Gold prices jump to near 3-week high amid US shutdown progress

Introduction & Market Context

Consensus Cloud Solutions, Inc. (NASDAQ:CCSI) presented its third quarter 2025 preliminary and unaudited results on November 5, 2025, revealing a company navigating divergent segment performance while maintaining overall stability. The stock responded positively to the results, rising 3.45% in aftermarket trading to close at $28.99, reflecting investor confidence in the company’s strategic direction.

The cloud services provider, known for its eFax solutions, demonstrated its ability to leverage corporate segment growth to counterbalance ongoing challenges in its Small Office/Home Office (SoHo) business. This balanced approach has allowed Consensus to maintain flat year-over-year revenue while generating substantial free cash flow.

Quarterly Performance Highlights

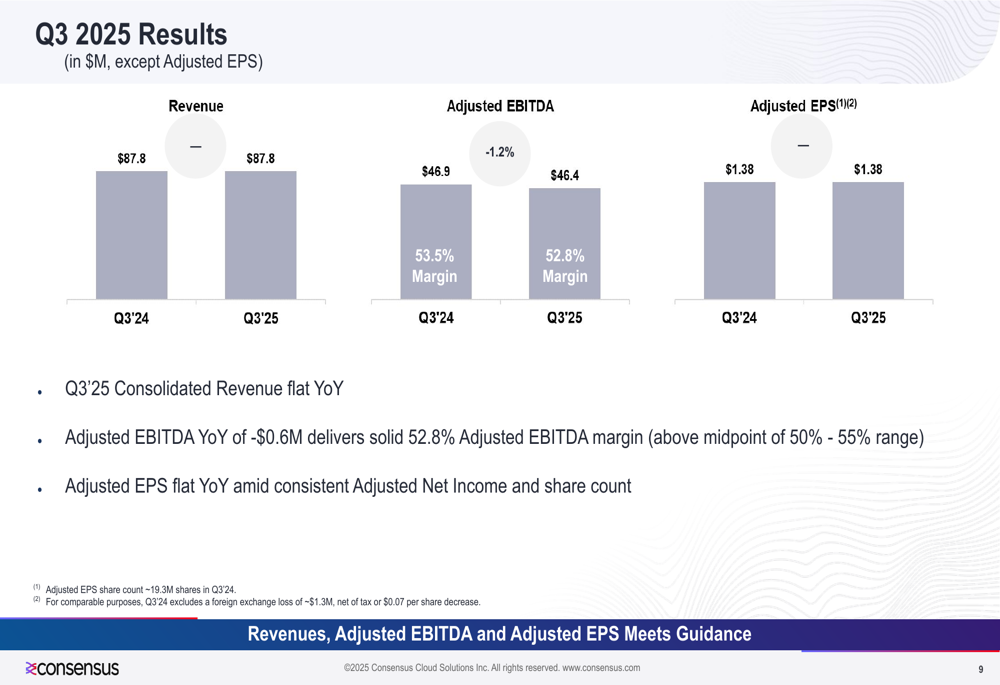

Consensus Cloud Solutions reported consolidated revenue of $87.8 million for Q3 2025, unchanged from the same period last year. Adjusted EBITDA reached $46.4 million, representing a slight decrease of 1.2% year-over-year, but still delivering a robust margin of 52.8%. Adjusted earnings per share remained flat at $1.38, exceeding analyst expectations of $1.33.

As shown in the following consolidated results:

The company’s performance demonstrates resilience in maintaining profitability despite segment-specific challenges. The adjusted EBITDA margin of 52.8% fell within the higher end of the company’s target range of 50-55%, indicating effective cost management and operational efficiency.

