Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Columbus McKinnon Corporation (NASDAQ:CMCO) reported a net loss for its first quarter of fiscal year 2026 ended June 30, 2025, despite growing orders and a record backlog. The company’s presentation, delivered on July 30, 2025, revealed significant impacts from tariffs and acquisition-related expenses while maintaining its full-year guidance.

Introduction & Market Context

Columbus McKinnon, a global provider of intelligent motion solutions for material handling, reported mixed results for Q1 FY26. The stock has experienced significant volatility, trading at $16.86 as of July 29, 2025, up 5.57% for the day but substantially below its 52-week high of $41.05. The company’s shares have faced pressure throughout 2025, with the current price reflecting ongoing market concerns despite some positive operational metrics.

The Q1 results come after a challenging Q4 FY25, where the company slightly exceeded earnings expectations but missed revenue forecasts, resulting in a stock decline. The first quarter of fiscal 2026 continues to show pressure on profitability, primarily due to tariff impacts and costs related to the pending Kito Crosby acquisition.

Quarterly Performance Highlights

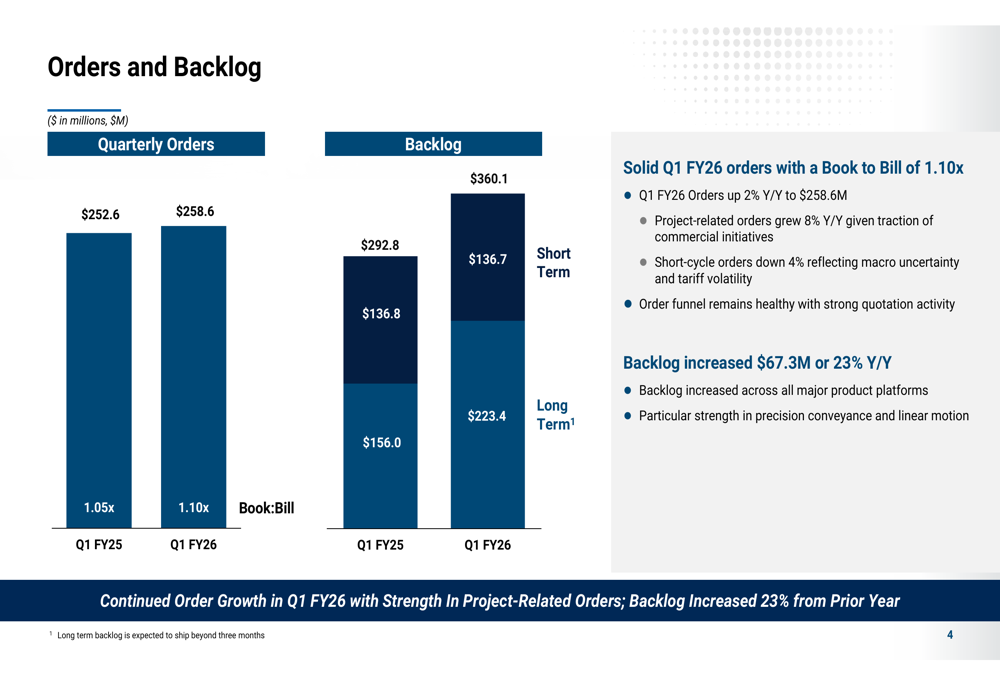

Columbus McKinnon reported strong order momentum in Q1 FY26, with orders reaching $259 million, up 2% year-over-year. This growth was driven primarily by an 8% increase in project-related business. The company achieved a book-to-bill ratio of 1.1x and built a record backlog of $360 million, representing a 23% increase from the prior year.

