Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Colabor Group Inc . (TSX:GCL) shares tumbled 13.86% following the release of its first quarter 2025 results on May 1, closing at $0.87 on May 2. The food distribution company reported a significant decline in profitability despite marginal revenue growth, while simultaneously announcing a major strategic acquisition aimed at expanding its presence in Western Quebec.

The company’s presentation, delivered by President & CEO Louis Frenette and SVP & CFO Pierre Blanchette, highlighted both the challenging quarter and the strategic rationale behind its expansion plans in a competitive food distribution market.

Quarterly Performance Highlights

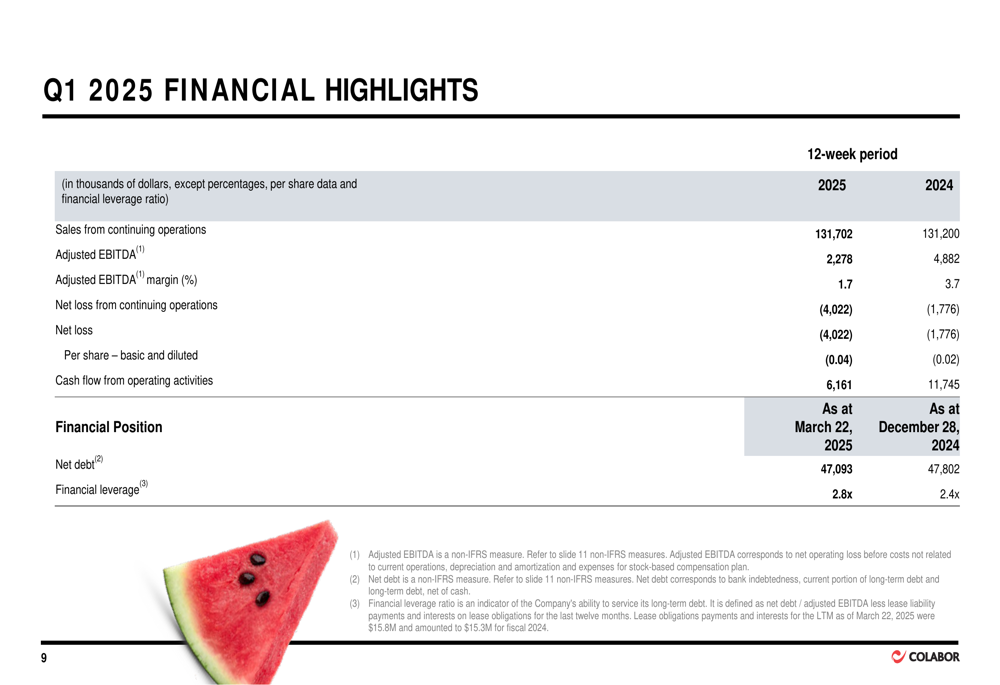

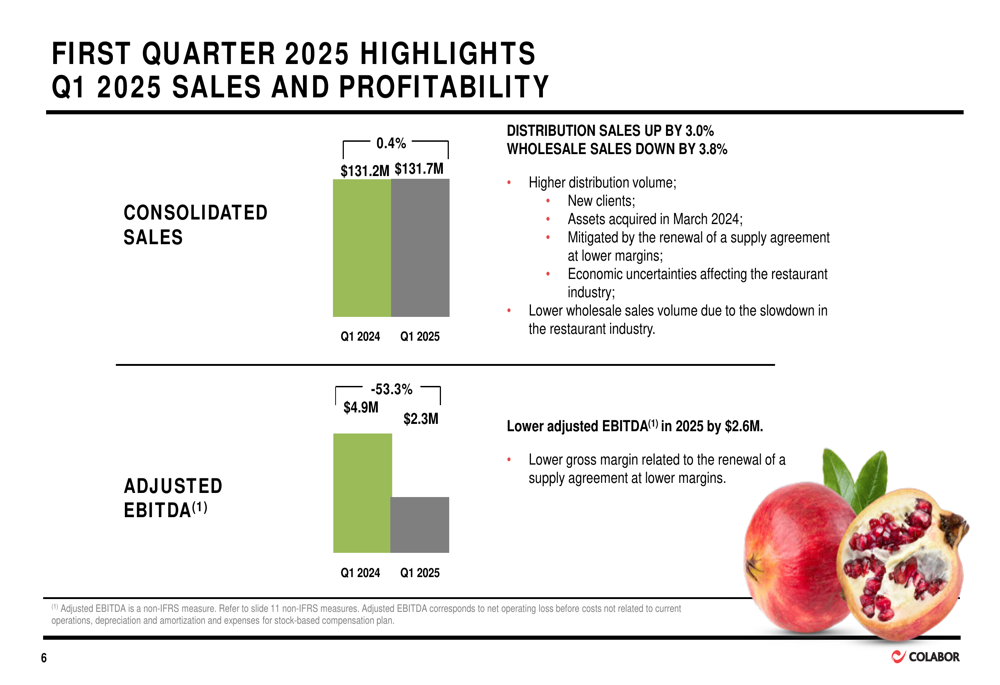

Colabor reported minimal revenue growth for Q1 2025, with sales increasing just 0.4% to $131.7 million compared to $131.2 million in the same period last year. However, profitability metrics deteriorated significantly during the quarter.

As shown in the following comprehensive financial summary:

Adjusted EBITDA plunged 53.3% to $2.3 million from $4.9 million in Q1 2024, while the adjusted EBITDA margin contracted sharply from 3.7% to 1.7%. The company attributed this decline primarily to lower gross margins related to the renewal of a supply agreement at reduced rates.

The distribution segment showed modest growth with sales up 3.0%, while wholesale sales declined by 3.8%. The following chart illustrates the company’s sales and profitability trends:

Net loss for the quarter more than doubled to $4.0 million ($0.04 per share) compared to $1.8 million ($0.02 per share) in Q1 2024. This deterioration was driven by the decrease in adjusted EBITDA and an increase in costs not related to current operations, partially offset by an increase in income tax recovery.

Strategic Acquisition Details

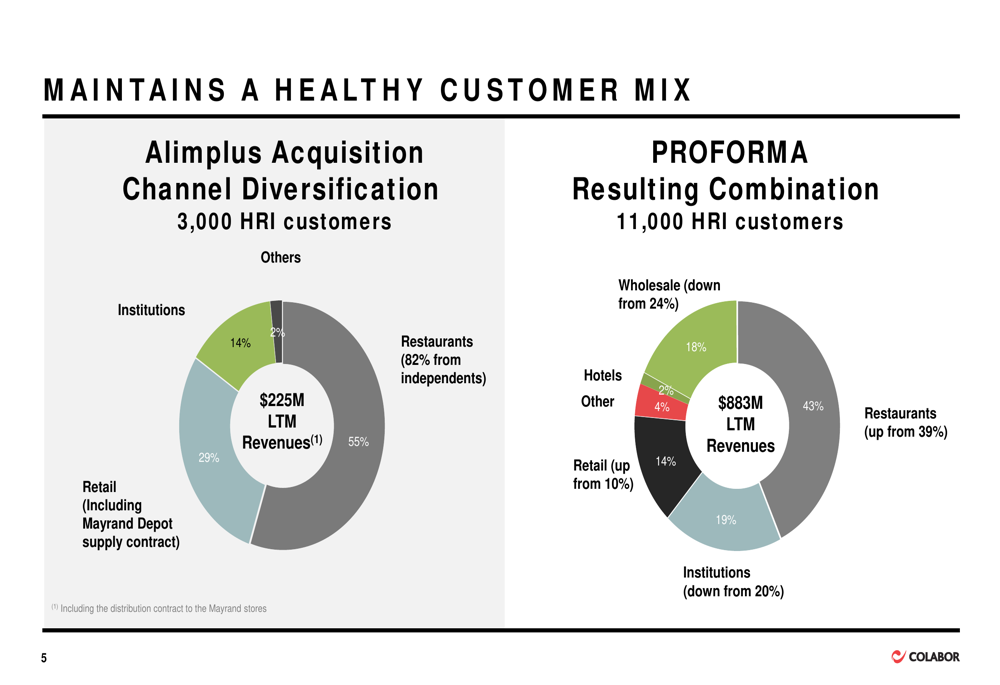

The centerpiece of Colabor’s presentation was the announcement of a significant acquisition that management believes will accelerate the company’s growth trajectory and improve profitability. Colabor has signed an agreement to acquire the food distribution assets of Alimplus Inc. (operating as Mayrand Plus) and all shares of its subsidiary Tout-Prêt Inc., which specializes in ready-to-use cut fruits and vegetables.