Segment Performance Analysis

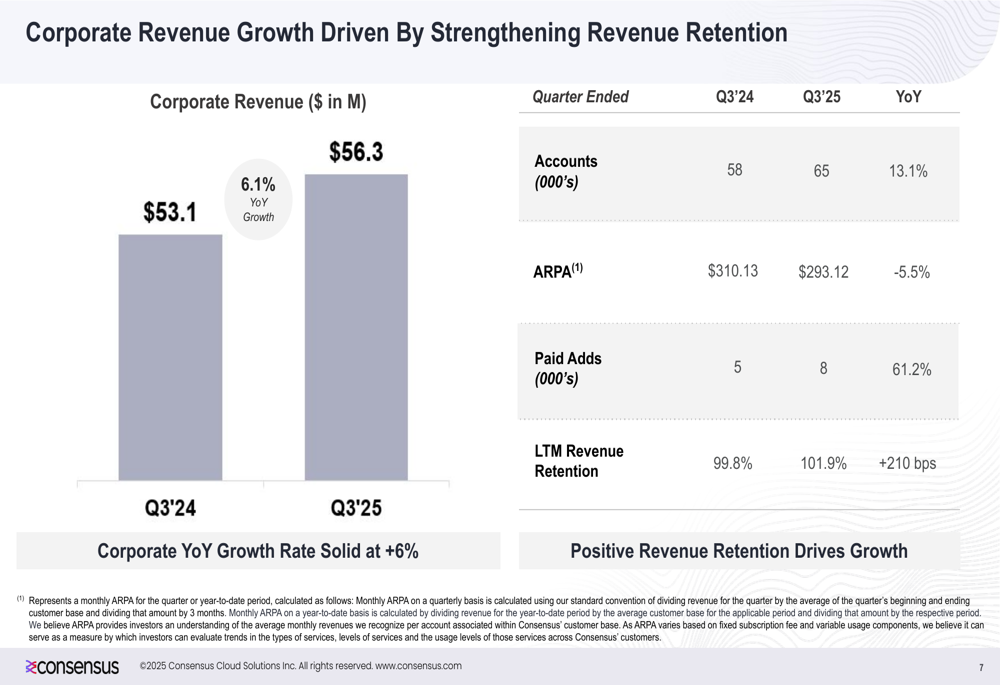

The corporate segment emerged as the growth driver for Consensus in Q3 2025, with revenue increasing by 6.1% year-over-year to $56.3 million. This growth was supported by a 13.1% expansion in the corporate customer base, which reached 65,000 accounts, and an improved revenue retention rate of 102%.

The following chart illustrates the corporate segment’s performance:

The corporate business benefited from record revenue, usage, and account base, along with sustained high revenue retention rates. The company reported over 6,700 e-commerce offerings through eFax Protect and corporate upsells during the quarter, demonstrating effective cross-selling initiatives.

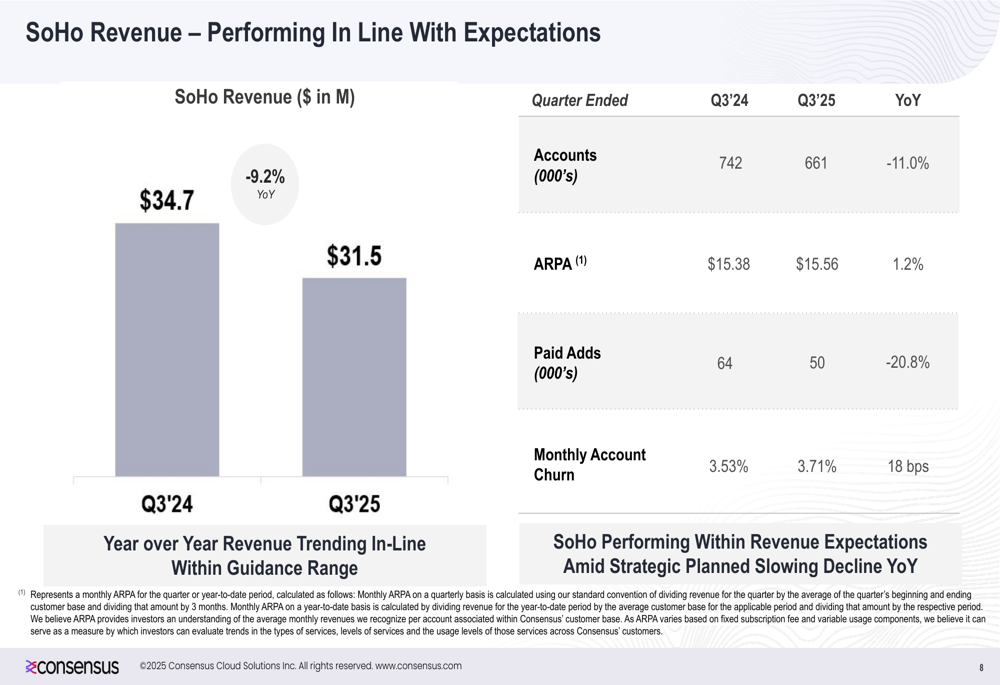

In contrast, the SoHo segment continued its expected decline, with revenue decreasing by 9.2% year-over-year to $31.5 million. However, the company noted this represented a slowing rate of decline compared to previous quarters, suggesting that stabilization efforts are yielding results.

The SoHo segment metrics show the managed decline:

Despite the revenue decrease, Consensus maintained its focus on profitability in the SoHo segment. The company reported a slight improvement in monthly account churn, which decreased to 3.71% in Q3 2025 from 3.84% in Q2 2025. Average revenue per account (ARPA) increased by 1.2% year-over-year to $15.56, indicating successful monetization of the existing customer base.

Cash Generation and Capital Allocation

One of the most impressive aspects of Consensus Cloud Solutions’ Q3 results was its strong cash generation. The company reported free cash flow of $44.4 million, representing a substantial 32% increase from $33.6 million in the same period last year. This robust cash flow supported the company’s strategic capital allocation initiatives.

The following slide details the company’s cash generation and capital deployment:

Consensus maintained approximately $98 million in cash and cash equivalents at the end of the quarter, generating around $0.8 million in interest income. The company continued its share repurchase program, buying back 121,000 shares for approximately $2.7 million during Q3 2025, bringing the program-to-date total to 1.8 million shares for $47.1 million.