As shown in the following chart of orders and backlog performance:

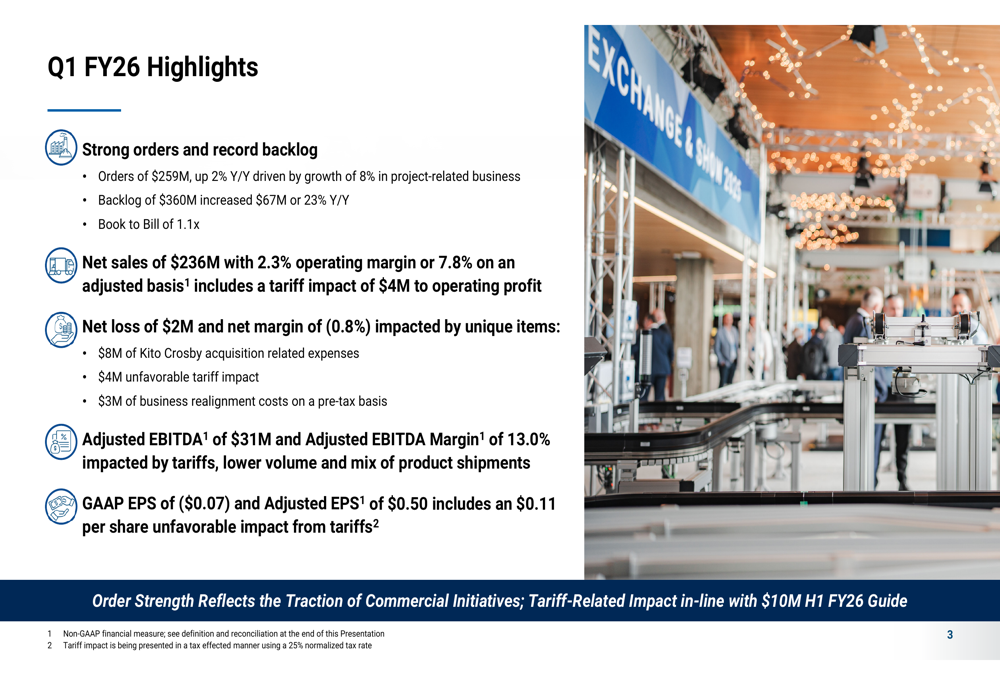

Despite the positive order trends, net sales decreased slightly to $236 million from $240 million in the prior year. The company reported a net loss of $2 million and a net margin of (0.8)%, significantly impacted by $8 million in Kito Crosby acquisition-related expenses, $4 million in unfavorable tariff impacts, and $3 million in business realignment costs.

The following slide summarizes the key financial highlights for the quarter:

Adjusted earnings per share came in at $0.50, which included an $0.11 per share unfavorable impact from tariffs. This compares to adjusted EPS of $0.62 in the same quarter last year. The company’s adjusted EBITDA was $31 million with a margin of 13.0%, down from $37 million and 15.6% in Q1 FY25.

