Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Community Healthcare Trust (NYSE:CHCT) released its July 2025 investor presentation, highlighting its diversified healthcare real estate portfolio and expansion strategy amid challenging market conditions. The healthcare REIT, which focuses on acquiring smaller, off-market healthcare properties, currently trades at $16.25, near its 52-week low of $14.76, despite maintaining its decade-long dividend growth streak.

The company’s stock fell 1.17% in premarket trading on July 30, 2025, following a mixed Q1 earnings report where EPS missed expectations at $0.03 versus the forecasted $0.08, though revenue exceeded predictions at $30.08 million.

Portfolio Overview

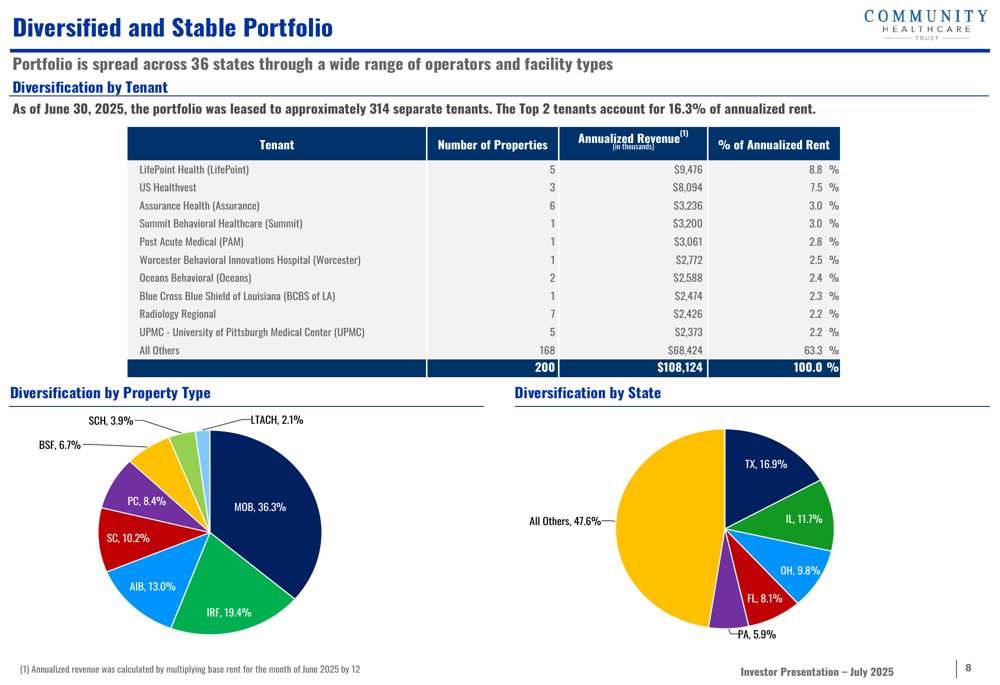

CHCT’s portfolio consists of 200 properties with 314 tenants across 36 states, creating a geographically diversified footprint. The company has strategically focused on smaller, off-market healthcare facilities to avoid competitive bidding situations.

As shown in the following portfolio diversification breakdown, CHCT maintains significant tenant diversification with its top two tenants accounting for 16.3% of annualized rent. The company’s properties span multiple healthcare segments, with medical office buildings (36.3%) and inpatient rehabilitation facilities (19.4%) representing the largest portions of the portfolio.

Geographic diversification remains a key strength, with properties spread across 36 states. The largest concentrations are in Texas (16.9%), Illinois (11.7%), Ohio (9.8%), Florida (8.1%), and Pennsylvania (5.9%), with all other states comprising 47.6% of the portfolio.