The company also made significant progress in debt reduction, calling $200 million of its 6.0% Notes at par on October 15, 2025, using a combination of a $150 million delayed draw term loan and $50 million from its revolving credit facility. The remaining $34 million of 6% Notes are scheduled to be called at par by mid-November 2025, resulting in interest rate savings of 10 to 35 basis points.

Forward Guidance

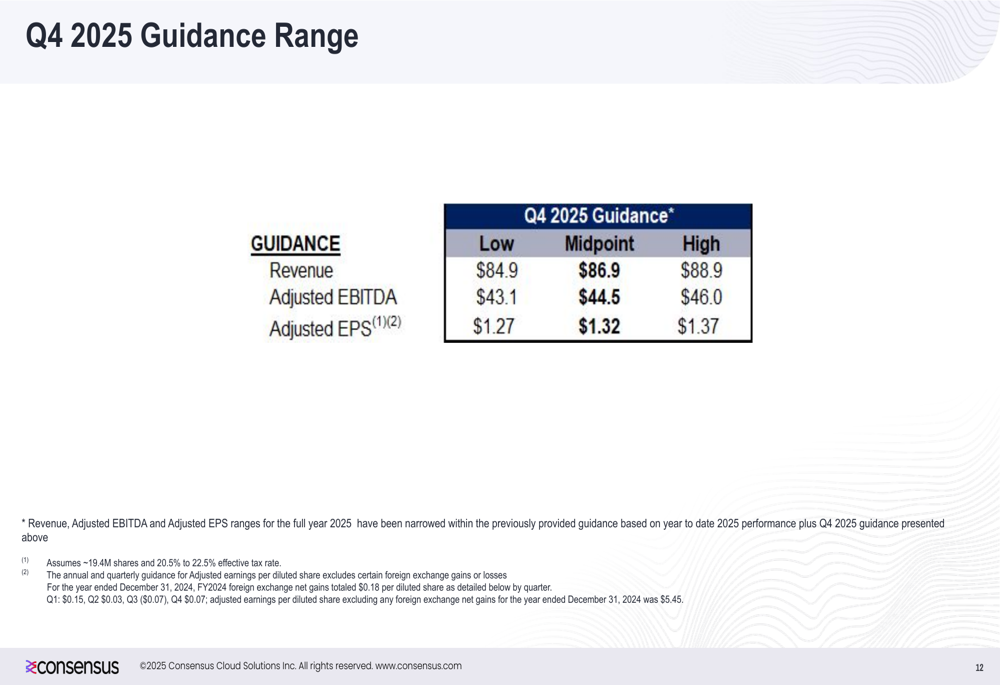

Looking ahead to Q4 2025, Consensus Cloud Solutions provided guidance that suggests continued stability with potential for modest growth. The company expects revenue between $84.9 million and $88.9 million, with adjusted EBITDA ranging from $43.1 million to $46.0 million and adjusted earnings per share between $1.27 and $1.37.

The detailed guidance ranges are presented below:

The company also narrowed its full-year 2025 guidance ranges based on year-to-date performance and the Q4 outlook. Management’s guidance assumes approximately 19.4 million shares outstanding and an effective tax rate between 20.5% and 22.5%.

Strategic Initiatives

During the earnings call, CEO Scott Turicchi characterized Q3 as "another solid quarter" with a slight increase in revenue. The company continues to focus on innovation with its AI product Clarity and the expansion of its eFax Protect service.

Chief Revenue Officer Johnny Hecker emphasized that "Healthcare remains at the center of our strategy," highlighting the company’s focus on industry-specific solutions. The company also sees significant growth potential in its VA platform, projecting revenue to increase from the current $5 million to $10-20 million over the next 2-3 years.

The strategic focus on the corporate segment appears to be yielding results, with the 13.1% year-over-year growth in corporate accounts and 6.1% revenue growth demonstrating the effectiveness of the company’s enterprise-focused approach. Meanwhile, the managed decline of the SoHo business is proceeding according to plan, with profitability remaining the primary focus for this segment.

Conclusion

Consensus Cloud Solutions’ Q3 2025 presentation reveals a company effectively managing the divergent trajectories of its business segments. The growth in the corporate segment, combined with the controlled decline of the SoHo business, has enabled the company to maintain stable overall revenue while generating substantial cash flow.

The company’s strong cash position and strategic capital allocation, including debt reduction and share repurchases, provide financial flexibility for future investments and shareholder returns. With a clear focus on healthcare and enterprise solutions, Consensus appears well-positioned to continue leveraging its corporate segment growth to drive long-term value.

As the company heads into the final quarter of 2025, investors will be watching closely to see if the corporate segment’s momentum can accelerate further while the SoHo segment continues its stabilization, potentially setting the stage for overall revenue growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.