Detailed Financial Analysis

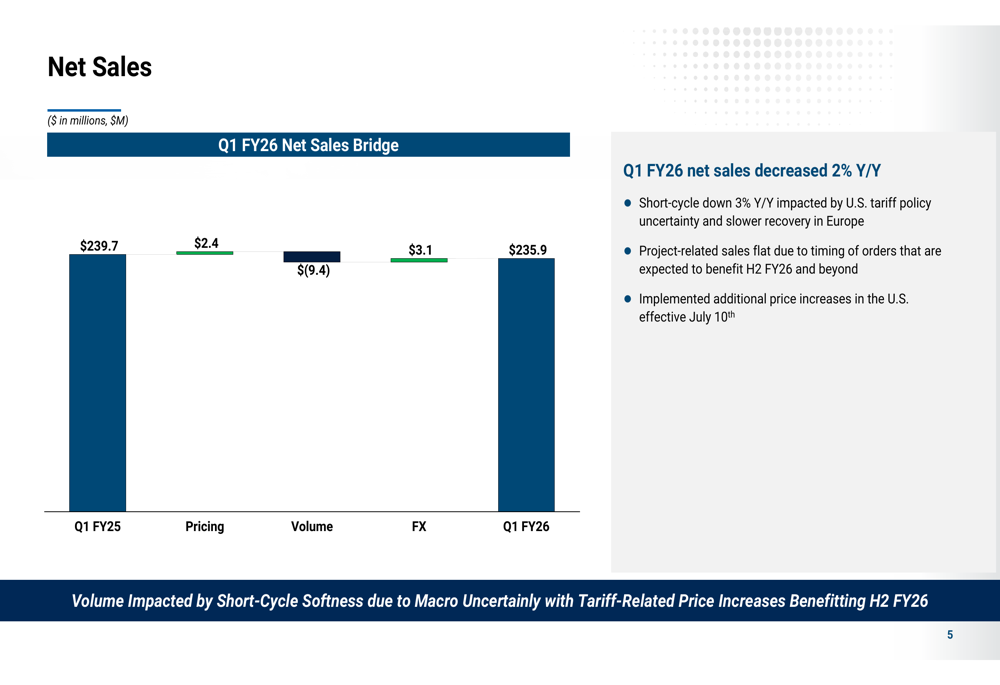

Net sales of $236 million represented a slight decrease from the prior year, with pricing contributing positively (+$2.4 million) and foreign exchange adding $3.1 million, offset by volume declines of $9.4 million. The company noted that short-cycle sales were down 3% year-over-year due to U.S. tariff policy uncertainty and slower recovery in Europe, while project-related sales remained flat due to timing of orders.

The following waterfall chart breaks down the components of the sales change:

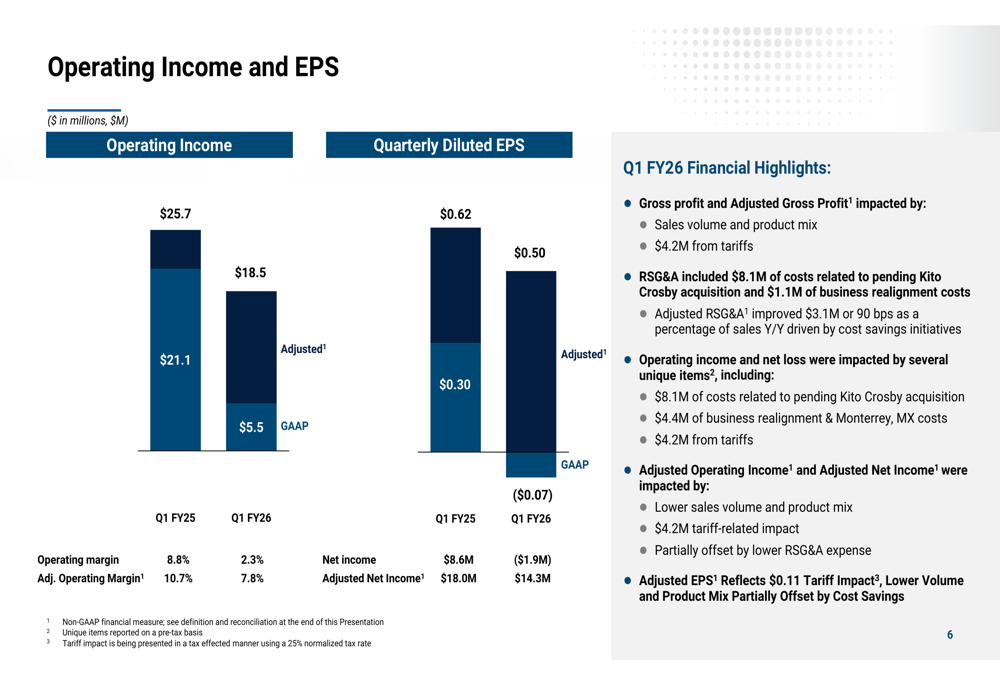

Operating income declined significantly from $21.1 million in Q1 FY25 to $5.5 million in Q1 FY26. On an adjusted basis, operating income was $18.5 million compared to $25.7 million in the prior year, with adjusted operating margin contracting from 10.7% to 7.8%. The decline was primarily attributed to lower sales volume, unfavorable product mix, and the $4.2 million tariff impact.