Financial Performance

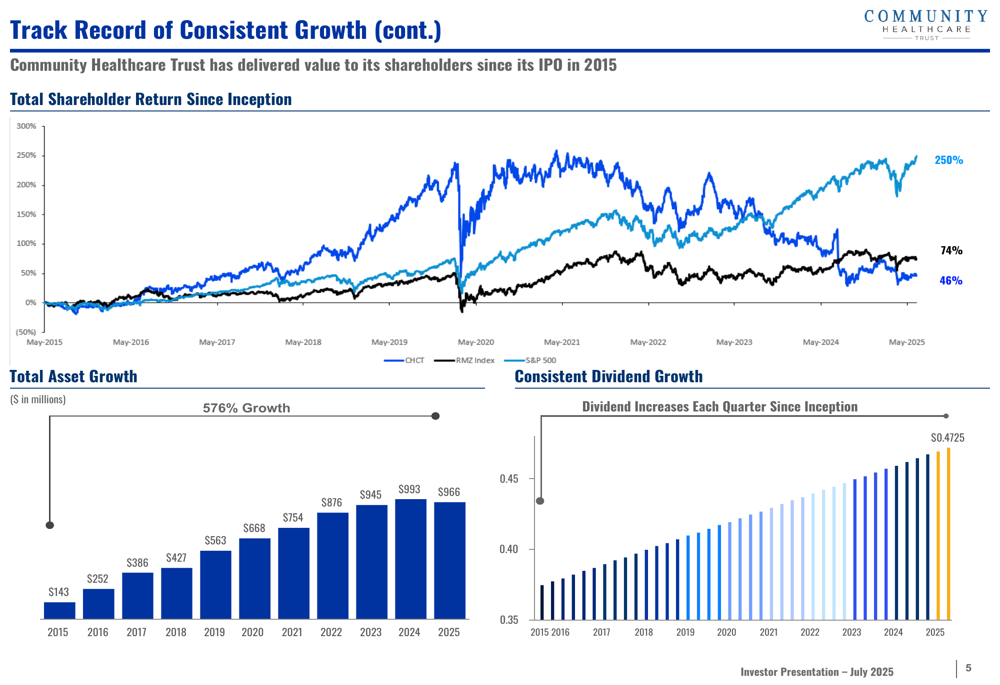

The presentation highlights CHCT’s significant growth since its 2015 IPO, with total assets increasing from $143 million in 2015 to $966 million in 2025, representing 576% growth. The company has delivered a total shareholder return of 250% since inception, substantially outperforming both the RMZ Index (74%) and S&P 500 (46%).

The following chart illustrates this impressive long-term performance trajectory:

A cornerstone of CHCT’s investor appeal has been its consistent dividend growth, with 40 consecutive quarterly increases bringing the current dividend to $0.4725 per share. This translates to an annualized dividend of $1.89 and a yield of approximately 11.56% at current share prices.

Despite these positive long-term trends, CHCT’s recent financial performance has shown some challenges. The company’s Q1 2025 EPS of $0.03 fell significantly short of the $0.08 forecast, though revenue of $30.08 million exceeded expectations by $0.5 million.