The following chart illustrates how the acquisition will transform Colabor’s customer mix:

The $51.5 million acquisition (subject to adjustments) includes a 6-year agreement to supply four Mayrand Food Depot stores and represents approximately $225 million in annual sales. Post-acquisition, Colabor’s customer base will expand to 11,000 HRI (Hotel, Restaurant, and Institutional) customers, with a greater concentration in the restaurant segment (increasing from 39% to 43% of revenue) and retail (increasing from 10% to 14%).

Management emphasized that the acquisition will be accretive to shareholders while maintaining a manageable leverage ratio. The transaction is expected to close during the second quarter of 2025.

Detailed Financial Analysis

Colabor’s cash flow generation weakened in Q1 2025, with cash flows from operating activities declining to $6.2 million from $11.7 million in the prior-year period. The company attributed this decrease to higher working capital requirements, particularly increased inventory investments, and the lower adjusted EBITDA.

The company’s balance sheet metrics showed mixed results. Net debt decreased slightly to $47.1 million from $47.8 million at the end of Q4 2024, primarily due to repayments of the credit facility of $5.8 million, partially offset by a decrease in cash of $5.0 million. However, the financial leverage ratio increased to 2.8x from 2.4x at the end of 2024, reflecting the lower trailing twelve-month adjusted EBITDA.

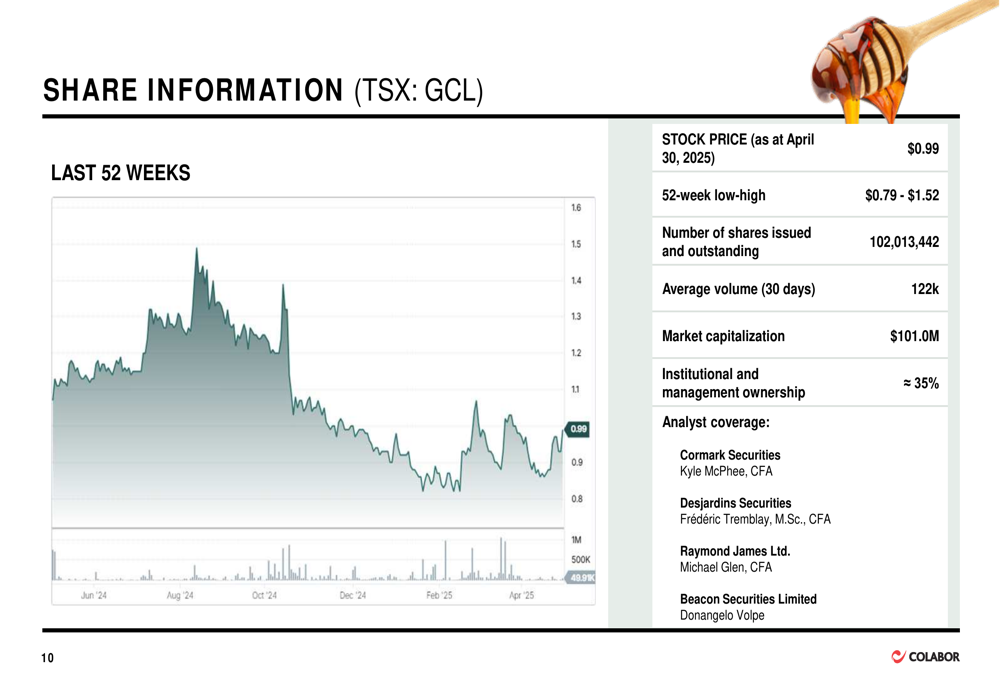

The following chart shows the company’s share price performance over the past year:

As of April 30, 2025, Colabor’s stock was trading at $0.99, with a 52-week range of $0.79 to $1.52. The company has 102,013,442 shares outstanding, with approximately 35% owned by institutional investors and management.

Forward-Looking Statements

To finance the Alimplus acquisition, Colabor has secured support from existing financial partners, including a $5 million increase on its existing credit facility with extended maturity, an extension of maturity on $15 million subordinated debt with Investissement Québec (IQ), and a new highly subordinated debt of $15 million with IQ.

The strategic rationale for the acquisition focuses on accelerating Colabor’s growth trajectory and profitability objectives. Management expects the transaction to improve the company’s reach in coveted markets, expand its offering, provide a value-added customer mix, and create synergies and cross-selling opportunities.

While the acquisition represents a significant strategic move, investors appear concerned about the company’s deteriorating profitability metrics and increasing leverage, as evidenced by the sharp stock price decline following the earnings release. The success of this acquisition and Colabor’s ability to reverse the negative profitability trends will likely be critical factors for investors to monitor in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.