The company’s operating income and EPS performance is illustrated in this chart:

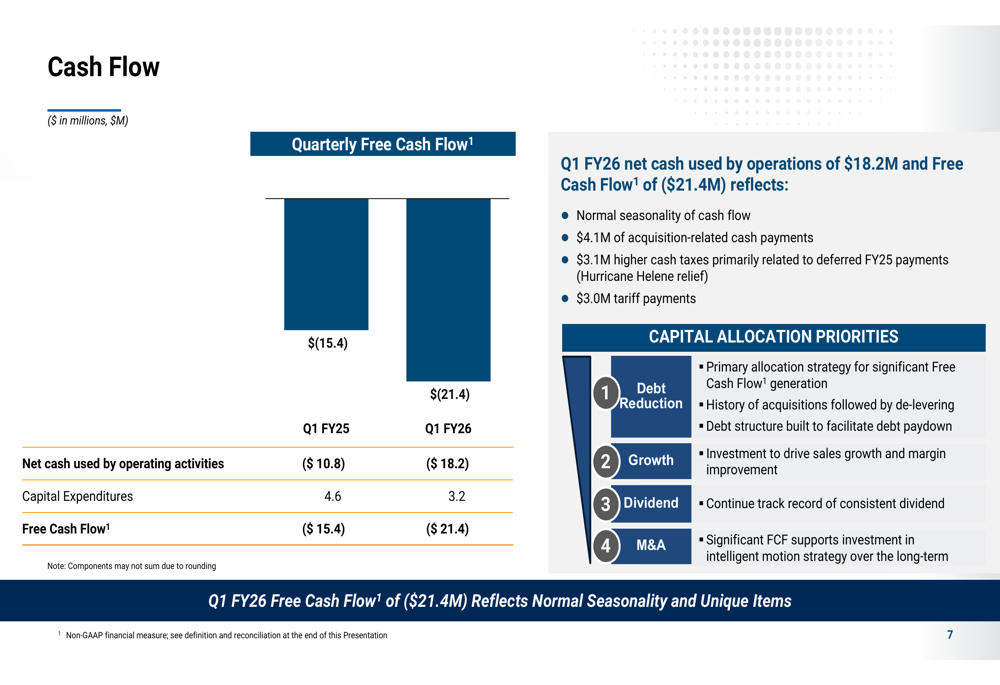

Free cash flow was negative at ($21.4 million) compared to ($15.4 million) in the same period last year. The decline was attributed to normal seasonality, $4.1 million in acquisition-related cash payments, $3.1 million in higher cash taxes, and $3.0 million in tariff payments.

The following slide details the cash flow performance and capital allocation priorities:

Strategic Initiatives

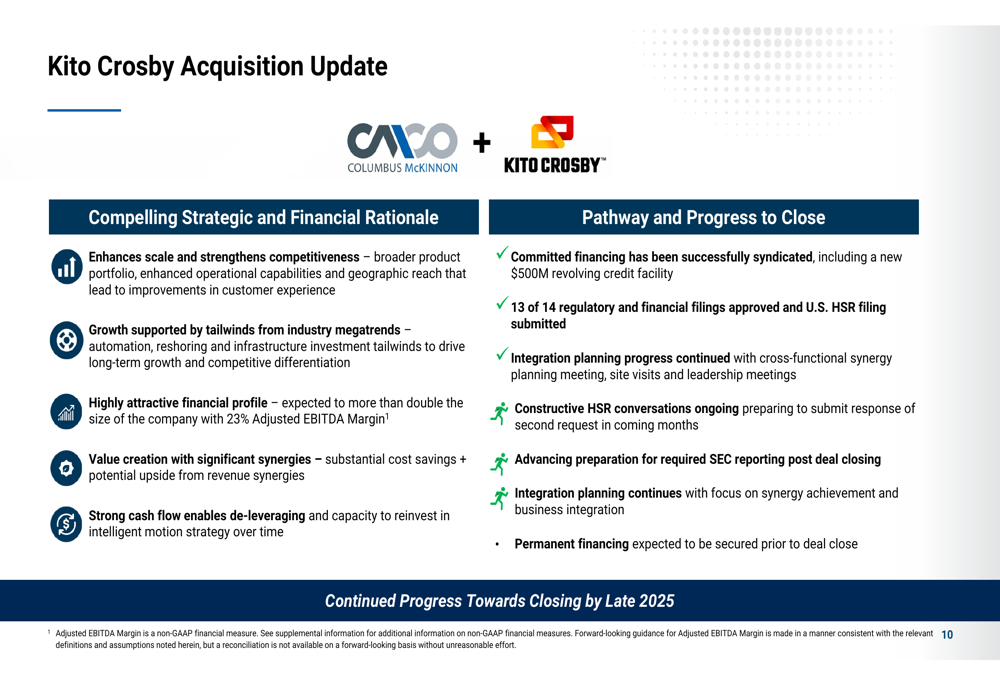

Columbus McKinnon continues to advance its pending acquisition of Kito Crosby, which is expected to close by late 2025. The company highlighted the strategic rationale for the acquisition, including enhanced scale and competitiveness, growth supported by industry megatrends, an attractive financial profile, and value creation through significant synergies.

The following slide provides an update on the acquisition progress:

To address tariff challenges, the company implemented additional price increases in the U.S. effective July 10, 2025. Management indicated that these increases are expected to benefit the second half of fiscal 2026, helping to offset the tariff-related headwinds experienced in the first half.

The company also continues to focus on cost savings initiatives, which have already shown positive results with adjusted RSG&A improving by $3.1 million or 90 basis points as a percentage of sales year-over-year.

Forward-Looking Statements

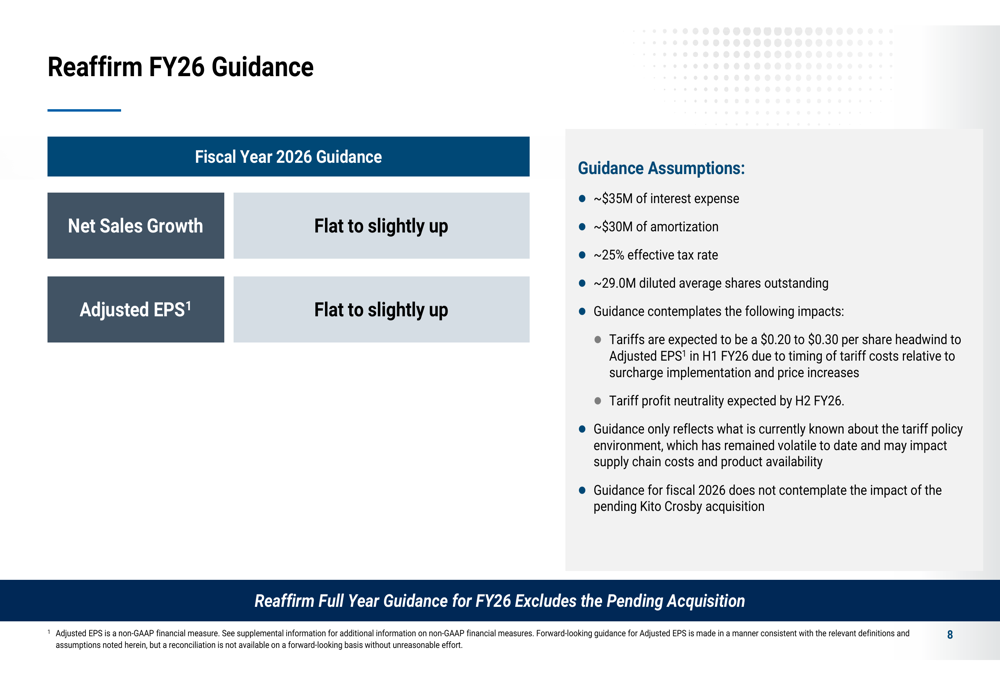

Despite the challenges in Q1, Columbus McKinnon reaffirmed its full-year guidance for fiscal 2026, expecting net sales and adjusted EPS to be flat to slightly up. This guidance excludes the impact of the pending Kito Crosby acquisition and reflects what is known about the current tariff policy environment.

The company’s guidance and assumptions are detailed in the following slide:

Key assumptions in the guidance include approximately $35 million of interest expense, $30 million of amortization, a 25% effective tax rate, and 29.0 million diluted average shares outstanding.

Management remains optimistic about the company’s long-term prospects, pointing to the strong order growth and record backlog as indicators of future potential. The company’s focus on strategic acquisitions, operational improvements, and pricing actions to offset tariff impacts demonstrates a proactive approach to navigating current market challenges while positioning for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.