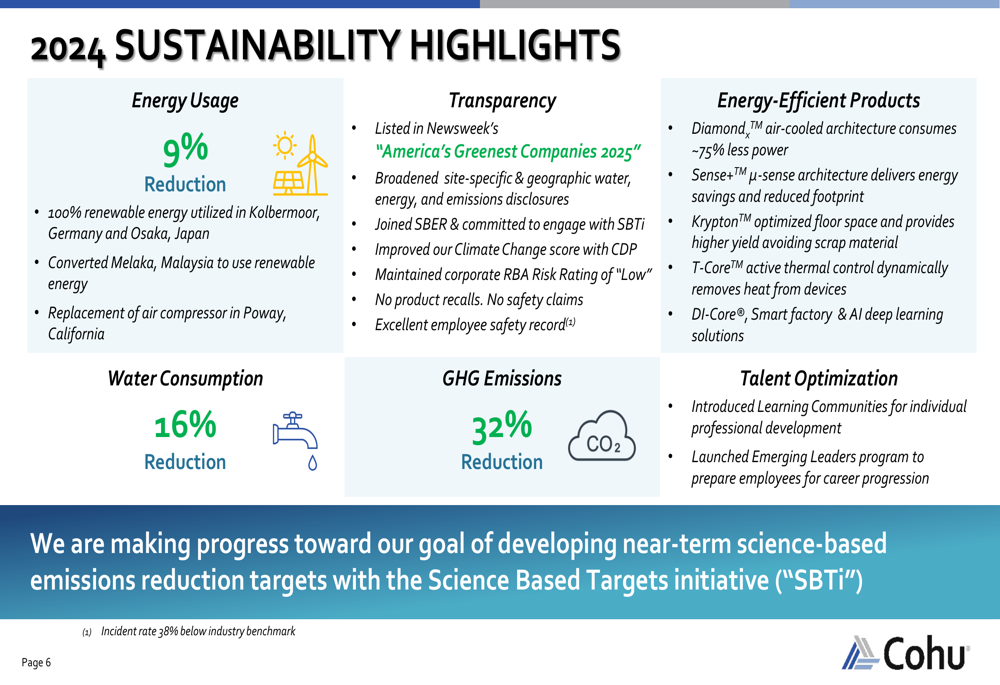

Cohu also emphasized its sustainability achievements in 2024, including a 9% reduction in energy usage, a 32% reduction in greenhouse gas emissions, and a 16% reduction in water consumption. The company was listed in Newsweek’s "America’s Greenest Companies 2025."

The following image highlights Cohu’s sustainability achievements:

Forward-Looking Statements

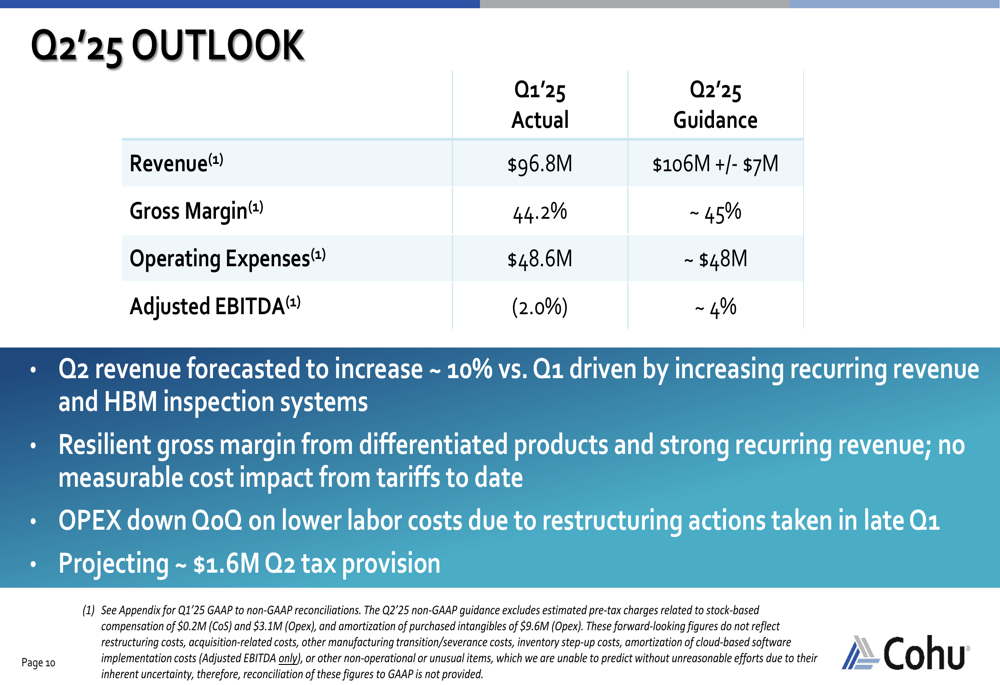

Cohu provided an optimistic outlook for Q2 2025, projecting revenue of $106 million (±$7 million), which would represent approximately 10% growth compared to Q1. The company expects gross margin to improve to approximately 45%, with operating expenses decreasing to around $48 million due to restructuring actions taken in late Q1.

Most notably, Cohu forecasts a return to positive adjusted EBITDA of approximately 4% in Q2 2025, a significant improvement from the -2.0% reported in Q1. This outlook is driven by increasing recurring revenue and HBM inspection systems.

The Q2 2025 guidance compared to Q1 2025 actual results is illustrated in this forecast:

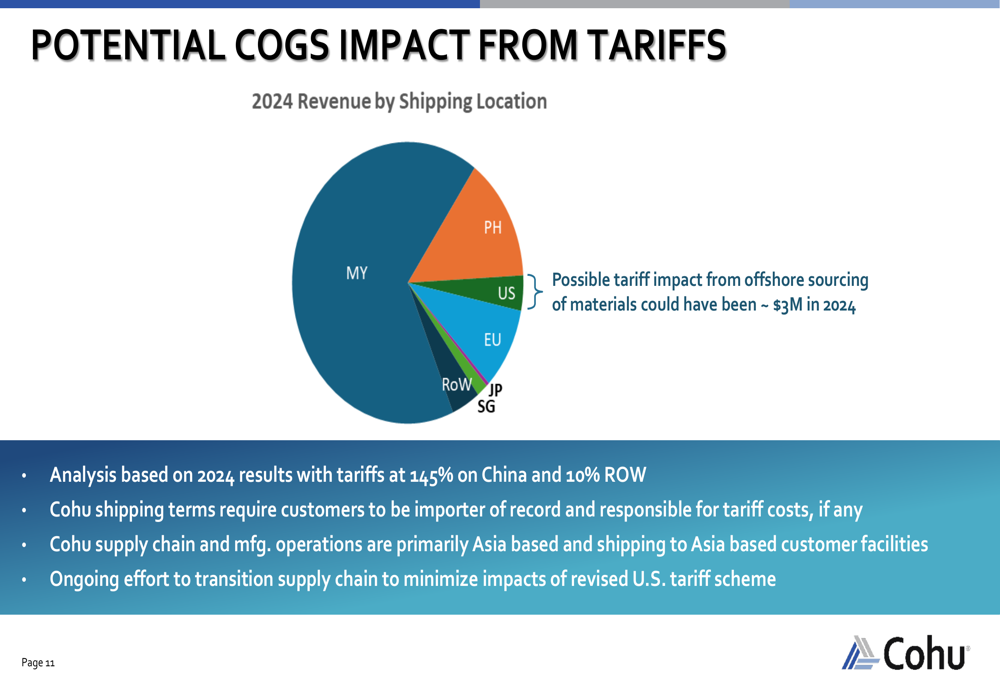

Cohu also addressed potential tariff impacts on its business, noting that its analysis based on 2024 results shows limited exposure. The company’s shipping terms require customers to be the importer of record responsible for tariff costs, and Cohu is working to transition its supply chain to minimize impacts from revised U.S. tariff schemes.

