Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

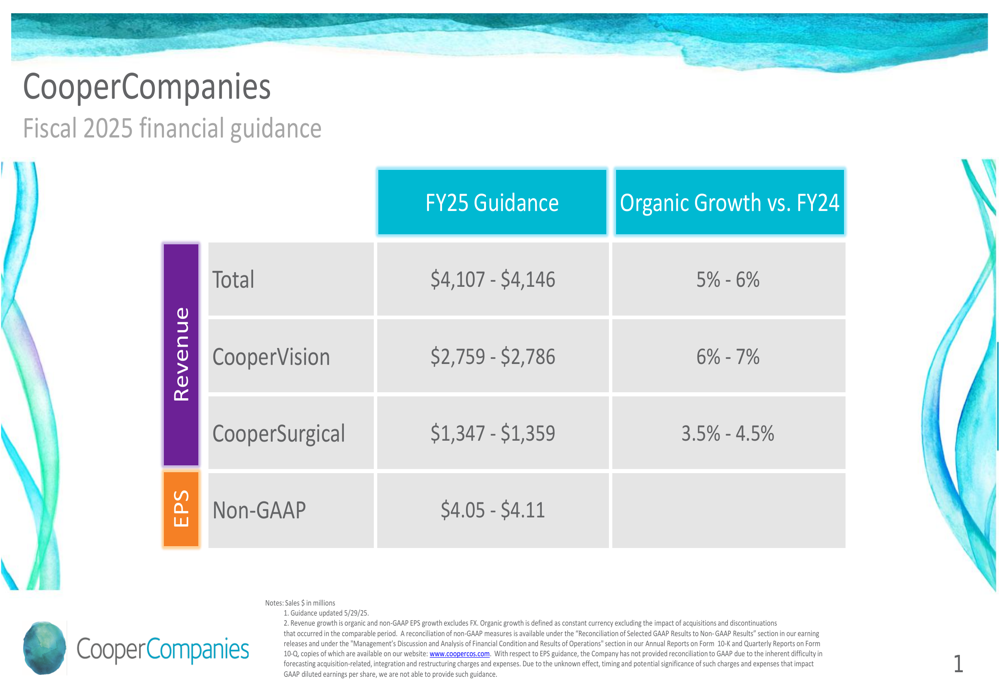

Cooper Companies Inc . (NYSE:NASDAQ:COO) released its fiscal year 2025 financial guidance on May 29, 2025, projecting modest growth across its business segments despite facing headwinds in key markets. The guidance comes as the medical device company’s stock has fallen sharply, dropping 14.64% to $68.25, well below its 52-week high of $112.38.

The presentation follows Cooper’s recent Q2 2025 earnings report, where the company beat expectations with EPS of $0.96 and revenue of $1,002 million, but still saw its stock decline amid concerns about slowing growth in contact lens and fertility markets.

FY25 Guidance Overview

Cooper Companies projects total revenue for fiscal year 2025 to reach between $4,107 million and $4,146 million, representing organic growth of 5-6% compared to fiscal 2024. This guidance is slightly below the $4.11-$4.15 billion range mentioned during the company’s recent earnings call, potentially reflecting further adjustments to market expectations.

The company’s non-GAAP earnings per share is expected to land between $4.05 and $4.11, consistent with previous projections of 10-11.5% growth. However, as noted in the recent earnings call, tariffs are anticipated to impact next fiscal year’s earnings by approximately 3%.

As shown in the following comprehensive guidance breakdown:

Segment Performance Expectations

The guidance reveals divergent growth trajectories for Cooper’s two main business segments. CooperVision, the company’s contact lens division, is projected to generate revenue between $2,759 million and $2,786 million in FY25, with organic growth of 6-7% compared to FY24. This segment continues to be the stronger performer, likely driven by products such as daily silicone hydrogel lenses and myopia management solutions that showed significant growth in recent quarters.

Meanwhile, CooperSurgical, which focuses on women’s health and fertility products, is expected to deliver more modest growth of 3.5-4.5%, with projected revenue between $1,347 million and $1,359 million. This tempered outlook aligns with comments from the recent earnings call about softness in the fertility market, which could be constraining the segment’s growth potential.

Market Reaction & Analyst Perspectives

The market’s reaction to Cooper’s guidance has been decidedly negative, with the stock continuing its downward trajectory that began after the Q2 earnings report. Despite beating earnings expectations, investors appear concerned about the company’s growth trajectory, particularly given the reduced expectations for contact lens and fertility markets mentioned during the earnings call.

The 5-6% overall organic growth projection, while solid, represents a moderation compared to the 7% organic growth reported in Q2 2025. This deceleration, combined with external pressures such as the anticipated 3% earnings impact from tariffs, has likely contributed to investor caution.

Forward-Looking Statements

Cooper Companies’ guidance explicitly notes that revenue growth figures are organic and exclude foreign exchange impacts. The company defines organic growth as constant currency excluding the impact of acquisitions and discontinuations that occurred in the comparable period.

The presentation also acknowledges the difficulty in forecasting acquisition-related charges and expenses, which is why a reconciliation to GAAP for EPS guidance has not been provided. This suggests the company may be keeping its options open for potential M&A activity in the coming fiscal year.

During the recent earnings call, CEO Al White emphasized the company’s continued market share gains and operational efficiency improvements, stating, "We continue to execute well, including taking share, delivering leverage, launching products, and completing capacity expansion projects." However, the more modest growth projections in the FY25 guidance may indicate a more challenging operating environment ahead.

The combination of channel inventory pressures, increased R&D expenses, and tariff impacts mentioned in the earnings call presents multiple headwinds that Cooper Companies will need to navigate as it works to deliver on its FY25 financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.