Strategic Positioning

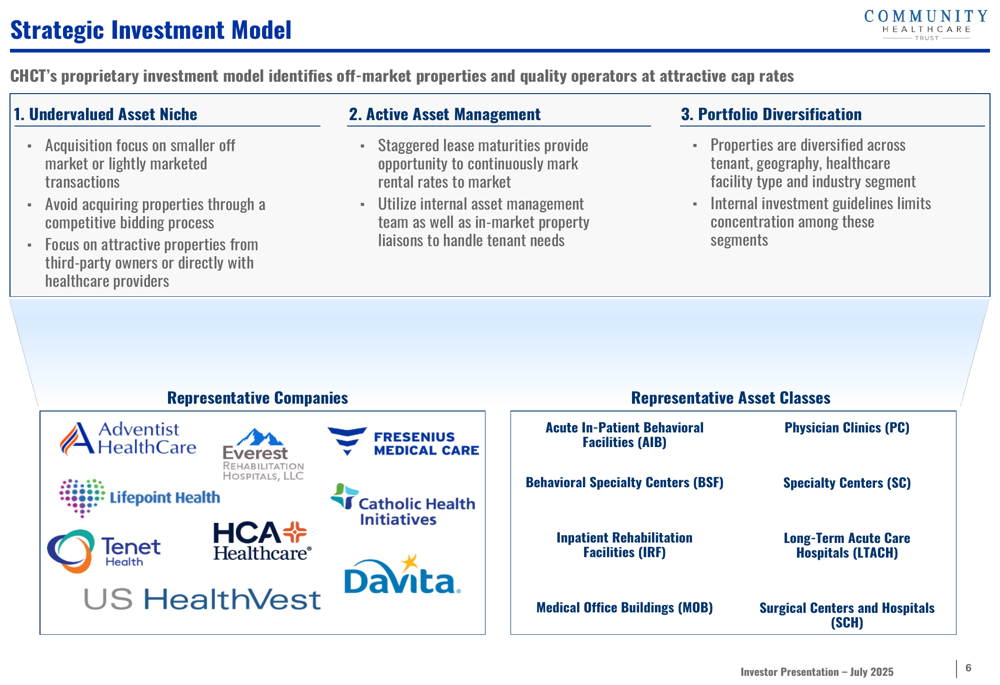

CHCT’s investment strategy focuses on three key pillars: targeting undervalued asset niches, active asset management, and portfolio diversification. The company specializes in acquiring smaller, off-market properties directly or through healthcare providers, avoiding competitive bidding situations.

The strategic model is illustrated below:

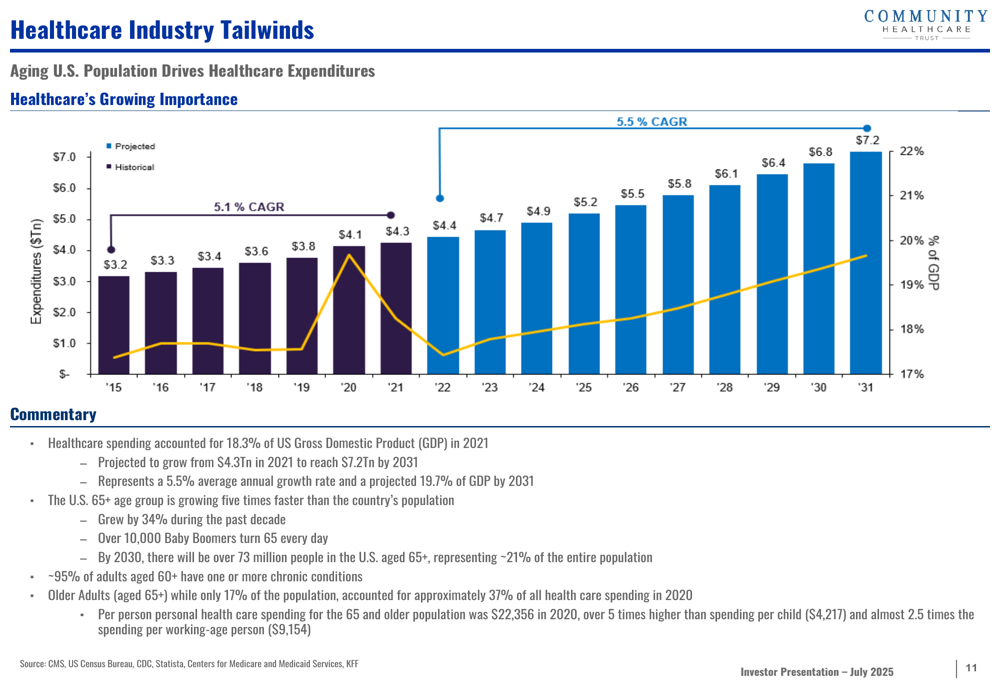

The company is positioning itself to benefit from significant healthcare industry tailwinds, including an aging U.S. population driving increased healthcare expenditures. These expenditures are projected to grow from $4.3 trillion in 2021 to $7.2 trillion by 2031, representing a 5.5% average annual growth rate and reaching 19.7% of GDP by 2031.

This favorable demographic and spending trend is captured in the following chart:

Another key trend supporting CHCT’s strategy is the ongoing shift from inpatient to outpatient care. Outpatient visits per 1,000 have grown 30.3% from 1999-2021, while inpatient admissions per 1,000 have declined 19.3%, driven by advances in clinical science, technology, and shifting consumer preferences.