The following chart shows Cohu’s revenue by shipping location and potential tariff impact:

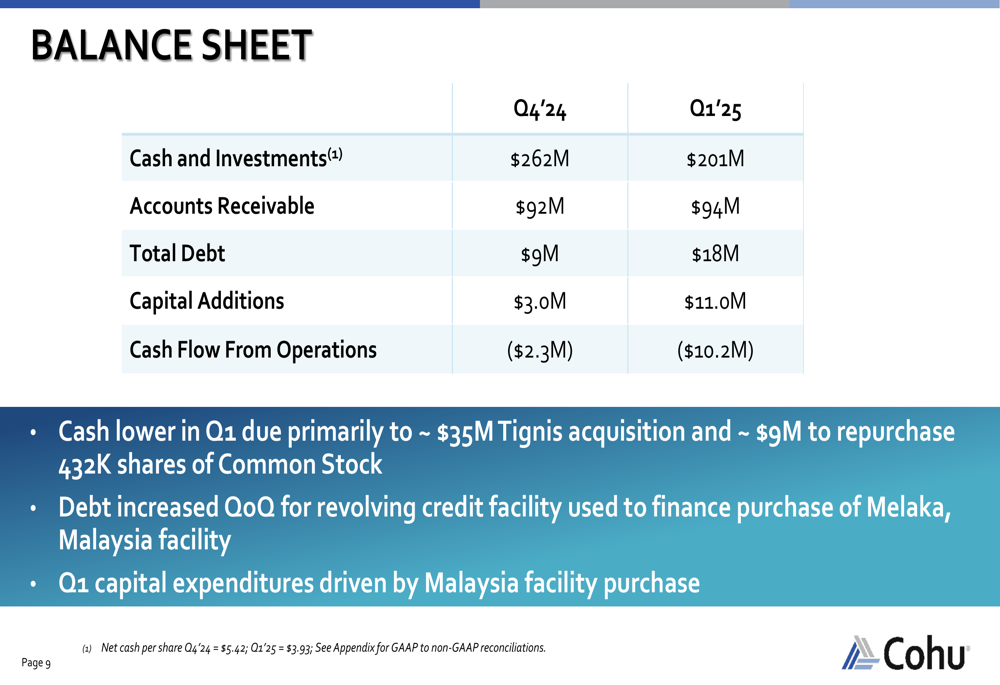

Financial Position

Cohu’s balance sheet showed some significant changes in Q1 2025. Cash and investments decreased to $201 million from $262 million in Q4 2024, primarily due to the approximately $35 million acquisition of Tignis and approximately $9 million used to repurchase 432,000 shares of common stock.

Total (EPA:TTEF) debt increased to $18 million from $9 million in the previous quarter, as the company utilized its revolving credit facility to finance the purchase of its Melaka, Malaysia facility. Net cash per share decreased to $3.93 from $5.42 in Q4 2024.

The balance sheet comparison between Q4 2024 and Q1 2025 is detailed in this financial summary:

Cash flow from operations was negative at $10.2 million in Q1 2025, compared to negative $2.3 million in Q4 2024. Capital additions increased significantly to $11.0 million from $3.0 million, driven primarily by the Malaysia facility purchase.

Despite these cash outflows, Cohu maintains a strong financial position with $201 million in cash and investments, providing flexibility to navigate the current market environment while continuing to invest in strategic initiatives.

As the semiconductor industry continues to evolve, Cohu’s focus on recurring revenue growth, expansion into new markets, and operational efficiency positions the company to capitalize on the eventual market recovery, particularly in the automotive and industrial segments that form a significant portion of its customer base.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.