Acquisition Pipeline & Growth Strategy

CHCT’s annual investments have fluctuated over the years, peaking at $152.0 million in 2019 before dropping to $36.0 million in 2025. However, the company has outlined a robust investment pipeline that includes:

- One property acquired after June 30, 2025, for $26.5 million, which is 100% leased until 2040

- Six properties under definitive purchase agreements with an expected cost of $146.0 million and anticipated returns of 9.1% to 9.75%

- A term sheet signed for dialysis clinic funding up to $60.0 million with expected returns of 9.5%

The company’s portfolio includes a diverse range of healthcare facilities, as shown in these representative properties:

Balance Sheet & Risk Management

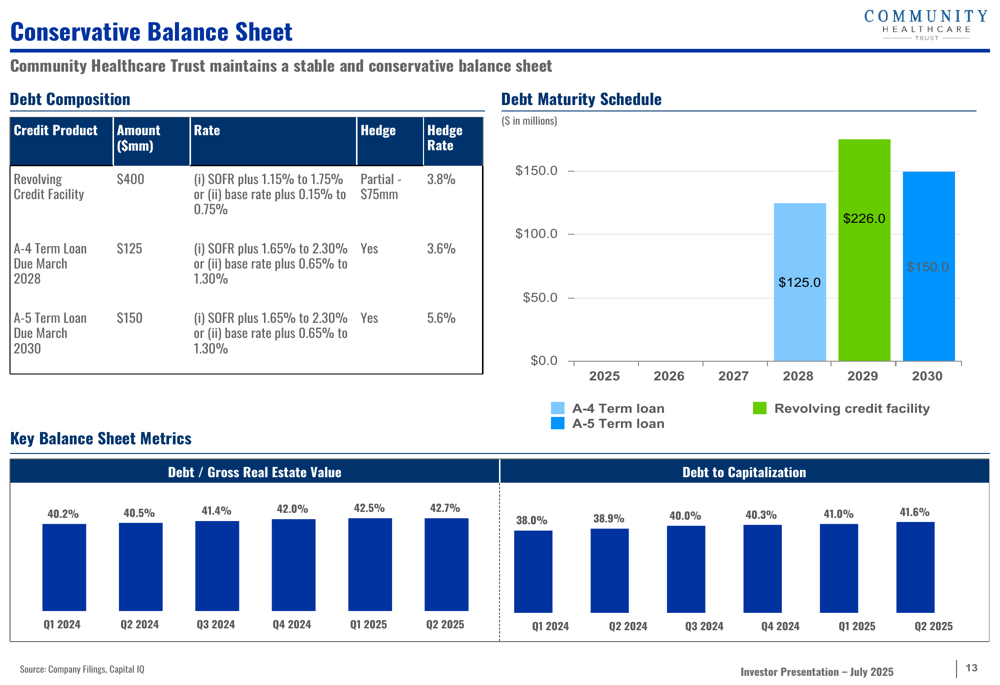

CHCT maintains a conservative balance sheet with a debt structure that includes a $400 million revolving credit facility, a $125 million term loan due March 2028, and a $150 million term loan due March 2030. The company’s debt to gross real estate value ranges from 40.2% to 42.7% between Q1 2024 and Q2 2025.

The debt maturity schedule is well-staggered, as illustrated below:

Risk management is further enhanced through lease diversification. With a weighted average lease term of 6.6 years, CHCT has staggered lease maturities to continuously adjust rental rates. Approximately 30.1% of annualized lease revenue extends beyond 2034, providing long-term stability.

Management Commentary & Outlook

During the Q1 2025 earnings call, CEO Dave DePuy highlighted the company’s cautious approach to equity raises, stating, "We are not excited raising equity at these prices." This comment reflects management’s awareness of the current valuation challenges despite the company’s long-term performance record.

The management team’s interests are aligned with shareholders, as each named executive officer has elected to take 50% of their salary, bonus, and annual incentive compensation in stock with up to 8-year cliff vesting.

Looking forward, CHCT plans to close on new inpatient rehab facilities in Q3 and Q4 2025, with additional property acquisitions anticipated. Analysts expect the company to return to profitability this year, with an EPS forecast of $0.25 for FY2025 and revenue growth of 6%.

The company’s unique value proposition remains focused on capitalizing on the attractive healthcare market through smaller, off-market acquisitions, disciplined growth, portfolio diversification, and maintaining a conservative balance sheet—all while ensuring strong shareholder alignment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.